A bonus issue and stock split are corporate actions that increase the number of shares while reducing the share price, without changing the total investment value. While both reduce the share price and improve accessibility, they work differently in terms of purpose and impact. Understanding how these two concepts function helps investors interpret changes in shareholding and make better investment decisions.

Key Takeaways

-

A bonus issue gives free shares from the company's reserves, while a stock split divides existing shares.

-

The share price declines in both cases, but the total investment value remains unchanged.

-

Face value stays the same in bonus issues, but reduces in a stock split.

-

Bonus issue uses reserves, whereas a stock split does not affect reserves or capital.

What is a Bonus Issue?

A bonus issue is when a company gives additional shares to its existing shareholders at no extra cost, based on a fixed ratio. These shares are issued from the company’s accumulated reserves, which are converted into share capital.

For example, in a 1:1 bonus issue, a shareholder receives one additional share for every share held. While the total number of shares increases, the overall investment value remains unchanged as the share price adjusts proportionately. Companies use bonus issues to capitalise reserves and increase share liquidity.

|

|

Before Bonus Issue |

After Bonus Issue |

||||||

|

Bonus Issue |

No. of shares held |

Share Price |

Face Value |

Value of Investment |

No. of shares held |

Share Price |

Face Value |

Value of Investment |

|

1:1 |

100 |

100 |

10 |

10,000 |

200 |

50 |

10 |

10,000 |

|

1:2 |

100 |

90 |

10 |

9,000 |

150 |

60 |

10 |

9,000 |

By issuing bonus shares, the number of outstanding shares increases, with a proportional decrease in the value of each share, ensuring no change in market capitalization, as shown in the table above. However, the face value of the shares remains unchanged.

Many companies see bonus issues as a viable alternative to dividends. Bonus issues are payments made to shareholders from a company’s net reserves, while dividends are paid out from net profits.

Dividends are paid to shareholders in cash, credited to your registered bank account (linked to your Demat account), while bonus issues are paid in additional shares. As a result, it may increase investor interest, but it does not increase the stock's overall value.

adCX

Advantages and Disadvantages of Bonus Shares

Advantages of Bonus Shares

-

Tax Benefits

Investors generally do not pay tax on bonus shares at the time of receipt, but tax may apply when they are sold. This can be particularly appealing for long-term shareholders aiming to amplify their investments without incurring immediate tax liabilities. For capital gains calculation, the cost of acquisition of bonus shares is considered ₹0.

-

Investment Growth

For long-term investors, bonus shares provide an effective way to increase their holdings in a company. This can be especially beneficial for those looking to grow their investment over time.

-

Boosts Investor Confidence

The issuance of bonus shares may indicate positive company performance and can influence investor sentiment. It demonstrates that the company is reinvesting its cash reserves into business expansion, signaling a positive outlook.

-

Higher Future Dividends

Holding a larger number of shares through bonus issues means that investors could receive higher dividends in the future, provided the company declares dividends.

-

Positive Market Signals

Issuing bonus shares may be viewed as a sign of strong reserves, but it does not guarantee future growth. This can improve the company’s reputation and attract more investors.

Disadvantages of Bonus Shares

-

Increased Volatility

The announcement and issuance of bonus shares can lead to increased market speculation and sentiment changes, contributing to greater stock price volatility.

-

Capital Allocation

Allocating additional shares involves converting existing reserves into share capital. This capital allocation might have otherwise been distributed as dividends to shareholders.

-

Unchanged Profits

Despite the increase in the number of shares, the company's overall profit remains unchanged. This results in a proportional decrease in earnings per share (EPS), which might not be favourable for all investors.

What is a Stock Split?

A stock split is an action taken in which a company divides its existing shares into multiple shares to boost the liquidity of shares. Split is usually undertaken when the stock price is high, making it pricey for investors to acquire. It brings down the share price as the number of shares increases. The market cap of the firm and the value of each shareholder’s investment stay unchanged after a stock split.

Like bonus issues, the price gets decreased by the ratio. To illustrate,

|

|

Before Split |

After Split |

||||||

|

Stock split |

No. of shares held |

Share Price |

Face Value |

Value of Investment |

No. of shares held |

Share Price |

Face Value |

Value of Investment |

|

1:2 |

10 |

900 |

10 |

9000 |

20 |

450 |

5 |

9000 |

|

1:5 |

10 |

900 |

10 |

9000 |

50 |

180 |

2 |

9000 |

However, the face value of the share changes with the stock split. If the face value of a stock is ₹10, and the stock is split in the ratio 1:2, the face value of the stock after the stock split becomes ₹5.

Advantages and Disadvantages of Stock Split

Advantages of Stock Split

-

Increase in outstanding shares: A stock split significantly increases the total number of outstanding shares, though the company's market capitalisation remains the same. This does not change the company's overall value but makes the stock more accessible.

-

Reduced share price: A stock split makes the stock more affordable for individual investors by proportionally reducing the share price. This can attract a broader range of investors who might have been previously priced out.

-

Enhanced accessibility: With more shares available at a lower price, acquiring and selling shares is easier. This increased liquidity can make the stock more attractive to retail and institutional investors.

-

Simplified portfolio management: The lower share price and higher share volume make it easier for investors to diversify and rebalance their portfolios. More shares at a lower price provide flexibility in managing investments.

-

Avoiding dilution: A stock split does not involve issuing new shares and maintains the ownership percentage of existing shareholders.

Disadvantages of Stock Split

-

Cost and regulatory compliance: Conducting a stock split involves procedural and compliance requirements under applicable regulations. This can be a resource-intensive process for the company.

-

No impact on company value: A stock split does not affect the company’s fundamental position. It does not add any intrinsic value and is merely an accounting adjustment to the number of shares and their price.

-

Potential for increased volatility: The new, lower share price post-split may attract more investors, increasing the stock’s accessibility. This influx can lead to higher volatility as more investors buy and sell the stock.

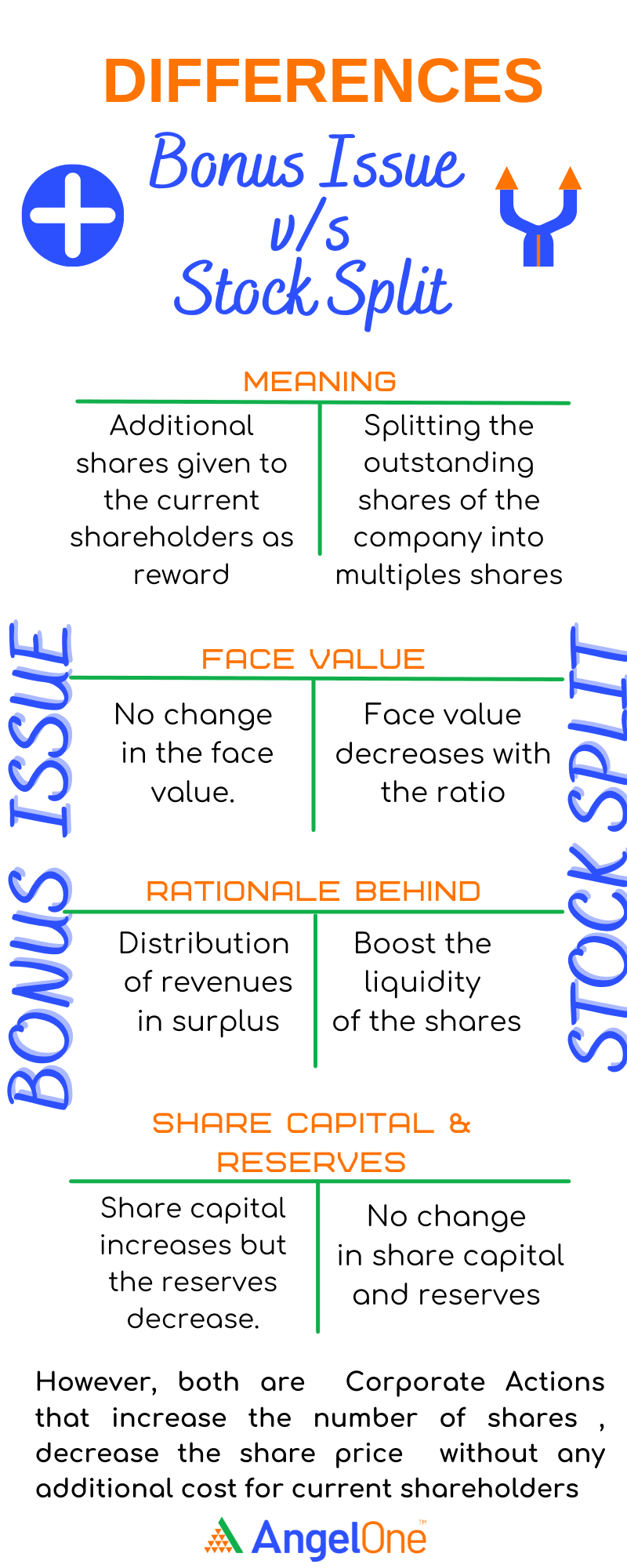

Differences Between Bonus Issue and Stock Split

The difference between bonus share vs stock split lies in how shares are issued, their impact on face value, and how company reserves are treated. The table below explains these differences in a simple way:

|

Basis |

Bonus issue |

Stock split |

|

Meaning |

Additional shares are given to existing shareholders free of cost in a fixed ratio. |

Existing shares are divided into multiple shares without issuing new ones. |

|

Face value |

Remains unchanged after the bonus issue. |

Reduces according to the split ratio (e.g., ₹10 to ₹1 in 1:10 split). |

|

Purpose |

Used to reward shareholders and capitalise company reserves. |

Used to make shares more affordable and improve liquidity. |

|

Company reserves |

Reserves decrease as they are converted into share capital. |

No impact on reserves or share capital. |

|

Impact on share price |

Share price falls proportionately after the bonus issue. |

Share price reduces based on the split ratio. |

|

Investment value |

Total investment value remains unchanged. |

Total investment value remains unchanged. |

This comparison helps in understanding the difference between bonus and split clearly, especially in terms of their purpose and financial impact.

Why Should You Care About Bonus Issues and Stock Splits

Bonus issues and stock split may look beneficial since you receive more shares, but they do not increase your total investment value by themselves. Still, they play an important role for investors.

-

Market Perception

A lower share price can make stocks seem more affordable, which may attract more buyers.

-

Improved Liquidity

An increase in the number of shares makes trading easier in the market.

-

Business Signal

Bonus issues often indicate strong reserves, while stock splits usually aim to widen investor participation.

-

Tax Treatment

Bonus shares and stock splits are not taxed at the time of receipt. There is a tax obligation only when these shares are sold, and the gain is categorised as capital gains.

Stock splits involve a proportional adjustment to the acquisition cost, unlike bonus shares, which have a zero acquisition cost for tax purposes and are taxed as LTCG or STCG.

The gains are taxed as LTCG at 12.5% if the holding period is more than 12 months and the gains exceed ₹1.25 lakh. On the other hand, if the holding period is less than 12 months, the gains are treated as STCG and taxed as 20%.

Conclusion

Understanding the difference between bonus and split helps investors interpret how corporate actions affect their holdings. Both increase the number of shares and reduce the share price, but they do not change the overall investment value.

A bonus issue involves converting company reserves into share capital, while a stock split only divides existing shares by reducing the face value. These actions mainly improve liquidity and accessibility in the market. Knowing how they work allows investors to better assess their impact and make informed investment decisions.