Understanding Mezzanine Capital

When companies try to raise funds from the market, there are quite a few channels they can opt for; one such avenue is receiving mezzanine capital. Mezzanine capital is a hybrid form of funds that lies in between pure equity and pure debt financing of a corporation’s capital structure. It allows investors rights to convert into equity interest if the company defaults. Some experts call it ‘cheap equity’.

Companies opt for mezzanine capital as a way out when either they have exhausted their borrowing capacity or want to preserve their ability to raise funds through debts in the future. For immediate capital requirements, mezzanine capital remains a choice for companies. This type of funding is perceived expensive since companies need to pay out a higher interest rate than funds borrowed from the bank. It is a costly debt; also less dilutive.

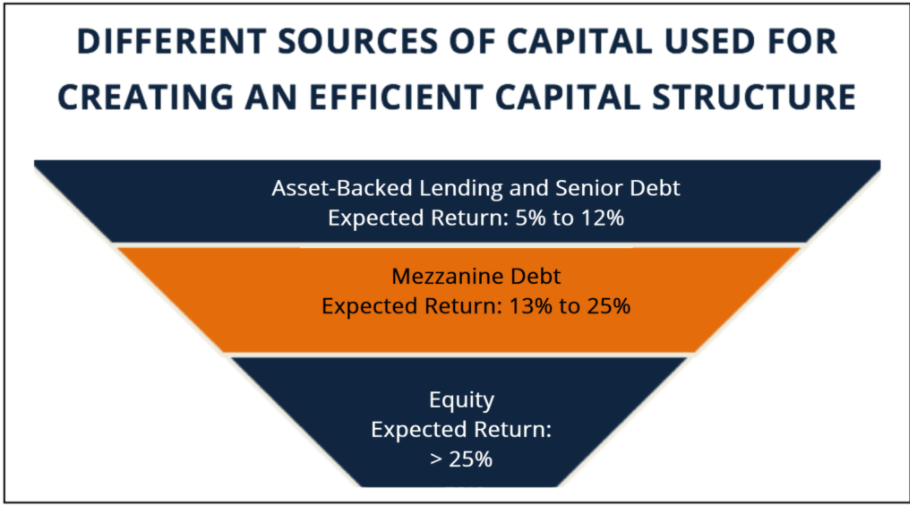

If you place mezzanine finance on a capital structure pyramid, it will look like below.

Source: https://corporatefinanceinstitute.com/resources/knowledge/finance/mezzanine-fund/

Mezzanine capital is a way for companies to raise money for specific projects, like expansion, or acquisition. Hence, this type of funding is common among matured companies than startups and young corporate.

It is typical to associate mezzanine funds with acquisitions and buyouts because it allows companies to prioritise new owners before the existing bondholders in case of bankruptcy. Among the many features of mezzanine debts, it has embedded equity instruments attached called ‘warrants’. It gives better control over the bondholders and increases the value of subordinated debt.

The Truth Behind Mezzanine Capital

Mezzanine capital enhances a company’s ability to borrow from the market. It is a form of junior debt that comes with added flexibility. It is either ‘subordinated debt’ or ‘preferred equity’ with a promise of fixed dividend or coupon payment and some participation rights in the common equity of the firm. But it isn’t dilutive like equities.

Points To Remember

- Offers easy access to market capital, especially when a company is looking for immediate financing for a project or acquisition for a short-to-medium term period

- Mezzanine funding bridges the gap between debt funds and equity capital

- It is the highest-risk debt, often more expensive than buying senior debt

- The mezzanine capitalis more patient – carrying longer tenor to maturity, typically 7 to 8 years

- Typically offers a higher rate of return, between 15 to 20 percent, but no amortisation benefit before maturity

It is typical for companies to consider mezzanine funds as short term financial solution. Because of the high cost of borrowing, companies eventually replace it with cheaper senior debt.

Mezzanine Funding And Rate Of Return

One of the main reasons behind the interest in mezzanine funding is a higher rate of return, typically 15 to 20 percent. Since it is an unsecured form of borrowing and subordinate to all other forms of debt, it is considered riskier. The return on mezzanine funds comes from five sources.

- Cash interest:The periodic cash interest payment on mezzanine funds can be both secured or unsecured linked to a base rate like LIBOR or CRR.

- Payable kind of interest:The interest gets added to the principal and paid on maturity. But no cash interest is paid.

- Ownership:It allows mezzanine lenders to convert their debt into equity or to ownership, in case of default.

- Participation payout:The lender can choose to take a stake in the company’s performance.

- Arrangement fee:The arrangement fee is paid upfront to the lenders as a processing fee for the fund.

Advantages And Disadvantages Of Mezzanine Funding

There are quite a few on both sides.

On the flip side, the mezzanine capital is costlier than senior debt. Owners pay out more in interest payment the longer it handles mezzanine funds. For the lenders, the risk is higher. Mezzanine debt is a subordinate form of debt, means in case of liquidation, mezzanine lenders come secondary to senior investors. If there is no asset left after paying senior lenders, mezzanine investors will lose out.

Why do companies then raise mezzanine funds? Because the advantages are quite a few. It is more flexible - often allowing owners to retain majority control of the company. Secondly, it is less expensive to direct equity issuance.

Companies avail mezzanine funds to finance long-term growth with an extended tenor of seven to eight years on average.

Conclusion

The risk with mezzanine funding is high for both the borrower and the lender. Companies show mezzanine funds on the equity side of the balance sheet. However, to raise mezzanine funds, the firm must have a good debt repayment history and a feasible expansion plan through IPO. As a result, mezzanine funding is often used by companies that are making a profit in the industry.

Learn Free Stock Market Course Online at Smart Money with Angel One.

Explore the Share Market Prices Today

| Tata Steel share price | Adani Power share price |

| PNB share price | Zomato share price |

| BEL share price | BHEL share price |

| Infosys share price | ITC share price |

| Jio Finance share price | LIC share price |

The Indian share market plays a central role in the country's economy by enabling capital formation, wealth creation, and corporate growth. For investors, it offers an opportunity to grow money over time by owning equity in some of the country's most successful companies. Angel One brings the share market to your fingertips with a powerful trading platform, ARQ Prime smart recommendations, IPO access, and research-backed insights. Whether you are starting small or building a long-term portfolio, the share market can be a powerful vehicle for wealth.