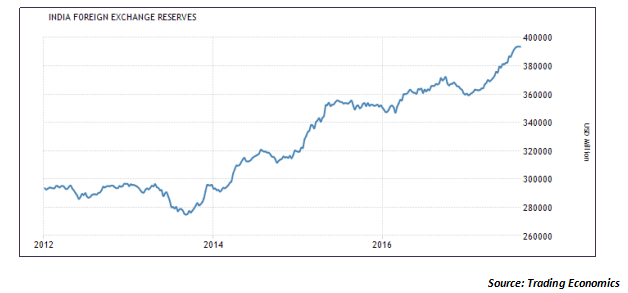

Recently, India’s forex reserves touched an all-time high of $394 billion. In fact, India is already the 8th largest economy in the world in terms of forex reserves and is expected to cross the$400 billion mark by the first week of September. India’s rising forex reserves also represents the shifting oil dividends due to sustained weakness in oil prices.

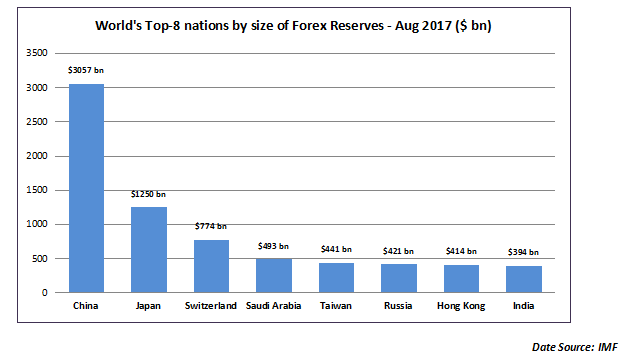

How India ranks in forex reserves among peers?

There is an interesting irony in the chart above. Saudi Arabia used to have forex reserves of over $750 billion prior to 2014. Over the last 3 years Saudi Arabia has depleted over $250 billion worth of forex reserves trying to balance its budget at a time when it was selling oil at below the breakeven rates. This has resulted in the dividends of cheap oil getting transmitted to countries like India. That perhaps explains why India’s forex reserves have surged from $274 billion in 2014 to $394 billion in 2017. There is one more contrast in the top-8 list as depicted in the chart above. The other 7 countries have built their forex reserves largely on the strength of their strong trade related earnings. India runs a large trade deficit of nearly $150 billion per year but this forex reserves are largely driven by FPI and FDI investments.

Remember, Foreign Portfolio Investors have been consistently buying into Indian equities and Indian debt. In fact, Indian debt has been specifically attractive or FPIs as they get the dual benefit of an attractive real rate of return as well as a strong to stable rupee. In fact, the real yield spread between Indian benchmark bond and the US benchmark bond is wide enough to encourage risk-on debt flows into India. Secondly, there is FDI which has picked up momentum in the last 3 years. Last year, India received over $50 billion in FDI making it the largest recipient in the world ahead of China and the US. FDI is relatively stable long-term money as against FPI flows, which is normally classified as hot money. It is this aggressive inflow of FDI and FPI flows that is adding to the forex kitty.

Why the momentum in the Indian forex kitty?

As the chart above captures, the forex reserves have grown from $274 billion in 2014 to $394 billion in 2017. This has been one of the sharpest rallies in the forex kitty in a span of 3 years. So what exactly does the forex kitty consist of? Nearly 90% of India’s forex kitty consists of foreign currency assets which includes holding of bonds that are denominated in dollars, Euros, Pounds, Yen and other hard currencies. As per the latest RBI report, India holds over $135 billion in US treasuries alone. Apart from these foreign currency assets, the forex reserves are also held in the form of gold and special drawing rights (SDR) of the IMF. The total forex kitty we see in the above chart is a combination of all these components.

So what leads to an accretion in forex reserves? While these inflows are responsible for a rising kitty, a key factor is the intervention by the RBI in currency markets. The RBI, since 2014, has tried to maintain a calibrated approach to managing the currency range. Since inflows through FPI and FDI flows have been robust since the beginning of January 2017, the INR has been appreciating and in fact went as high as 63.5/$. A strong rupee is unfavourable to the exporters of goods and services and therefore the RBI intervenes by mopping up the dollars from the market through open market purchases. It is this mopping up of dollars by the RBI to prevent the INR from appreciating that is leading to this consistent build-up in forex reserves.

But what then is the risk of rising forex reserves?

The primary risk of rising forex reserves arises from the fact that this accretion is happening due to the RBI mopping up dollars from the market. When dollars are mopped up by the RBI to prevent the INR from strengthening, there is a proportionate increase in the rupee supply in the financial market. The challenge is that the financial system is already flush with liquidity in the aftermath of demonetization as banks are struggling with a surfeit of high cost deposits but are unable to push credit growth. The latest credit/deposit ratio (C/D ratio) has come in at a low of just 72%. When surplus liquidity cannot be productively allocated to industry, then it becomes inflationary and results in a rise in consumer price inflation and even asset inflation.

The secondary challenge arises from the above situation. The RBI is now forced to sterilize this surplus rupee liquidity through the issue of fresh bonds. And that is where the real problem arises. As Dr. Urjit Patel has stated, the RBI will move the markets from surplus liquidity to neutral liquidity and that will happen through bond sales. On the one hand that keeps the debt markets

overcrowded and crowds out private borrowing. Secondly, the real rate on Indian debt is too high. Considering the 10-year yield at 6.55% and the inflation at around 2%, the government will effectively end up borrowing at a real yield of 4.55%. That is, by far, the highest real yield paid by any government in the developed world and that is the real challenge arising from a swelling forex kitty!

Published on: Sep 4, 2017, 12:00 AM IST

We're Live on WhatsApp! Join our channel for market insights & updates

Get the link to download the App