Market Outlook

November 9, 2015

Market Cues

Domestic Indices

Chg (%)

(Pts)

(Close)

Indian markets are expected to open in red tracking SGX Nifty.

BSE Sensex

(0.2)

(39)

26,265

Labor department on Friday released its jobs report. Labor department said that

Nifty

(0.0)

(1)

7,954

economy added 271,000 jobs in October, largest monthly gain this year. Also

Mid Cap

(0.4)

(45)

10,826

employment rate fell to 5%, and hourly wages rose at the fastest year-over-year

Small Cap

(0.6)

(67)

11,052

pace since 2009. These strong numbers have raised concerns for traders to wrestle

Bankex

0.6

123

19,496

between the impact of end of ultra loose monetary policy and signs that U.S.

economy is on a healthy path. U.S. stocks mostly ended the Friday’s session higher.

Global Indices

Chg (%)

(Pts)

(Close)

European stock ended mixed on Friday after better than expected U.S. jobs report.

DAX and CAC ended in green, whereas FTSE ended in red.

Dow Jones

0.3

47

17,910

Nasdaq

0.4

19

5,147

After some struggle, Indian markets ended Friday’s trading session in red for third

consecutive session. Banking stocks perked up, but Pharma and Metal stocks lagged

FTSE

(0.2)

(11)

6,364

behind. With outcome of the Bihar Elections ahead, investors turned cautious.

Nikkei

0.8

149

19,266

Hang Seng

(0.8)

(184)

22,867

News & Result Analysis

Shanghai Com

1.9

67

3,590

Dr Reddy’s gets Warning Letter from USFDA

Result Review: BEML, ITNL, State Bank of India, Bank of Baroda, Punjab

National Bank, MT Educare, Tata Motors, Banco Products, Abbott India, TVS

Advances / Declines

BSE

NSE

Srichakra, MM Forgings

Advances

1,018

512

Detailed analysis on Pg2

Declines

1,646

983

Investor’s Ready Reckoner

Unchanged

146

107

Key Domestic & Global Indicators

Volumes (` Cr)

Stock Watch: Latest investment recommendations on 150+ stocks

Refer P10 onwards

BSE

2,539

NSE

16,443

Top Picks

CMP

Target

Upside

Company

Sector

Rating

(`)

(`)

(%)

Net Inflows (` Cr)

Net

Mtd

Ytd

Axis Bank

Financials

Buy

465

630

35.5

FII

(1,298)

(1,305)

(16,124)

HCL Tech

IT

Buy

885

1,132

27.9

MFs

840

1,007

51,354

ICICI Bank

Financials

Buy

267

348

30.0

Ashok Leyland

Automobiles

Buy

88

111

26.8

Top Gainers

Price (`)

Chg (%)

Larsen & Toubro

Construction

Buy

1,377

1,646

19.5

Mothersumi

266

9.6

More Top Picks on Pg8

Hexaware

258

5.4

Key Upcoming Events

BankBaroda

167

5.0

Previous

Consensus

Date

Region

Event Description

Reading

Expectations

Godrejcp

1,304

4.4

Nov 11

CNY

Industrial Production (YOY) (Oct)

5.7%

5.8%

Sbin

243

3.9

Nov 11

AUD

Employment Change (Oct)

-5.1k

15.0k

Nov 13

EUR

German GDP (QoQ) (Q3)

0.4%

0.3%

Top Losers

Price (`)

Chg (%)

Nov 13

USD

Core Retail Sales (MOM) (Oct)

-0.3%

0.4%

Drreddy

3,630

(14.7)

Recltd

239

(10.4)

Den

100

(9.6)

Pfc

232

(7.8)

Pmcfin

1

(7.3)

As on November 06, 2015

Market Outlook

November 9, 2015

Dr Reddy’s gets Warning Letter from USFDA

Dr Reddy’s has received a warning letter issued by the USFDA, relating to its three

plants Srikakulam, and Miryalaguda, Telegana along with the oncology

formulation business at Duvvada. Dr Reddys has mentioned that it will respond to

the letter in 15 days. The company has said that Srikakulam facilities itself

contribute around 10-12% of sales of the company. However, according to the

company’s SEC filling the company had set up a new manufacturing facility in a

Special Economic Zone in Duvvada, Visakhapatnam, Andhra Pradesh, India for

the manufacture of parenteral (injectable form) products, so we think the

contribution of the plant, should not be significant. Further the impact of the API

facilities would be depend upon how quick the company fixes the USFDA issues

plant transfers or does third party sources. Nonetheless, the near term

performance of the company will be impacted. The stock has corrected around

10-12% on back of the news, which we believe should discount most of the

negatives in the stock. We remain neutral on the stock.

Result Review

BEML (CMP: `1,109/ TP: / Upside: )

BEML reported standalone sales of

`617cr, up

38.0% YoY (ahead of our

expectation of `599cr). We were expecting EBITDA level losses at `13.1cr, and the

company has reported EBITDA level losses of `13.4cr. Noteworthy, the company

has reported lower EBITDA losses from the year ago levels of `31.1cr. Impact of

EBITDA level losses was seen at the PAT level too, as the company reported net

loss of `30.2cr, against our loss expectation of `12cr. PAT level loss has narrowed

down from previous year’s `55.1cr. Despite 2QFY2016 losses, considering the

company's strong market positioning across business segments and improving

award activity environment, we are optimistic that BEML should report order wins

going forward. Increase in the order book, should translate to better execution and

again lead to turn-around in profits. We continue to maintain our NEUTRAL rating

on the stock.

ITNL (CMP: `90/ TP: / Upside: )

For 2QFY2016, IL&FS Transportation Network (ITNL) reported a top-line

of `1,872cr, up 24.7% YoY and 13.8% QoQ. The quarter’s top-line numbers

include `136cr of compensation claims made to 3 SPVs (vs `261cr in 2QFY2015).

On adjusting for the same, on an evenly basis, the reported top-line grew 39.9%

YoY to `1,736cr, which is below our expectations of `1,755cr. On the operating

front, ITNL reported an EBITDA margin of

35.2% for the quarter vs our

expectations of 32.0% and vs 41.0% in 2QFY2015. The company reported a PAT

of `69cr for the quarter against our expectation of `4cr. The surprise on the PAT

front was aided by better than expected other income and lower than expected

interest expenses, apart from a favorable EBITDA margin. We believe the order

book is not a concern for the company as of now. The core concern area in our

view is its highly levered balance sheet (consol. D/E at 4.48x). With successful

completion of the company’s recent `740cr rights issue, we expect the near-term

equity requirements towards the ongoing BOT projects to be addressed. The

Market Outlook

November 9, 2015

company should see some ease in their cash flow cycle, as 9 of the BOT projects

are about to commence operations in the next 15 months. However, the concern

area is the company’s high debt composition in the near-term. We expect further

news flow on fund raising/ asset divestment to help the stock, get re-rated going

forward. We await more details on the company’s 2QFY2016 performance from

the Management; till then, we maintain our NEUTRAL rating on the stock.

State Bank of India (CMP: `243/ TP: `283/ Upside: 16.4%)

State Bank of India reported 2QFY2016 results, which were above our as well as

street expectations. Advances grew by 10.5% yoy, which resulted in NII growth of

7.4% yoy. Other income saw a jump of 35.6% yoy at `6,197cr resulting in an

increase of operating income by

14.6% yoy. Asset quality shows signs of

improvement with Gross as well as Net NPA ratio declining by 14bp and 10bp

respectively at 4.15% and 2.14% respectively. Fresh slippages for the quarter came

in at `5,875cr as against `7,318cr for Q1FY2016. Provisions came in at `4,361cr

which grew marginally at 2% yoy. Overall, the PAT for the bank grew 25.1% yoy to

`3,879cr led due to healthy performance on all fronts. SBI has been reporting

stable numbers with respect to slippages and NPA ratios over the past several

quarters as compared to its peers. The bank’s core strength has been its high

CASA and fee income, which has supported its core profitability in challenging

times. Its strong capital adequacy also provides comfort. In our view, the stock is

currently trading at a moderate valuation of 0.9x FY2017E ABV as compared to its

peers. Hence we recommend a BUY rating on the stock.

Y/E

Op. Inc

NIM

PAT

EPS ABV ROA ROE

P/E P/ABV

March

(` cr)

(%)

(` cr)

(`)

(`)

(%)

(%)

(x)

(x)

FY2016E

82,520

2.7 14,954

20.0

183.9

0.7

11.5

11.8

1.3

FY2017E

93,299

2.8 18,266

24.5

207.7

0.7

12.8

9.7

1.1

Bank of Baroda (CMP: `167/ TP: / Upside: )

Bank of Baroda reported 2QFY2016 results with PAT de-growth of 88.7% yoy to

`124cr. Advances growth was muted at 7.6% yoy, whereas NII also fell 3.9% yoy.

However, operating income registered a marginal decline of 0.1% yoy largely

supported due to other income which grew 15.4% yoy. However, the main factor

which led to the sharp decline in the PAT was provisions which spiked 113% yoy to

`1,892cr against `888cr in 2QFY2015. Asset quality declined sharply with the

Gross NPA increased rising sequentially to 5.56% in 2QFY2016 from 4.13% in

1QFY2016, whereas Net NPA at 3.08% in the current quarter as compared to

2.07% in 1QFY2016. Fresh Slippages for the quarter was higher at `6,816cr as

compared to `1,685cr in 1QFY2016. From the valuation perspective, the stock

currently trades at 0.7x FY2017E ABV. We maintain our NEUTRAL rating on this

stock.

Y/E

Op. Inc

NIM

PAT

EPS ABV ROA ROE

P/E P/ABV

March

(` cr)

(%)

(` cr)

(`)

(`)

(%)

(%)

(x)

(x)

FY2016E

18,485

1.9

2,984

13.5

170.0

0.4

7.3

11.2

0.9

FY2017E

21,025

2.0

4,688

21.1

192.2

0.6

10.6

7.1

0.8

Market Outlook

November 9, 2015

Punjab National Bank (CMP: `167/ TP: / Upside: )

PNB reported moderate set of numbers for the quarter with PAT growth of 7.9%

which was below consensus expectations. NII grew at a modest pace of 4.1% yoy

due to tepid loan book growth of 6.7%. Other income de-grew 12.9% yoy which

restricted the operating income growth at 1% yoy. Provisions increased by 6.5%

yoy, which led to 7.9% yoy growth in PAT. On the asset quality front, the bank

found some respite on asset quality with Gross NPA ratio decreasing by 11bp qoq

to 6.36%, while Net NPA decreased by 6bp qoq to 3.99%.At CMP, the stock is

trading at 0.6x FY2017E P/ABV. We recommend a NEUTRAL rating on the stock.

Y/E

Op. Inc

NIM

PAT

EPS ABV ROA ROE

P/E P/ABV

March

(` cr)

(%)

(` cr)

(`)

(`)

(%)

(%)

(x)

(x)

FY2016E

23,638

2.8

3,316

18

180

0.5

8.5

8.0

0.8

FY2017E

26,557

2.8

5,052

27

218

0.7

12.0

5.2

0.7

MT Educare (CMP: `134/ TP: `169 Upside: 26%)

MT Educare’s 2QFY2016 results outperformed our estimates on all parameters. Its

consolidated top-line grew by a healthy ~26% yoy to ~`83cr (our estimate was

of `78.6cr), mainly due to strong growth in Robomate product sales as well as

Government Projects segment. However, core coaching business was subdued

during the quarter. The company reported a consolidated operating profit of

~`22cr, up 19% yoy. The operating margin contracted by 163bp yoy to 27.0%,

primarily on account of higher other costs. The consolidated reported net profit

grew by ~21% yoy to ~`14cr (our estimate was of `12.1cr), due to strong top-line

growth.

Going forward, we expect MT Educare to report strong top-line and bottom-line

growth in the coming financial years (FY2016E and FY2017E) on back of healthy

growth in the coaching business. We expect additional revenue growth from

execution of government projects, Robomate product, and tie up with Shri Gayatri

Educational Society (SGES) in Hyderabad. Currently, we have a BUY rating on the

stock.

Tata Motors (CMP: `396/ TP: `424 /Upside:7%)

Tata Motors 2QFY2016 results were below estimates on the operating front.

Consolidated revenues grew marginally by 1% yoy to `61,318cr (coming slightly

ahead of our estimates of `57,484cr). Growth was subdued mainly due to flattish

growth in JLR. JLR volumes grew a healthy 12% during the quarter but an adverse

mix led to lower realization, thereby dragging the topline. The operating margins

at 11.2% were below our estimates of 13.4%. JLR EBIDTA margins at 12.2% were

significantly below our estimates of 15%. JLR margins were impacted by lower

China sales, adverse product mix and higher launch expenses. During the quarter,

Tata Motors reported a loss at the net level due to a one off charge of `2,493cr

due to JLR vehicles which were destroyed in explosions caused at the China port

location. The company has put an insurance claim for the same which would take

some time for processing but has recognised the loss in the current quarter. During

the quarter, Tata Motors realized tax credit to the tune of `704cr which resulted

into Adj profit at `2,223cr coming in better than our estimates of `2,041cr. We

Market Outlook

November 9, 2015

currently have Accumulate rating on the stock but would review our estimates post

the disappointing performance at JLR.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV

EV/Sales

March

(`cr)

(%)

(`cr)

(`)

(%)

(x)

(x)

(x)

FY2016E

264,038

13.8

11,105

34.5

17.6

11.5

2.0

0.6

FY2017E

297,882

13.9

12,521

38.9

16.8

10.2

1.7

0.6

Banco Products (CMP: `130/ TP: -/ Upside: -)

For 2QFY2016, Banco has posted a good set of numbers. The Consolidated top-

line has grown by 5.8% yoy to `329cr, against our expectation of `320 cr. The

operating performance has improved led by 238bp yoy decline in raw material

cost to `51.8% of sales and employee expense declining by 137bp yoy to 12.3%

of sales. The other expenses have increased by 194bp yoy to 23.2% of sales

resulting in 181bp yoy expansion in EBITDA margin to 12.6%. We had built in an

estimate of 12.1%. The other income was lower as last year the company has

received the proceeds from the sale of cement business. Adjusting for that the

bottom-line grew by 40.7% yoy to `25cr vis-à-vis our estimate of `24cr.

The company had been facing issues in the past year in terms of subdued

environment in Europe affecting its Netherland subsidiary, which accounts for

33.0% of total top-line and Euro depreciation against the Rupee adding to the

assault. There have been a slew of management changes within the company over

the past year.

At the current market price, the stock is trading at 8.4x its FY2017E earnings. We

maintain our Neutral rating on the stock as we await more clarity from the

company and the new management.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,208

11.7

83

11.7

12.8

11.1

1.4

6.2

0.7

FY2017E

1,353

13.0

111

15.5

15.3

8.4

1.2

4.8

0.6

Abbott India (CMP: `5,350/ TP: -/ Upside: -)

For 2QFY2016, Abbott India reported numbers that were below our estimates. The

top-line for the quarter grew by 9.6% yoy to `645cr. The same was lower than our

estimate of `680cr. The other expenses increased during the quarter by 195bp yoy

to 16.1% of sales. The raw material and employee expenses were mostly flat

resulting in EBITDA margin declining by 157bp yoy to 13.4% against our estimate

of 14.5%. Depreciation expense declined by 22.8% yoy to `3cr while other income

increased by 7.0% yoy to `13cr. The net profit during the quarter declined by 1.3%

to `62cr vis-à-vis our estimate of `73cr.

At the current market price, the stock is trading at PE of 38.1x its FY2017E

earnings. We have a Neutral view on the stock.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

2,677

13.4

261

122.8

25.4

43.6

10.2

29.6

4.0

FY2017E

3,108

13.1

299

140.5

24.3

38.1

8.5

25.5

3.4

Market Outlook

November 9, 2015

TVS Srichakra (CMP: `2,803/ TP: `3,240/ Upside: 15.6%)

For 2QFY2016, TVS Srichakra reported a good set of numbers. The top-line grew

by 6.5% yoy to `522cr, against our estimate of `532cr. This is a positive

considering that it is a major 2wheeler tyre manufacturer and the 2W sales have

been lackluster in the current financial year. The EBITDA margin has expanded by

539bp yoy to 15.7% mainly due to 997bp yoy decline in raw material cost (owing

to rubber prices declining by ~6% on qoq basis). We had built in EBITDA margin

estimate of 16.1%. The company has reduced the debt significantly (from `176cr

to `37cr and is now net debt free) in 1HFY2016 and as a result its interest expense

has declined by 57.0% yoy to `4cr. Owing to better operational performance and

lower interest outgo the net profit nearly doubled to `49cr from `36cr in the same

quarter of the previous year (against our estimate of `50cr).

TVS Srichakra has been a clear cut outperformer in the Tyre industry as the 2W

replacement market seems to be unaffected by the cheaper Chinese imports. The

company has been increasing its share in the aftermarket segment which has

enabled it to post strong growth and improve its margins. We remain bullish on

the Stock as it has a leadership position in the OEM segment and will perform well

once the 2W sales improve. Currently, the stock trades at 10.4x its FY2017E

earnings. We have a Buy rating on the stock with a target price of 10.4x its

FY2017E earnings. We have a Buy rating on the stock with a target price of

`3,240 based on target PE of 12.0x.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

2,101

15.7

190

248.6

53.4

11.3

4.9

6.7

1.1

FY2017E

2,338

15.0

207

270.0

39.6

10.4

3.5

6.0

0.9

MM Forgings (CMP: `515/ TP: `614/ Upside:19.2%)

For 2QFY2016, the company reported numbers that disappointed on the top-line

front. The top-line during the quarter grew marginally by 1.8% yoy to `128cr. The

same was below our estimate of `139cr. The raw material cost declined by 111bp

yoy to 39.3% of sales, but the benefits were offset by an increase in employee cost

and power costs. Employee costs and power costs rose by 162bp yoy and 17bp

yoy to 11.1% and 10.4% of sales, respectively. As a result, the EBITDA margin

witnessed a slight decline of 31bp yoy to 21.69, which is in-line our estimate of

22.0%. Consequently, the net profit remained flat at

`13cr vis-à-vis our

expectation of `15cr.

At current market price, the stock is trading at 9.2x its FY2017E earnings. We

maintain our Buy rating on the stock with a revised target price of `614 based on

a target P/E of 11.0x for FY2017E.

Y/E

Sales OPM

PAT

EPS ROE P/E P/BV EV/EBITDA EV/Sales

Mar

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

511

21.7

52

43.1 19.9 16.0

2.2

6.5

1.4

FY2017E

615

21.6

67

55.8 21.2

9.2

1.8

5.0

1.1

Market Outlook

November 9, 2015

Economic and Political News

Grand Alliance secures majority in Bihar polls

Maharashtra govt to disinvest assets in 7 loss-making PSEs

PM announces `80,000cr plan for Jammu and Kashmir

Centre to revive 50 airports in two years

Swachh Bharat Cess of 0.5% on taxable services

Corporate News

Srei Equipment Finance chalks plans for $250-million ECB

Wipro restructures media and telecom business, company veteran Ayan

Mukerji quits

Orient Green Power to exit 20MW Kolhapur power plant

Crisis-hit Tata Steel asks suppliers to slash prices

Market Outlook

November 9, 2015

Top Picks ★★★★★

Large Cap

Market Cap

CMP

Target

Upside

Company

Rationale

(` Cr)

(`)

(`)

(%)

To outpace battery industry growth due to better technological

Amara Raja Batteries

15,145

887

1,040

17.3

products leading to market share gains in both the automotive

OEM and replacement segments.

Earnings to grow strongly given the MHCV cyclical upturn.

Ashok Leyland

24,916

88

111

26.8

Focus on exports and LCV's provides additional growth

avenue.

Healthy pace of branch expansion, backed by distribution

Axis Bank

110,535

465

630

35.5

network, will be the driving force for the bank’s retail business

and overall earnings.

The stock is trading at attractive valuations and is factoring all

HCL Tech

124,478

885

1,132

27.9

the bad news.

Strong visibility for a robust 20% earnings trajectory, coupled

HDFC Bank

272,166

1,081

1,262

16.8

with high quality of earnings on account of high quality retail

business and strategic focus on highly rated corporates.

Due to its robust franchise and capital adequacy position, the

bank is well positioned to grow by at least a few percentage

ICICI Bank

155,326

267

348

30.0

points higher than the average industry growth rate from a

structural point of view.

Back on the growth trend, expect a long term growth of 14%

Infosys

261,404

1,138

1,306

14.8

to be a US$20bn in FY2020.

Well positioned to benefit from such expected gradual

recovery in the overall domestic capex cycle, given its presence

Larsen & Toubro

128,189

1,377

1,646

19.5

across various infrastructure segments, its execution

capabilities, and its strong balance sheet.

LICHF continues to grow its retail loan book at a healthy pace

with improvement in asset quality. We expect the company to

LIC Housing Finance

23,608

468

571

22.0

post a healthy loan book which is likely to reflect in a strong

earnings growth.

Source: Company, Angel Research

Mid Cap

Market Cap

CMP

Target

Upside

Company

Rationale

(` Cr)

(`)

(`)

(%)

Government thrust on Renewable sector and strong order

Inox Wind

8,384

378

505

33.7

book would drive future growth.

Change in business focus towards high-margin chronic and

Ipca labs

8,870

703

900

28.0

lifestyle segments and increasing penetration in Europe and

US

Economic recovery to have favourable impact on advertising &

circulation revenue growth. Further, the acquisition of a radio

Jagran Prakashan

4,678

143

169

18.1

business (Radio City) would also boost the company's revenue

growth.

Strong brand & quality teaching with innovative technologies

MT Educare

534

134

169

25.9

& higher government educational spending to boost growth

Earnings boost on back of stable material prices and

Radico Khaitan

1,374

103

119

15.2

favourable pricing environment. Valuation discount to peers

provides additional comfort

Strong brands and distribution network would boost growth

Siyaram Silk Mills

866

924

1,145

23.9

going ahead. Stock currently trades at an inexpensive

valuation.

Structural shift in the Lighting industry towards LED lighting will

Surya Roshni

556

127

183

44.3

drive growth.

Source: Company, Angel Research

Market Outlook

November 9, 2015

Quarterly Bloomberg Brokers Consensus Estimate

Bank of India - November 9, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

PAT

362

786

(53.9)

130

179.1

Bharat Petroleum Corp Ltd - November 9, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

43,158

61,979

(30.4)

51,917

(16.9)

EBITDA

1,674

1,118

49.8

3,818

(56.2)

EBITDA margin (%)

3.9

1.8

7.4

Net profit

989

464

113.1

2,376

(58.4)

Hindustan Petroleum Corp Ltd - November 9, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

42,205

51,633

(18.3)

51,720

(18.4)

EBITDA

1,185

1,600

(25.9)

3,063

(61.3)

EBITDA margin (%)

2.8

3.1

5.9

Net profit

493

850

(42.0)

1,588

(69.0)

NHPC Ltd - November 9, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

2,238

2,086

7.3

1,986

12.7

EBITDA

1,430

1,288

11.0

1,253

14.1

EBITDA margin (%)

63.9

61.7

63.1

Net profit

842

684

23.1

767

9.8

Rural Electrification Corp Ltd - November 9, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

PAT

1,540

1,501

2.6

1,479

4.2

Tata Power Co Ltd (Consol.) - November 9, 2015

Particulars (` cr)

2QFY16E

2QFY15

y-o-y (%)

1QFY16

q-o-q (%)

Net sales

8,747

8,364

4.6

9,112

(4.0)

EBITDA

1,824

1,692

7.8

1,955

(6.7)

EBITDA margin (%)

20.9

20.2

21.5

Net profit

189

(32)

(684.4)

322

(41.4)

Market Outlook

November 9, 2015

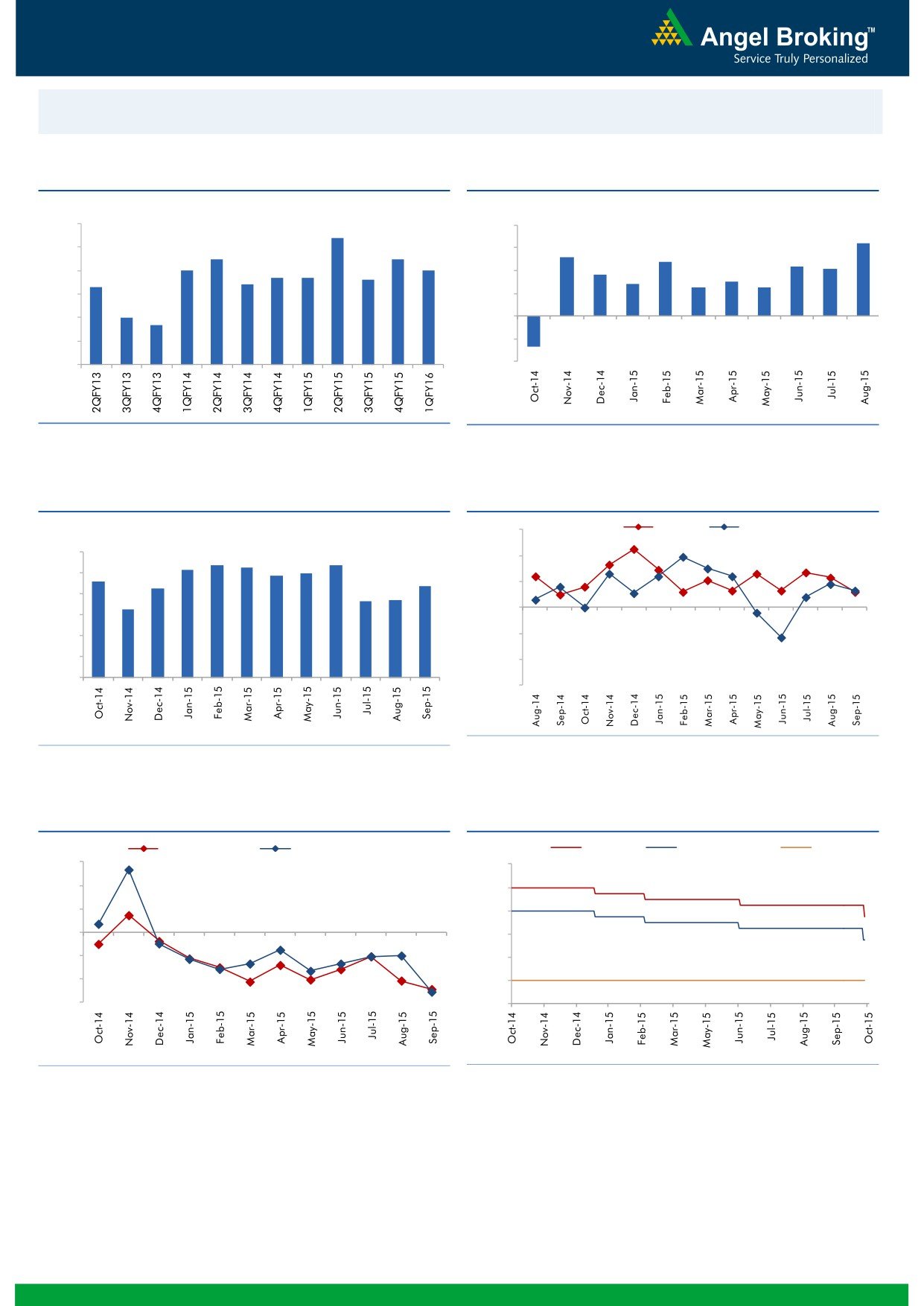

Macro watch

Exhibit 1: Quarterly GDP trends

Exhibit 2: IIP trends

(%)

(%)

9.0

8.4

8.0

6.4

7.5

7.5

5.2

8.0

6.0

4.8

7.0

7.0

4.4

4.1

6.7

6.7

3.6

7.0

6.4

6.6

4.0

2.8

3.0

6.3

2.5

2.5

6.0

2.0

5.0

4.7

5.0

-

4.0

(2.0)

3.0

(4.0)

(2.7)

Source: CSO, Angel Research

Source: MOSPI, Angel Research

Exhibit 3: Monthly CPI inflation trends

Exhibit 4: Manufacturing and services PMI

(%)

56.0

Mfg. PMI

Services PMI

6.0

5.4

5.3

5.4

54.0

5.2

5.0

4.9

4.6

5.0

4.3

4.4

52.0

3.7

3.7

4.0

3.3

50.0

3.0

2.0

48.0

1.0

46.0

-

44.0

Source: Market, Angel Research; Note: Level above 50 indicates expansion

Source: MOSPI, Angel Research

Exhibit 5: Exports and imports growth trends

Exhibit 6: Key policy rates

(%)

Exports yoy growth

Imports yoy growth

(%)

Repo rate

Reverse Repo rate

CRR

30.0

9.00

20.0

8.00

10.0

7.00

0.0

6.00

(10.0)

5.00

(20.0)

4.00

(30.0)

3.00

Source: Bloomberg, Angel Research

Source: RBI, Angel Research

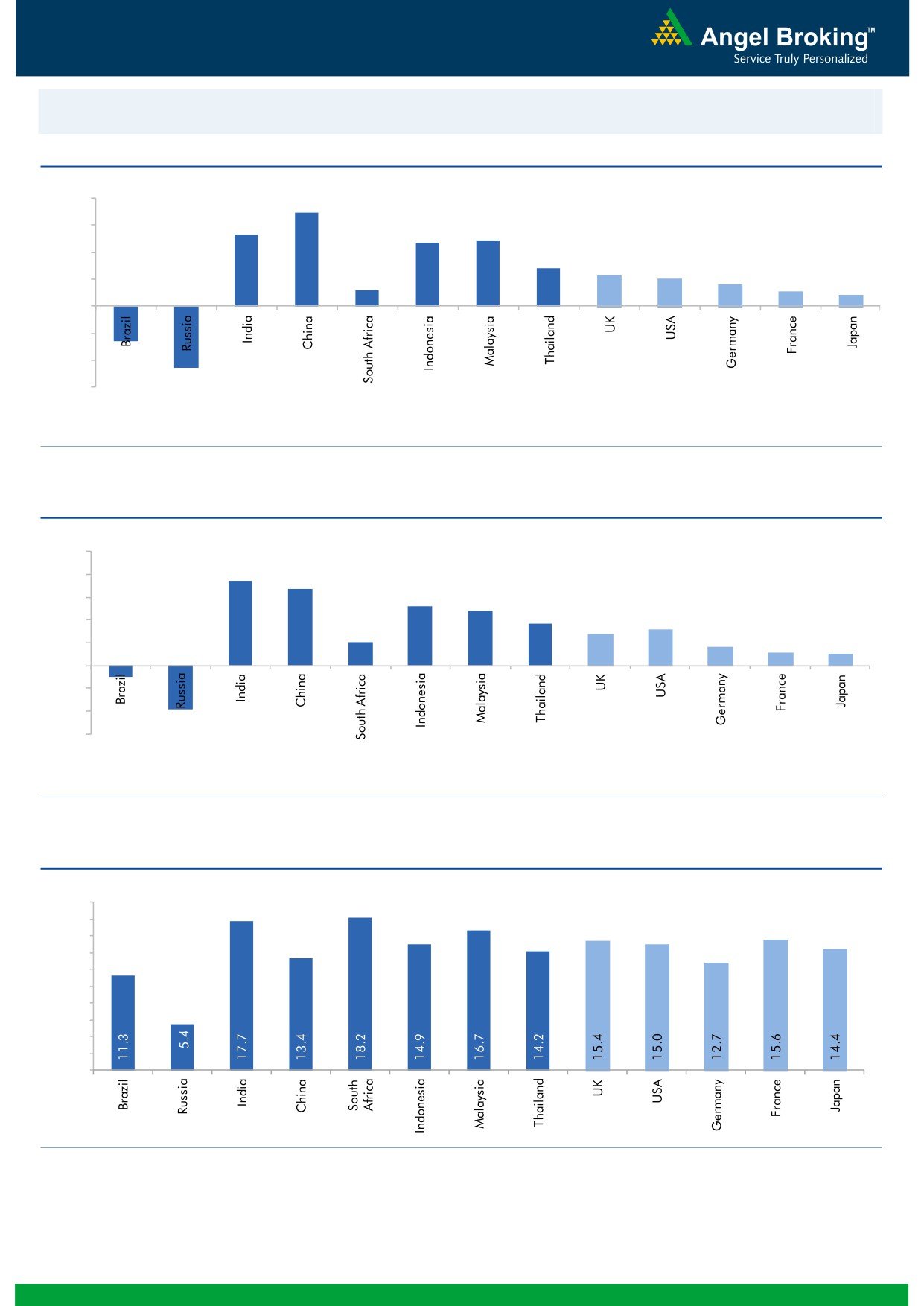

Market Outlook

November 9, 2015

Global watch

Exhibit 1: Latest quarterly GDP Growth (%, yoy) across select developing and developed countries

(%)

8.0

6.9

5.3

6.0

4.9

4.7

4.0

2.8

2.3

2.0

1.6

2.0

1.2

1.1

0.8

(2.6)

-

(2.0)

(4.0)

(4.6)

(6.0)

Source: Bloomberg, Angel Research

Exhibit 2: 2015 GDP Growth projection by IMF (%, yoy) across select developing and developed countries

(%)

10.0

7.5

8.0

6.8

5.2

6.0

4.8

3.7

3.1

4.0

2.7

2.0

1.6

2.0

1.2

1.0

-

(2.0)

(4.0)

(1.0)

(3.8)

(6.0)

Source: IMF, Angel Research

Exhibit 3: One year forward P-E ratio across select developing and developed countries

(x)

20.0

18.0

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2.0

-

Source: IMF, Angel Research

Market Outlook

November 9, 2015

Exhibit 4: Relative performance of indices across globe

Returns (%)

Country

Name of index

Closing price

1M

3M

1YR

Brazil

Bovespa

47,417

(3.2)

(3.5)

(10.8)

Russia

Micex

1,754

1.5

3.1

15.8

India

Nifty

7,954

(2.3)

(6.7)

(4.7)

China

Shanghai Composite

3,590

12.8

(8.6)

48.5

South Africa

Top 40

47,541

0.6

2.0

5.3

Mexico

Mexbol

45,244

2.1

(0.2)

1.6

Indonesia

LQ45

784

(1.6)

(3.0)

(7.1)

Malaysia

KLCI

1,686

(1.4)

1.9

(7.8)

Thailand

SET 50

914

(0.7)

(1.5)

(12.4)

USA

Dow Jones

17,910

4.8

1.7

1.9

UK

FTSE

6,364

(1.0)

(5.7)

(3.3)

Japan

Nikkei

19,266

4.5

(7.4)

14.1

Germany

DAX

10,988

8.6

(5.3)

17.5

France

CAC

4,984

6.3

(4.1)

18.0

Source: Bloomberg, Angel Research

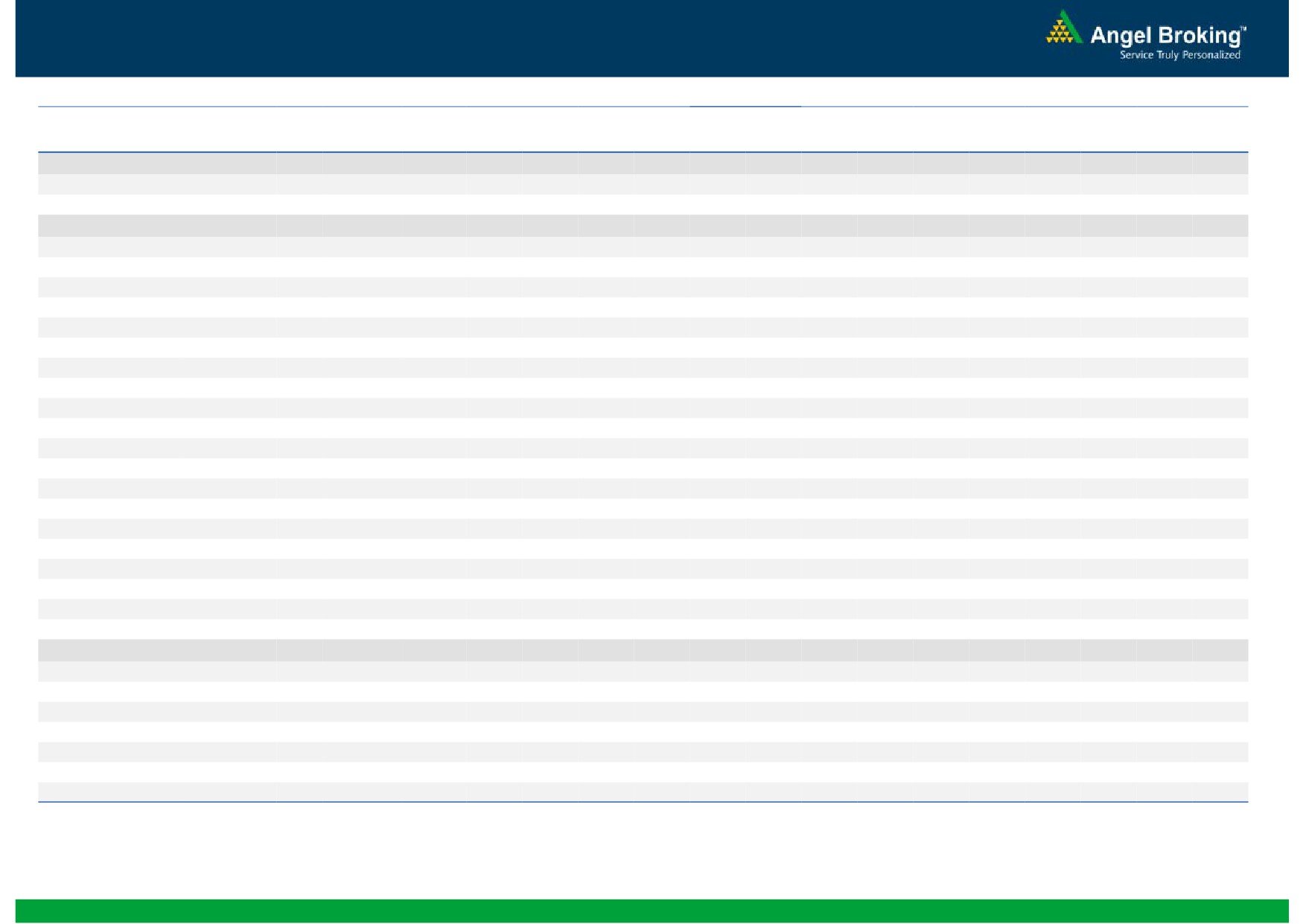

Stock Watch

November 09, 2015

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Agri / Agri Chemical

Rallis

Neutral

196

-

3,810

2,075

2,394

14.4

14.4

9.5

11.0

20.6

17.8

4.1

3.5

21.1

21.3

1.9

1.6

United Phosphorus

Buy

448

510

19,219

13,698

15,752

17.6

17.6

32.1

38.5

14.0

11.7

2.7

2.3

21.4

21.3

1.5

1.2

Auto & Auto Ancillary

Ashok Leyland

Buy

88

111

24,916

18,763

22,357

11.1

11.2

3.6

4.8

24.3

18.2

4.5

4.1

18.7

22.6

1.3

1.0

Bajaj Auto

Accumulate

2,423

2,672

70,111

24,115

27,600

21.3

21.0

136.8

157.2

17.7

15.4

5.7

4.9

32.2

31.5

2.5

2.1

Eicher Motors

Buy

16,693

22,900

45,308

11,809

15,609

15.5

17.0

362.9

567.0

46.0

29.4

14.0

10.4

30.1

35.0

4.0

3.0

Hero Motocorp

Neutral

2,633

-

52,576

28,561

31,559

14.7

14.7

151.1

163.2

17.4

16.1

6.8

5.8

38.7

35.6

1.7

1.5

L G Balakrishnan & Bros Neutral

470

-

738

1,254

1,394

11.6

11.8

35.9

41.7

13.1

11.3

1.8

1.6

13.5

13.8

0.7

0.6

Mahindra and Mahindra Neutral

1,248

-

77,522

37,231

41,710

12.4

12.8

48.8

58.3

25.6

21.4

3.6

3.2

14.0

14.9

1.8

1.5

Maruti

Accumulate

4,523

4,960

136,628

57,865

68,104

16.4

16.7

176.3

225.5

25.7

20.1

5.0

4.2

19.4

21.2

2.1

1.8

Minda Industries

Accumulate

749

809

1,188

2,567

2,965

8.0

8.3

46.1

57.8

16.3

13.0

2.7

2.2

16.7

17.3

0.5

0.4

Rane Brake Lining

Accumulate

333

366

263

454

511

11.1

11.4

23.8

28.1

14.0

11.8

2.0

1.8

14.2

15.3

0.7

0.6

Setco Automotive

Neutral

211

-

563

594

741

12.7

13.7

8.4

15.8

25.1

13.3

2.6

2.3

10.4

16.9

1.4

1.2

Tata Motors

Accumulate

396

424

114,405

264,038

297,882

13.8

13.9

34.5

38.9

11.5

10.2

1.9

1.6

17.6

16.8

0.6

0.6

TVS Motor

Accumulate

283

313

13,438

11,845

14,040

7.2

9.0

10.4

17.4

27.2

16.3

6.8

5.2

25.1

32.0

1.1

0.9

Amara Raja Batteries

Buy

887

1,040

15,145

4,892

5,871

17.4

17.6

28.8

37.1

30.8

23.9

7.2

5.8

23.4

24.1

3.0

2.5

Exide Industries

Accumulate

143

162

12,164

6,950

7,784

14.4

14.8

6.6

7.3

21.7

19.6

2.7

2.5

12.6

12.8

1.5

1.3

Apollo Tyres

Neutral

159

-

8,081

12,576

12,978

16.8

16.1

22.3

19.9

7.1

8.0

1.2

1.1

17.2

13.4

0.7

0.8

Ceat

Accumulate

1,015

1,119

4,107

6,041

6,597

14.1

13.7

99.5

111.9

10.2

9.1

2.0

1.7

19.6

18.5

0.8

0.7

JK Tyres

Neutral

93

-

2,108

7,446

7,669

15.2

14.0

19.6

18.4

4.7

5.1

1.2

1.0

25.2

19.5

0.7

0.6

Swaraj Engines

Neutral

945

-

1,173

552

630

14.2

14.7

44.6

54.1

21.2

17.5

4.9

4.5

23.2

25.6

2.0

1.7

Subros

Neutral

84

-

502

1,268

1,488

11.6

11.9

3.7

6.6

22.6

12.7

1.5

1.4

6.8

11.4

0.7

0.6

Indag Rubber

Neutral

194

-

508

283

329

17.0

17.2

13.0

15.4

14.9

12.5

3.3

2.7

21.8

21.6

1.6

1.3

Capital Goods

ACE

Neutral

43

-

428

660

839

4.7

8.2

1.0

3.9

43.3

11.1

1.4

1.2

3.2

11.3

0.8

0.6

BEML

Neutral

1,109

-

4,617

3,277

4,006

6.0

8.9

29.2

64.3

38.0

17.2

2.1

1.9

5.7

11.7

1.5

1.2

BGR Energy

Neutral

109

-

785

3,615

3,181

9.5

9.4

16.7

12.4

6.5

8.8

0.6

0.6

10.0

7.0

0.6

0.8

BHEL

Neutral

192

-

46,945

33,722

35,272

10.8

11.7

10.5

14.2

18.3

13.5

1.4

1.3

7.0

9.0

1.5

1.4

Blue Star

Accumulate

352

382

3,162

3,624

4,157

5.3

6.0

9.6

14.5

36.5

24.3

6.7

5.7

18.6

25.4

1.0

0.9

Crompton Greaves

Buy

169

204

10,586

13,484

14,687

4.9

6.2

4.5

7.1

37.5

23.8

2.7

2.5

7.2

10.8

0.9

0.8

Inox Wind

Buy

378

505

8,384

4,980

5,943

17.0

17.5

26.6

31.6

14.2

12.0

4.2

3.1

35.0

30.0

1.9

1.5

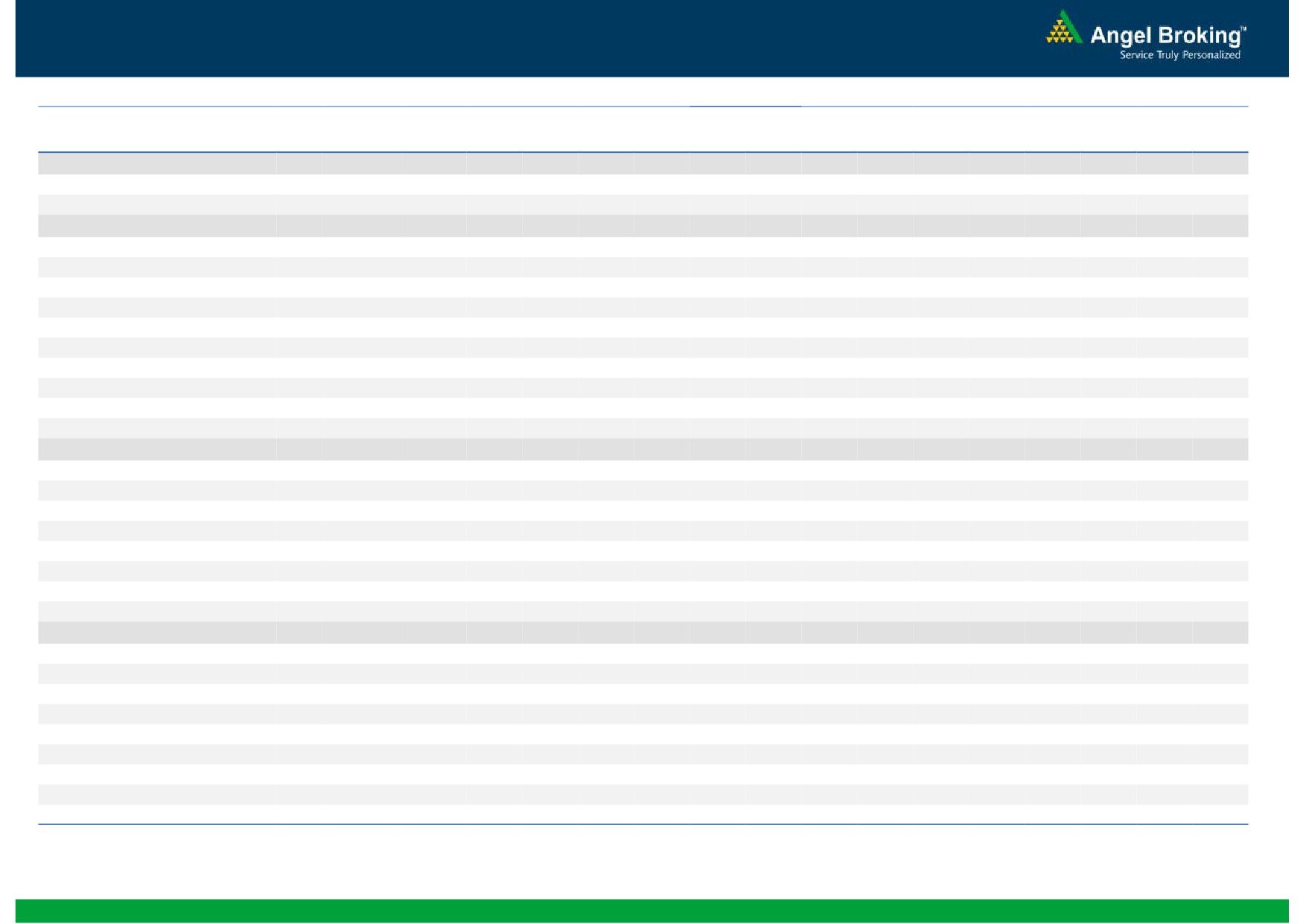

Stock Watch

November 09, 2015

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Capital Goods

KEC International

Neutral

137

-

3,523

8,791

9,716

6.1

6.8

5.4

8.2

25.4

16.7

2.5

2.3

10.0

14.0

0.6

0.6

Thermax

Neutral

848

-

10,107

6,413

7,525

7.4

8.5

30.5

39.3

27.8

21.6

4.3

3.7

15.0

17.0

1.6

1.3

Cement

ACC

Buy

1,386

1,630

26,016

13,151

14,757

16.4

18.3

63.9

83.4

21.7

16.6

2.8

2.6

13.3

16.1

1.8

1.5

Ambuja Cements

Accumulate

210

233

32,559

11,564

12,556

19.4

20.7

8.9

10.1

23.6

20.8

3.0

2.8

12.8

13.8

2.4

2.2

India Cements

Buy

79

112

2,419

4,216

4,840

18.0

19.5

4.0

9.9

19.7

8.0

0.8

0.7

4.0

9.5

0.9

0.7

JK Cement

Accumulate

648

744

4,528

3,661

4,742

10.1

15.8

18.0

61.0

36.0

10.6

2.6

2.3

7.5

22.9

1.7

1.3

J K Lakshmi Cement

Buy

354

430

4,168

2,947

3,616

16.7

19.9

11.5

27.2

30.8

13.0

2.9

2.5

9.8

20.8

1.8

1.5

Mangalam Cements

Neutral

209

-

557

1,053

1,347

10.5

13.3

8.4

26.0

24.9

8.0

1.1

1.0

4.3

12.5

0.9

0.7

Orient Cement

Accumulate

164

183

3,351

1,854

2,524

21.2

22.2

7.7

11.1

21.2

14.7

3.1

2.6

13.3

15.7

2.6

1.8

Ramco Cements

Neutral

374

-

8,898

4,036

4,545

20.8

21.3

15.1

18.8

24.8

19.9

3.0

2.7

12.9

14.3

2.7

2.3

Shree Cement^

Neutral

11,999

-

41,800

7,150

8,742

26.7

28.6

228.0

345.5

52.6

34.7

7.8

6.5

15.7

20.3

5.6

4.5

UltraTech Cement

Buy

2,792

3,282

76,604

25,021

30,023

19.1

21.6

89.0

132.0

31.4

21.2

3.6

3.2

12.2

15.9

3.2

2.7

Construction

ITNL

Neutral

90

-

2,957

7,360

8,825

34.0

35.9

1.0

5.0

89.9

18.0

0.4

0.4

0.3

1.4

3.8

3.7

KNR Constructions

Neutral

561

-

1,577

915

1,479

14.3

13.9

20.3

37.2

27.6

15.1

2.5

2.2

9.6

15.6

1.9

1.2

Larsen & Toubro

Buy

1,377

1,646

128,189

64,148

73,241

11.5

11.7

62.0

66.0

22.2

20.9

2.3

2.1

13.4

14.0

2.2

1.9

Gujarat Pipavav Port

Neutral

165

-

7,960

629

684

51.0

52.2

6.4

5.9

25.7

27.9

3.4

3.1

15.9

12.7

12.2

11.0

MBL Infrastructures

Buy

212

285

881

2,313

2,797

12.2

14.6

19.0

20.0

11.2

10.6

1.2

1.1

11.3

10.6

1.1

1.0

Nagarjuna Const.

Neutral

74

-

4,108

7,892

8,842

8.3

9.1

2.4

5.3

30.8

13.9

1.2

1.2

4.2

8.6

0.8

0.7

PNC Infratech

Neutral

523

-

2,681

1,798

2,132

13.2

13.5

22.0

30.0

23.8

17.4

2.1

1.9

11.5

11.4

1.6

1.3

Simplex Infra

Neutral

307

-

1,519

6,241

7,008

10.4

10.7

20.0

36.0

15.4

8.5

1.3

1.1

6.8

11.1

0.8

0.6

Financials

Allahabad Bank

Neutral

74

-

4,471

8,332

9,259

2.8

2.8

21.0

25.6

3.5

2.9

0.4

0.3

9.8

10.9

-

-

Axis Bank

Buy

465

630

110,535

26,473

31,527

3.5

3.6

35.7

43.5

13.0

10.7

2.5

2.2

17.9

18.9

-

-

Bank of Baroda

Neutral

167

-

38,572

19,105

21,474

2.0

2.0

19.1

24.8

8.8

6.8

0.9

0.8

10.2

12.1

-

-

Bank of India

Neutral

134

-

10,643

15,972

17,271

1.9

2.0

15.3

33.4

8.8

4.0

0.4

0.3

3.6

7.6

-

-

Canara Bank

Neutral

275

-

14,930

15,251

16,725

2.0

2.0

59.3

68.6

4.6

4.0

0.5

0.4

10.1

10.7

-

-

Dena Bank

Neutral

43

-

2,421

3,440

3,840

2.1

2.3

7.3

10.0

6.0

4.3

0.5

0.4

6.1

7.9

-

-

Federal Bank

Neutral

55

-

9,372

3,477

3,999

3.0

3.0

5.0

6.2

10.9

8.8

1.1

1.0

10.6

11.9

-

-

HDFC

Neutral

1,206

-

190,244

10,358

11,852

3.3

3.3

41.1

47.0

29.4

25.6

5.6

5.1

24.7

24.9

-

-

HDFC Bank

Buy

1,081

1,262

272,166

38,309

47,302

4.3

4.3

49.3

61.1

21.9

17.7

3.8

3.3

18.5

19.7

-

-

Stock Watch

November 09, 2015

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Financials

ICICI Bank

Buy

267

348

155,326

35,168

40,517

3.4

3.4

21.4

25.2

12.5

10.6

2.1

1.8

14.7

15.2

-

-

IDBI Bank

Neutral

85

-

13,578

9,625

10,455

1.8

1.8

8.5

14.2

9.9

6.0

0.6

0.6

5.9

9.3

-

-

Indian Bank

Neutral

128

-

6,138

6,160

6,858

2.5

2.5

24.5

29.8

5.2

4.3

0.4

0.4

7.7

8.6

-

-

LIC Housing Finance

Buy

468

571

23,608

3,101

3,745

2.5

2.5

33.0

40.2

14.2

11.7

2.7

2.3

19.7

20.5

-

-

Oriental Bank

Neutral

145

-

4,355

7,643

8,373

2.4

2.4

37.2

45.4

3.9

3.2

0.3

0.3

8.2

9.4

-

-

Punjab Natl.Bank

Neutral

133

-

26,077

23,638

26,557

2.8

2.8

17.9

27.2

7.4

4.9

0.7

0.6

8.5

12.0

-

-

South Ind.Bank

Neutral

21

-

2,775

1,965

2,185

2.5

2.5

2.5

3.3

8.3

6.2

0.8

0.7

9.5

11.7

-

-

St Bk of India

Buy

243

283

188,830

82,520

93,299

2.7

2.8

20.0

24.5

12.1

9.9

1.3

1.2

11.5

12.8

-

-

Union Bank

Neutral

163

-

11,205

12,646

14,129

2.3

2.4

31.0

39.1

5.3

4.2

0.6

0.5

9.8

11.4

-

-

Vijaya Bank

Neutral

34

-

2,921

3,536

3,827

1.9

1.9

5.5

6.7

6.2

5.1

0.5

0.5

7.8

8.8

-

-

Yes Bank

Buy

758

914

31,762

7,228

9,043

3.2

3.3

57.7

69.4

13.1

10.9

2.3

2.0

19.1

19.6

-

-

FMCG

Asian Paints

Neutral

802

-

76,947

16,553

19,160

16.0

16.2

17.7

21.5

45.4

37.3

12.1

10.8

29.4

31.2

4.5

3.9

Britannia

Neutral

3,123

-

37,470

8,065

9,395

9.6

10.2

47.2

65.5

66.2

47.7

22.0

20.8

38.3

41.2

4.6

3.9

Colgate

Neutral

939

-

25,533

4,836

5,490

19.5

19.7

48.5

53.2

19.4

17.6

14.2

12.4

99.8

97.5

5.2

4.6

Dabur India

Neutral

268

-

46,995

9,370

10,265

17.1

17.2

7.3

8.1

36.5

33.0

11.0

9.0

33.7

30.6

4.9

4.5

GlaxoSmith Con*

Neutral

5,902

-

24,820

4,919

5,742

17.2

17.4

168.3

191.2

35.1

30.9

10.0

8.5

28.8

28.9

4.6

3.9

Godrej Consumer

Neutral

1,304

-

44,392

10,168

12,886

16.1

16.1

32.1

38.4

40.6

34.0

8.3

7.6

19.7

21.0

4.3

3.4

HUL

Neutral

799

-

172,861

34,940

38,957

17.5

17.7

20.8

24.7

38.4

32.3

42.7

34.1

110.5

114.2

4.8

4.3

ITC

Buy

337

409

270,413

41,068

45,068

37.8

37.4

13.9

15.9

24.2

21.2

8.1

7.1

34.1

33.8

6.2

5.6

Marico

Neutral

403

-

25,968

6,551

7,766

15.7

16.0

10.4

12.5

38.8

32.2

11.3

9.4

33.2

32.4

3.9

3.3

Nestle*

Accumulate

6,172

6,646

59,506

11,291

12,847

22.2

22.3

158.9

184.6

38.8

33.4

20.3

18.3

55.0

57.3

5.1

4.5

Tata Global

Accumulate

126

144

7,933

8,635

9,072

9.8

9.9

6.5

7.6

19.4

16.6

1.9

1.9

6.8

7.4

0.9

0.8

IT

HCL Tech^

Buy

885

1,132

124,478

42,038

47,503

23.2

23.5

55.8

62.9

15.9

14.1

3.6

2.8

23.0

19.8

2.5

2.0

Infosys

Buy

1,138

1,306

261,404

60,250

66,999

28.0

28.0

58.3

63.7

19.5

17.9

4.1

3.5

20.9

19.7

3.6

3.1

TCS

Buy

2,506

3,165

493,740

111,274

126,852

28.4

28.7

125.4

143.9

20.0

17.4

7.9

7.3

39.9

42.2

4.0

3.5

Tech Mahindra

Buy

533

646

51,252

25,566

28,890

16.0

17.0

26.3

31.9

20.3

16.7

3.6

3.1

17.9

18.6

1.8

1.5

Wipro

Buy

572

719

141,167

52,414

58,704

23.7

23.8

38.4

42.3

14.9

13.5

2.9

2.6

19.5

18.0

2.3

1.9

Media

D B Corp

Accumulate

319

356

5,863

2,241

2,495

27.8

27.9

21.8

25.6

14.7

12.5

3.8

3.4

26.7

28.5

2.5

2.2

HT Media

Neutral

78

-

1,824

2,495

2,603

11.2

11.2

7.3

8.6

10.7

9.1

0.9

0.8

7.4

8.1

0.2

0.2

Stock Watch

November 09, 2015

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Media

Jagran Prakashan

Buy

143

169

4,678

2,170

2,355

27.0

27.6

12.8

10.3

11.2

13.9

3.1

2.9

21.8

19.4

1.9

1.6

Sun TV Network

Neutral

364

-

14,349

2,779

3,196

70.2

70.5

22.8

27.3

16.0

13.3

3.9

3.6

26.7

28.3

5.2

4.5

Hindustan Media

Neutral

279

-

2,049

920

1,031

20.0

20.0

19.2

20.9

14.5

13.4

2.4

2.1

16.4

15.3

1.7

1.5

Ventures

Metals & Mining

Coal India

Buy

342

400

215,799

77,508

85,330

21.4

23.7

24.8

27.6

13.8

12.4

5.3

5.0

38.6

41.6

2.1

1.8

Hind. Zinc

Accumulate

153

175

64,626

14,641

14,026

50.4

50.4

17.7

16.0

8.7

9.6

1.3

1.2

16.2

13.2

2.1

1.9

Hindalco

Neutral

81

-

16,706

104,356

111,186

8.7

9.5

6.7

11.1

12.0

7.3

0.4

0.4

3.5

5.9

0.7

0.6

JSW Steel

Neutral

872

-

21,083

42,308

45,147

16.4

20.7

(10.3)

49.5

17.6

1.0

0.9

(1.0)

5.6

1.5

1.4

NMDC

Neutral

93

-

36,912

8,237

10,893

46.6

44.5

10.0

11.7

9.4

8.0

1.0

0.9

12.5

13.0

4.3

3.3

SAIL

Neutral

47

-

19,453

45,915

53,954

7.2

10.5

1.5

4.4

31.3

10.8

0.5

0.4

2.3

4.1

1.1

1.0

Vedanta

Neutral

92

-

27,349

71,445

81,910

26.2

26.3

12.9

19.2

7.2

4.8

0.5

0.4

7.2

8.9

0.8

0.6

Tata Steel

Neutral

220

-

21,376

126,760

137,307

8.9

11.3

6.4

23.1

34.6

9.5

0.7

0.7

2.0

7.1

0.8

0.7

Oil & Gas

Cairn India

Neutral

151

-

28,254

11,323

12,490

49.4

51.0

20.7

20.7

7.3

7.3

0.5

0.5

6.4

6.1

1.6

0.9

GAIL

Neutral

289

-

36,615

64,856

70,933

9.1

9.6

24.0

28.9

12.1

10.0

1.0

1.0

8.8

9.6

0.8

0.7

ONGC

Neutral

252

-

215,513

154,564

167,321

36.8

37.4

28.6

32.5

8.8

7.8

1.1

1.0

12.7

13.5

1.6

1.5

Petronet LNG

Neutral

201

-

15,094

29,691

31,188

5.8

6.2

12.8

13.4

15.7

15.0

2.4

2.1

15.8

14.8

0.6

0.5

Indian Oil Corp

Accumulate

412

455

99,947

359,607

402,760

5.9

6.1

42.5

48.7

9.7

8.5

1.3

1.2

14.1

14.4

0.4

0.3

Reliance Industries

Accumulate

952

1,050

308,444

304,775

344,392

12.6

13.4

91.3

102.6

10.4

9.3

1.2

1.1

11.8

12.0

0.9

0.8

Pharmaceuticals

Alembic Pharma

Neutral

667

-

12,566

2,601

3,115

21.2

20.2

20.8

23.9

32.1

27.9

10.3

7.8

37.2

31.8

4.9

4.0

Aurobindo Pharma

Accumulate

813

872

47,491

14,923

17,162

23.0

23.0

38.2

43.6

21.3

18.7

6.6

4.9

36.0

30.2

3.6

3.0

Aventis*

Neutral

4,310

-

9,926

2,082

2,371

17.4

20.8

118.2

151.5

36.5

28.5

5.3

4.3

19.9

25.5

4.4

3.7

Cadila Healthcare

Neutral

411

-

42,096

10,224

11,840

21.0

22.0

14.6

17.6

28.2

23.4

7.7

6.0

30.8

29.0

4.4

3.7

Cipla

Neutral

658

-

52,840

14,359

16,884

21.3

19.7

28.4

30.5

23.2

21.6

4.1

3.5

19.3

17.5

3.7

3.1

Dr Reddy's

Neutral

3,630

-

61,890

18,213

21,214

22.6

22.7

163.0

192.5

22.3

18.9

4.6

3.8

22.5

20.0

3.9

3.3

Dishman Pharma

Neutral

388

-

3,132

1,716

1,888

20.2

20.2

16.3

21.6

23.8

18.0

2.2

2.0

9.7

11.7

2.1

1.7

GSK Pharma*

Neutral

3,192

-

27,036

2,870

3,158

20.0

22.1

59.5

68.3

53.6

46.7

15.8

16.3

28.5

34.3

8.9

8.2

Indoco Remedies

Neutral

305

-

2,810

1,088

1,262

18.2

18.2

13.1

15.5

23.3

19.7

4.6

3.8

21.2

21.1

2.7

2.3

Ipca labs

Buy

703

900

8,870

3,363

3,909

12.9

18.6

13.4

28.0

52.5

25.1

6.8

5.5

7.4

14.0

3.0

2.6

Lupin

Neutral

1,853

-

83,432

14,864

17,244

26.9

26.9

62.1

71.1

29.8

26.1

7.2

5.7

27.4

24.6

5.3

4.4

Sun Pharma

Buy

804

950

193,405

28,163

32,610

25.8

30.7

17.4

26.9

46.2

29.9

4.4

3.8

13.0

16.6

6.4

5.3

Stock Watch

November 09, 2015

Company Name

Reco

CMP

Target

Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

FY16E

FY17E

Power

Tata Power

Neutral

68

-

18,283

35,923

37,402

22.6

22.8

4.1

5.2

16.7

13.1

1.3

1.2

7.5

9.3

1.5

1.3

NTPC

Buy

135

157

111,520

87,064

98,846

23.5

23.5

11.7

13.2

11.6

10.3

1.3

1.2

11.4

12.1

2.3

2.1

Power Grid

Buy

131

170

68,586

20,702

23,361

86.7

86.4

12.1

13.2

10.9

9.9

1.6

1.4

15.6

15.1

8.2

7.7

Telecom

Bharti Airtel

Neutral

339

-

135,512

101,748

109,191

32.1

31.7

12.0

12.5

28.3

27.1

1.9

1.8

6.9

6.7

2.0

1.8

Idea Cellular

Neutral

139

-

50,107

34,282

36,941

32.0

31.5

5.9

6.2

23.6

22.5

2.2

2.0

9.9

9.3

2.0

1.9

zOthers

Abbott India

Neutral

5,350

-

11,369

2,715

3,153

14.5

14.1

134.3

152.2

39.9

35.1

9.9

8.2

27.4

25.6

4.0

3.4

Bajaj Electricals

Buy

239

341

2,408

4,719

5,287

5.2

5.8

8.6

12.7

27.9

18.9

3.2

2.8

11.4

14.8

0.5

0.5

Finolex Cables

Neutral

240

-

3,665

2,728

3,036

10.8

11.0

14.4

16.8

16.6

14.3

2.5

2.2

15.2

15.3

1.1

0.9

Goodyear India*

Accumulate

560

622

1,292

1,888

1,680

12.1

11.9

62.2

56.6

9.0

9.9

2.1

1.8

25.9

19.7

0.5

0.5

Hitachi

Neutral

1,347

-

3,662

1,779

2,081

7.8

8.8

21.8

33.4

61.8

40.3

10.0

8.1

17.4

22.1

2.1

1.8

Jyothy Laboratories

Neutral

305

-

5,515

1,620

1,847

11.5

11.5

7.3

8.5

41.8

35.9

5.4

5.0

13.3

14.4

3.3

2.8

MRF

Buy

38,512

45,575

16,334

20,316

14,488

21.4

21.1

5,488.0

3,798.0

7.0

10.1

2.4

1.9

41.1

21.2

0.8

1.0

Page Industries

Neutral

13,462

-

15,016

1,929

2,450

19.8

20.1

229.9

299.0

58.6

45.0

25.8

18.0

52.1

47.1

7.9

6.2

Relaxo Footwears

Neutral

503

-

6,039

1,767

2,152

12.3

12.5

19.3

25.1

26.2

20.1

6.4

4.9

27.7

27.8

3.6

2.9

Siyaram Silk Mills

Buy

924

1,145

866

1,636

1,815

11.5

11.5

89.9

104.1

10.3

8.9

1.7

1.5

17.9

17.8

0.7

0.6

Styrolution ABS India*

Neutral

717

-

1,261

1,271

1,440

8.6

9.2

32.0

41.1

22.4

17.5

2.3

2.1

10.7

12.4

1.0

0.9

Tree House

Buy

261

347

1,102

259

324

56.8

56.8

17.0

21.7

15.3

12.0

1.5

1.4

10.1

11.5

4.3

3.6

TVS Srichakra

Buy

2,803

3,210

2,146

2,127

2,388

15.2

14.9

237.7

267.5

11.8

10.5

5.0

3.6

51.7

39.8

1.1

0.9

HSIL

Accumulate

279

302

2,013

2,123

2,384

16.1

16.5

15.0

18.9

18.5

14.8

1.4

1.3

8.0

9.4

1.3

1.1

Kirloskar Engines India

Neutral

263

-

3,798

2,634

3,252

10.1

12.0

10.9

17.4

24.1

15.1

2.7

2.4

11.4

16.8

1.1

0.8

Ltd

M M Forgings

Buy

515

670

621

541

634

21.7

21.4

47.8

55.9

10.8

9.2

2.1

1.8

21.8

20.9

1.3

1.1

Banco Products (India)

Neutral

130

-

928

1,208

1,353

11.0

12.3

10.8

14.5

12.0

9.0

1.4

1.2

11.9

14.5

0.7

0.6

Competent Automobiles Neutral

135

-

83

1,007

1,114

3.1

3.1

23.7

28.2

5.7

4.8

0.8

0.7

13.9

14.6

0.1

0.1

Nilkamal

Neutral

997

-

1,487

1,910

2,083

10.5

10.3

63.3

69.2

15.7

14.4

2.6

2.2

17.6

16.5

0.9

0.8

Visaka Industries

Buy

131

166

208

1,158

1,272

8.6

9.5

23.7

32.7

5.5

4.0

0.6

0.5

10.1

12.5

0.3

0.3

Transport Corporation of

Neutral

271

-

2,059

2,830

3,350

8.8

9.0

14.4

18.3

18.8

14.8

2.9

2.5

15.4

17.1

0.9

0.7

India

Elecon Engineering

Accumulate

77

85

839

1,369

1,533

13.7

14.9

3.3

6.1

23.2

12.7

1.5

1.4

6.6

11.4

1.0

0.9

Surya Roshni

Buy

127

183

556

2,992

3,223

8.1

8.4

14.7

18.3

8.6

6.9

0.8

0.7

9.7

11.0

0.5

0.4

MT Educare

Buy

134

169

534

286

366

18.3

17.7

7.7

9.4

17.4

14.3

3.7

3.2

20.2

21.1

1.8

1.4

Stock Watch

November 09, 2015

Company Name

Reco

CMP

Target Mkt Cap

Sales ( Čcr )

OPM(%)

EPS (Č)

PER(x)

P/BV(x)

RoE(%)

EV/Sales(x)

(Č)

Price ( Č)

( Č cr )

FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E FY16E FY17E

zOthers

Radico Khaitan

Accumulate

103

119

1,374

1,565

1,687

11.9

12.4

5.4

6.6

19.1

15.7

1.5

1.4

8.0

9.0

1.4

1.3

Garware Wall Ropes

Buy

347

423

760

875

983

10.4

10.6

23.1

27.8

15.0

12.5

2.1

1.8

14.1

14.8

0.9

0.7

Wonderla Holidays

Neutral

332

-

1,873

206

308

44.0

43.6

9.0

12.9

36.8

25.7

5.0

4.6

13.7

17.8

9.0

6.0

Linc Pen & Plastics

Accumulate

162

185

240

340

371

8.3

8.9

10.8

13.2

15.0

12.3

2.4

2.1

16.0

17.1

0.8

0.7

The Byke Hospitality

Buy

160

181

642

222

287

20.5

20.5

5.6

7.6

28.4

21.2

5.4

4.4

18.9

20.8

2.8

2.2

Source: Company, Angel Research; Note: *December year end; #September year end; &October year end; Price as on November 06, 2015

Market Outlook

November 09, 2015

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitian Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial ownership

of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation / managed or co

-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst has not served as

an officer, director or employee of company covered by Analyst and has not been engaged in market making activity of the company

covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way responsible for any

loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Pvt.

Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any

representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking

Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance,

or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or

in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may have

investment positions in the stocks recommended in this report.