3QFY2019 Result Update | IT

February 2, 2019

HCL Technologies

REDUCE

CMP

`1034

Performance Highlights

Target Price

`900

(` cr) - Consl.

3QFY19

2QFY19

% chg (qoq)

3QFY18

% chg (yoy)

Net revenue

15,699

14,861

5.6

12,808

22.6

Investment Period

12 Months

EBIT

3,086

2,966

4.0

2,509

23.0

Stock Info

EBIT margin (%)

19.7

20.0

(30)bps

19.6

7bps

Sector

IT

PAT

2,611

2,540

2.8

2,194

19.0

Market Cap (` cr)

139,987

Net Debt (` cr)

(12140)'

Source: Company, Angel Research

Beta

0.4

52 Week High / Low

1125/880

HCL Tech on sales front posted 4.9% sequential growth in USD revenues to

Avg. D aily Volum e

87,836

US$2,202mn v/s. US$2,099mn in 2QFY2019. In Constant currency terms (CC), the

Face Value (`)

2

BSE Sensex

36,257

company posted a 5.6% qoq growth. EBIT margin came in at 19.7% v/s 20.0% in

Nifty

110,831

2QFY2019. Consequently, PAT came in at `2,611cr v/s. `2,540cr in 2QFY2019, a rise of

Reuters Code

HCLT.BO

Bloomberg Code

HCLT@IN

2.8% qoq. FY2019 revenue guidance is kept at the mid-range of 9.5-11.5% in CC,

while operating margin are expected to be in the range of

19.5-20.5%. We

Shareholding Pattern (%)

recommend a Reduce; given that the company is too dependent on the

Prom oters

60.1

MF / Banks / Indian Fls

8.2

acquisition as a strategy to grow higher than Industry. This will keep a check on

FII / NRIs / OCBs

28.3

its business ROIC & hence multiples.

Indian Public / Others

3.5

Quarterly highlights: HCL Tech on sales front posted 4.9% sequential growth in USD

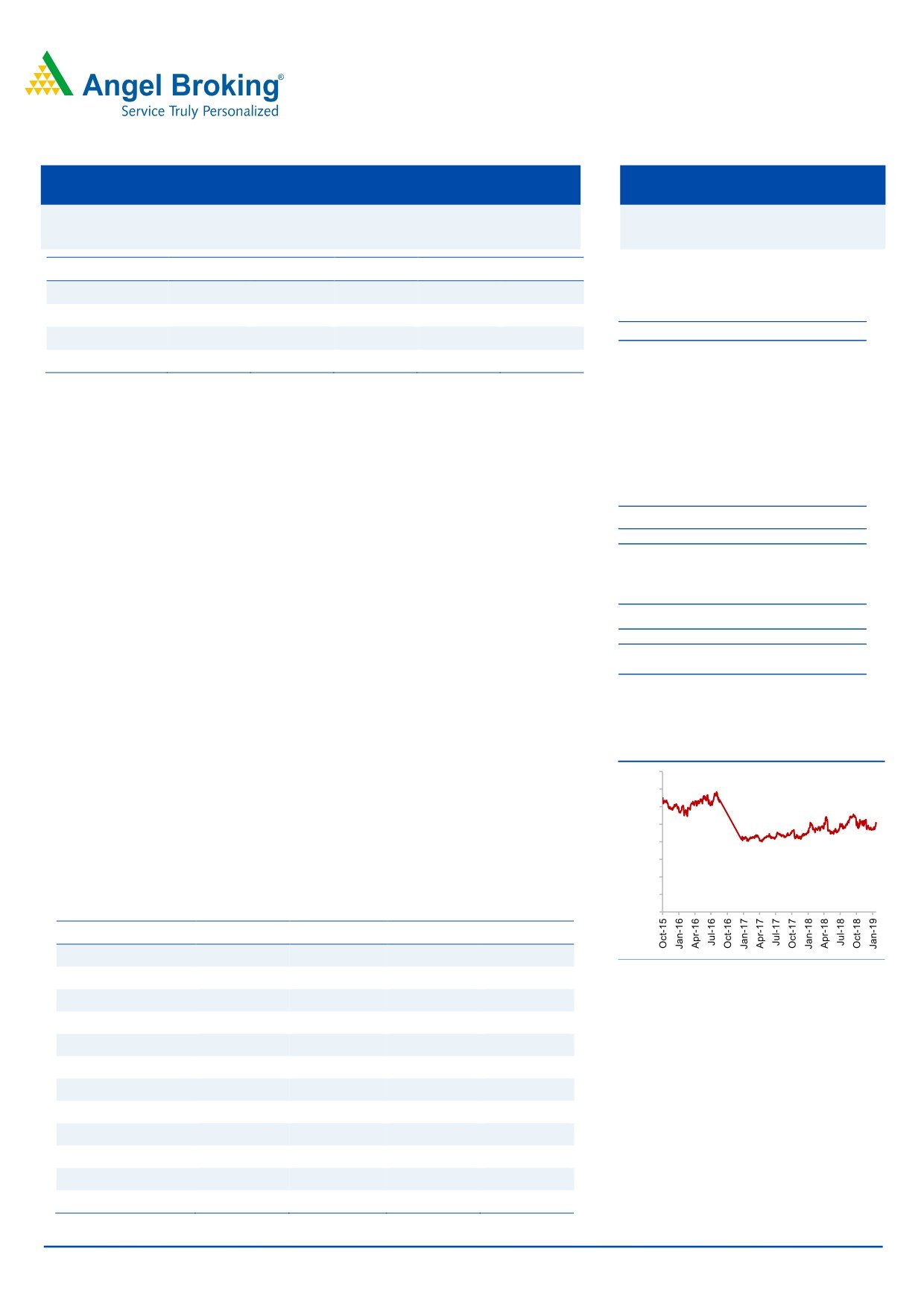

Abs .(% )

3m

1 yr

3 yr

Sensex

7.0

0.8

46.1

revenues to US$2,202mn V/s. US$2,099mn in 2QFY2019. In Constant currency terms

HCL Tech

0.1

2.0

14.4

(CC), the company posted a 5.6% qoq growth. EBIT margin came in at 19.7% v/s

20.0% in 2QFY2019. Consequently, PAT came in at `2,611cr V/s. `2,540cr in 2QFY2019,

a rise of 2.8% qoq. Industry segment wise, the company’s Financial Services vertical

posted a 0.6% qoq de-growth in CC terms. The Manufacturing vertical (contributing

3-year price chart

17.7% to revenue) posted a 3.9% qoq growth in CC terms. Consequently, PAT came in

1,600

at `2,611cr V/s. `2,540cr in 2QFY2019, a rise of 2.8% qoq.

1,400

1,200

Outlook and valuation: We expect HCL Tech to post a USD and INR revenue CAGR

1,000

of 11.6% and 15.2% respectively over FY2018-21E. The growth will be aided by the

800

acquisitions. However, given its profitability & valuations & given the backdrop that it is

600

400

concentrated on few services; we recommend a Reduce stance.

200

Key financials (Consolidated, US GAAP)

0

Y/E March (` cr)

FY2018

FY2019E

FY2020E

FY2021E

Net sales

50,570

60,937

68,853

77,255

8.2

20.5

13.0

12.2

Source: Company, Angel Research

% chg

Net profit

8,781

10,150

11,229

12,575

% chg

3.8

15.6

10.6

12.0

EBITDA margin (%)

22.6

22.9

23.9

23.9

EPS (`)

62.3

72.0

79.6

89.2

P/E (x)

16.6

14.4

13.0

11.6

P/BV (x)

4.0

3.6

3.2

2.9

RoE (%)

23.9

24.7

24.6

24.7

20.6

22.0

21.3

21.7

Sarabjit kour Nangra

RoCE (%)

+91 22 3935 7800 Ext: 6806

EV/Sales (x)

2.6

2.1

1.9

1.6

EV/EBITDA (x)

11.4

9.0

8.0

6.7

Source: Company, Angel Research; Note: CMP as of February 1, 2019

Please refer to important disclosures at the end of this report

1

HCL Technologies | 3QFY2019 Result Update

Exhibit 1: 3QFY2019 performance (Consolidated, US GAAP)

Y/E March (` cr)

3QFY19

2QFY19

% chg (qoq)

3QFY18

% chg (yoy)

9MFY19

9MFY18

% chg(yoy)

Net revenue

15,699

14,861

5.6

12,808

22.6

44,437

37,391

18.8

Cost of revenue

10,152

9,589

5.9

8,412

20.7

22,781

19,329

17.9

Gross profit

5,547

5,272

5.2

4,396

26.2

21,656

18,062

19.9

SG&A expense

1,900

1,773

7.2

1,432

32.7

11,324

9,838

15.1

EBITDA

3,647

3,499

4.2

2,964

23.0

10,332

8,224

25.6

Dep. and amortization

561

533

5.3

455

23.3

1,528

954

60.2

EBIT

3,086

2,966

4.0

2,509

23.0

8,804

7,270

21.1

Other income

105

252

(58.3)

264

(60.2)

638

878

(27.3)

PBT

3,191

3,218

(0.8)

2,773

15.1

9,442

8,148

15.9

Income tax

566

678

(16.5)

579

(2.2)

1,872

1,656

13.0

PAT

2,625

2,540

3.3

2,194

19.6

7,570

6,492

16.6

Forex gain/(loss)

14

-

-

-

1

Adjusted PAT

2,611

2,540

2.8

2,194

19.0

7,570

6,493

16.6

EPS

19.3

18.2

5.7

15.8

22.2

55.8

46.6

19.7

Gross margin (%)

35.3

35.5

(14)bps

34.3

101bps

48.7

48.3

43bps

EBITDA margin (%)

23.2

23.5

(31)bps

23.1

9bps

23.3

22.0

126bps

EBIT margin (%)

19.7

20.0

(30)bps

19.6

7bps

19.8

19.4

37bps

PAT margin (%)

16.6

17.1

(46)bps

17.1

(50)bps

17.0

17.4

(33)bps

Source: Company, Angel Research

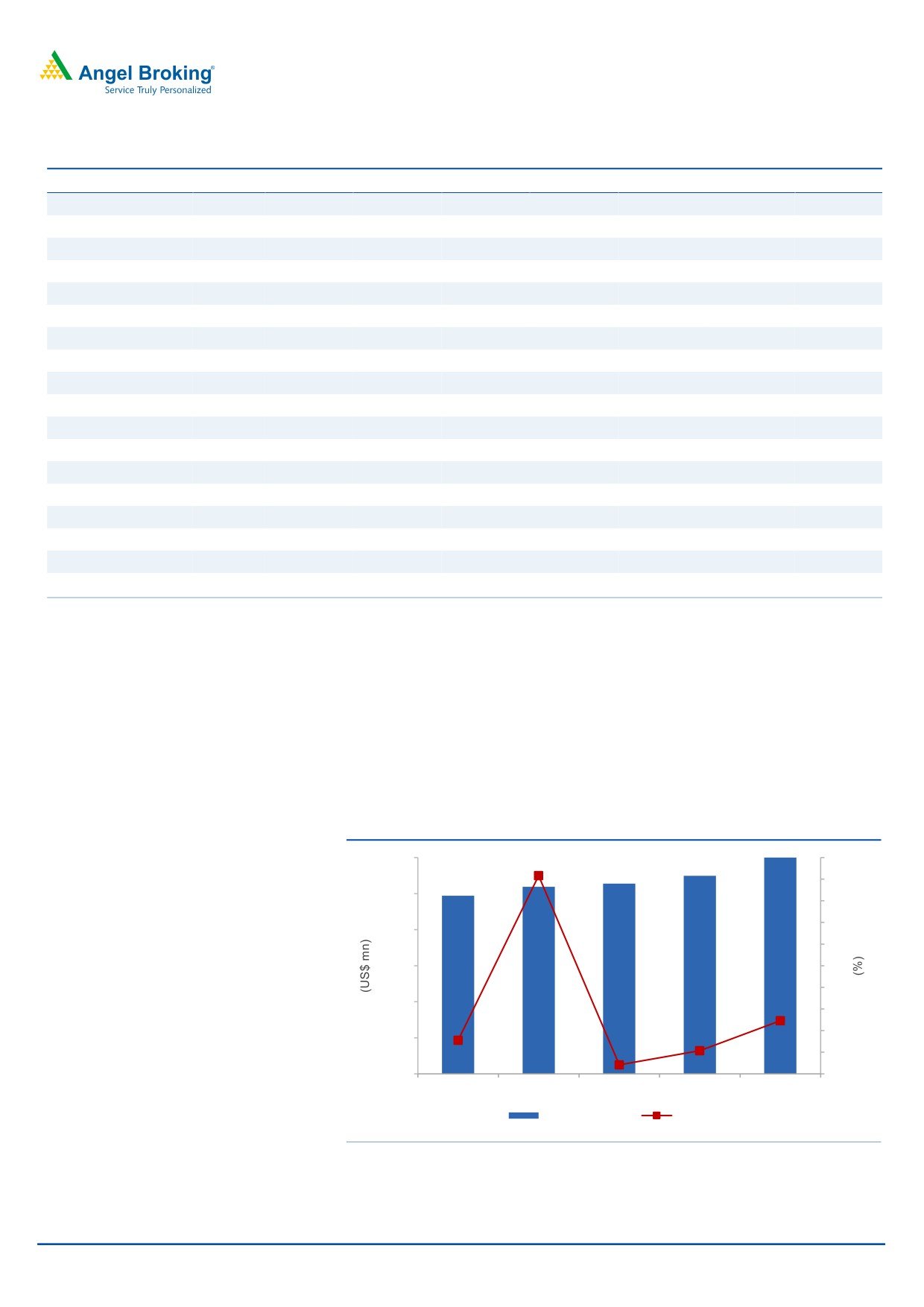

Robust Sales growth

HCL Tech on sales front posted 4.9% sequential growth in USD revenues to

US$2,202mn v/s. US$2,099mn in 2QFY2019. In Constant currency terms (CC), the

company posted a 5.6% qoq growth. Industry segment wise, the company’s Financial

Services vertical posted a 0.6% qoq de-growth in CC terms. The Manufacturing vertical

(contributing 17.7% to revenue) posted a 3.9% qoq growth in CC terms.

Exhibit 2: Revenue growth trend

2,200

20

18.3

18

2,000

16

14

1,800

12

1,600

10

8

1,400

6

4.9

4

1,200

3.1

2.1

2

1,988

2,038

2,055

2,099

2,202

0.8

1,000

0

3QFY18

4QFY18

1QFY19

2QFY19

3QFY19

Revenue (USD)

qoq growth (%)

Source: Company, Angel Research

February 2, 2019

2

HCL Technologies | 3QFY2019 Result Update

In terms of services, Engineering & R&D services (which constituted 25.5% of

sales) posted a growth of 5.1% qoq (CC), while Application services (accounting

for 32.0% of sales) grew by 2.3% qoq (CC). Infrastructure services, another

important segment of the company, which contributes around 37.5% to overall

sales, posted growth of 10.4% qoq (CC). Business services, which constituted 5.0%

of sales, de-grew by 5.1% qoq (CC).

Exhibit 3: Revenue growth trend (Service wise)

% of revenue

% growth CC (qoq) % growth (yoy)

Application services

32.0

2.3

2.5

Infrastructure services

37.5

10.4

16.5

Business services

5.0

(3.7)

50.1

Engineering and R&D services

25.5

5.1

17.4

Source: Company, Angel Research

Industry segment wise, the company’s Financial Services vertical (contributing

21.6% to revenue) posted a 0.6% qoq de-growth in CC terms. The Manufacturing

vertical (contributing 17.7% to revenue) posted a 3.9% qoq growth in CC terms.

Public services, Life Sciences & Healthcare, and Telecommunication, Media,

Publishing & Entertainment reported a qoq growth of (4.4) %, 5.8% and 35.4%

respectively, all in CC terms. Retail & CPG (contributing 10.2% of the revenue), on

the other hand, reported growth of 8.4% qoq in CC terms during the quarter.

Exhibit 4: Revenue growth trend (Industry wise)

% of revenue

% growth (CC qoq)

% growth (yoy)

Financial services

21.6

(0.6)

0.1

Manufacturing

17.7

3.9

1.5

Life sciences & Healthcare

13.0

5.8

23.4

Public Services

9.7

(4.4)

8.1

Retail & CPG

10.2

8.4

21.5

Telecom, MPE

9.2

35.4

40.3

Technology & Services

18.7

7.5

24.4

Source: Company, Angel Research

Among geographies, in CC terms, America grew by 2.7% qoq; RoW grew by 4.5%

qoq, while Europe grew by 12.9% qoq, during the period.

February 2, 2019

3

HCL Technologies | 3QFY2019 Result Update

Exhibit 5: Revenue growth trend (Geography wise in CC terms)

15

12.9

12

9

5.9

4.9

6

4.4

9

41.

1.9

3

2.7

(1.0)

0

4.5

(3)

(0.9)

(3.9)

(6)

(3.9)

(9)

(7.1)

3QFY18

4QFY18

1QFY19

2QFY19

3QFY19

US

Europe

Rest of the world

Source: Company, Angel Research

Hiring and utilization

During the quarter, the overall headcount of HCL Tech increased by 13,191 to

1,32,328 employees. The attrition rate in IT Services inched upwards to 17.8% (v/s.

17.1% in 2QFY2019) and the blended utilization level of the company remained

stagnant at 86.6% (86.7% in 2QFY2019).

Exhibit 6: Hiring trend

Particulars

3QFY18 4QFY18 1QFY19

2QFY19

3QFY19

Technical

1,08,831

1,09,565

1,13,404

1,16,910

1,21,273

Support

10,460

10,516

10,717

10,965

11,055

Total employee base

1,19,291

1,20,081

1,24,121

1,27,875

1,32,328

Gross addition

7,113

8,476

12,558

11,683

13,191

Net addition

251

790

4,040

3,754

4,453

Attrition - IT services (LTM) - %

15.2

15.5

16.3

17.1

17.8

Source: Company, Angel Research

February 2, 2019

4

HCL Technologies | 3QFY2019 Result Update

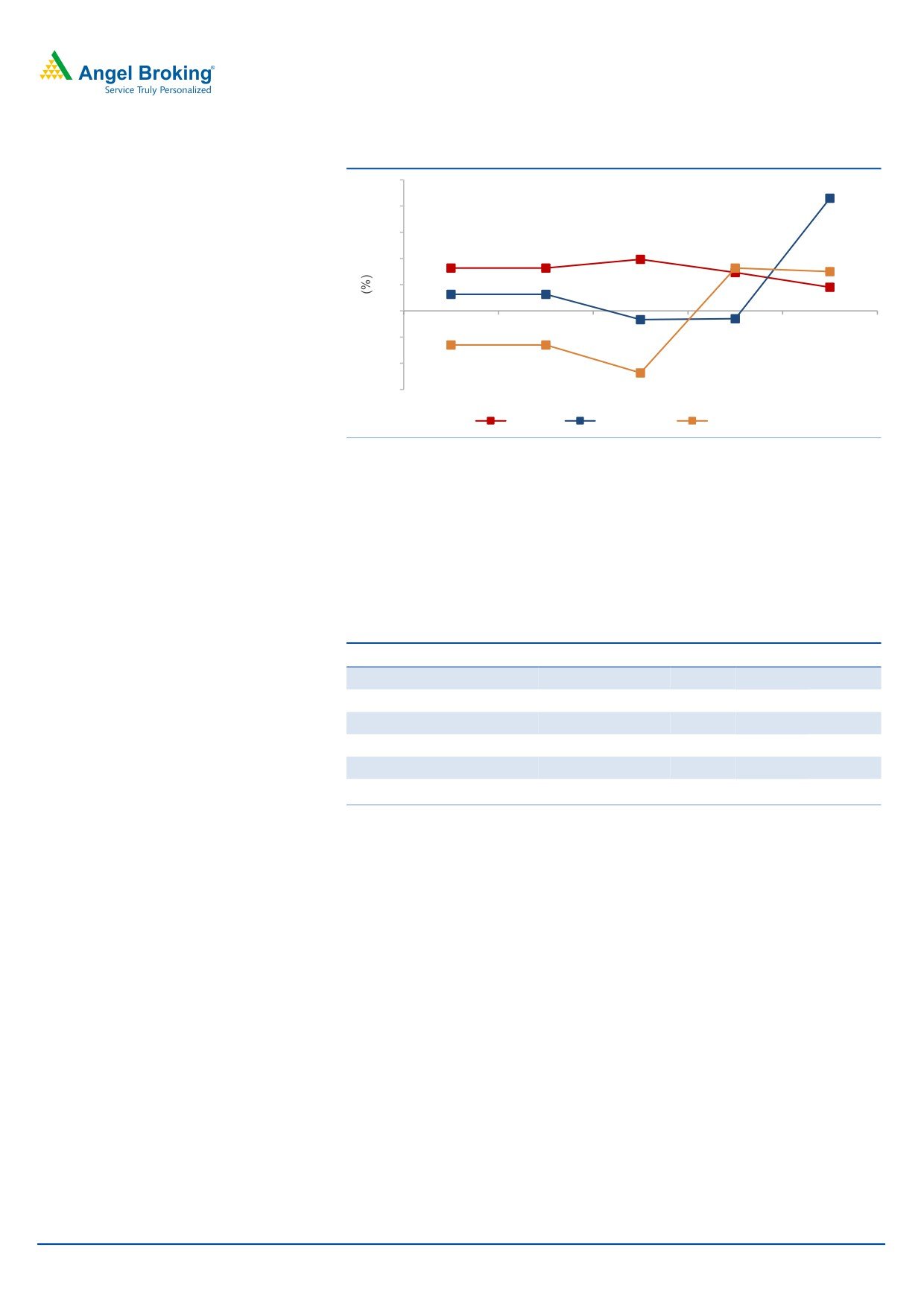

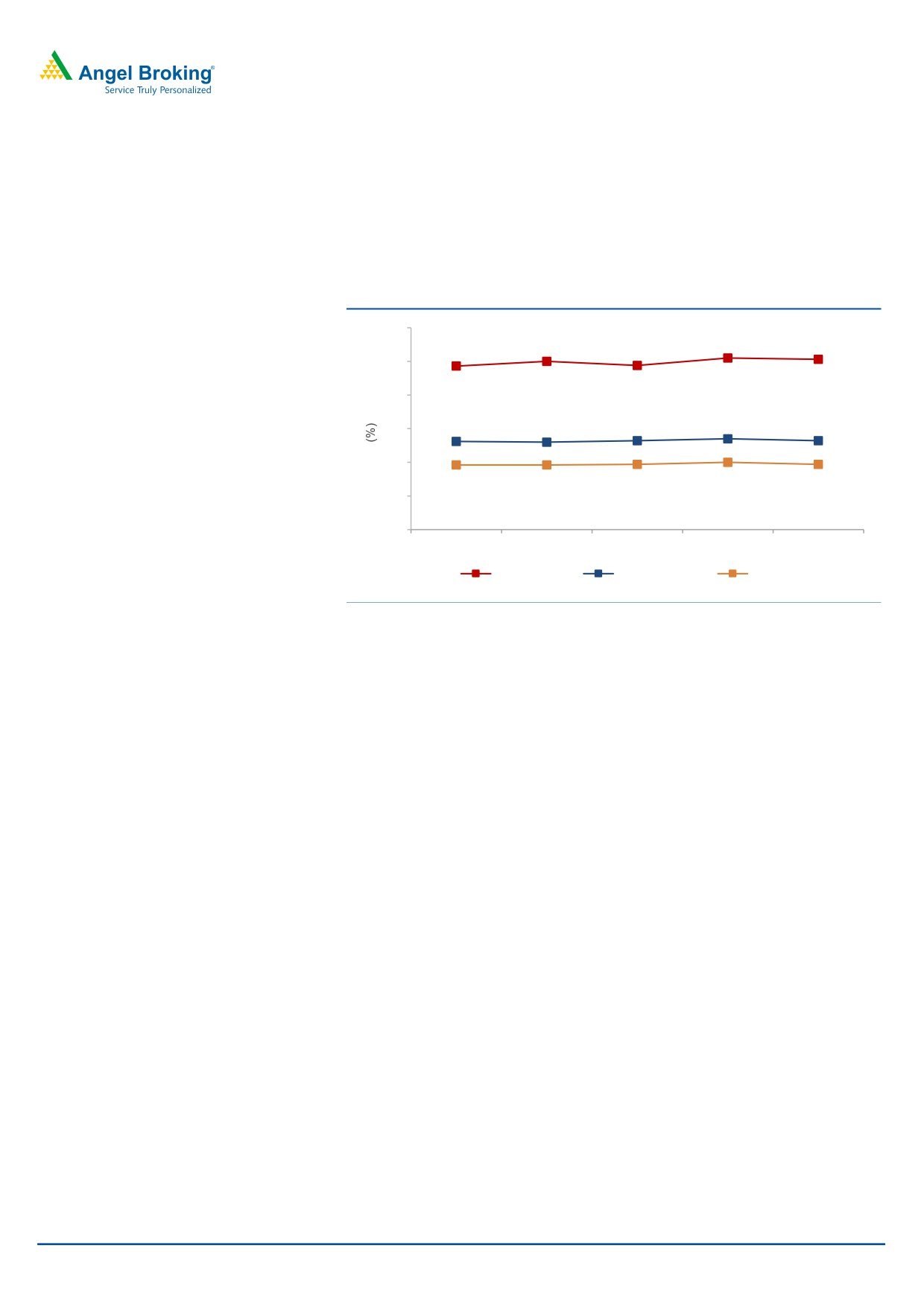

Operating margin shrink

On the operating front, the EBDITA margins came in at 23.2% (v/s. 23.5% in

2QFY2019), a qoq dip of 31bps, while the EBIT margins came in at 19.7%, a qoq

dip of 30bps. The negative impact of wage hikes was partly offset by higher

utilization and currency benefits.

Exhibit 7: Margin profile

40

35.0

35.5

35.3

34.3

34.4

35

30

23.1

23.0

23.2

23.5

23.2

25

20

19.6

19.7

20.0

19.6

19.7

15

10

3QFY18

4QFY18

1QFY19

2QFY19

3QFY19

Gross margin

EBITDA margin

EBIT margin

Source: Company, Angel Research

Client pyramid

The company signed

17 transformational deals this quarter. These deals

represented a well-balanced mix across service lines, industry verticals and

geographies. Company added US$5+ mn clients up by 15, US$10+ mn clients up by

8, US$50+ mn clients up by 4 and US$100+ mn clients up by 1.

February 2, 2019

5

HCL Technologies | 3QFY2019 Result Update

Investment arguments

Guidance re-iterated for FY2019: On the basis of deals on hand, the company

maintained to meet it’s revenue growth guidance of 9.5-11.5% in CC terms (

striving to achieve a mid-point of the guidance ) for FY2019, which includes a

component of inorganic growth, adjusting for which, the organic growth would

be in the range of 6.0-6.5% in CC for FY2019. The operating margin (EBIT) for

FY2019 is expected to be in the range of 19.5-20.5%. We expect HCL Tech to post

a USD and INR revenue CAGR of 11.6% and 15.2% respectively, over FY2018-21E.

IBM - Deal will mark its foray into enterprise product space: HCL Tech during

the quarter acquired 7 products from IBM for US$1.8bn. The products span across

areas such as Application Security, Endpoint Management, Low Code, Digital

Commerce and Experience, and Marketing Automation. The deal will close in 6

months and mostly funded through the internal accrual & debt of US$300mn.

Approximately 48% to be paid at close, most of balance to be paid after one year

of acquisition. The deal is likely to bring in incremental revenue of ~US$650mn on

a run-rate basis in second year after close. On operating front, EBITDA margins

are expected to be over 50% on a run-rate basis (slightly lower in year one of

acquisition), while Cash EPS accretion of ~15% is expected. With this, the product

contribution to the sales will increase from 11.9% in 9MFY2019 to 17%. The deal

seems though seems fairly valued on PE basis; but given high that the portfolio

will have a little growth; given mature nature of products, we find the deal

expensive on EV/ sales basis at around 2.7x.

Healthy pipeline: HCL Tech signed 17 transformational deals this quarter, across

service lines and industry verticals. The broad-based business wins were driven by

next-generation integrated offerings - Next-Gen ITO, BEYONDigital, and IoT

WoRKS, reflecting investments in Internet of Things, digital technologies, cloud,

automation and artificial intelligence. These deals represented a well-balanced

mix across service lines, industry verticals and geographies. Company added

US$5+ mn clients up by 15, US$10+ mn clients up by 8, US$50+ mn clients up by

4 and US$100+ mn clients up by 1.

Outlook & Valuation

We expect HCL Tech to post a USD and INR revenue CAGR of 11.6% and 15.2%

respectively over FY2018-21E. The growth will be aided by the acquisitions.

However, given its profitability & valuations & given the backdrop that it is

concentrated on few services; we recommend a Reduce stance.

Company Background

HCL Tech is India's fifth largest IT services company, with over 1,30,000 employees

catering to more than 600 clients. The company's service offerings include

Enterprise Application Services (EAS), Custom Applications, Engineering Research

& Development (ERD), and Infrastructure Management Services (IMS). In

December 2008, HCL Tech acquired UK-based SAP consulting company - Axon.

During 3QFY2016, the company acquired Geometric Software. In 3QFY2019, it

acquired seven products from IBM for US$1.8bn.

February 2, 2019

6

HCL Technologies | 3QFY2019 Result Update

Profit and loss statement (Consolidated, US GAAP)

Y/E Mar (` cr)

FY2017

FY2018

FY2019E

FY2020E

FY2021E

Net sales

46,723

50,570

60,937

68,853

77,255

Cost of revenues

30,890

33,237

39,852

43,928

49,288

Gross profit

15,833

17,333

21,084

24,925

27,966

% of net sales

33.9

34.3

34.6

36.2

36.2

SG&A expenses

5,524

5,894

7,130

8,469

9,502

% of net sales

11.8

11.7

11.7

12.3

12.3

EBITDA

10,309

11,439

13,954

16,456

18,464

% of net sales

22.1

22.6

22.9

23.9

23.9

Depreciation and amort.

835

1453

1767

2920

3245

% of net sales

1.8

2.9

2.9

4.2

4.2

EBIT

9,474

9,986

12,187

13,536

15,219

% of net sales

20.3

19.7

20.0

19.7

19.7

Other income, net

934

1,111

500

500

500

Profit before tax

10,408

11,097

12,687

14,036

15,719

Provision for tax

1,952

2,316

2,537

2,807

3,144

% of PBT

18.8

20.9

20.0

20.0

20.0

PAT

8,457

8,781

10,150

11,229

12,575

Fully diluted EPS (`)

60.0

62.3

72.0

79.6

89.2

February 2, 2019

7

HCL Technologies | 3QFY2019 Result Update

Balance sheet (Consolidated, US GAAP)

Y/E Mar (` cr)

FY2017 FY2018 FY2019E FY2020E FY2021E

Cash and cash equivalent

1,317

1,694

574

1,437

2,733

Account receivables, net

8,301

9,639

11,615

13,123

14,725

Unbilled receivables

2,501

2,618

3,169

3,580

4,017

Deposit with banks

10,220

5,727

10,806

11,056

11,036

Deposit (one year with HDFC ltd)

-

-

-

-

-

Invest. securities, available for sale

1,146

2,357

2,251

255

3,435

Other current assets

2,983

2,520

2,825

3,125

3,126

Total current assets

26,468

24,555

31,240

32,577

39,072

Property and equipment, net

4,681

5,185

5,485

5,785

6,085

Intangible assets, net

11,426

14,406

14,406

20,775

20,775

Deposits with HDFC Ltd.

-

-

-

-

Fixed deposits with banks

-

-

-

-

-

Investment securities HTM

147

27

27

27

48

Investment in equity investee

-

-

-

-

-

Other assets

3,712

4,263

4,263

4,263

4,263

Total assets

46,432

48,435

55,420

63,426

70,243

Current liabilities

11,148

9,914

11,876

13,091

14,688

Borrowings

542

437

437

2,567

2,567

Other liabilities

1,253

1,267

2,078

2,079

2,080

Total liabilities

12,942

11,618

14,391

17,737

19,335

Minority interest

-

-

-

-

-

Total stockholder equity

33,490

36,817

41,029

45,689

50,908

Total liab. and stock holder equity

46,432

48,435

55,420

63,426

70,243

February 2, 2019

8

HCL Technologies | 3QFY2019 Result Update

Cash flow statement (Consolidated, US GAAP)

Y/E Mar (` cr)

FY2017

FY2018

FY2019E FY2020E FY2021E

Pre tax profit from operations

8,457

8,781

10,150

11,229

12,575

Depreciation

835

1,453

1,767

2,920

3,245

Expenses (deffered)/written off/others

(48)

(48)

(48)

(48)

(48)

Pre tax cash from operations

9,244

10,186

11,869

14,101

15,772

Other income/prior period ad

934

1,111

500

500

500

Net cash from operations

10,178

11,297

12,369

14,601

16,272

Tax

(1,952)

(2,316)

(2,537)

(2,807)

(3,144)

Cash profits

8,226

8,981

9,832

11,793

13,128

(Inc)/dec in current assets

(653)

(992)

(2,831)

(2,220)

(2,039)

Inc/(dec) in current liabilties

1,639

(1,233)

1,962

1,215

1,597

Net trade working capital

987

(2,225)

(869)

(1,006)

(442)

Cashflow from operating activities

9,213

6,756

8,963

10,787

12,686

(Inc)/dec in fixed assets

(358)

(504)

(300)

(300)

(300)

(Inc)/dec in intangibles

(5,006)

(2,980)

-

(6,369)

-

(Inc)/dec in investments

(242)

3,282

(4,974)

1,746

(3,160)

(Inc)/dec in minority interest

-

-

-

-

-

Inc/(dec) in non current liabilities

(11)

-

-

-

-

(Inc)/dec in non current assets

(573)

463

(305)

(300)

(1)

Cashflow from investing activities

(6,189)

260

(5,579)

(5,223)

(3,461)

Inc/(dec) in debt

-

-

-

-

-

Inc/(dec) in equity/premium

-

-

-

-

-

ESOP charges

(103)

(103)

(103)

(103)

(103)

Dividends

(3,960)

(1,980)

(5,938)

(6,569)

(7,357)

Others

1,769

(3,617)

4,350

1,681

(329)

Cashflow from financing activities

(2,294)

(5,700)

(1,690)

(4,991)

(7,788)

Cash generated/(utilised)

587

377

(1,120)

863

1,296

Cash at start of the year

729

1,317

1,694

574

1,437

Cash at end of the year

1,317

1,694

574

1,437

2,733

February 2, 2019

9

HCL Technologies | 3QFY2019 Result Update

Key ratios

Y/E Mar

FY2017 FY2018 FY2019E FY2020E FY2021E

Valuation ratio (x)

P/E (on FDEPS)

17.2

16.6

14.4

13.0

11.6

P/CEPS

15.7

14.3

12.2

10.3

9.2

P/BVPS

4.4

4.0

3.6

3.2

2.9

Dividend yield (%)

2.3

1.2

3.5

3.8

4.3

EV/Sales

2.7

2.6

2.1

1.9

1.6

EV/EBITDA

12.4

11.4

9.0

8.0

6.7

EV/Total assets

2.8

2.7

2.3

2.1

1.8

Per share data (`)

EPS (Fully diluted)

60.0

62.3

72.0

79.6

89.2

Cash EPS

65.9

72.6

84.5

100.3

112.2

Dividend

24.0

12.0

36.0

39.8

44.6

Book value

237

261

291

324

361

Dupont analysis

Tax retention ratio (PAT/PBT)

0.8

0.8

0.8

0.8

0.8

Cost of debt (PBT/EBIT)

1.1

1.1

1.0

1.0

1.0

EBIT margin (EBIT/Sales)

0.2

0.2

0.2

0.2

0.2

Asset turnover ratio (Sales/Assets)

1.0

1.0

1.1

1.1

1.1

Leverage ratio (Assets/Equity)

1.4

1.3

1.4

1.4

1.4

Operating ROE

25.3

23.9

24.7

24.6

24.7

Return ratios (%)

RoCE (pre-tax)

20.4

20.6

22.0

21.3

21.7

Angel RoIC

28.2

25.8

29.2

26.7

28.7

RoE

25.3

23.9

24.7

24.6

24.7

Turnover ratios (x)

Asset turnover (fixed assets)

10.4

10.3

11.4

12.2

13.0

Receivables days

78

72

76

74

74

February 2, 2019

10

HCL Technologies | 3QFY2019 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National

Commodity & Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and

Investment Adviser with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered

entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164.

Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in

securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of

securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate

the contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this

report. Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we

cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this

document. While Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there

may be regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or

in connection with the use of this information.

Disclosure of Interest Statement

HCL Tech

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or

No

relatives

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 2, 2019

11