OFS | Metals

July 2, 2013

Hindustan Copper

AVOID

CMP

`73

Stretched Valuations

OFS floor price

`70

Government of India is divesting 37,119,152 shares (4.01% of equity capital) in

Hindustan Copper Ltd. (HCL). It has set a floor price of `70 for the issue. We

recommend investors to AVOID subscribing to shares due to expensive valuation.

Company overview

HCL was incorporated in 1967 to take over NMDC’s copper mines and plants.

The company’s core business includes exploration, mining beneficiation, smelting,

refining and casting of finished copper.The company has four operating units

namely Khetri Copper Complex in Rajasthan, Indian Copper Complex in Bihar

(both mining cum metallurgical complex), Malanjkhand Copper Complex in M.P.

(mining complex) & Taloja copper project in Maharastra (collaboration with

Southwire Company, US). The company's copper reserves and resources in

accordance with JORC standard are 411mn tonnes (average grade 1.05%) and

623mn tonnes (Average grade 1.04%) as on April 1, 2010, respectively, making

it the largest copper company in India.

Investment arguments

Expanding capacity to fully exploit India’s copper ore demand: India has a large

imbalance between its smelting/refining capacity as against its copper mining

capacity. Currently India’s smelting/refining capacity stands at 1MTPA for which

100MT of copper ore is required (assuming 1% cu). Currently India’s actual

copper ore production stands at 3.2MTPA which is entirely produced by HCL. So

in order to capitalize on this sustained demand, HCL plans to ramp up its

production capacity from the current 3.2MTPA to 12.4MTPA by FY2018 at a

capex of `2,500cr. The company aims to expand its Malanjkhand, Khetri, Kolihan

and Surda mines and Banwas Mine; further, it aims to re-open Rakha and

Kendadih mines and develop new mine Chapri-Sidheswar.

Single vertically integrated player in India: HCL is the only vertically integrated

player in India which has its operations span across the entire value chain. Their

core operations include mining of copper ore, concentration of copper ore into

copper concentrate through a beneficiation process and also smelting, refining

and extruding of the copper concentrate into refined copper in downstream

saleable products.

Possesses first mover advantage: Copper mining requires substantial investments

and time for greenfield projects to be set up. Also many clearances need to be

obtained from the Government for the same. This entails a lot of entry barriers in

this industry. HCL on the other hand has all its mining complexes near the major

copper ore deposits of the country. Thus any greenfield projects undertaken by

the company can rely on its existing infrastructure. Moreover, HCL has applied for

prospecting, mining and Reconnaissance Permit in the states of Rajasthan,

Jharkhand, Madhya Pradesh and Haryana.

Bhavesh Chauhan

Valuation: HCL is the only vertically integrated copper producer in India.

Tel: 022- 39357800 Ext: 6821

However, at the OFS price of `70, the stock is available at a valuation of 21.0x PE

and 11.9x EV/EBITDA based on FY2012 numbers, which is expensive compared

to its peers. Miners such as Coal India, MOIL and NMDC are trading in the range

Vinay Rachh

of

3-7x FY2012 EV/EBTIDA. Hence, we recommend investors to AVOID

Tel: 022- 39357600 Ext: 6841

subscribing to HCL issue.

Please refer to important disclosures at the end of this report

1

Hindustan Copper | FPO

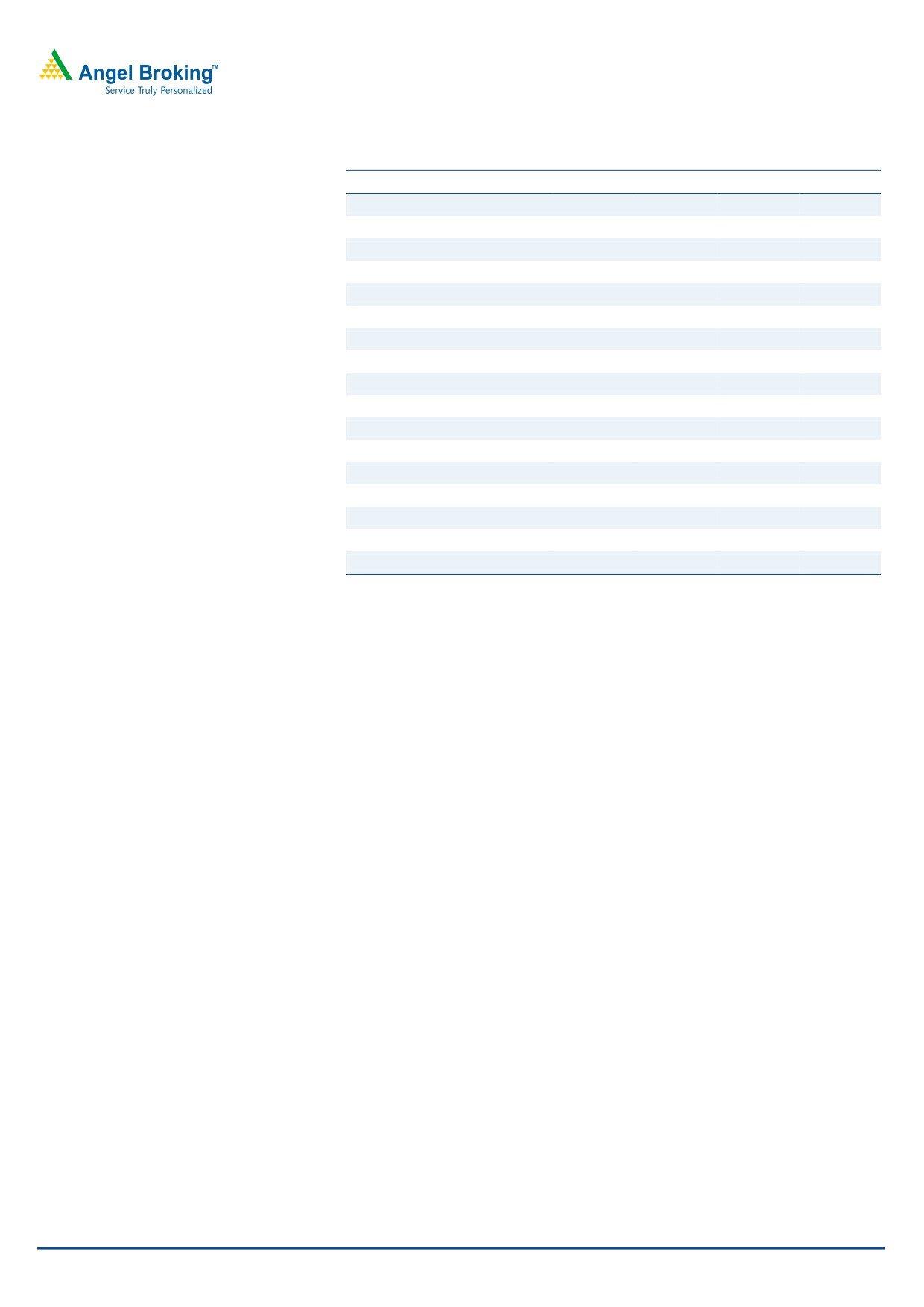

Profit & loss statement (Standalone)

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012

Net Sales

1,210

1,319

1,171

1,492

% chg

(24.1)

9.0

(11.2)

27.4

Total Expenditure

1,297

1,134

790

961

EBIDTA

(88)

184

381

530

(% of Net Sales)

(7.3)

14.0

32.5

35.6

Other Income

120

53

56

88

Depreciation & Amortization

19

18

97

144

Interest

8

3

4

2

PBT

5

216

335

473

(% of Net Sales)

0.5

16.4

28.6

31.7

Extraordinary Expense/(Inc.)

(3)

1

(1)

(1)

Tax

16

61

111

149

(% of PBT)

288.1

28.3

33.1

31.6

PAT

(7)

154

226

324

% chg

-

-

46.3

43.7

Ad. PAT

(10)

155

224

323

% chg

-

-

44.9

44.3

July 2, 2013

2

Hindustan Copper | FPO

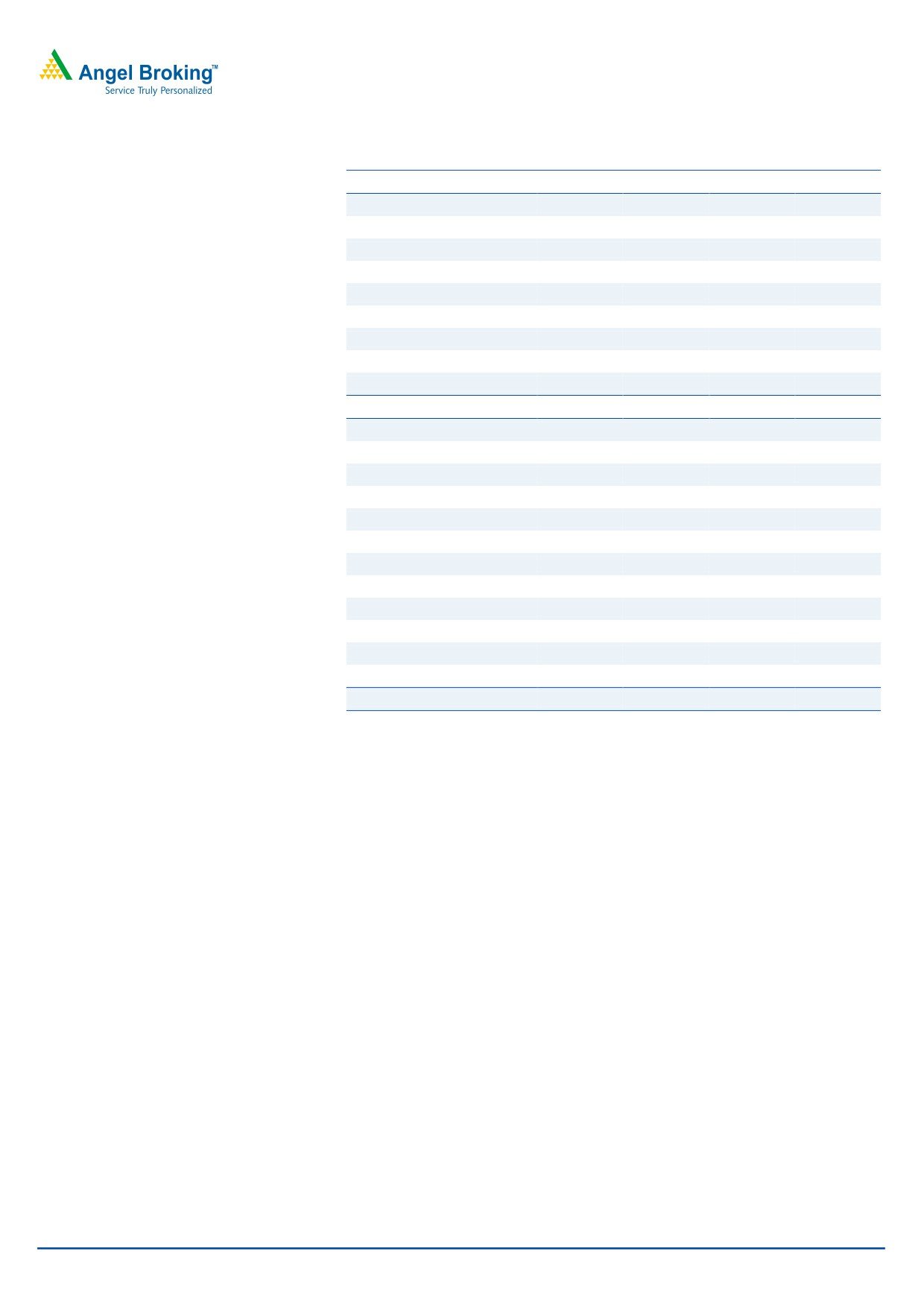

Balance sheet (Standalone)

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012

SOURCES OF FUNDS

Equity Share Capital

463

463

463

463

Reserves & Surplus

505

660

719

935

Shareholders Funds

968

1,123

1,182

1,398

Share warrants

-

-

-

-

Minority Interest

-

-

-

-

Total Loans

36

0.05

-

-

Other Liabilities

-

-

77

85

Deferred Tax Liability (net)

(54)

(57)

3

(6)

Total Liabilities

950

1,065

1,262

1,477

APPLICATION OF FUNDS

Gross Block

731

760

770

788

Less: Acc. Depreciation

522

541

557

579

Net Block

210

220

213

209

Capital Work-in-Progress

379

409

459

480

Goodwill

-

-

-

-

Investments

0

72

64

149

Current Assets

1,007

863

879

1,014

Current liabilities

646

498

371

421

Net Current Assets

361

365

508

594

Other assets

0

0

17

45

Misc Expenditure

-

-

-

-

Total Assets

950

1,065

1,262

1,477

July 2, 2013

3

Hindustan Copper | FPO

Cash flow statement (Stanalone)

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012

Profit before tax

5

216

335

473

Depreciation

19

18

21

18

(Inc)/Dec in Working Capital

(48)

(116)

30

(83)

Direct taxes paid

44

67

120

154

Others

(79)

(90)

(157)

(219)

Cash Flow from Operations

(59)

94

349

343

(Inc.)/Dec. in Fixed Assets

(53)

(28)

(18)

(20)

Free Cash Flow

(112)

66

332

323

(Inc)/Dec in Investments

0

(72)

(15)

(84)

Others

(7)

68

(80)

(10)

Issue of Equity

-

-

-

-

Inc./(Dec.) in loans

(79)

(34)

0

0

Dividend Paid (Incl.Tax)

0

0

46

46

Cash Flow from Financing

(86)

(37)

(49)

(48)

Inc./(Dec.) in Cash

(231)

(124)

169

85

Opening Cash balances

528

297

173

342

Closing Cash balances

297

173

342

428

July 2, 2013

4

Hindustan Copper | FPO

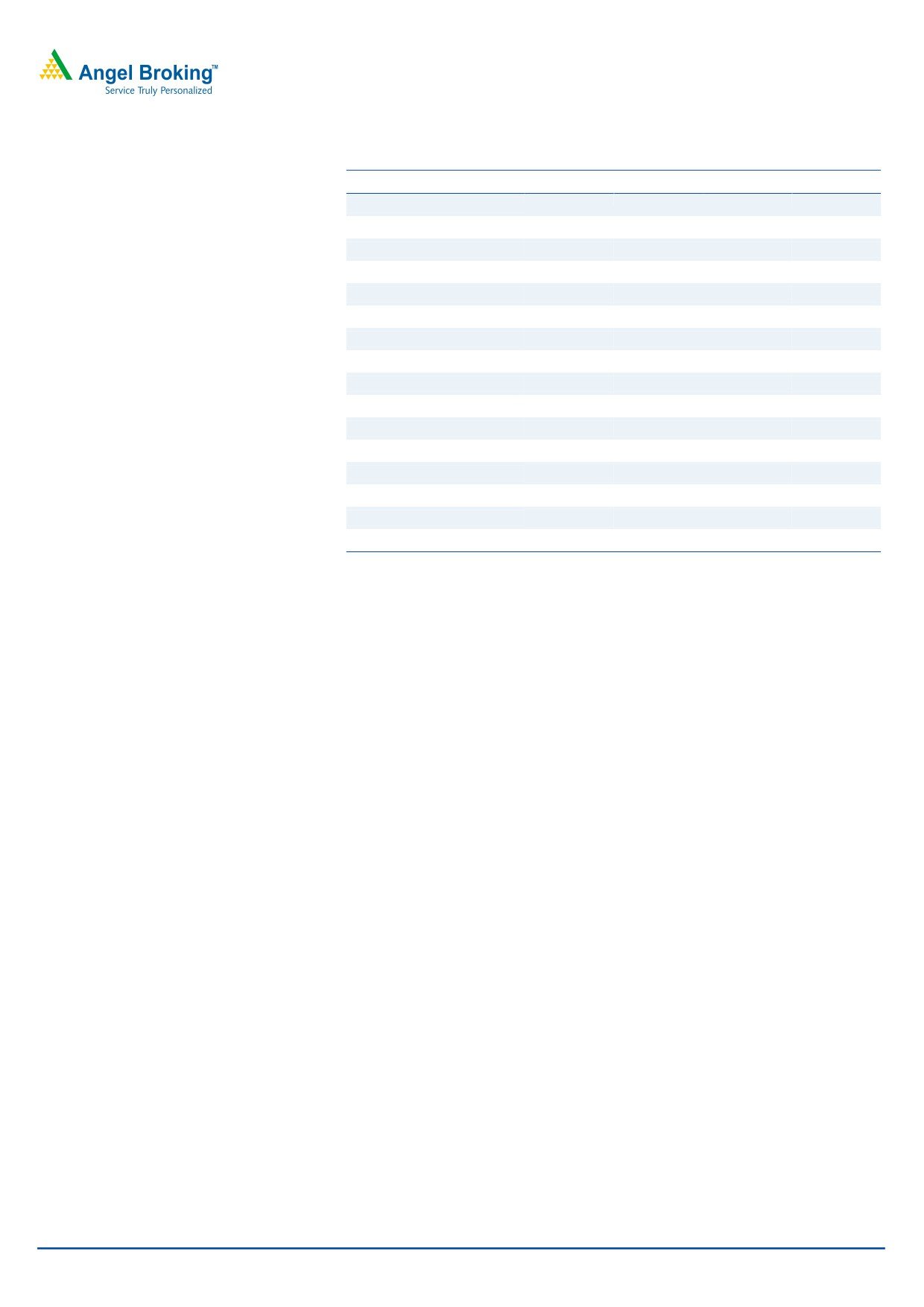

Key Ratios

Y/E March

FY2009

FY2010

FY2011

FY2012

Per Share Data(`)

EPS (diluted)

-

1.7

2.3

3.3

Book Value

(17.2)

15.1

5.3

18.3

Ratios

EBITDA margin (%)

2.3

16.6

34.1

37.8

Adj. Net margin (%)

(0.6)

10.8

17.5

19.7

Net Debt/Equity

0.1

0.0

0.0

0.0

Returns %

RoE

34.6

1.1

20.6

28.5

RoCE

1.1

20.6

28.5

34.6

RoIC

10.3

11.1

16.4

20.5

Valuation Ratio (x)

P/E

-

41.9

31.0

21.0

P/BV

6.7

5.8

5.5

4.6

EV/Sales

5.3

5.0

5.4

4.2

EV/EBITDA

-

35.5

16.7

11.9

July 2, 2013

5

Hindustan Copper | FPO

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Pvt. Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Pvt. Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking

or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or

in the past.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

July 2, 2013

6

Hindustan Copper | FPO

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Bhavesh Chauhan

Sr. Analyst (Metals & Mining)

Viral Shah

Sr. Analyst (Infrastructure)

Sharan Lillaney

Analyst (Mid-cap)

V Srinivasan

Analyst (Cement, FMCG)

Yaresh Kothari

Analyst (Automobile)

Ankita Somani

Analyst (IT, Telecom)

Sourabh Taparia

Analyst (Banking)

Bhupali Gursale

Economist

Vinay Rachh

Research Associate

Amit Patil

Research Associate

Twinkle Gosar

Research Associate

Tejashwini Kumari

Research Associate

Akshay Narang

Research Associate

Harshal Patkar

Research Associate

Technicals:

Shardul Kulkarni

Sr. Technical Analyst

Sameet Chavan

Technical Analyst

Sacchitanand Uttekar

Technical Analyst

Derivatives:

Siddarth Bhamre

Head - Derivatives

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Dealer

Akshay Shah

Sr. Executive

Production Team:

Tejas Vahalia

Research Editor

Dilip Patel

Production Incharge

CSO & Registered Office: G-1, Ackruti Trade Centre, Road No. 7, MIDC, Andheri (E), Mumbai - 93. Tel: (022) 3083 7700. Angel Broking Pvt. Ltd: BSE Cash: INB010996539 / BSE F&O: INF010996539, CDSL Regn. No.: IN - DP - CDSL - 234 - 2004, PMS Regn. Code: PM/INP000001546, NSE Cash: INB231279838 /

NSE F&O: INF231279838 / NSE Currency: INE231279838, MCX Stock Exchange Ltd: INE261279838 / Member ID: 10500. Angel Commodities Broking (P) Ltd.: MCX Member ID: 12685 / FMC Regn. No.: MCX / TCM / CORP / 0037 NCDEX: Member ID 00220 / FMC Regn. No.: NCDEX / TCM / CORP / 0302.

July 2, 2013

7