Initiating coverage | FMCG

December 19, 2011

Tata Global Beverages

BUY

CMP

`84

Poised to perform

Target Price

`97

Tata Global Beverages Limited (TGBL) is an emerging player in the global

Investment Period

12 Months

beverage market. The company has made a strategic shift from being a local tea

Stock Info

company to a global beverage company through various acquisitions and

Sector

FMCG

strategic partnerships with global beverage giants like PepsiCo and Starbucks. As

a result, the company has made an entry into the top 10 global companies list in

Market Cap (` cr)

5,219

the hot drinks category, posing a challenge to global players like Nestlé, Unilever

Beta

1.0

and Kraft Foods. The company’s product portfolio comprises leading global

52 Week High / Low

120/80

brands like Tetley, Eight O’ Clock and local brands like Tata Tea.

Avg. Daily Volume

294,179

Bottomed-out margins; expect a positive surprise: We model in TGBL’s OPM to

Face Value (`)

1

improve by ~150bp over FY2011-13E from 8.6% in FY2011 to ~10.1% in

BSE Sensex

15,391

FY2013E, driven by a shift in the company’s focus from the plantation business to

Nifty

4,613

branded products and rationalization in the operating cost structure. While

Reuters Code

TAGL.BO

TGBL’s focus on volume growth remains intact, selective price increases and

Bloomberg Code

TGBL@IN

stable ad spends will further aid in margin improvement. Also, with the Tea Board

of India estimating higher tea production in 2011 as compared to 2010 (~5%

higher production), we expect auction prices of tea to soften, thereby providing a

Shareholding Pattern (%)

relief to the company from heightened input cost pressure.

Promoters

35.2

Estimate ~40% plus adjusted EPS CAGR over FY2011-13E: We model a ~40%

MF / Banks / Indian Fls

33.4

EPS CAGR over FY2011-13, led by (1) 9% revenue growth and (2) a ~150bp

FII / NRIs / OCBs

9.8

margin improvement. We believe the company is set to outperform the industry’s

Indian Public / Others

21.6

growth, with the help of selective price increases and strong brands like Tata Tea

Premium, Tata Tea Gold, Agni Dust and Kanan Devan.

Key valuation trigger: Despite its leadership position in the Indian packaged tea

Abs. (%)

3m 1yr

3yr

market, No. 2 position in the global tea market and generating ~90% of its total

Sensex

(10.0)

(22.5)

52.7

revenue from branded products, TGBL is trading at 12.2x FY2013E EPS (which is

TGBL

(7.8)

(26.4)

54.8

at a discount to its FMCG peers, trading at 20x-35x FY2013E EPS). Also, on

EV/Sales basis, the stock is trading at 0.6x FY2013E EV/Sales (historical average

of 1x EV/ Sales). Hence, we initiate coverage on the stock with a Buy

recommendation and a target price of `97, based on 14x FY2013E EPS of

`6.9(0.8x FY2013 EV/Sales).

Key financials (Consolidated)

Y/E March (` cr)

FY2010

FY2011

FY2012E

FY2013E

Net Sales

5,784

5,984

6,522

7,110

% chg

19.3

3.5

9.0

9.0

Net Profit

390

254

336

427

% chg

73.2

(34.8)

32.1

27.2

EBITDA (%)

8.9

8.6

9.2

10.1

EPS (`)

6.2

3.4

5.4

6.9

P/E (x)

14.5

26.4

16.6

12.2

P/BV (x)

1.5

1.4

1.4

1.3

RoE (%)

10.4

5.4

8.4

10.2

RoCE (%)

6.2

6.7

8.0

9.6

Sreekanth P.V.S

EV/Sales (x)

0.9

0.8

0.7

0.6

022-39357800 Ext: 6841

EV/EBITDA (x)

10.8

8.9

8.6

8.6

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Tata Global Beverages | Initiating coverage

Investment thesis

Fast emerging global beverage player

Among the top 10 global players in the

TGBL, led by its various acquisitions in recent years, has become a global

hot drinks category, posing a challenge

non-alcoholic beverage company. The company now features among the global

to Nestlé, Kraft Foods and Unilever,

top 10 players list in the hot drinks category.

among others.

Exhibit 1: Top-10 Global players (%Off-trade value) - Hot drinks category

Company

2005

2010

Nestlé SA

15.1

15.2

Kraft Foods Inc.

7.9

7.8

Unilever Group

4.5

4.4

Sara Lee Corp

3.2

3.4

Tchibo GmbH

1.8

1.6

Tata Global Beverages Ltd

-

1.3

Associated British Foods Plc (ABF)

1.4

1.3

JM Smucker Co, The

-

1.2

Strauss Group Ltd

0.1

1.2

Lavazza SpA, Luigi

1.2

1.1

Source: Euromonitor International, Angel Research

Spreading its wings across the globe

TGBL has a very ambitious plan to generate revenue of US$5bn by 2015, which it

may fall short of due to the slow growth in its key categories (tea and coffee) and

slowdown due to the ongoing global as well as local macroeconomic scenario.

The company has a commanding position in the tea and coffee categories in

North America and South Asia. With leadership positions in India, UK and Canada

in the tea market, TGBL has been consistent in maintaining its market share.

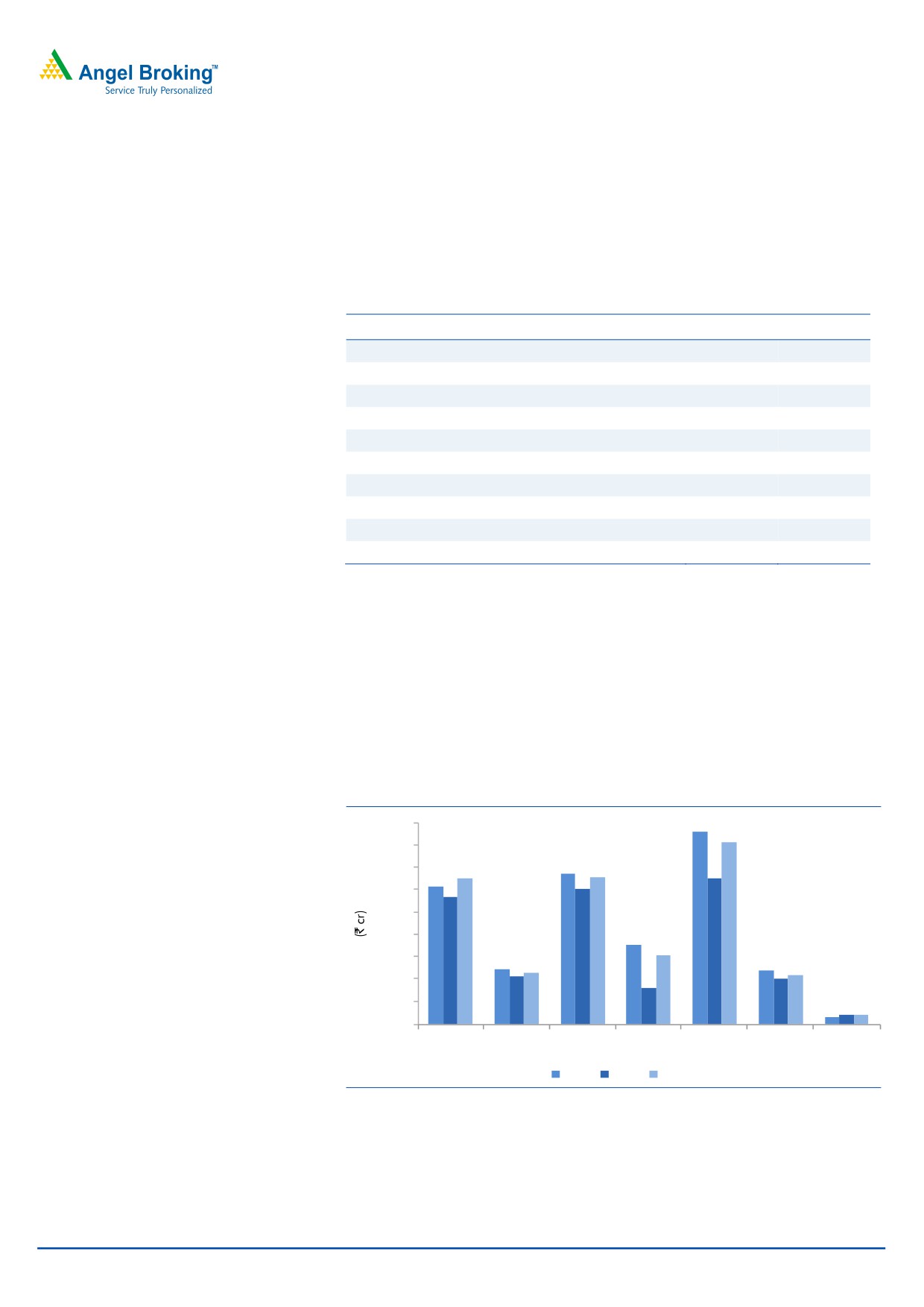

Exhibit 2: TGBL’s increasing global footprint in beverages

1,800

1,600

1,400

1,200

1,000

800

600

400

200

0

USA Canada &

UK & Africa Europe & South Asia

Non

Others

Australia

ME

Branded

2011

2009

2010

Source: Company, Angel Research

December 19, 2011

2

Tata Global Beverages | Initiating coverage

The company generates over 70% of its

During FY2011, TGBL reported more than 70% of its revenue from outside India.

consolidated sales from outside India.

The company has a leadership position in the tea and coffee markets in several

countries. The company is the second largest global tea marketing company and

the third largest player (post acquisition of Eight O’ Clock coffee through its

Branded products constitute 90% of the

subsidiary Tata Coffee) in the branded coffee market in the US.

company’s top line.

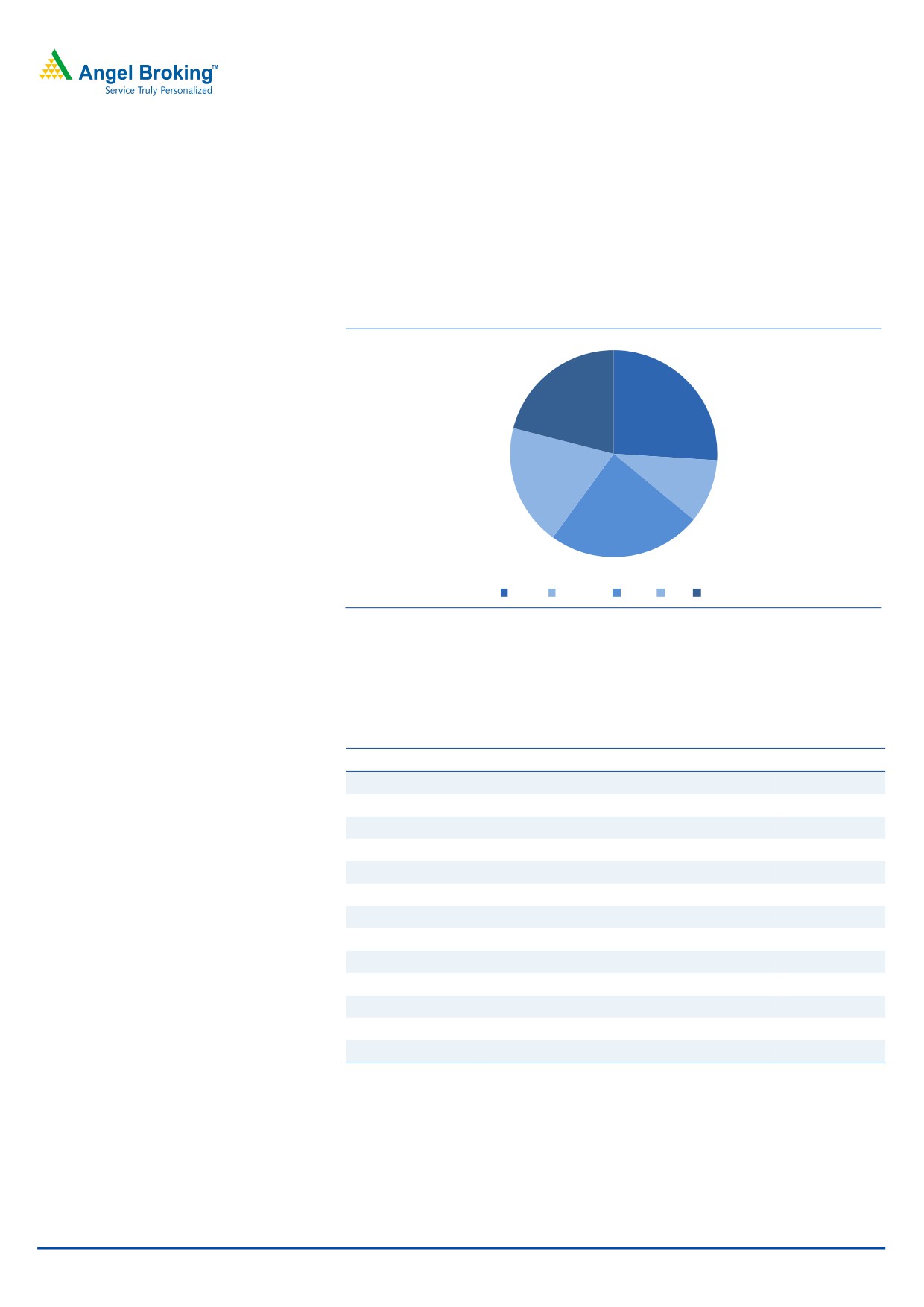

Exhibit 3: TGBL’s country-wise sales of hot drinks in CY10 (% retail value)

21

26

19

10

24

India Canada USA UK Others

Source: Euromonitor International, Angel Research

Apart from being among the leaders in global tea markets, TGBL’s leadership in

the Indian tea market has also been increasing. Currently, iconic brands like Tata

Tea, Kanan Devan and Tetley feature among the top tea brands in the country.

Exhibit 4: Top tea brand shares in India (% retail value)

Brand

Company

CY2010

Tata Tea

TGBL

19.7

Brooke Bond

HUL

19.1

Duncans

Duncans Industries

8.6

Lipton

HUL

6.2

Wagh Bakri

Wagh Bakri

3.5

Kanan Devan

TGBL

3.3

Goodricke

Goodricke Group

1.5

Twinings

Twinings Pvt Ltd

1.2

Golden Tips

Golden Tips Tea Co

1.1

Girnar

Girnar Food & Beverages

1

Jay Green Tea

Jay Shree Tea

0.7

Tetley

TGBL

0.5

Kho-Cha

Kho-Cha Darjeeling Tea Bureau

0.2

Source: Euromonitor International, Angel Research

December 19, 2011

3

Tata Global Beverages | Initiating coverage

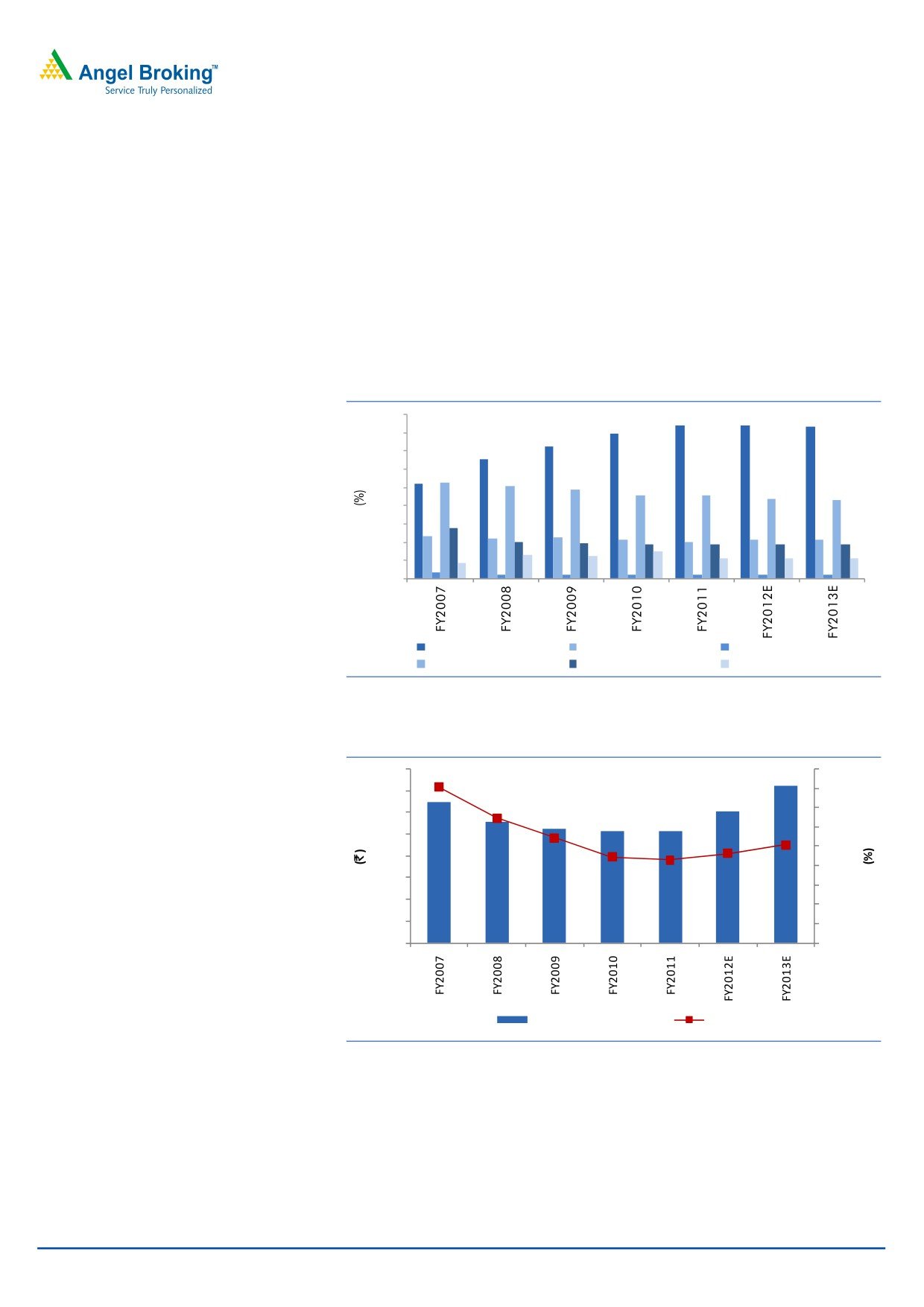

Bottomed-out margins; expect a positive surprise

We model in TGBL’s OPM to improve by ~150bp over FY2011-13E from 8.6% in

FY2011 to ~10.1% in FY2013E, driven by a shift in its focus from the plantation

business to branded products business and rationalization in its operating cost

structure. We expect a rejig in the company’s cost structure due to the ongoing

hiving off of the plantation business and expect staff cost, power and fuel cost and

manufacturing expenses to come down going forward. While TGBL’s focus on

volume growth remains intact, selective price increases and stable ad spends will

further aid in margin improvement.

Exhibit 5: Changes in cost structure to improve OPM

45.0

40.0

35.0

30.0

25.0

20.0

15.0

10.0

5.0

0.0

RM Expenses

Staff Cost

Power & Fuel Cost

SG&A Expenses

Manufacturing Expenses

Miscellaneous Expenses

Source: Company, Angel Research

Exhibit 6: We expect OPM to improve by ~150bp over FY2011-13E

800

18.0

700

16.0

14.0

600

12.0

500

10.0

400

8.0

300

6.0

200

4.0

100

2.0

-

-

EBITDA

OPM

Source: Company, Angel Research

December 19, 2011

4

Tata Global Beverages | Initiating coverage

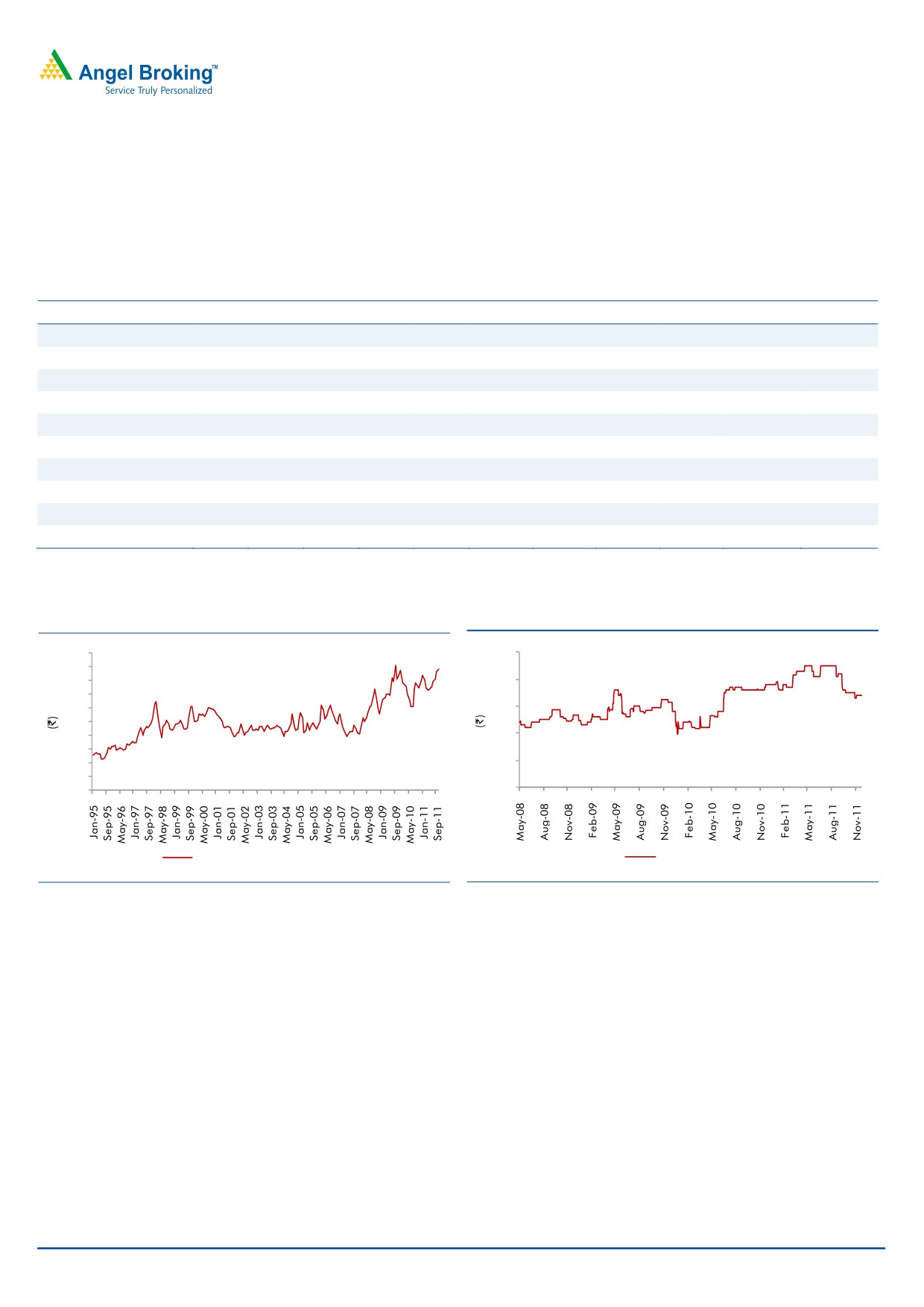

Also, with the Tea Board of India estimating higher production of tea in 2011 as

compared to 2010 (~5% higher production), we expect auction prices of tea to

soften, thereby providing a relief to the company from the heightened input cost

pressure. It is estimated that tea production in India will cross 1,000mn kgs in

2011 with increased tea production from North India.

Exhibit 7: Monthly estimated tea production for CY2011

CY2011 (‘000kgs)

Jan

Feb

Mar

April

May

June

July

Aug

Sept

Oct Jan to Oct

Total Assam

3,426

94

23,669

37,025

30,968

62,824

76,311

84,080

66,962

70,467

455,826

Growth (yoy %)

(37)

114

60

(3)

9

24

14

7

7

(2)

9

Total W. Bengal

2,934

909

14,364

11,954

20,330

25,955

33,934

27,148

23,762

22,973

184,263

Growth (yoy %)

(8)

(39)

(4)

27

10

2

(1)

(1)

(2)

(10)

-

Total North India

6,412

1,004

38,137

49,451

51,738

89,458

111,940

112,757

93,062

95,039

648,998

Growth (yoy %)

(26)

(34)

28

3

9

16

9

5

4

(4)

6

Total South India

14,518

15,728

18,595

23,593

24,439

25,251

21,329

14,250

17,999

22,458

198,160

Growth (yoy %)

(21)

(4)

(3)

17

(3)

(7)

5

(4)

(2)

4

(2)

All India

20,930

16,732

56,732

73,044

76,177

114,709

133,269

127,007

111,061

117,497

847,158

Growth (yoy %)

(23)

(7)

16

7

5

10

8

3

3

(3)

4

Source: Indian Tea Board, Angel Research

Exhibit 8: Mombasa tea auction price (`/kg)

Exhibit 9: India Tea price - signs of cooling down (`/kg)

250

200

180

160

200

140

120

150

100

80

100

60

40

50

20

0

0

Mombasa Tea Auction Price

Indian Tea Price

Source: Industry, Angel Research

Source: Indian Tea Board, Angel Research

December 19, 2011

5

Tata Global Beverages | Initiating coverage

Exhibit 10: Increase in tea plantation acreage to increase production

Year

Area (hectares)

Production (‘000 kgs)

1981

383,629

560,427

1982

394,170

560,562

1983

396,066

581,484

1984

398,453

639,864

1985

399,964

656,162

1986

407,647

620,803

1987

411,335

665,251

1988

414,347

700,014

1989

414,953

688,105

1990

416,269

720,338

1991

420,470

754,192

1992

420,289

732,322

1993

418,363

760,826

1994

425,966

752,895

1995

427,065

756,016

1996

431,204

780,140

1997

434,294

810,031

1998

474,027

874,108

1999

490,200

825,935

2000

504,366

846,922

2001

509,806

853,923

2002

515,832

838,474

2003

519,598

878,129

2004

521,403

892,965

2005

523,000

927,984

2006

567,020

981,800

2007

578,458

986,430

2008

NA

980,820

2009

NA

978,999

2010

NA

966,403

2011

NA

1000000E

Source: Indian Tea Board, Angel Research

Estimate ~40% plus adjusted CAGR over FY2011-13E

We model a ~40% EPS CAGR over FY2011-13, led by (1) 9% revenue growth and

(2) a 150bp margin improvement. We believe the company is set to outperform

the industry’s growth with the help of selective price increases and strong brands

like Tata Tea Premium, Tata Tea Gold, Agni Dust and Kanan Devan.

December 19, 2011

6

Tata Global Beverages | Initiating coverage

We estimate return ratios to improve

Despite being a leading player in the consumer space, TGBL (unlike its FMCG

peers) does not have very high RoE and RoCE - the reason being high goodwill

(~50% of total assets in FY2011) in the balance sheet as a result of acquisitions

over many years.

Exhibit 11: RoCE to improve over FY2011-13E

(%)

Reported

Adjusted for goodwill

Adjusted for goodwill & cash

FY2007

7.5

30.2

32.3

FY2008

6.6

11.2

16.4

FY2009

6.0

10.3

14.1

FY2010

6.2

11.0

22.6

FY2011

6.7

13.2

19.4

FY2012E

8.0

15.8

23.8

FY2013E

9.6

18.8

27.2

Source: Company, Angel Research

Revenue overview

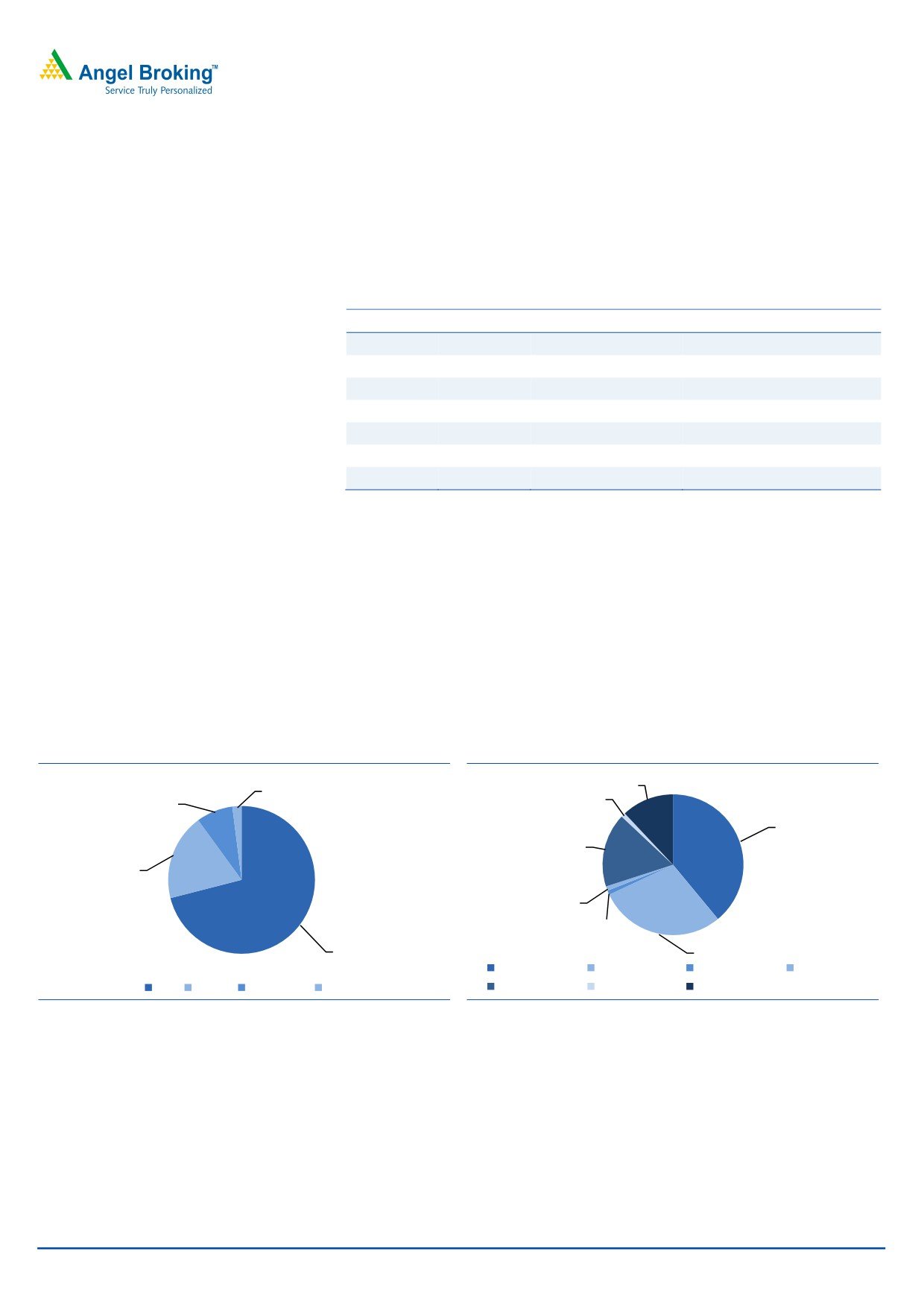

TGBL has become a global non beverage player post its various acquisitions in

many geographical regions. Though the company’s key revenue generating

product remains tea, it is also present in coffee though its subsidiary Tata Coffee

Ltd. The company has recently started to expand its product portfolio by entering

into other beverages. The company has recently entered into a JV with PepsiCo

India Pvt. Ltd. to develop non-carbonated, ready-to-drink beverages focused on

health and enhanced wellness for international markets.

Exhibit 12: Category-wise sales breakup FY2011

Exhibit 13: Brand-wise sales breakup FY2011

12

2

8

1

39

17

19

1

1

71

29

Tetley

Indian Tea Brands Good Earth

Jemca

Tea

Coffee

Plantations

Others

Eight O'Clock

Vitax

Others

Source: Company, Angel Research

Source: Company, Angel Research

December 19, 2011

7

Tata Global Beverages | Initiating coverage

We expect the company’s consolidated revenue to witness a ~9% CAGR over

FY2011-13E, driven by modest volume growth and selective price hikes in the

company’s key categories - tea and coffee.

The tea industry has witnessed a number of changes over the years with changing

consumer behavior due to changing lifestyles and increased awareness. Though

tea remains the key focus area for TGBL, the company is focusing on expanding its

footprint across the globe, strengthening its position in the global tea market and

getting noticed in the global beverages category. Over the years, TGBL has grown

inorganically - considering the sluggish growth in the domestic tea market.

Exhibit 14: Time line of acquisitions and JVs of TGBL

Year

Company

Country

FY2000

Tetley

UK

FY2005

Good Earth, Inc., USA

USA

FY2006

Eight O' Clock Coffee Company, USA

USA

FY2009

Grand, Russia

Russia

FY2011

Rising Beverage Company Llc

USA

FY2012

Nourishco Beverages Ltd (With PepsiCo India)

India

Source: Company, Angel Research

Exhibit 15: Brand portfolio of TGBL

Brands

Category

Country

Tetley

Black tea, herbal tea, fruit tea

UK and Canada

Vitax

Fruit tea

Poland

Jemca

Black tea, green tea, herbal tea, fruit tea Czech

Phendula

Tea

South Africa

Tata Tea

Tea

India

Eight O’Clock

Coffee

USA

Grand

Coffee and tea

Russia

Good Earth

Tea

USA

Himalayan

Mineral water

India

T4 KIDZ

Hot flavoured drink

UK

Laager

Tea

South Africa

Activate

Flavoured water

USA

Nourishco

Non carbonated RTD beverage

India & Intl. markets

Sukk

Drinkable jelly snack

UK

Source: Company, Angel Research

December 19, 2011

8

Tata Global Beverages | Initiating coverage

Outlook and valuation

We estimate modest revenue growth at a ~9% CAGR over FY2011-13E on the

basis of price and volume-led growth. Inspite of the slow revenue growth, we

expect healthy expansion of 150bp in the company’s OPM over FY2011-13E, from

8.6% in FY2011 to ~10% in FY2013E, due to changes in cost structure and

selective price hikes in key products. Adjusted earnings for the company are

expected to witness a robust ~40% EPS CAGR over FY2011-13E, primarily due to

increased OPM.

Despite its leadership position in the Indian packaged tea market, No. 2 position

in the global tea market and generating ~90% of its total revenue from branded

products, TGBL is trading at 13.3x FY2013E EPS (which is at a discount to its

FMCG peers, trading at 20x-35x FY2013E EPS). Also, on EV/Sales basis, the stock

is trading at 0.6x FY2013E EV/Sales (historical average of 1x EV/ Sales). Hence,

we initiate coverage on the stock with a Buy recommendation and a target price of

`104, based on 16x FY2013E EPS of `6.5 (0.9x FY2013 EV/Sales).

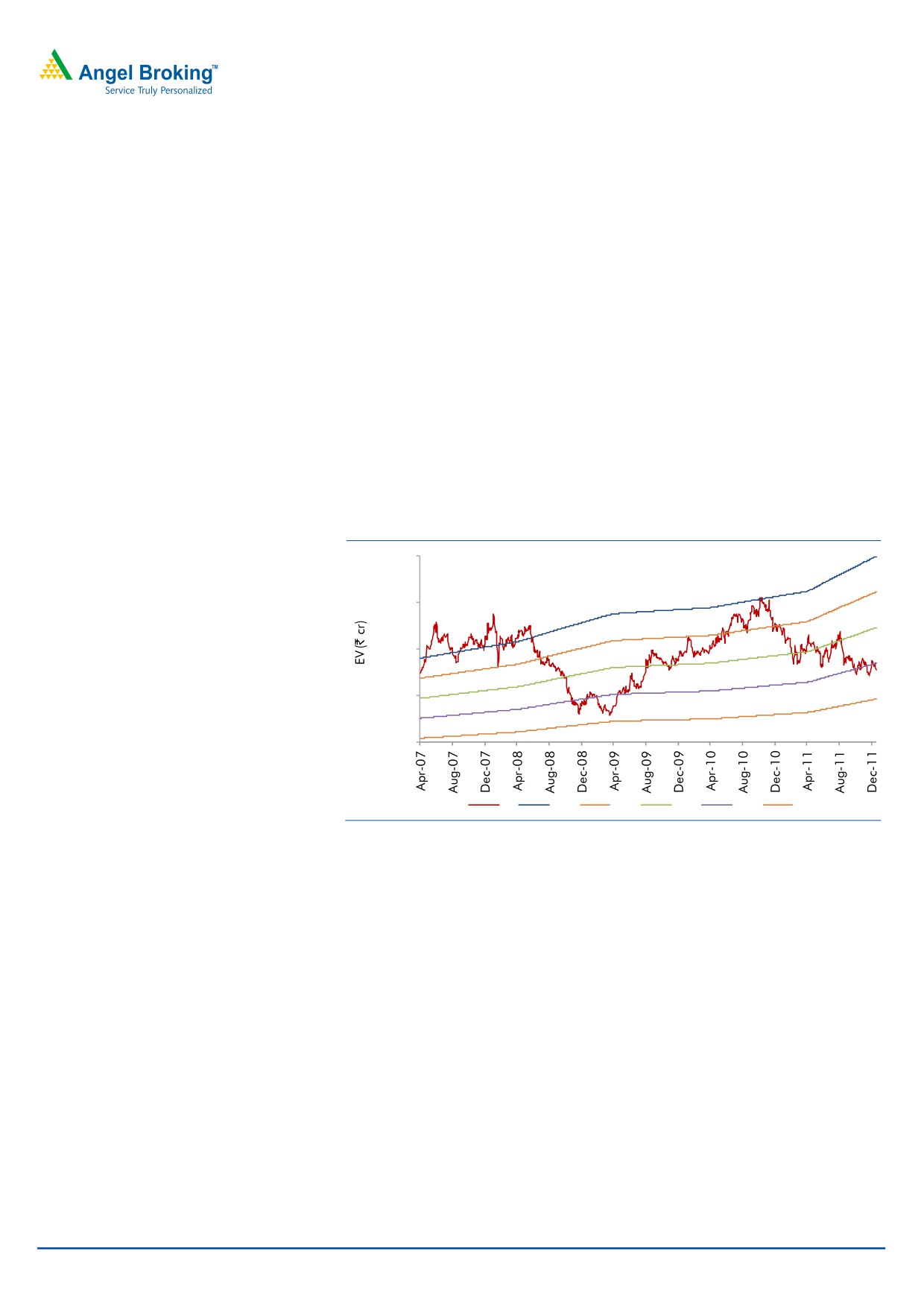

Exhibit 16: Trading at attractive 0.6x FY2013E EV/Sales

10,000

8,000

6,000

4,000

2,000

EV

1.3

1.1

0.9

0.7

0.5

Source: Angel Research

We believe the stock will be re-rated due to the following

reasons:

Improvement in OPM and return ratios going forward

The company has been taking initiatives to expand globally and emerge as a

global beverage player. Going ahead, we believe higher revenue visibility

from the recent JVs and further expansion in non-alcoholic beverages would

result in higher revenue growth.

Key risk

Tea and coffee prices have been at their peaks and volatile. Any further

hardening of key raw materials will negatively impact the company’s margins

and earnings.

December 19, 2011

9

Tata Global Beverages | Initiating coverage

Tea market dynamics in India

According to a report by Euromonitor, tea over the past five years has witnessed

over a 4% CAGR in volumes, with black tea contributing ~98% of volumes.

Volumes of green tea have grown at a faster pace at ~10% in the past five years,

with increasing awareness among consumers about the benefits of green tea.

Exhibit 17: Category-wise volume sales of tea

Tea type (cr tones)

2005

2006

2007

2008

2009

2010 CAGR (%)

Black Tea

2,109

2,171

2,227

2,310

2,396

2,472

15

Green Tea

29

31

33

35

38

42

10

Tea

2,138

2,202

2,260

2,345

2,434

2,514

15

Source: Euromonitor, Angel Research, CAGR over CY2005-10

In terms of value sales, tea has grown by ~15% over CY2005-10 due to higher

demand, as tea remains the most preferred hot drink in most parts of India.

Exhibit 18: Category-wise retail sales value of tea

Tea type (` cr)

2005

2006

2007

2008

2009

2010

CAGR (%)

Black Tea

347.5

368.3

399.5

463.2

527.4

608.5

4.1

Green Tea

25.9

27.8

29.7

31.6

34.0

37.8

9.2

Total Tea

373.4

396.1

429.1

494.9

561.4

646.3

4.1

Source: Euromonitor, Angel Research, CAGR over CY2005-10

During the past few years, changing consumer behavior and increased awareness

about green tea have led to high growth in this category. Though the category is

very small in terms of volume and value sales, it is gaining acceptance among

consumers in the country’s major towns.

The packaged tea market in India is dominated mainly by two players, HUL and

TGBL, with both players competing neck to neck in terms of their market shares.

TGBL has a vast presence in various price points. Tata Tea Premium and Tetley are

its premium brands, whereas Agni Dust and Chakra Gold are the mass brands.

December 19, 2011

10

Tata Global Beverages | Initiating coverage

Company snapshot

TGBL is a global beverage company headquartered in London. The company has

a strong portfolio of global and regional brands such as Tata Tea, Tetley, Eight

O’Clock Coffee, Good Earth, Jemca, Grand Vitax and Himalayan.

During the past decade, TGBL has made acquisitions in various countries in the

tea, coffee, water and other beverages categories. Tea constitutes more than 70%

of the company’s total turnover; coffee constitutes a ~19% share; and the rest

comes from other activities.

Branded products constitute 90% of the company’s annual turnover, with the

remaining sales coming from B2B plantation and extraction activities. About 70%

of the company’s sales are from outside India in countries like US, UK, Czech

Republic and Poland.

Key subsidiaries of TGBL

Exhibit 19: TGBL’s key subsidiaries

Company

Country

Tata Global GB Ltd.

UK

Stansand (Africa) Ltd.

Kenya

OOO Sunty LLC

Russia

Tata Coffee Ltd.

India

Consolidated Coffee, Inc.

US

Source: Company, Angel Research

December 19, 2011

11

Tata Global Beverages | Initiating coverage

Exhibit 20: TGBL vs. local peers relative valuation

Company Reco

Mcap CMP

TP Upside

P/E (x)

EV/Sales (x)

RoE (%)

CAGR #

(` cr)

(`)

(`)

(%) FY12E FY13E FY12E FY13E FY12E FY13E Sales

EPS

Asian Paints Accumulate

25,414

2,650

3,030

14

25.8

21.0

2.7

2.3

39.6

38.3

17.3

19.8

Britannia

Accumulate

5,279

442

495

12

28.7

19.6

1.0

0.9

37.8

46.0

17.3

36.0

Colgate

Neutral

13,817

1,016

-

-

31.5

26.9

5.2

4.5

111.7

108.0

14.9

12.9

Dabur

Buy

16,885

97

115

19

24.1

21.0

3.3

2.9

44.9

41.6

20.5

18.8

GSKCHL*

Neutral

10,306

2,450

-

-

29.6

24.9

3.4

2.9

32.6

31.8

20.1

23.9

GCPL

Accumulate

12,915

399

457

15

24.1

18.5

3.2

2.6

36.6

29.4

22.9

20.2

HUL

Neutral

86,450

396

320

-

33.9

29.8

3.8

3.3

87.5

85.3

12.7

17.1

ITC

Accumulate

152,711

197

219

11

26.5

22.3

5.9

4.9

32.7

31.5

17.6

17.4

Marico

Accumulate

8,546

139

151

9

27.7

22.0

2.4

2.1

30.2

28.8

17.2

28.0

Nestlé*

Neutral

39,918

4,140

3,603

-

41.0

34.5

5.5

4.7

91.1

72.9

16.1

18.9

TGBL

Buy

5,219

84

104

23

16.6

12.2

0.7

0.6

8.4

10.2

9.0

42.3

Source: Angel Research, #Denotes CAGR over FY2011-13E, *Denotes December ending

Exhibit 21: TGBL vs. global non-alcoholic beverage companies

Company

Mcap (mn)

CMP Curr. Country

P/E (x)

EV/Sales (x)

RoE (%)

CAGR #

FY12E FY13E

FY12E FY13E FY12E FY13E Sales EPS

TGBL

52,193

85

INR

INDIA

16.6

12.2

0.7

0.6

8.4

10.2

9.0

42.3

Tingyi Cayman Islands Holding Corp.

131,647

24

Yuan CHINA

15.4

14.0

0.89

0.81

7.8

8.2

7.7

21.3

Green Mountain Coffee Roasters, Inc.

7,108

46

USD USA

27.8

21.9

1.71

1.35

26.3

28.3

36.7

32.2

Dr. Pepper Snapple Group, Inc.

8,260

39

USD USA

17.4

12.6

1.86

1.39

17.6

19.3

45.3

58.0

Hansen Natural Corp.

8,295

95

USD USA

13.1

12.1

1.74

1.68

27.3

29.6

5.7

9.8

Arca Continental SAB de CV

93,663

58

Peso

MEXICO

25.7

21.6

4.18

3.41

31.9

44.5

30.4

23.0

Yakult Honsha Co Ltd.

411,806

2,341

Yen

JAPAN

16.4

13.6

1.85

1.69

15.8

17.1

46.6

27.4

Uni-President China Holdings Ltd.

16,341

5

Yuan CHINA

28.2

25.5

1.28

1.22

6.1

6.5

2.9

16.5

Ito En Ltd.

118,941

1,304

Yen

JAPAN

20.2

14.3

0.58

0.48

8.8

11.3

52.3

33.0

Britvic PLC

724

300

Pound BRITAIN

18.6

16.9

0.42

0.38

7.9

7.4

2.8

(1.4)

Cott Corp.

617

7

CAD CANADA

8.4

7.6

0.90

0.86

189.0

110.9

4.0

27.7

Source: Bloomberg, # Denotes CAGR over CY2011-13E, CMP as on December 19, 2011

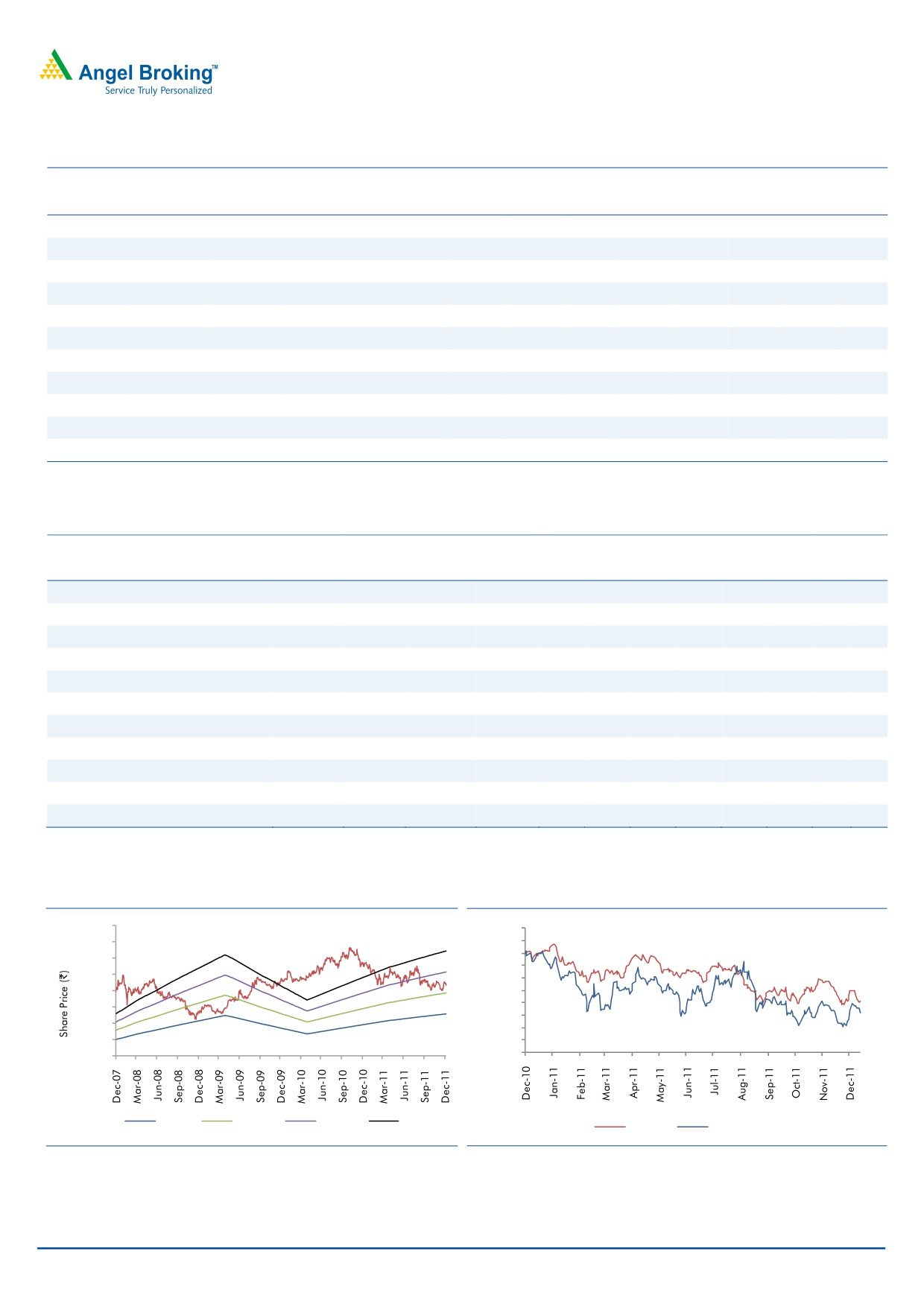

Exhibit 22: One-year forward PE band

Exhibit 23: TGBL’s one-year return to the Sensex

160

110%

140

105%

100%

120

95%

100

90%

80

85%

80%

60

75%

40

70%

20

65%

-

60%

8x

12x

16x

20x

Sensex

TGBL

Source: Angel Research

Source: Angel Research

December 19, 2011

12

Tata Global Beverages | Initiating coverage

Profit and loss statement (Consolidated)

Y/E March (` cr)

FY2008 FY2009 FY2010 FY2011 FY2012E

FY2013E

Gross sales

4,311

4,849

5,784

5,984

6,522

7,110

Less: Excise duty

1.4

1.1

0.9

1.5

0.7

0.7

Net Sales

4,310

4,848

5,783

5,982

6,522

7,109

% chg

7.1

12.5

19.3

3.4

9.0

9.0

Total Expenditure

3,753

4,322

5,269

5,469

5,919

6,389

Cost of Materials

1,416

1,753

2,310

2,521

2,739

2,957

Advertising Exp (Incl Promotion)

825

879

985

1,013

1,057

1,137

Personnel

480

550

611

610

698

754

Others

278

304

437

336

365

398

EBITDA

556

526

514

513

602

720

% chg

(14.1)

(5.6)

(2.3)

(0.0)

17.3

19.5

(% of Net Sales)

12.9

10.8

8.9

8.6

9.2

10.1

Depreciation& Amortisation

92

99

103

99

111

121

EBIT

465

427

411

414

492

600

% chg

(15.7)

(8.2)

(3.8)

0.8

18.8

21.9

(% of Net Sales)

10.8

8.8

7.1

6.9

7.5

8.4

Interest & other Charges

306

210

149

120

122

97

Other Income

1,929

1,039

379

200

188

191

(% of PBT)

92.4

82.7

59.2

40.5

33.8

27.6

Reported PBT

2,088

1,256

641

494

558

694

% chg

258.0

(39.8)

(49.0)

(22.9)

12.8

24.4

Prior Period & Extra Exp/(Inc.)

1,517

480

8

44

-

-

PBT (recurring)

571

776

633

451

558

694

Tax

153

424

248

202

184

229

(% of PBT)

7.3

33.8

38.6

40.9

33.0

33.0

PAT (reported)

1,935

832

393

292

374

465

Add: Share of earnings of asso.

-

25

33

20

20

20

Less: Minority interest (MI)

392

156

36

58

58

58

PAT after MI (reported)

1,543

701

390

254

336

427

ADJ. PAT

25

221

382

211

336

427

% chg

(92.3)

778.0

73.2

(44.8)

59.4

27.2

(% of Net Sales)

0.6

4.5

6.6

3.5

5.2

6.0

ADJ. EPS (`)

0.4

3.6

6.2

3.4

5.4

6.9

Fully Diluted EPS (`)

0.4

3.6

6.2

3.4

5.4

6.9

% chg

(92.3)

778.0

73.2

(44.8)

59.4

27.2

December 19, 2011

13

Tata Global Beverages | Initiating coverage

Balance sheet (Consolidated)

Y/E March (` cr)

FY2008 FY2009 FY2010 FY2011 FY2012E

FY2013E

SOURCES OF FUNDS

Equity Share Capital

62

62

62

62

62

62

Preference Capital

-

-

-

-

-

-

Reserves& Surplus

3,353

3,591

3,662

3,895

3,976

4,152

Shareholders’ Funds

3,414

3,653

3,723

3,957

4,038

4,214

Minority Interest

1,028

1,022

1,057

1,108

1,108

1,108

Total Loans

2,609

2,431

1,797

1,042

942

842

Deferred Tax Liability

37

48

75

64

64

64

Total Liabilities

7,088

7,154

6,652

6,170

6,152

6,227

APPLICATION OF FUNDS

Gross Block

1,351

1,442

1,470

1,563

1,703

1,856

Less: Acc. Depreciation

629

707

752

842

952

1,073

Net Block

722

735

718

721

750

783

Capital Work-in-Progress

50

63

47

39

43

46

Goodwill

2,938

3,027

2,929

3,038

3,038

3,038

Investments

1,391

351

519

587

615

623

Current Assets

3,329

4,587

3,998

3,376

3,620

3,757

Cash

1,323

1,089

1,904

997

1,052

981

Loans & Advances

1,012

2,303

653

736

802

874

Other

400

267

28

30

30

30

Current liabilities

1,358

1,617

1,560

1,590

1,914

2,020

Net Current Assets

1,971

2,970

2,438

1,786

1,705

1,736

Misc. Exp. not written off

16.61

7.64

-

-

-

-

Total Assets

7,088

7,154

6,652

6,170

6,152

6,227

Cash flow statement (Consolidated)

Y/E March (` cr)

FY2008 FY2009 FY2010 FY2011 FY2012E

FY2013E

Profit before tax

2,088

1,256

641

494

558

694

Depreciation

92

99

103

99

111

121

Change in Working Capital

(502)

381

42

(143)

140

(114)

Interest / Dividend (Net)

256

154

91

44

65

48

Direct taxes paid

153

424

248

202

184

229

Others

557

(2,338)

(147)

(71)

(8)

12

Cash Flow from Operations

2,337

(872)

482

221

681

531

(Inc.)/ Dec. in Fixed Assets

(70)

(68)

(89)

(85)

(144)

(157)

(Inc.)/ Dec. in Investments

2,818

1,155

1,472

5

(29)

(8)

Cash Flow from Investing

2,749

1,087

1,384

(81)

(173)

(165)

Issue of Equity

203

-

-

(63)

-

-

Inc./(Dec.) in loans

(1,968)

(178)

(634)

(755)

(100)

(100)

Dividend Paid (Incl. Tax)

253

125

146

145

289

289

Interest / Dividend (Net)

256

154

91

44

65

48

Cash Flow from Financing

(2,274)

(457)

(871)

(1,007)

(454)

(437)

Inc./(Dec.) in Cash

1,204

(234)

815

(907)

54

(70)

Opening Cash balances

119

1,323

1,089

1,904

997

1,052

Closing Cash balances

1,323

1,089

1,904

997

1,052

981

December 19, 2011

14

Tata Global Beverages | Initiating coverage

Key ratios

Y/E March

FY2008 FY2009 FY2010 FY2011 FY2012E FY2013E

Valuation Ratio (x)

P/E (on FDEPS)

220.8

25.2

14.5

26.4

16.6

12.2

P/CEPS

2.7

6.0

11.4

17.9

12.5

9.5

P/BV

1.6

1.5

1.5

1.4

1.4

1.3

Dividend yield (%)

3.9

2.0

2.2

2.2

4.4

4.7

EV/Sales

1.3

1.4

0.9

0.8

0.7

0.6

EV/EBITDA

9.8

12.5

9.6

9.8

8.0

6.2

EV / Total Assets

0.8

0.9

0.7

0.8

0.8

0.7

Per Share Data (`)

EPS (Basic)

0.4

3.6

6.2

3.4

5.4

6.9

EPS (fully diluted)

0.4

3.6

6.2

3.4

5.4

6.9

Cash EPS

32.9

15.1

7.9

5.0

7.2

8.9

DPS

3.5

1.8

2.0

2.0

4.0

4.0

Book Value

54.7

58.5

59.6

63.4

64.6

67.4

Returns (%)

RoCE

6.6

6.0

6.2

6.7

8.0

9.6

Angel ROIC (Pre-tax)

-

-

-

-

-

-

RoE

57.4

23.1

10.4

5.4

8.4

10.2

Turnover ratios (x)

Asset Turnover (Gross Block)

3.3

3.5

4.1

3.9

3.9

3.9

Inventory / Sales (days)

45

49

53

61

62

62

Receivables (days)

37

34

31

33

34

34

Payables (days)

84

88

83

83

83

83

WC cycle (ex-cash) (days)

1

-

1

-

1

-

December 19, 2011

15

Tata Global Beverages | Initiating coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

TGBL

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to 15%)

Sell (< -15%)

December 19, 2011

16

Tata Global Beverages | Initiating coverage

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai - 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Shailesh Kanani

Infrastructure

Srishti Anand

IT, Telecom

Bhavesh Chauhan

Metals, Mining

Sharan Lillaney

Mid-cap

V Srinivasan

Research Associate (Cement, Power)

Yaresh Kothari

Research Associate (Automobile)

Shrinivas Bhutda

Research Associate (Banking)

Sreekanth P.V.S

Research Associate (FMCG, Media)

Hemang Thaker

Research Associate (Capital Goods)

Nitin Arora

Research Associate (Infra, Real Estate)

Ankita Somani

Research Associate (IT, Telecom)

Varun Varma

Research Associate (Banking)

Sourabh Taparia

Research Associate (Cement, Power)

Technicals:

Shardul Kulkarni

Sr. Technical Analyst

Sameet Chavan

Technical Analyst

Sacchitanand Uttekar

Technical Analyst

Derivatives:

Siddarth Bhamre

Head - Derivatives

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Hiten Sampat

Sr. A.V.P- Institution sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Dealer

Akshay Shah

Dealer

Production Team:

Simran Kaur

Research Editor

Dilip Patel

Production

CSO & Registered Office: G-1, Ackruti Trade Centre, Rd. No. 7, MIDC, Andheri (E), Mumbai - 400 093.Tel.: (022) 3083 7700. Angel Broking Ltd: BSE Sebi Regn No: INB010996539 / PMS Regd Code: PM/INP000001546 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / NSE Sebi Regn Nos: Cash: INB231279838 / NSE

F&O: INF231279838 / Currency: INE231279838 / MCX Currency Sebi Regn No: INE261279838 / Member ID: 10500 / Angel Commodities Broking Pvt. Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

December 19, 2011

17