IPO Note | Capital Goods / Renewable Energy

March 17, 2015

Inox Wind

SUBSCRIBE

Issue Open: March 18, 2015

IPO Note - Strong growth prospects; Subscribe

Issue Close: March 20, 2015

Company background: Inox Wind Ltd (IWL), incorporated in 2009 and a part of

the Inox Group, is one of the leading manufacturers of wind turbine generators

Issue Details

(WTG’s) in India. The company also provides turnkey solutions, and operation

Face Value: `10

and maintenance services for wind power projects. Currently, IWL has an installed

Present Eq. Paid up Capital: `200cr

capacity of 550 nacelles and hubs, 256 rotor blade sets and a capacity of 150

towers. The company is setting up a new integrated capacity which would take the

Fresh Issue**: 2.12cr Shares

total nacelles and hubs capacity to 950 units, rotor blades capacity to 800 sets

Offer for Sale: 1.0cr Shares

and tower capacity to 600 units.

Post Eq. Paid up Capital**: `221.54cr

Strong order book: IWL has shown a strong growth during FY2014 and

Issue size (amount)**: `1,014cr - `1,046cr

9MFY2015 periods, wherein it sold 330MW and 380MW of WTGs during the

period; plus, it also has a strong order book (as of December 2014). Currently

Price Band**: `315-325

IWL has an order book of

1,136MW, as against Suzlon’s order book

Post-issue implied mkt. cap**: `6,999.3cr-

7,221.5cr

of 1,148MW, and Gamesa India Pvt Ltd’s order inflow of 850MW (as of

Promoters holding Pre-Issue: 100.0%

December 2014). These provide strong revenue visibility for FY2016.

Promoters holding Post-Issue: 85.5%

IWL has access to wind project sites which have been acquired or are under the

Note:**at Lower and Upper price band respectively

acquisition process by its group companies - GFL and IRL - and its subsidiary

IWISL. Currently the wind sites acquired have an aggregate power project

capacity of 2,130MW, while the wind sites which are under the acquisition

Book Building

process have a power project capacity of 1,922MW. Thus, it provides healthy

QIBs

50% of issue

revenue visibility for IWL in the medium term.

Non-Institutional

At least 15%

Government focus on renewable energy: The government has set a target of

Retail

At least 35%

installed wind power capacity of 60,000MW till FY2022 from the current capacity

of 21,150MW. This will create a huge opportunity for the company in the

upcoming period. Hence we expect order inflow to increase at a faster pace

Post Issue Shareholding Pattern

during the next few years. We expect industry order flow to come in at the run rate

Promoters Group

85.5

of 5,000-6,000MW per annum as against the current run rate of 2,000MW per

MF/Banks/Indian

annum. The government has provided various incentives and framed several rules

FIs/FIIs/Public & Others

14.5

and regulations to increase demand for renewable energy.

Outlook and Valuation: On EV/sales, the company is valued at 3.3x (at the upper

end of the price band) on the basis of 9MFY2015 annualized numbers. Looking

at the strong order book of the company and government focus on the sector, we

recommend a Subscribe on the issue.

Key Financials

Y/E March (` cr)

FY2013

FY2014

Net Sales

1059

1567

Net Profit

150

131

OPM (%)

18.6

11.2

EPS (`)

6.8

5.9

P/E (x)*

48.0

54.9

Shrenik C. Gujrathi

P/BV (x)*

4.4

15.5

+91 22 3935 7800 Ext: 6872

EV/Sales (x)*

7.1

4.9

Source: Company, Angel Research; Note: *The above numbers are considering subscription at the

upper end of the price band

Please refer to important disclosures at the end of this report

1

Inox Wind | IPO Note

Issue details

The company’s issue consists of fresh issue of equity shares of `10 each via the

book building process in the price band of `315-325, aggregating up to `700cr;

and offer for sale by promoters group of 1.0cr shares. Further, the company has

offered a discount of `15 per share to employees and retail investors. The issue

will constitute 14.5% of the post-issue paid-up equity share capital of company.

Exhibit 1: Share Holding pattern

Particulars

Pre-Issue

Post-Issue

No. of shares

(%)

No. of shares

(%)

Promoter group

200,000,000

100.0

190,000,000

85.8

Others

-

-

31,538,460

14.2

Total

200,000,000

100.0

221,538,460

100.0

Source: RHP, Angel Research

Objects of the issue

Expansion and up gradation of existing manufacturing facilities. Amount to be

financed from the net proceeds will be `147.5cr.

Long term working capital requirements. Amount to be financed from the net

proceeds will be `290cr.

Investment in subsidiary (IWISL) for the purpose of development of power

evacuation infrastructure and other infrastructure development. Amount to be

financed from the net proceeds will be `131.5cr.

March 17, 2015

2

Inox Wind | IPO Note

Key investment arguments

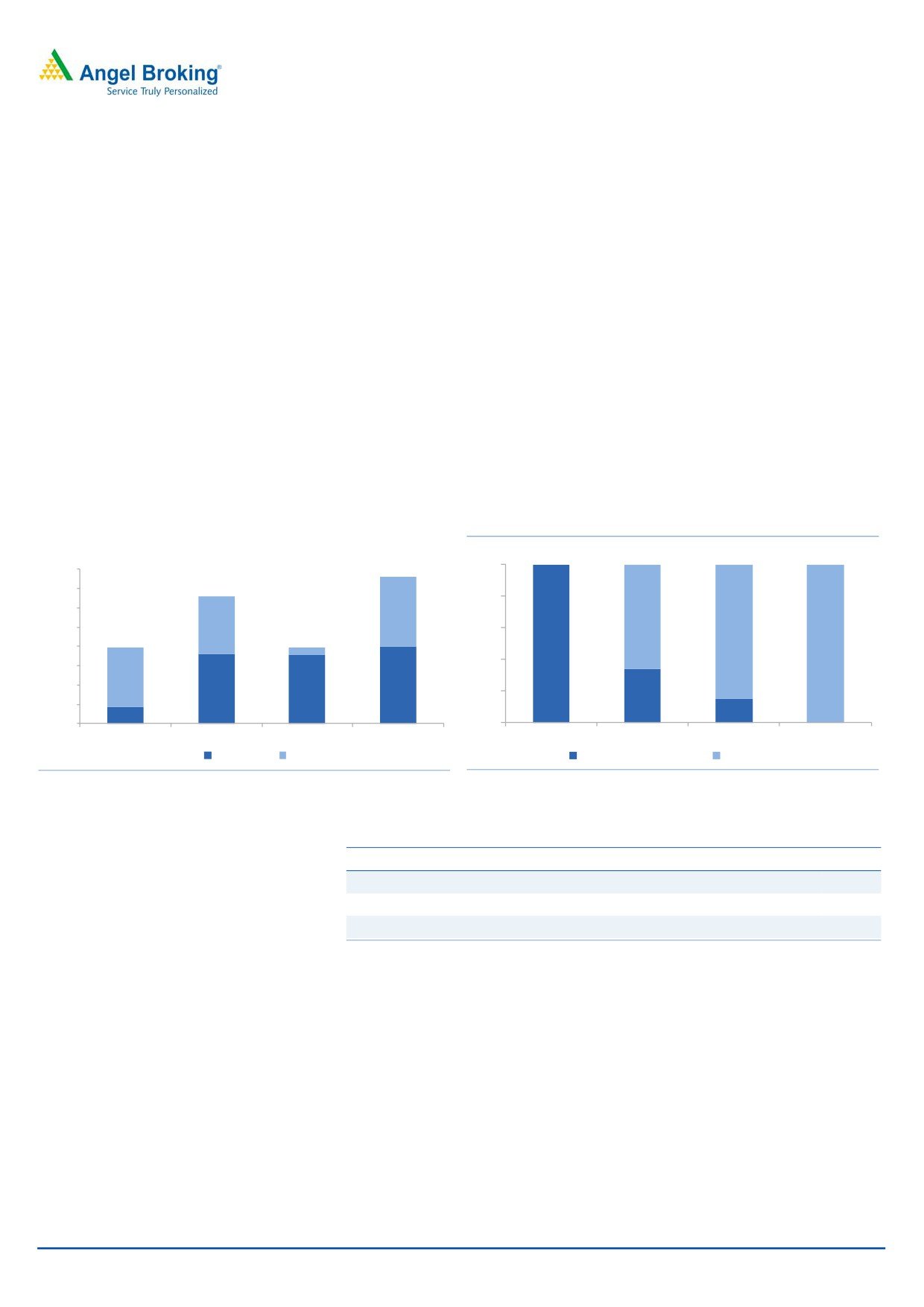

Strong order book and ready pipeline of project sites: IWL has shown a strong

growth during FY2014 and 9MFY2015 period wherein it has sold 330MW and

380MW of WTGs during the period; plus, it has a strong order book (as of

December 2014). In the initial years of business, IWL’s orders were only from the

group companies, but now it has orders from major corporates like Oil India, Tata

Power, CESE, Welspun, Bangur and Hero group companies. Currently IWL has an

order book of 1,136MW (only 50MW is from group companies) as against

Suzlon’s order book of 1,148MW and Gamesa India Pvt Ltd’s order inflow of

850MW, as of December 2014. These provide us strong revenue visibility for

FY2016. Out of this order book 694MW orders are turnkey orders where it has to

supply WTGs and carry out wind studies, energy assessment, land acquisition,

infrastructure development, erection and commissioning of the projects. The

remaining 564MW order is only for the supply of WTGs. IWL has already executed

122MW and revenue in respect of this has been booked as of December 2014.

Exhibit 2: Inox WTG sales/commissioning in India (MW)

Exhibit 3: Declining in house contribution in net sales

(MW)

(%)

400

100

350

80

300

180

66

250

150

60

85

200

100

100

20

40

150

154

100

200

180

178

20

34

50

44

15

0

0

FY2013

FY2014

9MFY14

9MFY15

FY2013

FY2014

FY2014

9MFY15

WTG Sales EPC

Group company Sales

Third Party Sales

Source: RHP, Angel Research

Source: RHP, Angel Research

Exhibit 4: Peers companies order book as on December 2014

Company Name

MW

Inox Wind Ltd

1136

Suzlon Ltd

1148

Gamesa Corp*

850

Source: RHP, Angel Research; Note: *Order inflow from India during 2014.

IWL has access to wind sites which have been acquired or are under the

acquisition process by its group companies - GFL and IRL - and its subsidiary

IWISL. Currently the wind sites acquired have an aggregate power project capacity

of 2,130MW, while the wind sites which are under the acquisition process have a

power project capacity of 1,922MW. All these sites are located in Rajasthan,

Gujarat, Madhya Pradesh and Andhra Pradesh. IWL has made an agreement with

group companies under which they get access to the wind sites for construction of

wind power projects. IWL would reimburse the cost incurred by group companies

on site acquisition along with markup equal to 10% p.a.

March 17, 2015

3

Inox Wind | IPO Note

Procedure for Acquisition of Wind Sites

A project developer is required to apply to the government to obtain leasehold

rights in government land for the development of wind farms.

After that the project developer does the survey (collection of wind availability

data and project feasibility study) for selection of potential sites for project.

Once the site is identified then the project develpoer would register the project

in its name.

After that, the project developer is required to make certain payments pursuant

to the rules, following which the government makes a recommendation to the

district collector to allot the specified land to the project developer for wind

farm development.

Upon the land being allotted to the project developer, the project developer

enters into a lease deed with the relevant authority, and acquires possession of

the land.

The project developer is required to ensure that the project commences

operation within certain period of time (differs from state to state) following the

date of allotment of land. For acquisition of land, the project developer

doesn’t require much funds as the same is provided by the government or is

provided at a nominal lease rental.

The company has acquired healthy amount of wind sites (2,130MW) so far, which

is likely to convert in sales and moreover, the process for acquiring additional

1,922MW wind sites is under process. In our view the company has a strong

potential to convert this additional sites into order book. Thus this gives us a

medium term revenue visibility for the company going forward.

Exhibit 5: Visibility of Project Pipeline

Acquired Wind sites

MW Wind Sites under acquisition process

MW

Rajasthan

1,415

Rajasthan

1,194

Gujarat-IRL

154

Gujarat

74

Gujarat-GFL

212

Madhya Pradesh

634

Gujarat-IWISL

44

Andhra Pradesh

20

Madhya Pradesh

285

Andhra Pradesh

20

Total

2,130

Total

1,922

Source: RHP, Angel Research

Capacity addition to drive growth

The strong order book shows the medium term revenue visibility for the company.

To improve the utilization levels of its nacelles and hubs plant, IWL is increasing

rotor blade and tower production capacity from 256 to 400 rotor blade sets and

150 to 300 towers per annum at its Rohika unit, Ahmedabad, Gujarat. The

company is also constructing new integrated manufacturing unit at Barwani,

Madhya Pradesh with nacelles and Hubs capacity of 400 units, rotor blades

capacity of 400 sets and tower capacity of 300 units. This new plant is expected to

March 17, 2015

4

Inox Wind | IPO Note

commence operations during 2HFY2016. Thus, IWL’s total capacity of nacelles

and hubs will increase to 950 units, rotor blade capacity to 800 sets and tower

capacity to 600 units.

Exhibit 6: Manufacturing Capacity

Installed

Post

Component(s)

Plant Location

Annual Production

Proposed

Capacity

Expansion

Nacelles and Hubs

Himachal Pradesh

550

550

Nacelles and Hubs

Madhya Pradesh

-

400

Rotor blade sets

Madhya Pradesh

-

400

Towers

Madhya Pradesh

-

300

Rotor blade sets

Gujarat

256

400

Towers

Gujarat

150

300

Source: RHP, Angel Research

Government focus on renewable energy: The government has set a target of

installed wind power capacity of 60,000MW till FY2022 from the current capacity

of 21,150MW. This will create a huge opportunity for the company in the

upcoming period. Hence we expect order inflow to increase at a faster pace

during the next few years. We expect industry order flow to come in at the run

rate of 5,000-6,000MW per annum as against the current run rate of

2,000MW per annum. The government has reintroduced the accelerated

depreciation and generation based incentives scheme which are the major

demand drivers for the wind energy sector. Furthermore, in order to increase the

demand for renewable energy, Renewable Purchase Obligation (RPO) is being

implemented throughout the country and SERCs are obliged to purchase certain

percentage of their power consumption from renewable energy sources.

Exhibit 7: Potential versus currently installed wind capacity (MW)

Installable Potential

State / UTs

at 50 meter

at 80 meter

Installed Capacity

hub height

hub height

Andhra Pradesh

5,394

14,497

748

Gujarat

10,609

35,071

3,454

Karnataka

8,591

13,593

2,324

Kerala

790

837

35

Madhya Pradesh

920

2,931

423

Maharashtra

5,439

5,961

4,086

Rajasthan

5,005

5,050

22,802

Tamil Nadu

5,374

14,152

7,273

Others

7,008

10,336

4

Total

49,130

102,788

21,489

Source: RHP, Angel Research

March 17, 2015

5

Inox Wind | IPO Note

Availability of high quality technology and ability to provide

turnkey solution

IWL has perpetual license from ASMC, a leading wind technology company from

Austria, to manufacture 2MW WTGs in India. The company also provides turnkey

solution services to its customers as it is preferred by wind farm developers and

independent power producers as they do have capabilities to undertake such large

project development.

Strong financials: Typically WTG manufacturers require large working capital,

mainly due to higher receivables. Therefore companies with well capitalized

balance sheets are likely to be in a position to manage their working capital

requirement and successfully expand business going forward. IWL plans to utilize

`290cr from this IPO issue for long term working capital so as to expand business

activity going forward.

Outlook and Valuation

IWL has shown a strong growth in its initial stage of business operation. Given the

government thrust on renewable energy sector and the company’s strong order

book, we think the company is well positioned to grow at a healthy rate in the

coming years. Currently it is attractively placed in terms of financial stability as its

margins are quite strong and has healthy balance sheet as compared to its closely

listed peer Suzlon Energy. On EV/sales, the company is valued at 3.3x (at the

upper end of the price band) on the basis of 9MFY2015 annualized numbers.

Looking at the strong order book of the company and government focus on the

sector, we recommend a Subscribe on the issue.

Exhibit 8: Valuation table (9MFY2015 annualized)

Inox Wind

**Suzlon Energy

Sales

2,373

5,276

EV

7,910

16,446

Order Book (MW)

1,136

1,148

EV/Sales

3.3

3.1

Source: Company, Angel Research, Note: Considered upper price band to arrive at implied market

cap, EV and Book value.** Suzlon valuation is based on sale of overseas business and fresh equity

infusion.

March 17, 2015

6

Inox Wind | IPO Note

Key investment concerns

Wind energy potential of the country is limited

Centre of Wind Energy Technologies, a research organization in wind energy, has

said in a report (released in March 2014) that India has a wind power potential of

102,788MW on 80 meter hub height. Currently 20.5% of wind energy potential

has been exploited. Moreover, based on government target of wind capacity

addition by 2022, 60% of the potential would be exhausted.

Increase in competition might put pressure on margin

The WTG manufacturing capacity in India currently is estimated to be 12,000MW

per annum, and we expect competition to increase in this segment in the coming

years. IWL competes with players like Suzlon Energy, Gamesa Wind Turbine Pvt

Ltd, Vestas and Win Wind Power Energy Pvt Ltd. Moreover, some more

international players are eyeing the Indian market. Therefore, competition is likely

to remain high. In order to gain market share, the company might have to reduce

the prices of its product and services. This might put pressure on its margins going

forward.

Exhibit 9: WTG manufacturing Capacity

Manufacturer name

MW (per annum)

Gamesa Wind Turbine Private Limited

1,500

GE India

450

Leitner Shiram Manufacturing Ltd

1,100

Kenersys India Pvt. Ltd

400

Leitner Shiram Manufacturing Ltd

250

ReGen Powertech Pvt. Ltd.

750

Suzlon Energy Limited

3,700

Vestas Wind Technology India Pvt. Ltd.

1,000

WinWinD Power Energy Pvt. Ltd.

1,000

Inox Wind Ltd

1,100

Total Industry

12,000

Source: Company, Angel Research

March 17, 2015

7

Inox Wind | IPO Note

Profit & Loss

Y/E March (` cr)

FY2013

FY2014

9MFY14

9MFY15

Net Sales

1,058.9

1,567.2

877.4

1,779.5

% chg

70.3

48.0

(44.0)

102.8

Total Expenditure

862.4

1,391.7

756.6

1,496.7

Raw Materials

678.9

939.7

578.4

1,152.6

(% of Net Sales)

64.1

60.0

65.9

64.8

Employee Cost

25.0

38.4

29.4

39.1

(% of Net Sales)

2.4

2.5

3.3

2.2

EPC, O&M, Common

94.1

273.4

56.4

172.6

Inf Facility and Site Dev exp.

(% of Net Sales)

8.9

17.4

6.4

9.7

Other Expenses

64.4

140.2

92.4

132.4

(% of Net Sales)

6.1

8.9

10.5

7.4

EBITDA

196.5

175.5

120.8

282.8

(% of Net Sales)

18.6

11.2

13.8

15.9

Depreciation

8.9

11.6

8.6

14.7

EBIT

187.6

163.9

112.2

268.1

Interest

38.7

46.0

38.0

46.4

Other Income

4.8

9.1

7.9

15.5

PBT before exceptional items

153.7

127.0

82.1

237.1

PBT

153 7

127 0

82 1

237 1

Tax

3.3

(4.4)

(3.2)

57.8

(% of PBT)

2.1

(3.5)

(3.9)

24.4

PAT

150.4

131.5

85.3

179.3

Adj. Net Profit

150.4

131.5

85.3

179.3

Margin (%)

14.2

8.4

9.7

10.1

yoy growth (%)

50.7

(12.6)

110.3

EPS

6.8

5.9

8.1

38

March 17, 2015

8

Inox Wind | IPO Note

Balance sheet

Y/E March (` in cr)

FY2013

FY2014

9MFY14

9MFY15

SOURCES OF FUNDS

Equity Share Capital

40

200

200

200

Reserve and Surplus

256

220

174

398

Net Worth

296

420

374

598

Loans

337

480

533

729

Other Long term liabilities

2

2

2

2

Deferred tax liabilities

20

15

16

4

Total Liabilities

654

918

926

1,333

APPLICATION OF FUNDS

Fixed Assets

157

174

177

168

Capital Work-in-Progress

4

25

15

45

Investments

-

45

45

-

Current Assets

789

1,228

1,092

1,962

Inventories

79

271

234

312

Sundry Debtors

500

710

613

1,251

Cash

2

4

2

19

Loans & Advances

196

203

228

341

Other Assets

12

41

15

40

Current Liabilities

296

555

403

842

Net Current Assets

494

673

688

1,120

Total Assets

654

918

926

1,333

March 17, 2015

9

Inox Wind | IPO Note

Cash flow statement

Y/E March (` in cr)

FY2013

FY2014

9MFY14

9MFY15

Profit before tax

154

127

82

237

Depreciation

9

12

9

15

Change in Working Capital

(286)

(238)

(307)

(292)

Interest / Dividend (Net)

34

39

32

40

Direct taxes paid

(29)

(33)

(21)

(48)

Others

(3)

6

4

4

Cash Flow from Operations

(121)

(88)

(202)

(45)

(Inc.)/ Dec. in Fixed Assets

(351)

(44)

(32)

(54)

(Inc.)/ Dec. in Investments

216

(0)

21

(17)

Cash Flow from Investing

(135)

(44)

(11)

(71)

Issue of Equity

0

0

0

0

Inc./(Dec.) in loans

256

179

250

191

Dividend Paid (Incl. Tax)

0

0

0

0

Interest / Dividend (Net)

(38)

(46)

(38)

(71)

Cash Flow from Financing

219

132

212

120

Inc./(Dec.) in Cash

(37)

0

(1)

4

Opening Cash balances

39

2

2

2

Closing Cash balances

2

2

1

6

March 17, 2015

10

Inox Wind | IPO Note

Key Ratios

Y/E March

FY2013

FY2014

Valuation Ratio (x)

P/E (on FDEPS)

48.0

54.9

P/CEPS

45.3

50.5

P/BV

4.4

15.5

EV/Sales

7.1

4.9

EV/EBITDA

38.4

43.5

EV / Total Assets

11.5

8.3

Debt/Equity

1.1

1.1

EPS (fully diluted)

6.8

5.9

Cash EPS

7.2

6.4

Book Value

73.9

21.0

Turnover ratios (x)

Inventory / Sales (days)

27

63

Receivables (days)

172

165

Payables (days)

125

146

WC cycle (ex-cash) (days)

170

156

Note: Valuation Ratio at the upper price band

March 17, 2015

11

Inox Wind | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel has received in-principal approval

from SEBI for registering as a Research Entity in terms of SEBI (Research Analyst) Regulations, 2014. Angel or its associates has not

been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its associates

including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in the company covered by

Analyst. Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of securities of

the company covered by Analyst during the past twelve months. Angel/analyst has not served as an officer, director or employee of

company covered by Analyst and has not been engaged in market making activity of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

March 17, 2015

12