Market Outlook

October 29, 2015

Market Cues

Domestic Indices

Chg (%)

(Pts)

(Close)

Indian markets are expected to open on a Negative note tracking the SGX Nifty and

BSE Sensex

(0.8)

(109)

27,040

most Asian markets.

Nifty

(0.8)

(62)

8,171

The US markets were volatile post the release of Federal Reserve’s (Fed)

Mid Cap

(0.6)

(61)

11,037

announcement but closed on a positve note. The Fed left the rates unchanged as

Small Cap

(0.0)

(1)

11,453

expected and indicated that it will revisit the decision to hike rates in December.

Bankex

(2.5)

(514)

19,811

After weak performance in the past two sessions, the European markets closed on

the positive note on Wednesday.

Global Indices

Chg (%)

(Pts)

(Close)

Indian markets fell for the third straight day as traders awaited FOMC rate decision.

Dow Jones

1.1

198

17,780

Banking stocks led by Axis Bank and ICICI bank took a beating on the expiry day on

reports of Axis Bank selling its loans to asset reconstruction companies at ~65%

Nasdaq

1.3

66

5,096

discount.

FTSE

1.1

73

6,438

Nikkei

0.7

126

18,903

News & Result Analysis

Hang Seng

(0.8)

(186)

22,957

Result Review: Ambuja Cement, JK Tyre, Kirloskar Oil Engines, Transport

Shanghai Com

(1.8)

(59)

3,375

Corporation of India, Elecon Engineering

Result Preview: GPPL, DRL, Dishman Pharma

Detailed analysis on Pg2

Advances / Declines

Bse

Nse

Advances

1,144

18

Investor’s Ready Reckoner

Declines

1,514

32

Key Domestic & Global Indicators

Unchanged

176

-

Stock Watch: Latest investment recommendations on 150+ stocks

Refer P9 onwards

Volumes (` Cr)

Top Picks

BSE

2,702

CMP

Target

Upside

Company

Sector

Rating

(`)

(`)

(%)

NSE

18,683

Axis Bank

Financials

Buy

483

674

39.6

HCL Tech

IT

Buy

875

1,132

29.3

Net Inflows (` Cr)

Net

Mtd

Ytd

ICICI Bank

Financials

Buy

272

370

36.3

FII

(731)

4,317

(29,561)

Power Grid

Power

Buy

131

170

30.1

MFs

160

(2,780)

56,123

TCS

IT

Buy

2,525

3,165

25.4

More Top Picks on Pg6

Top Gainers

Price (`)

Chg (%)

Key Upcoming Events

Rtnpower

8

9.5

Previous

Consensus

Date

Region

Event Description

Sksmicro

426

6.4

Reading

Expectations

Oct 29

Germany

Unemployment change (000's)

2.0

(4)

Edelweiss

60

5.4

Oct 29

US

GDP Qoq (% change)

3.9

1.6

Ncc

83

5.1

Nov 1

China

PMI Manufacturing

49.8

-

Pmcfin

1

4.5

Nov 2

US

ISM manufacturing PMI

50.2

49.6

Top Losers

Price (`)

Chg (%)

Axisbank

483

(7.4)

Amarajabat

915

(6.3)

Thermax

845

(5.4)

Bharatforg

867

(5.1)

Icicibank

272

(4.3)

As on October 28, 2015

Market Outlook

October 29, 2015

Result Review

Ambuja Cement (CMP: `209 / TP: `233/Upside: 11.5%)

Ambuja Cement 3QCY2015 numbers were in line with our expectation on

operating front; however lower other income led to sharp fall in profitability.

EBIDTA at `310cr declined 21% yoy, mainly due to subdued cement demand and

higher other expenses (led by `40cr provision towards contribution for DMF) but

were in line with our estimate of `318cr. EBIDTA margin at 14.7% declined 317bp

yoy, but were in line with our estimate of 14.7%. Net sales declined by 4.2% yoy to

`2095.2cr due to flat cement demand and weak realization. Realization came in

at `4347 per tonne a decline of 4.2% yoy, but in line with our estimate of `4345

per tonne. Sales volume was flat yoy to 4.82mt but below our estimate of 4.95mt.

Net profit at `153.6cr, were below our estimate of `220.2cr. We maintain our

Accumulate rating on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

CY2016E

12,022

22.7

1,699

11.0

15.5

18.9

2.8

10.1

2.3

CY2017E

13,053

23.4

1,911

12.3

16.4

16.8

2.7

8.5

2.0

JK Tyres (CMP: `106 / TP: -/Upside: -)

JK Tyres 2QFY2016 results were in line with our estimates on the operating front;

however forex loss led to lower than estimated profitability. JKT revenues,

expectedly declined 3% yoy to `1,810 cr (our estimate was `1,818 cr) owing to

subdued demand in the truck replacement market, increased imports from China

and price cuts to pass on the lower raw material prices. Operating margins at 17%

improved sharply 460 bp yoy primarily due to softness in the raw material prices.

The margins met our estimates of 16.6%. EBIDTA at `307 cr was in line with our

expectation of `303 cr. However, forex loss of `29 cr lead to the profitability

missing our estimates. Net Profit at `118 cr was below our estimates of `130 cr.

We maintain our Neutral rating on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

7,446

15.2

445

19.6

25.2

5.4

1.4

4.7

0.7

FY2017E

7,669

14.0

417

18.4

19.5

5.8

1.1

4.4

0.6

Kirloskar Oil Engines Ltd (CMP-`300/ TP: - / Upside: -)

For 2QFY2016, Kirloskar Oil Engines (KOEL) reported a disappointing set of

numbers. The top-line for the quarter declined by 6.0% yoy to `590cr. The poor

top-line can mainly be attributed to low contribution from the large engines

business which had completed the order for NPCIL in 4QFY2015 and overall

sluggishness in the PowerGen Segment. The net raw material cost declined by

286bp yoy to 62.3% of sales while employee expense increased by 79bp yoy to

8.5% of sales, and other expenses increased by 405bp yoy to 21.0% of sales. This

resulted in EBITDA margin contracting by 198bp yoy to 8.2%, lower than our

Market Outlook

October 29, 2015

estimate of 9.8%. Other income increased by 61.1% yoy to `20 and consequently,

the net profit remained flat at `36cr (against our estimate of `37cr).

Since the completion of Large Engines order in FY2015, the top-line is expected to

remain weak for the current year as there are no orders expected in the current

year. Additionally, the sluggishness in the DG set market continues to exist. We

have scaled down our estimates for the current year to reflect the poor demand

scenario. Currently, we have a Neutral rating on the stock and will/may update

out numbers post management interaction.

Y/E

Sales OPM PAT EPS

ROE

P/E

P/BV EV/EBITDA EV/Sales

Mar

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

2,471

8.8

132

9.1

9.7

30.8

2.9

14.6

1.3

FY2017E

2,830

10.4

192

13.3

13.3

21.2

2.7

10.5

1.1

Transport Corporation of India (CMP: `291 / TP: -/Upside: -)

For 2QFY2016, Transport Corporation of India Ltd (TCIL)’s earnings has come in

below our estimates. The top-line, at ~`556cr (our estimate was of ~`625cr), is

flat on a yoy basis, with all business segments posting poor performances, barring

Seaways which reported a growth of ~11% yoy to `32cr. For the quarter, the

company reported an operating profit of ~`44cr, up ~7% yoy. Further, the

company’s operating margin expanded by 53bp yoy to 7.9%, primarily on account

of lower operating expenses, which were down 245bp as a percentage of sales.

The net profit grew by ~9% yoy to ~`23cr (which is below our estimates of `25cr)

mainly due to lower sales growth during the quarter. Currently, we have a Neutral

rating on the stock and will update the same post our interaction with the

Management.

Elecon Engineering (CMP: `1,518/ TP: -/ Upside: -)

For 2QFY2016, Elecon Engineering reported standalone numbers that were mostly

below our estimates. The top-line for the quarter declined by 5.5% yoy to `111cr.

Our estimate was on the higher side at `145cr. As per management’s indication,

the momentum in the infrastructure activity is yet to pick up, causing a muted

performance on the top-line front. However, the operating performance improved

significantly during the quarter led by 1,516bp yoy decline in raw material cost to

43.9% of sales. The same was neutralized by 394bp yoy and 236bp yoy increase

in employee and other expenses to 12.4% and 18.9% of sales respectively. This

resulted in EBITDA margin expanding by 859bp yoy to 24.9% (against our

estimated of 22.1%). Led by better operating performance, the standalone net

profit increased by 158.9% yoy to `7cr, which is below our estimate of `10cr.

On consolidated basis, Elecon’s top-line declined by 5.1% yoy to `283cr. The

Material Handling division revenues declined by 2.6% yoy to `101cr while the

segment reported a loss of `6cr against loss of `3cr in the same quarter of the

previous year. The Gears division revenues declined by 7.8% yoy to `190cr and

the segment profits increased by 78.6% yoy to `25cr. The Consolidated net profit

after minority interest and profits from associated stood at `1.4cr against loss of

`3.0cr in the same quarter of the previous year.

Market Outlook

October 29, 2015

The MHE business of the company continues to be under pressure as the company

is not seeing any significant movement in terms of project execution at customer

level. We currently have a Neutral view on the stock and will update our rating

post management discussion.

Result Preview

Gujarat Pipavav Port (CMP: `180/ TP: - / Upside: -)

Gujarat Pipavav Port Ltd. (GPPL) would be shortly announcing its results for the

quarter ended Sep-2015. We expect revenues to grow by 14.4% yoy to `179.8cr,

mainly led by higher Bulk business volumes. We expect revenues from the

Container business to be adversely impacted on account of disruption in railway

lines and owing to loss of a key client to Mundra Port. We expect EBITDA margins

to remain almost flat at 53% for the quarter. In absence of any dividend

announcement by Pipavav Railway Corporation Ltd (PRCL), we expect GPPL to

report a 47.9% PAT margin for the quarter. Reported PAT is expected to decline by

5.2% yoy. Currently we have a Neutral rating on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BVEV/EBITDAEV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

721

53.1

397

8.2

20.0

21.9

3.5

21.8

10.8

FY2017E

784

53.6

439

9.1

18.3

19.8

2.9

19.2

9.6

DRL (CMP: `4,108 / TP: -/Upside: -)

For 2QFY2016, the company is expected to post moderate growth in sales and net

profit. The company is expected to post an 11.5% growth in sales to end the

period at `4000cr V/s `3588cr in 2QFY2015, mainly driven by domestic markets.

Other markets Like Russia and ROW could be under pressure, on back of

currency. Its key market like US is likely to be stagnant during the period, on back

of few approvals, while domestic formulation market should post good growth.

On operating front, the EBIT margins are expected to come in at 18.7% V/s 17.3%

in 2QFY2015. Thus, the net profit came in at `631cr V/s `574cr in 2QFY2015, a

yoy growth of 9.9%. The stock has seen decent up move, making valuations, fair,

thus we maintain our Neutral stance on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

18,213

22.6

2,777

163.0

22.5

25.2

5.2

16.8

3.8

FY2017E

21,214

22.7

3,282

192.6

22.0

21.3

4.3

14.2

3.2

Dishman Pharma (CMP: `362 / TP: -/Upside: -)

For 2QFY2016, company is expected to post a moderate set of numbers. The

company is expected to post a 9.3% yoy growth in sales to end the period at

`429cr V/s `392cr in 2QFY2015. On operating front, the GPM, is expected to

come in at 72.3% V/s 69.7% in 2QFY2015. This is expected to lead the OPM to

come in at 22.0% V/s 20.5% in 2QFY2015. The net profit is consequently expected

Market Outlook

October 29, 2015

to come in at came in at `35.6cr V/s `33.4cr in 2QFY2015, a yoy growth of 6.6%.

We maintain our Neutral stance on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,716

20.2

132

16.3

9.7

22.2

2.1

9.7

1.9

FY2017E

1,888

20.2

174

21.6

11.7

16.8

1.9

11.7

1.6

Economic and Political News

Proposal to allow jewellers to participate in GMS

FoodMin proposes `47.50 a qtl of first-ever direct subsidy to cane farmers

PSU disinvestment nets 71% of total fund raising in April-September

Corporate News

Sun Pharma recalls anti-allergic drug in the US

Novartis' generic drug arm gets USFDA warning letter for two plants in India

JK Tyre to increase passenger car tyre capacity by 50% at its Mexican facility

FIPB rejects Apollo Hospitals' proposal to raise FDI through rights issue

Market Outlook

October 29, 2015

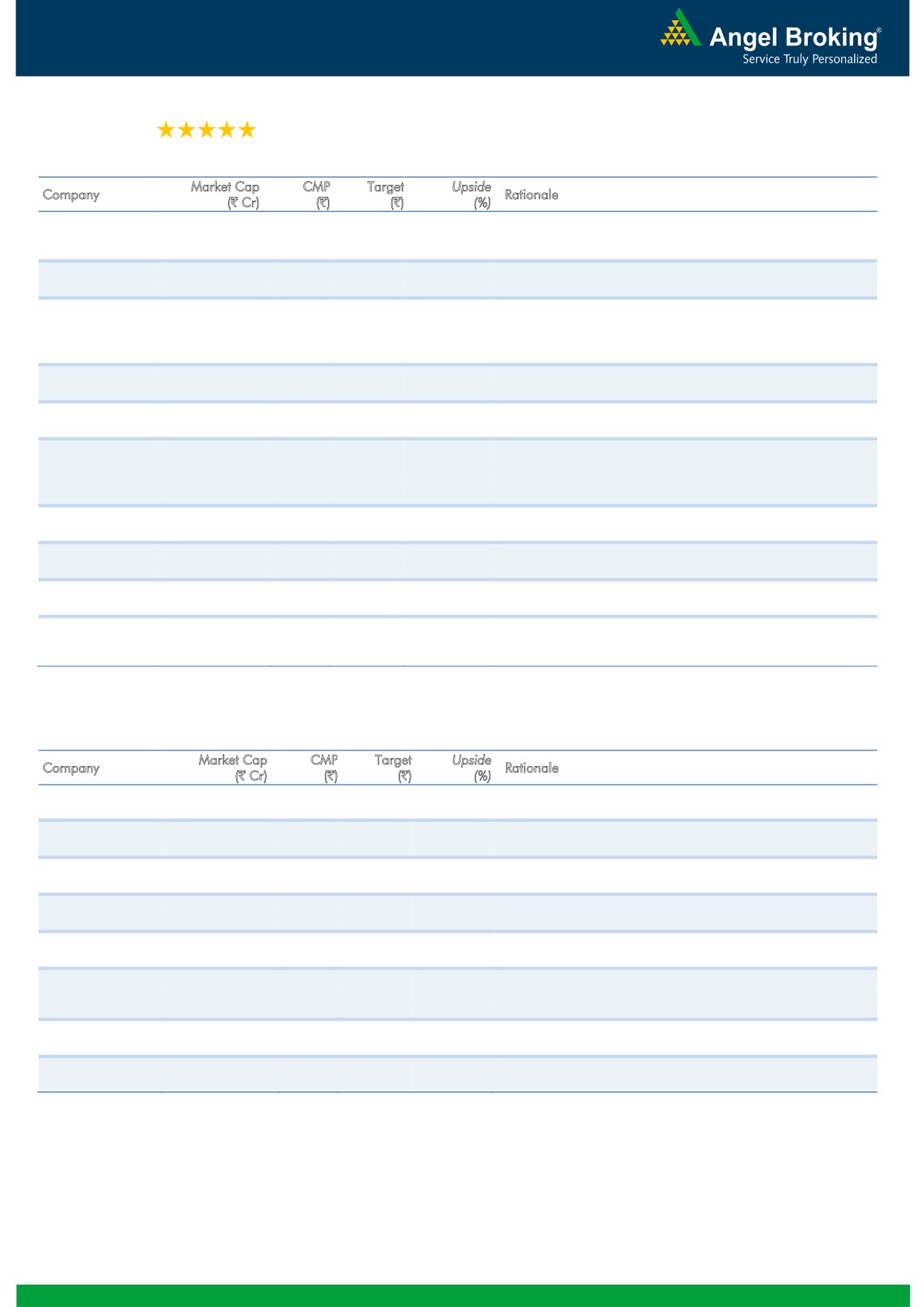

Top Picks

Large Cap

M

arket Cap

CM

P

T

arget

Upsid

e

Company

Rationale

(` Cr)

(`)

(`)

(%)

Healthy pace of branch expansion, backed by distribution

Axis Bank

1,14,839

483

674

39.6

network, will be the driving force for the bank’s retail business

and overall earnings.

The stock is trading at attractive valuations and is factoring all

HCL Tech

1,23,103

875

1,132

29.3

the bad news.

Due to its robust franchise and capital adequacy position, the

bank is well positioned to grow by at least a few percentage

ICICI Bank

1,57,679

272

370

36.3

points higher than the average industry growth rate from a

structural point of view.

Back on the growth trend, expect a long term growth of 14% to

Infosys

2,64,459

1,151

1,306

13.4

be a US$20bn in FY2020.

Government thrust on Renewable sector and strong order book

Inox Wind

8,917

402

505

25.7

would drive future growth.

LICHF continues to grow its retail loan book at a healthy pace

with improvement in asset quality. We expect the company to

LIC HFL

24,716

490

570

16.4

post a healthy loan book which is likely to reflect in a strong

earnings growth.

Direct beneficiary of the huge investments lined up in the power

Power Grid

68,377

131

170

30.1

transmission sector.

Growth to pick up from 2HFY2017, attractive given the risk-

TCS

4,97,464

2,525

3,165

25.4

reward.

Tech Mahindra

52,856

549

646

17.6

Acquisitions, to drive growth, normalised valuations attractive.

An improving liability franchise, capital adequacy well above

Yes Bank

30,555

729

906

24.2

Basel III requirements and lowest NPA ratio in the industry, will

help Yes Bank to deliver a stronger growth.

Source: Company, Angel Research

Mid Cap

M

arket Cap

CM

P

T

arget

Upsid

e

Company

Rationale

(` Cr)

(`)

(`)

(%)

Bajaj Electricals

2,513

249

341

36.9

Visible turnaround in E&P business to drive the earnings.

Garware Wall Ropes

721

330

390

18.3

Higher exports & easing material prices to drive profitability

Comfortable balance sheet to support strong growth; this

MBL Infrastructures

887

214

360

68.3

coupled with attractive valuation to lead to rerating.

New product introductions and increased sourcing by clients to

Minda Industries

812

512

652

27.4

enable outpace industry growth.

Strong brand & quality teaching with innovative technologies &

MT Educare

557

140

169

20.7

higher government educational spending to boost growth.

Earnings boost on back of stable material prices and favourable

Radico Khaitan

1,340

101

112

11.2

pricing environment. Valuation discount to peers provides

additional comfort.

Structural shift in the Lighting industry towards LED lighting will

Surya Roshni

590

135

183

36.0

drive growth.

Tree House

1,188

281

449

59.9

Robust expansion plan for pre-schools to drive growth.

Source: Company, Angel Research

Market Outlook

October 29, 2015

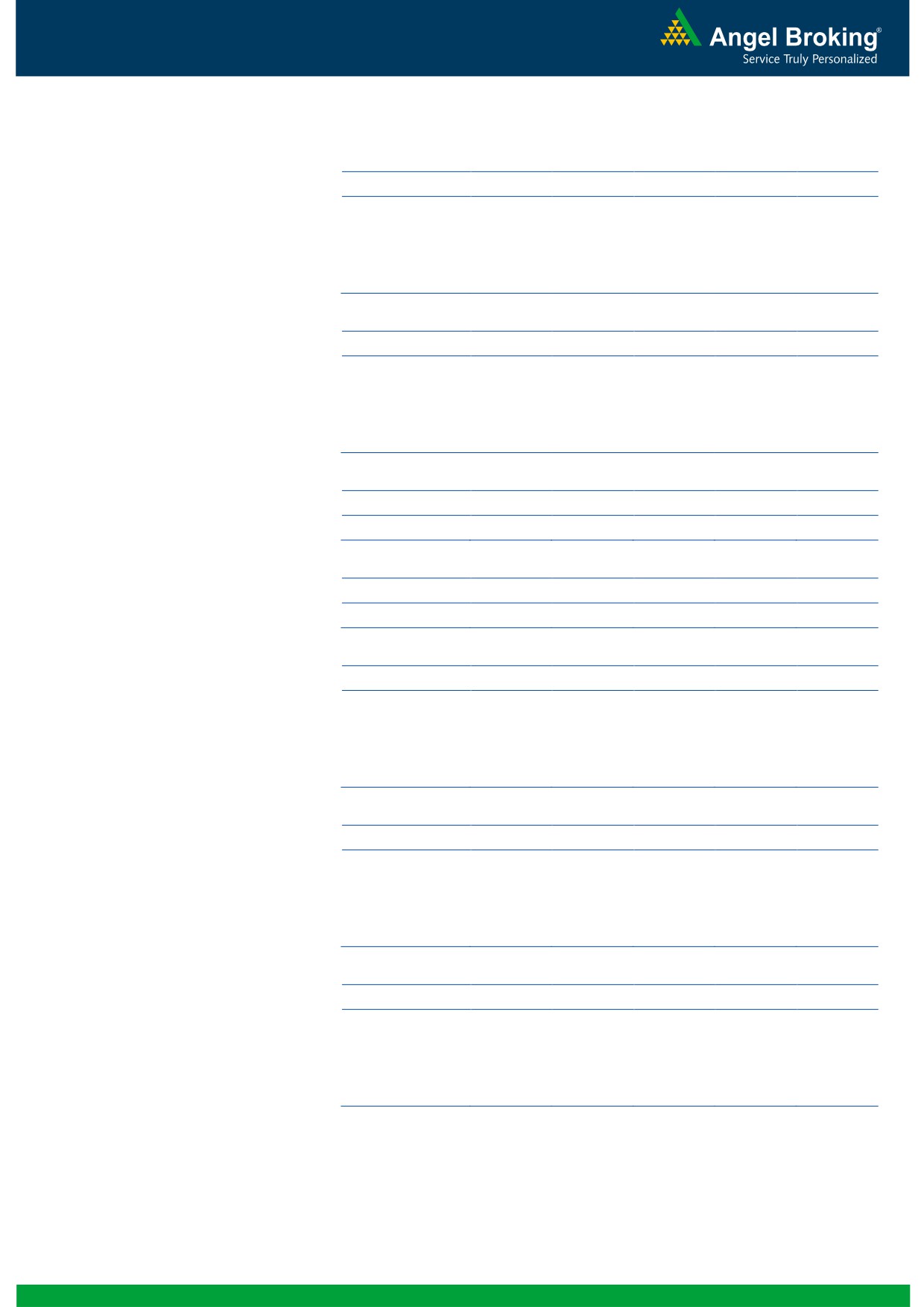

Quarterly Bloomberg Brokers Consensus Estimate

Grasim Industries - October 29, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

8,230

7,866

4.6

8,508

(3.3)

EBITDA

1,293

1,175

10.0

1,417

(8.8)

EBITDA margin (%)

15.7

14.9

16.7

Net profit

433

416

4.1

485

(10.7)

Nestle India Ltd - October 29, 2015

Particulars (` cr)

3QCY15E

3QCY14

y-o-y (%)

2QCY15

q-o-q (%)

Net sales

2,028

2,399

(15.5)

1,934

4.9

EBITDA

393

470

(16.4)

383

2.6

EBITDA margin (%)

19.4

19.6

19.8

Net profit

231

311

(25.7)

(6)

3,687.0

Shriram transport Finance- October 29, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

PAT

351

302

16.2

321

9.3

Yes Bank - October 29, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

PAT

566

482

17.4

551

2.7

NTPC ltd - October 29, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

18,166

16,582

9.6

17,019

6.7

EBITDA

4,234

3,242

30.6

3,438

23.2

EBITDA margin (%)

23.3

19.6

20.2

Net profit

2,022

2,072

(2.4)

2,135

(5.3)

Bharat Forge Ltd - October 29, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

1,223

1,109

10.3

1,103

10.9

EBITDA

355

325

9.2

346

2.6

EBITDA margin (%)

29.0

29.3

31.4

Net profit

203

175

16.0

195

4.1

Colgate Palmolive India Ltd - October 29, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

1,064

994

7.0

1,003

6.1

EBITDA

229

187

22.5

222

3.2

EBITDA margin (%)

21.5

18.8

22.1

Net profit

139

130

6.9

114

21.9

Market Outlook

October 29, 2015

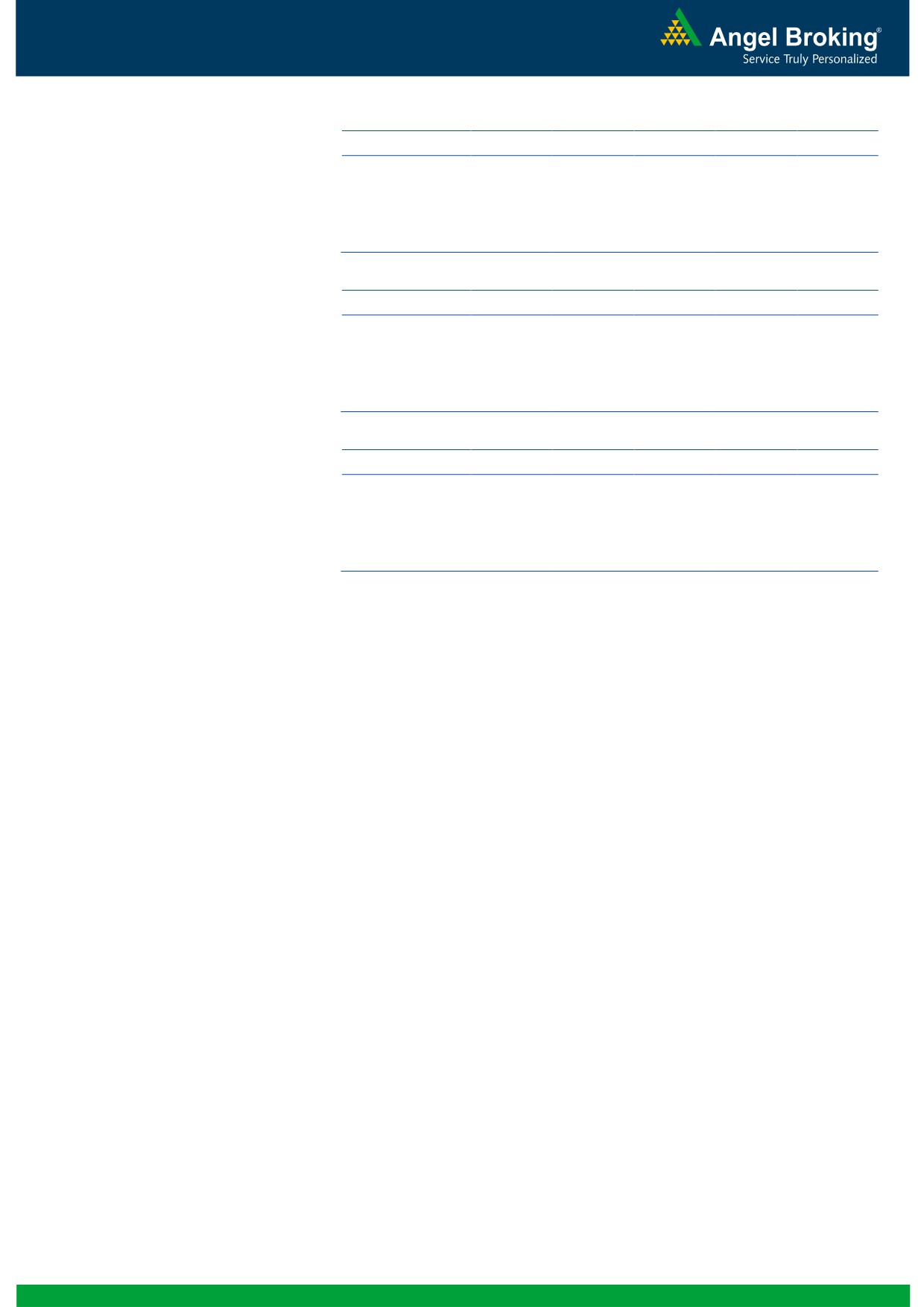

Crompton Greaves Ltd - October 29, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

3,393

3,430

(1.1)

3,166

7.2

EBITDA

148

168

(11.9)

79

87.3

EBITDA margin (%)

4.4

4.9

2.5

Net profit

48

70

(31.4)

16

200.0

DR Reddy's Laboratories Ltd- October 29, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

3,161

3,588

(11.9)

3,758

(15.9)

EBITDA

979

842

16.3

926

5.7

EBITDA margin (%)

31.0

23.5

24.6

Net profit

637

574

11.0

626

1.8

Glenmark Pharmaceuticals Ltd - October 29, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

1,835

1,672

9.7

1,626

12.9

EBITDA

387

335

15.5

360

7.5

EBITDA margin (%)

21.1

20.0

22.1

Net profit

214

165

29.7

178

20.2

Market Outlook

October 29, 2015

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.