Advisory Desk

March 10, 2012

Cera Sanitaryware

BUY

CMP

`220

Organic growth and changing lifestyle to be the key drivers

Target Price

`289

Cera Sanitaryware Ltd. (CSL) is the third largest sanitary ware company in the

Investment Period

12 months

organized sector with about 22% market share in India. The company is engaged

into manufacturing sanitary ware and faucet ware (commenced since September

Sector

Ceramic products

2010) products. The company also markets wellness products, which are majorly

Market Cap (` cr)

279

outsourced. Owing to the changing lifestyle of people, increasing awareness for

Beta

0.6

improving sanitation coverage, expenditure on sanitary ware has been

52 Week High / Low

248 / 150

consistently increasing as a percentage of total construction expenditure, thereby

Avg. Daily Volume

5,070

providing significant traction for the sanitary ware sector. CSL is trading at an

Face Value (`)

5

attractive PE of 7.6x and EV/Sales of 0.9x on FY2013E. We recommend Buy on

BSE Sensex

17,503

CSL with a target price of `289, based on target PE of 10x and implied EV/Sales

Nifty

5,334

of 1.1x for FY2013E.

Reuters Code

CERA.BO

Bloomberg Code

CRS.IN

Investment rationale

Increased contribution of sanitary ware towards domestic expenditure

Shareholding Pattern (%)

On the back of increasing awareness towards improving sanitation coverage,

Promoters

55.0

changing lifestyle of people towards nuclear families, the number of households is

MF / Banks / Indian Fls

4.7

increasing, thereby creating robust demand for sanitary ware products.

FII / NRIs / OCBs

3.6

Simultaneously, increased disposable income has led to a shift from the

Indian Public / Others

36.7

unbranded to branded products. This trend is likely to drive strong growth for the

sanitary ware industry going forward.

Capacity expansion and better utilisation to drive revenue growth

Abs.(%)

3m 1yr 3yr

Sensex

3.7

(5.2)

9.9

CSL is extending its installed sanitary ware capacity from 24,000MT to 32,400MT,

CSL

20.3

39.1

299.6

which is expected to be operational by 1QFY2013. Also, CSL has entered into

new avenues like production of faucet ware since September 2010 with initial

capacity of 2,500mn pieces per annum, which was previously outsourced.

Considering these factors, we expect CSL’s top line to post a 26% CAGR over

FY2011-13E.

Benefit from unmatched distribution network and high brand visibility

CSL has a very strong distribution network with 500 dealers and connection with

nearly 5,000 retailers to distribute its products. Owing to continuous marketing

activities, which are creating a high brand visibility, CSL’s advertisement cost has

witnessed a 30% CAGR over FY2007-11 and is consistently moving northwards.

Outlook and valuation

CSL’s top line is expected to grow to `385cr in FY2013E. The company’s revenue

and profit are expected to post a CAGR of 26% and 16%, respectively, over

FY2011-13E. The stock is currently trading at PE of 8.9x and 7.6x for FY2012E

and FY2013E, which makes it attractive. We recommend Buy on CSL with a target

price of `289, offering an upside of 31% from current levels.

Key financials

Sales OPM PAT EPS ROIC P/E P/BV EV/ EBITDA EV/ Sales

CSL

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2011

243

18.8

27

22

38

10.2

2.5

6.0

1.1

FY2012E

296

18.2

31

25

29

8.9

2.0

5.9

1.0

Twinkle Gosar

FY2013E

385

17.2

37

29

24

7.6

1.6

5.2

0.9

Tel: 022- 3935 7800 Ext: 6848

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Advisory Desk

Cera Sanitaryware

Investment rationale

Increased contribution of sanitary ware towards domestic expenditure

Owing to the changing lifestyle of people, the role of sanitary products has

advanced from being a necessity to a status statement - thus impacting the

spending structure of individuals and improving the proportion expended on these

basic amenities. Growth in per capita income, leading to a simultaneous increase in

the disposable income of people, has been a vital factor supporting the changing

lifestyle of people.

Also, requirement of personal space and privacy gaining an inevitable place,

subsequently leading to nuclear families, have augmented residential figures,

thereby increasing demand for sanitary products. This trend is expected to continue,

providing sustainable demand visibility for sanitary ware products.

Considering India’s dense population, its sanitation coverage is only ~40%. With

increasing awareness for improving public health, the sanitary ware segment is

expected to witness high attention.

Lastly, with aesthetics gaining a significant importance, CSL’s initiatives to provide

better designs and quality are bound to perk up its top line.

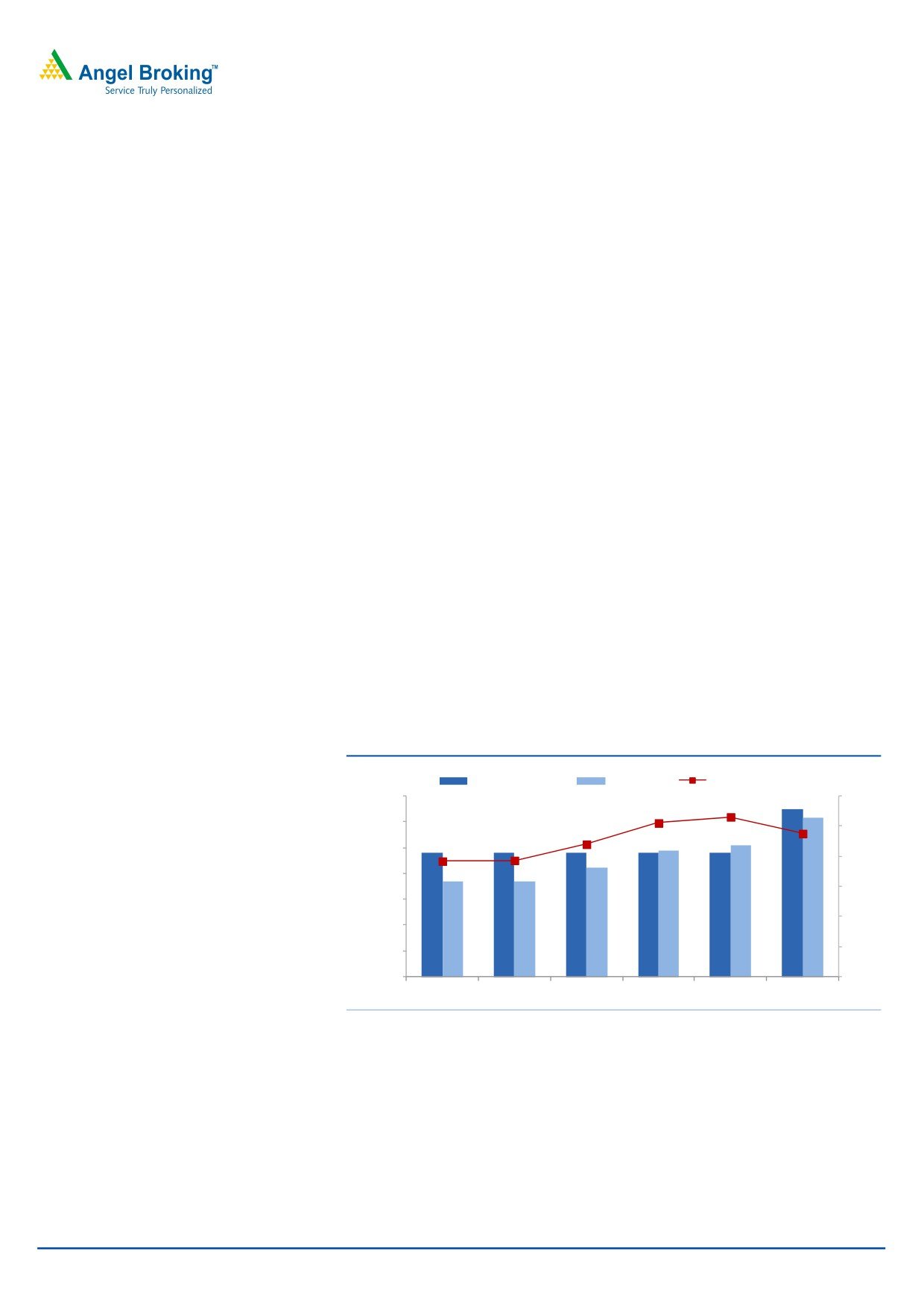

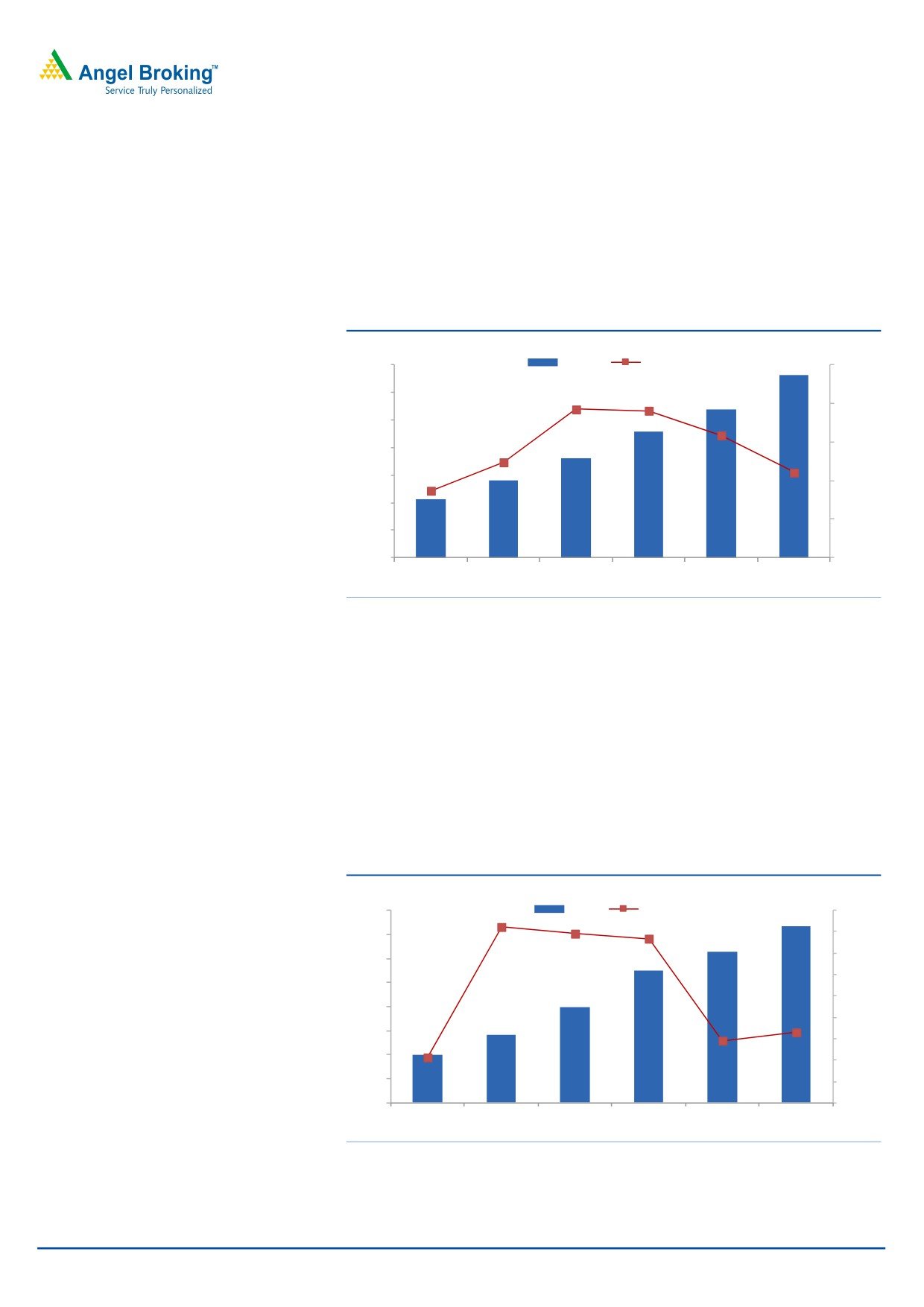

Capacity expansion and better utilisation to drive revenue growth

CSL is currently operating at its full capacity for its sanitary ware unit. The company

is expanding its sanitary ware unit’s capacity from the existing installed capacity of

24,000MT, which produces 2mn pieces per annum, to

32,400MT, which

would produce

2.7mn pieces per annum at an estimated capital outlay of

`125cr - thereby encashing the growing demand.

Exhibit 1: Capacity utilization of the sanitary ware unit

(` Cr)

(%)

Installed Capacity

Production

Capacity Utilization

35,000

120

30,000

100

25,000

80

20,000

60

15,000

40

10,000

20

5,000

0

0

FY2008

FY2009

FY2010

FY2011E

FY2012E

FY2013E

Source: Company, Angel Research

CSL started production at its faucet ware unit at Kadi in September 2010. The

company had set up this plant with an initial investment of `10cr, met by internal

accruals, with current capacity of 2,500 pieces per day, which would be doubled by

FY2014E.

Faucets, which accounted for 17% of the company’s revenue in FY2010, were

mainly outsourced directly through imports from Chinese suppliers or from domestic

markets. In-house production of the same is expected to boost the company’s

top-line going forward.

March 10, 2012

2

Advisory Desk

Cera Sanitaryware

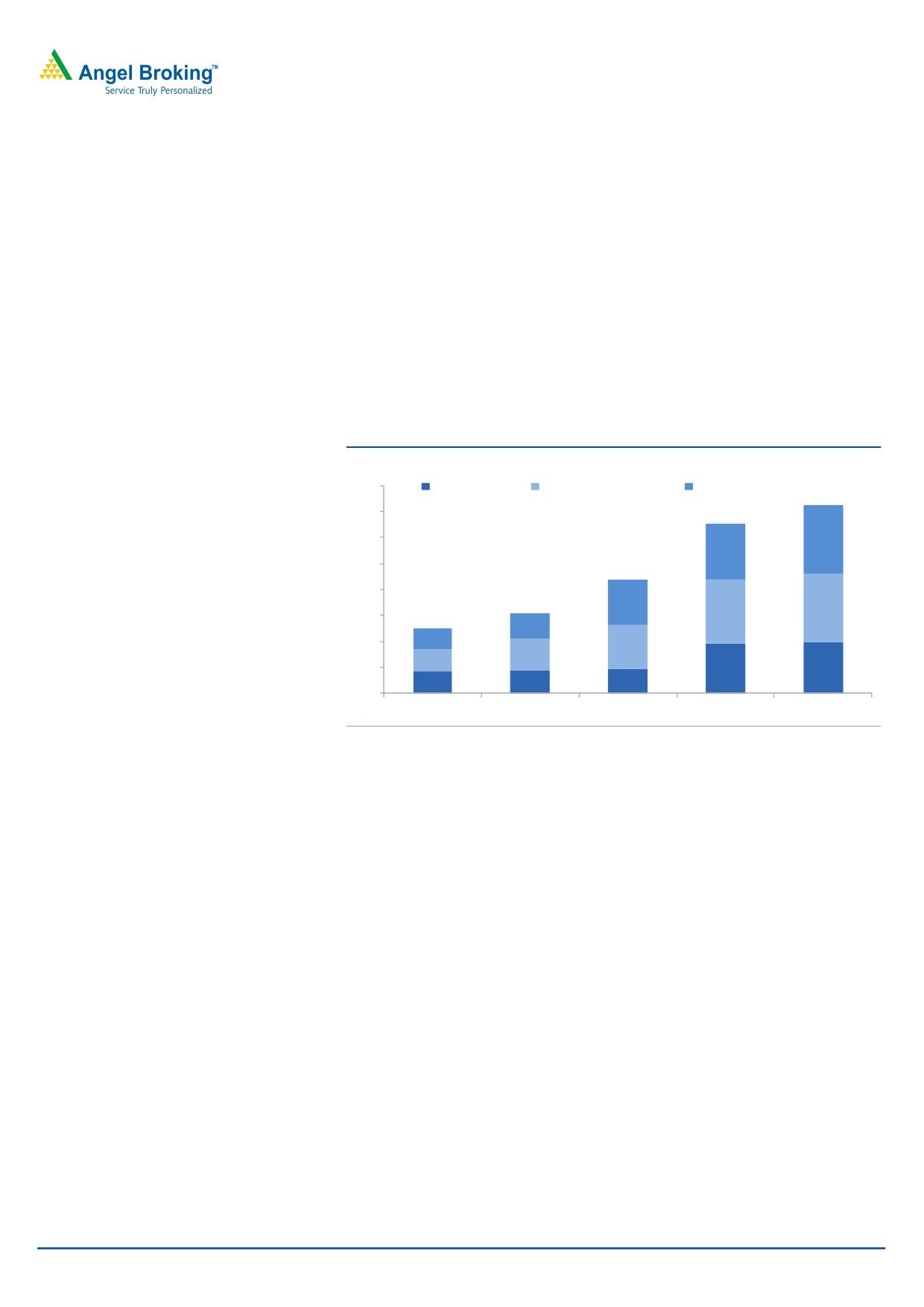

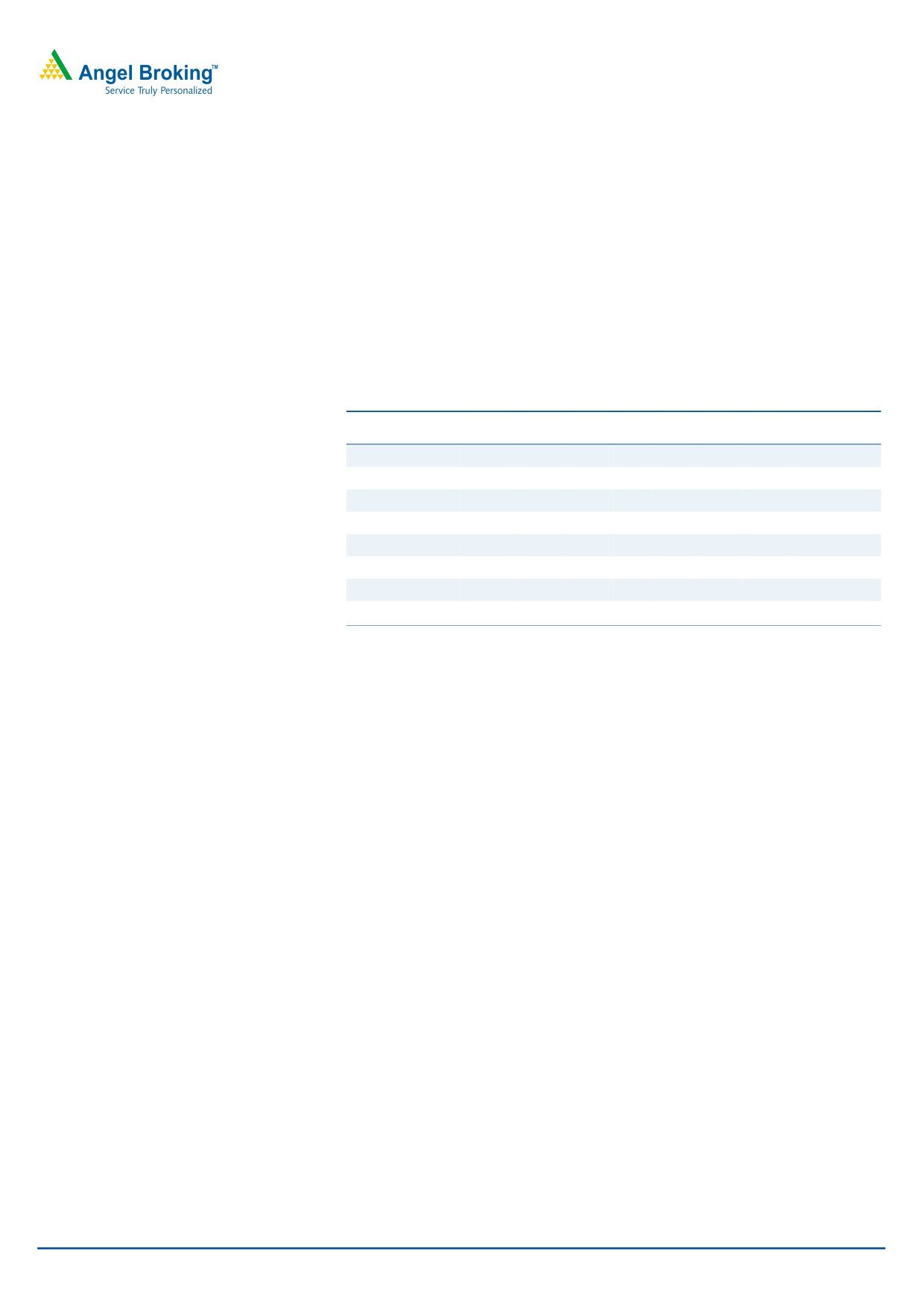

Benefit from unmatched distribution network and high brand visibility

CSL has a very strong distribution network with 500 dealers and connection with

~5,000 retailers to distribute its products. The company has established 12 major

stock points, 10 zonal sales offices and 7 bath studios pan India to establish its

presence. CSL has also initiated opening of Cera Bath Galleries in different towns.

Owing to continuous marketing activities that are creating high brand visibility, the

advertisement cost of CSL is consistently moving northwards. Marketing expenses

constitute around 15% of the company’s net sales and have witnessed a 30% CAGR

over FY2007-11. CSL has a strong foothold in northeast and central India, while the

company is eyeing southern states such as Andhra Pradesh, Tamil Nadu and

Karnataka to establish its footings.

Exhibit 2: Marketing expenses moving northwards

(` cr)

40

Advertisement

Commssion expenses

Distribution expenses

35

30

25

20

15

10

5

0

FY2007

FY2008

FY2009

FY2010

FY2011

Source: Company

Immense fresh demand on the back of the construction sector’s growth

In India, the construction sector is growing at a robust pace because of rapid

urbanization. For the sanitary ware industry, ~93% of the demand is fresh demand.

Only 7% is derived from the replacement segment, which arises out of renovations,

improvement and refurnishing. In developed economies, 20% is fresh demand,

while 80% demand is from the replacement segment. Considering the above facts,

the Indian construction sector’s development is bound to register strong growth for

sanitary ware industry and eventually for CSL.

Also, CSL is trying to tap fresh construction activities in Tier 2 and 3 cities, the

untapped potential markets, by building relationships with developers, consultants

and interior designers in these areas. Moreover, the competitive pricing policy of the

company to some extent has enabled it to secure an assured place in the

consumer’s mind.

March 10, 2012

3

Advisory Desk

Cera Sanitaryware

Company financials

Key assumptions

We expect CSL’s expanded sanitary ware capacity to be operational by

1QFY2013E; hence, we have not factored the same in our FY2012 estimates.

Following are the other key assumptions used to forecast the company’s financials:

Exhibit 3: Key assumptions

FY2011

FY2012E

FY2013E

Sanitary ware

Installed capacity (MT)

24,000

24,000

32,400

Capacity utilization (%)

102.0

106.0

95.0

Sales quantity growth (%)

14.9

12.0

20.0

Sales value growth (%)

28.5

25.0

28.4

Sale price/Unit growth (%)

11.8

7.0

7.0

Faucet ware

Installed capacity (‘000 units)

750

900

900

Capacity utilization (%)

11.6

20.0

20.0

Sales value (` cr)

0.0

5.0

12.0

Raw material

Sanitaryware, allied products value growth (%)

15.0

20.0

40.0

Traded goods value growth (%)

1.6

1.6

1.4

Sandstone/Clay value growth (%)

11.8

20.0

40.0

Brass ingots value growth (%)

0.0

20.0

35.0

Source: Company, Angel Research

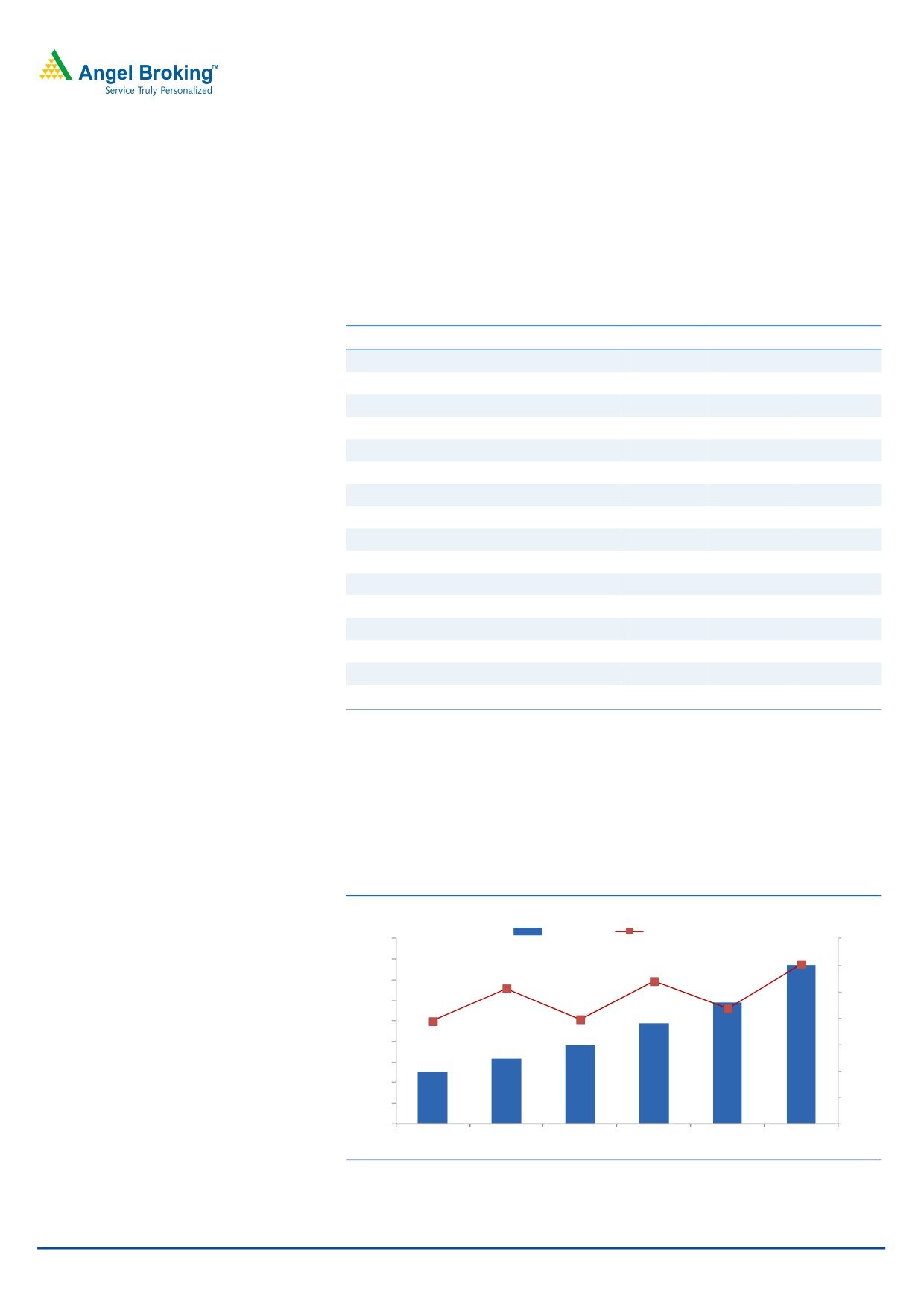

Net sales expected to post a 26% CAGR over FY2011-13E

With new developments in capacity and avenues, we expect CSL’s net sales to post

a 26% CAGR over FY2011-13E to `385 in FY2013E. Of the total sales, exports

(majorly to Gulf and Africa) contribute ~5% to sales.

Exhibit 4: Net sales and net sales growth

(` Cr)

(%)

Net Sales

Net Sales Growth

450

35

400

30

350

25

300

250

20

200

15

150

10

100

5

50

0

0

FY2008

FY2009

FY2010

FY2011E FY2012E FY2013E

Source: Company, Angel Research

March 10, 2012

4

Advisory Desk

Cera Sanitaryware

EBITDA to post a 20% CAGR over FY2011-13E

The company’s EBITDA is expected to rise from `46cr in FY2011 to `66cr in

FY2013E. However, the company’s EBITDA margin is expected to dip from 18.8% in

FY2011 to 18.2% in FY2012E and to 17.2% in FY2013E, mainly due to the increase

in raw-material cost and transport cost to some extent. CSL is operating at its full

capacity currently, thereby benefiting from economies of scale.

Exhibit 5: EBITDA and EBITDA margin

(` Cr)

(%)

70

EBITDA

EBITDA Margin

20

60

19

50

18

40

30

17

20

16

10

0

15

FY2008

FY2009

FY2010

FY2011

FY2012E FY2013E

Source: Company, Angel Research

Net profit to post a 16% CAGR over FY2011-13E

On the back of remarkable growth in top-line, bottom-line too is expected to grow

at 16% CAGR over FY2011-13E. We expect the company’s net profit to increase

from `27cr in FY2011 to `37cr in FY2013E.

Net profit margin is expected to dip from 11.3% in FY2011 to 10.3% in FY2012E

and 9.5% in FY2013E, mainly due to increase in depreciation on extended capacity

and increased interest cost. CSL’s debt-equity ratio is comfortably placed at 0.4x

FY2013E, keeping interest cost at a manageable level.

Exhibit 6: PAT and PAT growth

(` Cr)

(%)

40

PAT

PAT Growth

45

35

40

35

30

30

25

25

20

20

15

15

10

10

5

5

0

0

FY2008

FY2009

FY2010

FY2011E FY2012E FY2013E

Source: Company, Angel Research

March 10, 2012

5

Advisory Desk

Cera Sanitaryware

The company

CSL, a Gujarat-based company, is a premium bathroom solutions provider. Apart

from sanitary ware and faucet ware products, CSL also deals in wellness products,

consisting high-end and luxury bath tubs, steam cubicles, shower partitions and

shower panels. The company has also expanded its brand presence to other related

categories such as showers and PVC cistern (seat covers).

The company’s sanitary ware product, Snow White was voted Product Of The Year in

2011. The product added to the company’s list of innovations, which included

products like water-saving twin-flush coupled WCs, four-liter flush WCs and

one-piece WCs.

Sanitary ware unit

CSL has a ~22% market share in the Indian sanitary ware products market. The

company is expanding its sanitary ware production capacity from 2mn pieces per

annum currently to

2.7mn pieces per annum, nearly

25% addition, to be

operational by 1QFY2013E.

Faucet ware unit

The Indian faucet ware industry is worth ~`4,000cr. The industry offers a huge

scope of growth to CSL. Until now, the company outsourced its faucet ware products

from either China or domestic markets. However, CSL will now roll out its facet

ware products from its own plant, which started production in September 2010. The

plant is set up at Kadi, with an initial investment of `10cr (met by internal accruals)

having initial capacity of 2,500 pieces per day. This capacity will be doubled to

5,000 pieces a day by FY2014E.

Wellness products

CSL’s bath ware unit continues to market under the brand name Cera. Imported

products such as shower cubicles, shower panels and steal cubicles form part of the

unit’s product portfolio, which has helped CSL to grow at a fast pace.

Power unit

CSL has wind farms in Gujarat for captive electricity generation. The installed

capacity of the company’s wind power unit is 4.97MW. Non-conventional wind

power generation for FY2011 was 5,676MWH against 5,965MWH in FY2010.

CSL’s power requirement is met through electricity generated by its wind power unit

and DG sets, which are completely based on natural gas.

March 10, 2012

6

Advisory Desk

Cera Sanitaryware

Sanitary ware industry

The Indian sanitary ware industry, estimated to be `1,500cr-1,800cr, contributes to

~8% of the world’s sanitary ware production. The industry has a sustained growth

rate of 12-14% per annum due to increasing housing demand, purchasing power

and consciousness towards hygiene. India is emerging as the second largest

sanitary ware market in India and is expected to witness robust growth owing to the

following:

Low penetration in Indian sanitation coverage

Considering India’s dense population, its sanitation coverage is only ~40%, which

is considered to be one of the lowest in the world, thus increasing the risk of health

hazards and epidemics. With increasing awareness towards improving public

health, the sanitary ware segment is expected to witness high attention.

Changing lifestyle and rising awareness about health and fitness

Demand for premium sanitary ware products will be driven by the growing shift

towards upper-class lifestyle, rising per capita income, increasing awareness about

health and fitness and changing consumer mindsets. The concept of making a clean

and hygienic toilet is growing rapidly in rural areas, where a toilet did not even exist

a few years ago.

Wide exports horizon

Indian sanitaryware products are very competitive because of their low production

costs and, hence, export from India is increasing every day. Seven foreign brands

such as H&R Johnson, Roca and Kohler have established their operations in India.

March 10, 2012

7

Advisory Desk

Cera Sanitaryware

Competition

The Indian sanitary ware industry comprises players from the organized sector,

unorganized sector, foreign players establishing facilities in India, domestic players

and even retailers importing (mainly from China) and marketing in the domestic

market.

HSIL is the market leader in sanitary ware products with ~41% market share,

followed by Roca Parryware (~26% share) and CSL (~22% share). While in the

faucet ware segment (where the company has just entered), Jaguar has the major

market share of 45-50%.

Exhibit 7: Peer comparison

Sales

OPM

PAT

EPS ROE

P/E

P/BV

EV/EBITDA

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

CSL

FY2011

243

18.8

27

22

27

10.2

2.5

6.0

FY2012E

296

18.2

31

25

25

8.9

2.0

5.9

FY2013E

385

17.2

37

29

23

7.6

1.6

5.2

HSIL

FY2011

1,079

17.5

77

11

12

8.4

1.2

5.2

FY2012E

1,410

18.2

107

16

16

8.7

1.3

5.1

FY2013E

1,740

18.2

135

20

17

6.9

1.1

4.1

Source: Angel Research, Bloomberg

As compared to market leader HSIL, CSL has consistently given higher returns of on

equity. Considering the expansion and development plans being undertaken by the

company, CSL’s returns are expected to rise further and valuations are likely to

become more attractive on forward basis.

March 10, 2012

8

Advisory Desk

Cera Sanitaryware

Risk factors

Unorganized and local players pose the main risk to the sanitary ware

segment. Unorganized sanitary ware manufacturers enjoy the benefit of nil

excise duty and sales tax and, hence, their products are ~70% cheaper than

the organized sector’s products. The increase in excise duty, from 8% to 10%

and further to 12%, will make products from organized players more expensive.

The advent of foreign brands in India also poses a threat because people are

shifting to better, bigger brands, with increasing purchasing power.

Low-cost imports from China.

Any drastic changes in government policy related to housing construction and

imports, among others, is bound to impact the industry.

Any increase in the price of brass, the main raw material for faucets, may dent

EBITDA margin.

Any slowdown in the housing segment will cease growth, as in India the major

demand for sanitary ware is fresh demand.

March 10, 2012

9

Advisory Desk

Cera Sanitaryware

Standalone Profit and Loss Account

Y/E March (` cr)

FY2008

FY2009

FY2010

FY2011

FY2012E

FY2013E

Gross sales

139

171

200

256

311

405

Less: Excise duty

12

11

9

13

15

20

Net Sales

127

160

191

243

296

385

Other operating income

-

-

-

-

-

-

Total operating income

127

160

191

243

296

385

% chg

19.4

25.6

19.8

27.0

21.8

30.2

Net raw materials

47

59

67

86

110

147

% chg

17.4

26.1

12.8

29.6

27.2

33.4

Other Mfg costs

9

9

12

15

18

24

% chg

29.9

1.4

31.8

18.8

21.8

30.2

Power

6

5

6

12

15

19

% change

31.2

(14.1)

27.1

94.3

22.0

25.0

Personnel

19

22

23

28

40

53

% chg

33.2

14.8

3.9

21.1

44.4

32.5

Other

25

36

47

56

59

77

% chg

13.9

46.8

29.4

19.4

5.7

30.2

Total Expenditure

106

132

155

197

242

319

EBITDA

21

28

36

46

54

66

% chg

12.7

31.2

29.2

26.8

17.7

23.3

(% of Net Sales)

16.7

17.5

18.8

18.8

18.2

17.2

Depreciation & Amortisation

5

6

6

7

10

13

EBIT

16

22

30

39

44

53

% chg

6.4

34.5

36.3

30.8

11.8

20.7

(% of Net Sales)

12.9

13.8

15.7

16.1

14.8

13.7

Interest & other charges

3

4

3

3

4

6

Other Income

2

2

2

5

8

9

(% of Net Sales)

1.9

1.2

1.3

2.1

2.7

2.3

Recurring PBT

13

18

27

36

40

47

% chg

0.8

36.8

52.2

32.9

8.9

17.7

Extraordinary expense/(Inc.)

(0)

(1)

(0)

(1)

(1)

(1)

PBT (reported)

16

20

30

42

49

57

Tax

5

7

10

15

17

20

(% of PBT)

35.3

34.2

34.4

35.3

35.3

35.3

PAT (reported)

10

14

20

27

31

37

PAT after MI (reported)

10

14

20

27

31

37

ADJ. PAT

10

14

20

27

31

37

% chg

10.7

41.1

39.5

38.4

14.6

16.5

(% of Net Sales)

7.9

8.9

10.4

11.3

10.6

9.5

Basic EPS (`)

8

11

16

22

25

29

Fully Diluted EPS (`)

8

11

16

22

25

29

% chg

10.7

41.1

39.5

38.4

14.6

16.5

Dividend

1

1

2

3

3

3

Retained Earning

9

13

18

24

28

33

March 10, 2012

10

Advisory Desk

Cera Sanitaryware

Standalone Balance Sheet

Y/E March ( ` cr)

FY2008

FY2009

FY2010

FY2011

FY2012E

FY2013E

SOURCES OF FUNDS

Equity Share Capital

3

3

3

6

6

6

Preference Capital

-

-

-

-

-

-

Reserves & Surplus

55

68

85

105

134

167

Shareholders' Funds

58

71

89

112

140

173

Minority Interest

-

-

-

-

-

-

Total Loans

39

36

27

38

57

85

Deferred Tax Liability

12

14

13

14

14

14

Total Liabilities

110

120

129

163

211

272

APPLICATION OF FUNDS

Gross Block

94

99

99

113

173

233

Less: Acc. Depreciation

19

24

30

35

45

58

Net Block

76

74

69

78

128

175

Capital Work-in-Progress

1

0

2

6

3

3

Lease adjustment

-

-

-

-

-

-

Goodwill

-

-

-

-

-

-

Investments

-

-

-

8

8

8

Current Assets

71

89

120

146

148

187

Cash

11

22

34

36

13

15

Loans & Advances

8

10

17

21

26

34

Inventory

27

27

36

50

57

72

Debtors

26

31

33

39

53

66

Current liabilities

38

44

62

75

86

109

Net Current Assets

33

45

58

71

63

78

Mis. Exp. not written off

-

-

-

-

-

-

Total Assets

110

120

129

163

211

272

March 10, 2012

11

Advisory Desk

Cera Sanitaryware

Cash flow

Y/E March (` cr)

FY2008 FY2009 FY2010 FY2011 FY2012E FY2013E

Profit Before Tax

16

20

30

42

49

57

Depreciation

5

6

6

7

10

13

Interest paid

3

4

3

3

4

6

Change in WC

3

(1)

(0)

(11)

(15)

(14)

Other income

(2)

(2)

(2)

(5)

(8)

(9)

Direct taxes paid

(5)

(7)

(10)

(15)

(17)

(20)

Others

(8)

(2)

(2)

(0)

(1)

(1)

Cash from Operations

10

18

23

21

21

32

(Inc)/ Dec in Fixed Assets

(31)

(5)

(0)

(14)

(60)

(60)

(Inc)/Dec In Investments

-

-

-

8

-

-

Other Income

2

2

2

5

8

9

Others

7

(1)

(4)

(26)

(5)

(1)

Cash from Investing

(21)

(4)

(1)

(28)

(57)

(52)

Issue of Equity

0

0

0

3

-

-

Inc/(Dec) in Debt

10

(4)

(8)

11

19

28

Dividend Paid (Incl. Tax)

(1)

(1)

(2)

(3)

(3)

(3)

Interest paid

(3)

(4)

(3)

(3)

(4)

(6)

Others

5

6

3

4

-

2

Cash from Financing

11

(3)

(9)

9

12

21

Inc/(Dec) in cash

-

11

12

2

(24)

1

Opening cash balance

11

11

22

34

36

13

Closing cash balance

11

22

34

36

13

15

March 10, 2012

12

Advisory Desk

Cera Sanitaryware

Key ratios

Y/E March

FY2008

FY2009

FY2010

FY2011

FY2012E

FY2013E

Valuation Ratio (x)

P/E (on FDEPS)

27.7

19.6

14.1

10.2

8.9

7.6

P/CEPS

18.6

13.8

10.8

8.2

6.7

5.6

P/BV

4.8

3.9

3.2

2.5

2.0

1.6

Dividend yield (%)

0.3

0.4

0.6

0.2

0.2

0.2

EV/Sales

2.4

1.8

1.4

1.1

1.1

0.9

EV/EBITDA

14.4

10.5

7.5

6.0

5.9

5.2

EV / Total Assets

2.8

2.4

2.1

1.7

1.5

1.3

Per Share Data (`)

EPS (Basic)

8.0

11.2

15.7

21.7

24.8

28.9

EPS (fully diluted)

8.0

11.2

15.7

21.7

24.8

28.9

Cash EPS

11.9

15.9

20.5

26.8

32.7

39.6

DPS

0.7

1.0

1.2

2.5

2.5

2.5

Book Value

46.1

55.8

69.9

88.2

110.5

136.9

DuPont Analysis

EBIT margin

12.9

13.8

15.7

16.1

14.8

13.7

Tax retention ratio

0.6

0.7

0.7

0.6

0.6

0.6

Asset turnover (x)

1.3

1.6

2.1

2.2

1.6

1.6

ROIC (Post-tax)

10.7

14.7

21.2

22.4

15.2

13.8

Cost of Debt (Post Tax)

5.2

7.4

6.1

4.6

4.6

4.6

Leverage (x)

0.5

0.2

(0.1)

(0.1)

0.3

0.4

Operating ROE

13.4

16.1

20.0

21.4

17.9

17.2

Returns (%)

ROCE (Pre-tax)

16.7

19.1

24.0

26.8

23.4

21.9

Angel ROIC (Pre-tax)

20.0

22.3

31.3

38.1

29.3

24.4

ROE

19.1

22.0

24.9

27.4

25.0

23.4

Turnover ratios (x)

Asset Turnover

1.3

1.6

1.9

2.1

1.7

1.7

Inventory / Sales (days)

67

61

60

65

65

64

Receivables (days)

69

64

61

54

65

63

Payables (days)

129

113

124

127

129

125

WC cycle (ex-cash) (days)

65

54

46

52

61

60

Solvency ratios (x)

Net debt to equity

0.5

0.2

(0.1)

(0.1)

0.3

0.4

Net debt to EBITDA

1.3

0.5

(0.2)

(0.1)

0.7

0.9

Int. Coverage (EBIT / Int.)

5.2

5.5

11.8

14.4

10.7

8.6

March 10, 2012

13

Advisory Desk

Cera Sanitaryware

Advisory Team Tel: (91) (022) 39500777

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Cera Sanitary

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns):

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

Reduce (-5% to 15%)

Sell (< -15%)

March 10, 2012

14