In a recent filing with the US Securities and Exchange Commission (SEC), Infosys has highlighted increased shareholder activism as a major risk to the company’s market value. The reference may or may not have been to Mr. Murthy’s recent disapproval on management pay and corporate governance, but that is off the point. The point is that companies in India need to be increasingly open to shareholder activism. Remember, Murthy is not a minor shareholder of Infosys because he along with co-promoters owns nearly 13% of Infosys. In a way the Infosys DNA has been synonymous with the DNA of its promoters and therefore they surely have a point to make. For those who are still sceptical, it would be worthwhile to peruse this famous case of Benjamin Graham, which was featured in the Harvard Business Review.

The famous case of Benjamin Graham…

To people even remotely connected with stock markets and investments, Ben Graham needs no introduction. Suffice to say that he is considered the father of value investing and Warren Buffett looks up to Graham as his mentor and Guru. But for now, back to the case of shareholder activism!

Back in 1926, Ben Graham was a small shareholder in the Northern Pipeline Company. Graham found out from the annual report that the company held millions in railroad bonds and other securities. Graham was of the view that Northern Pipeline should sell off these bonds and distribute the proceeds to shareholders as a special dividend. Over the next 1 year Graham solicited the support of every shareholder holding more than 100 shares of Northern Pipeline and eventually the company had to relent.

The same happened in the case of General Motors. Billionaire shareholder, Ross Perot, urged the company to entirely change its strategy in the mid-1980s to counter the threat of Japanese competition. At that time, GM was sinking billions of dollars into technology and manufacturing facilities but the fact was the Japanese were managing the auto business much better. Not too long ago, it needed the persuasiveness of Carl Icahn to compel Apple to take up a buyback of shares. As the Harvard Business Review pointed out, “When CEOs are focused purely on quarterly earnings you need a larger vision to look at the bigger picture”. That is exactly what Murthy and his team of promoter shareholders are trying to play. But first, what exactly is the challenge at Infosys?

Infosys has underperformed markets by a margin; and that is rankling…

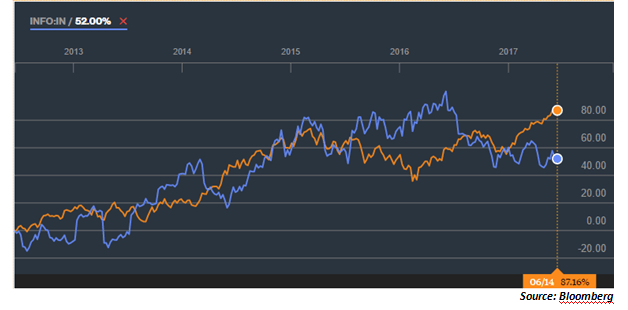

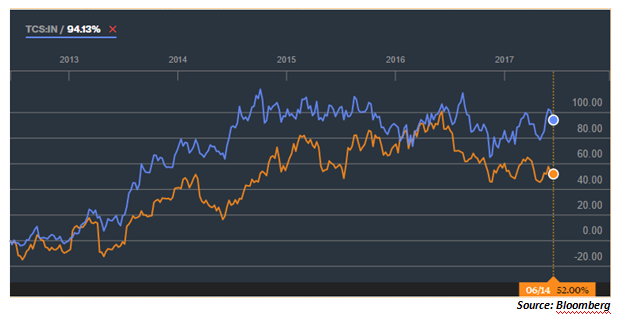

Consider two charts of Infosys stock price performance over the last five years. The irony is that when the stock performance of Infosys is compared with the Nifty and with TCS, the real divergence in performance has come in the last one year. That is also the period when Infosys has been faced with a plethora of challenges. Firstly, the grand plan of achieving $20 billion in revenues by year 2020 has now been put on hold. That obviously means that the company is no longer confident of aggressive growth targets in the light of the global demand scenario. Secondly, the last 1 year has seen a visible contraction in tech spending in the US and European markets as well as a clear shift in spending patterns from erstwhile BFSI focus to a new-age SMAC focus. SMAC focuses on emerging growth areas like social media, mobility, analytics and cloud. Thirdly, the last 1 year is also the period when the differences between the promoter shareholders and the board have come out into the open. Consider the charts below…

The chart above captures the relative performance of Infosys and the Nifty over the last 5 years. The real divergence has been in the last one year when the Nifty and Infosys have diverged by nearly 35%. To get a better apple-to-apple comparison, let us also compare the 5-year performance of Infosys vis-à-vis TCS, the largest and most valuable Indian IT company.

Over the last 5 years, even TCS has outperformed the Infosys stock by 42%. If you look at the returns on Infosys over the last 5 years on a CAGR basis, the annualized returns are hardly 8.75%. That is obviously what rankles the promoters as the company has never reported such a tepid stock market performance over a longer time frame. Coming back to the case of TCS, it has had a few advantages. Firstly, Tata Sons has virtual control over TCS and hence there is unity of command. Secondly, TCS already derives 18% of its annual revenues from SMAC and that gives it a big advantage. Which is the reason shareholder activism becomes important and essential for Infosys!

Why Infosys actually requires Murthy’s shareholder activism…

Globally, there are large investors who act as meaningful activist shareholders. Bill Ackman, Daniel Loeb and Carl Icahn are examples of large shareholders who have the capacity and the will to enforce discipline of performance on corporate managements. In India, there are the proxy advisory firms who do not have the powers to enforce decisions on the management. Domestic mutual funds and FIIs have typically chosen to keep out of shareholder activism and focus purely on ROI of their investments. Financial institutions like LIC have traditionally chosen to maintain stability of management and they have therefore limited their role. It, therefore, just leaves interested shareholders like the original promoters who can play a critical role in guiding the management.

It is ironic that at a time when Infosys requires the guidance and shareholder activism of Murthy more than ever before, the grapevine is rife with rumours of a likely exit by the promoters. One hopes that Murthy continues to play his activist role and the board and the other institutional shareholders take the feedback more as an actionable input. For the sake of Infosys and for the sake of India Inc, this is essential!

Published on: Jun 22, 2017, 12:00 AM IST

We're Live on WhatsApp! Join our channel for market insights & updates

Get the link to download the App