How Does LTCG Tax Impact on Equity Mutual Funds?

One of the significant changes in the Union Budget 2018 was the introduction of tax on long term capital gains (LTCG) at the rate of 10% above the profit level of Rs.1 lakh per year. For example, if your long term capital gains for the year 2018-19 are Rs.145,000/- then your LTCG up to Rs.100,000 will be exempt. On the additional LTCG of Rs.45,000/- tax at 10% (Rs.4500) will have to be paid. That means your long term capital gains on equities, which will be tax-free till March 31st 2018, will be taxable after that. Here are 5 things you need to know about the LTCG tax that was imposed in the Union Budget 2018…

5 things you need to know about the tax on LTCG on equities…

While the tax looks like a fairly straightforward flat tax on profits exceeding a threshold of Rs.1 lakh per annum, there are some nuances that you need to understand here…

- 1. The tax on LTCG will apply to direct equities and equity mutual funds. If the sum of the profits on equities and equity funds exceeds Rs.1 lakh then you will have to pay tax at 10% on the excess profit above Rs.1 lakh. For that purpose you will be tracked through your PAN number to which both your trading account and your mutual fund folios are mapped.

- 2. When we talk of profits on equity here, we are referring to net profits (net of losses). For the year 2018-19 if you are having capital gains of Rs.135,000 on your trading account and if you are having losses of Rs.40,000 on your equity mutual funds then you net LTCG will be Rs.95,000/- Since this below the threshold of Rs.1 lakh, you will not be required to pay any LTCG tax.

- 3. Since losses can be set off against profits, it logically follows that losses on equity and losses on equity funds can also be carried forward for a period of 8 years and written off against future long term capital gains. This will help you to reduce your tax payable.

- 4. It needs to be remembered that the LTCG tax is a flat tax. That means, the benefit of indexation will not be available while calculating the LTCG tax. For example, whether you make an LTCG of Rs.2 lakh at the end of 2 years or an LTCG of Rs.5 lakh after 6 years, the LTCG tax will be charged on the profits without giving you any benefit of indexation of acquisition price.

It may be recollected that when the securities transaction tax (STT) was introduced in 2004, it was introduced in lieu of the tax exemption granted to LTCG. However, this 10% tax on LTCG above Rs.1 lakh will be payable by you in addition to the STT that you will be anyway paying on your equity market transactions.

How will the tax on LTCG impact you?

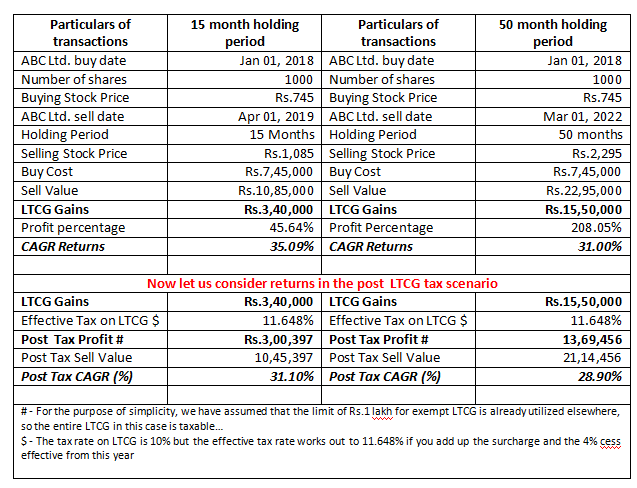

Obviously, the attractiveness of equities as an asset class will reduce. Let us understand how big the difference will be after you consider the impact of tax on LTCG under two different holding period assumptions. But, how big will the impact of this LTCG tax actually be?

If you are really worried about the impact of the LTCG tax, you can afford to relax! We have considered two scenarios where an investor makes LTCG after a holding period of 15 months and 50 months. In the first case, the CAGR return is lower by 4% after tax whereas in the latter case, the CAGR returns falls by just about 2% post tax. So as your holding period gets longer, the actual impact of this LTCG tax on your CAGR returns will be quite negligible. So, to answer your big query, it will not make any substantial difference to your long term financial plan.

Here are 3 things for you to remember about LTCG Tax on equities…

- The impact on the CAGR returns over longer periods of time will actually become negligible. However, you can look at one of the two options with respect to your financial plan. You can either look to downsize some of your wealth creation targets and plan accordingly. Alternatively, you can start saving and investing more so that your eventual target corpus still remains the same in post-tax terms.

- There is a cooling period till March 31st 2018 for the implementation. Till then, whatever long term profits you book will be tax-free. You can plan your profit booking accordingly, so as to monetize as much of your book profits as possible.

- You will be better off holding equities for much longer periods, as is evident from the above example. Over longer periods the impact of tax on CAGR returns is much lower. Alternatively, you can look to split your profits across financial years to circumvent the Rs.1 lakh annual limit.

Read More About Tax on Mutual Funds

Published on: Mar 5, 2018, 12:00 AM IST

We're Live on WhatsApp! Join our channel for market insights & updates

- Income Tax Department Flags Wrong Tax Benefit Claims Through Data Analytics, CBDT Tightens Compliance Checks

- Will the Taxation (Amendment) Bill 2026 Change REIT Tax Benefits for Investors?

- ITR Revised Return: Can You Correct Mistakes After Filing Your Income Tax Return?

- Missed the July 31, 2026, ITR Filing Deadline? Here's What Happens Next and How You Can Still File

- Taxation And Other Laws Amendment Bill 2026 Proposes Relief for Offshore Funds and Key Sector Tax Changes

Related Articles

Enjoy ₹0 Account Opening Charges

Get the link to download the App