IPO Note | Telecom Infrastructure

December 7, 2012

Bharti Infratel

AVOID

Issue Open: December 11, 2012

Valuations at premium

Issue Close: December 14, 2012

Bharti Infratel limited (Bharti Infratel) is tower and related infrastructure providing

Issue Details

company of Bharti group. It is one of the largest tower infrastructure providers in

terms of number of towers own and operated by a company having pan India

Face Value: `10

presence on a consolidated basis.

Present Eq. Paid-up Capital: `1742.4cr

Largest player in the sector: Bharti Infratel is one of the largest tower infrastructure

Offer Size*: 18.89cr Shares

providers in terms of number of towers own and operated by a company on a

Post Eq. Paid-up Capital: `1888.6cr

consolidated basis. Given the nationwide network of towers we believe the

company is well placed to gain an advantage over their existing and potential

Issue size (amount):** `3,967-4,534cr

competitors.

Price Band: `210-240

Long term contract provides revenue visibility: Bharti Infratel has entered into

Post-issue implied mkt cap**: `39,661cr-

MSAs with the leading wireless telecommunications service providers in India. We

45,327cr

believe long term contract agreement and the adverse consequences of contract

Promoters holding Pre-Issue: 86.1%

termination provide stability to Bharti Infratel business throughout the term of the

Promoters holding Post-Issue: 79.4%

MSAs thereby providing comfortable visibility of future revenues.

Note:*42,665,888 equity shares are for offer sale

**At the lower and upper price band, respectively

Strong parental, an advantage: The Bharti group has been one of India’s leading

business conglomerates, with operations in the telecommunications, retail,

insurance and real estate sectors. Over more than decade, company created a

Book Building

strong brand and credibility which we believe Bharti Infratel can leverage to its

QIBs

Up to 50%

advantage in growing its business.

Non-Institutional

At least 15%

Outlook and valuation: Bharti Infratel has registered a 3.4% and 9.6% CAGR in

Retail

At least 35%

towers and tenancies, respectively over the last three years. The company posted

15.9% and 21.0% revenue and EBITDA CAGR over FY2010-12. In terms of

valuation, the current IPO price band of

`210-240 implies a June

2012

Post Issue Shareholding Pattern

annualized EV/EBITDA of 11-13x, EV/tower of `0.5-0.56cr; P/E of 45-53x, and

Promoters Group

79.4

P/BV of 2.7-3.0x, which we believe is at a premium. In addition, low asset

MF/Banks/Indian

turnover and minimal use of leverage in a capital intensive industry have resulted

FIs/FIIs/Public &

in low RoE for Bharti Infratel over the past three years. Bharti Infratel’s RoE has

Others

20.6

remained in the range of 4.0-5.2 in the past couple of years. Also, the

overcapacity in the industry is expected to limit the demand for rollout of new

towers. Further, regulatory changes and the resultant uncertainty pose a risk to

telecom players as their network rollout plans could be hampered. Hence, we

recommend Avoid to the issue on account of its premium valuations.

Key financials

Y/E March (` cr)

FY2009

FY2010

FY2011

FY2012 1HFY2013

Net Sales

5,051

7,039

8,508

9,452

4972

% chg

616.3

39.4

20.9

11.1

-

Viral Shah

Adj. Net Profit

195

253

551

751

460

022-39357800 Ext: 6842

% chg

383.6

29.6

118.0

36.1

-

EBITDA Margin (%)

29.9

34.4

36.8

37.4

37.1

P/E (x) Lower End

203.1

156.8

71.9

52.8

46.5

Ankita Somani

P/E (x) Upper End

232.2

179.2

82.2

60.4

53.2

022-39357800 Ext: 6819

RoE (%)

1.9

1.9

3.9

5.2

5.8

Source: Company, Angel Research; Note: P/E and ROE for 1HFY13 calculated on an

annualized basis

Please refer to important disclosures at the end of this report

1

Bharti Infratel | IPO Note

Company Background

Bharti Infratel Limited (Bharti Infratel) is tower and related infrastructure providing

company of Bharti Group. It is one of the largest tower infrastructure providers in

terms of number of towers own and operated by a company having pan India

presence on a consolidated basis. The business of Bharti Infratel and Indus is to

acquire, build, own and operate tower and related infrastructure. Currently the

company provides access to their towers primarily to wireless telecommunications

service providers on long-term contracts and share basis. We believe there exist

opportunity for providing additional services such as signal transmission and first

level maintenance services in relation to customer equipment at towers which

Bharti Infratel is well placed to tap. Bharti Infratel client includes - Bharti Airtel

(together with Bharti-Hexacom), Vodafone India and Idea Cellular who are three

leading wireless telecommunication service providers in India by wireless revenue.

(Source: TRAI)

Bharti Infratel has a pan India presence with operations in all

22

telecommunications circles in India, with Bharti Infratel’s and Indus’ operations

overlapping in four telecommunications circles. Bharti Infratel own and operates

33,446 towers spread across 11 telecommunications circles as on June 2012

while Indus operates 109,539 towers spread across 15 telecommunications circles.

As on June 2012, the company has an economic interest of 79,452 towers

(including its 42% interest in Indus) spread across 22 telecommunication circles.

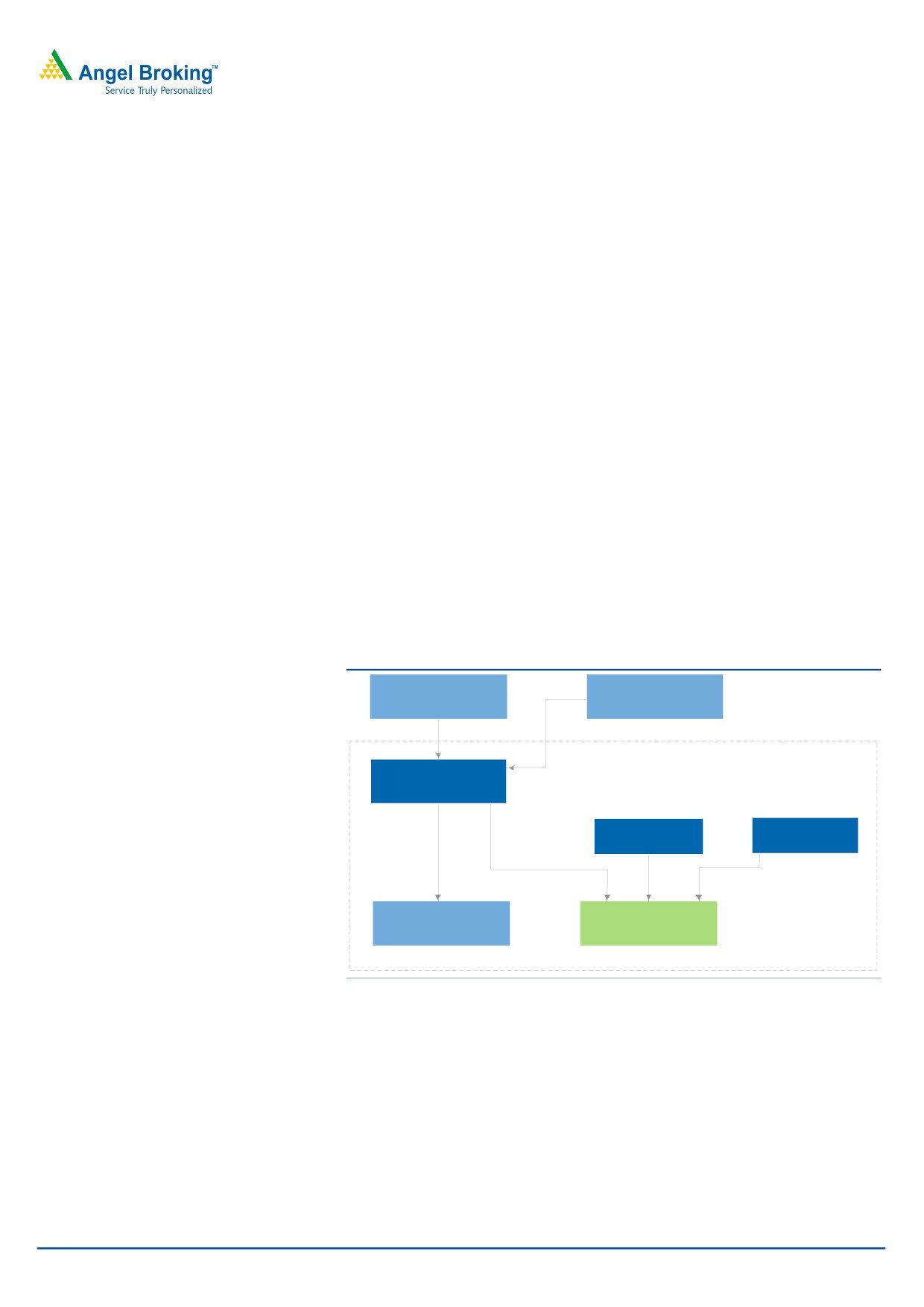

Exhibit 1: Group Structure

Bharti Airtel

Financial Investors

86.1%

13.9%

Bharti Infratel

Aidtya Birla

Vodafone India

100%

Telecom

42%

42%

16%

Bharti Infratel Ventures

Indus Towers

Source: Company, Angel Research

December 7, 2012

2

Bharti Infratel | IPO Note

Issue Details

The IPO comprises an issue of 188.9mn equity shares of face value `10 each out

of which ~146.2mn equity shares are fresh equity issue to the public and

remaining ~42.7mn equity shares are offer for sale. Bharti Infratel has fixed

the issue price band at `210-240 per share, implying an equity valuation of

`3967-4534cr (US$7.3bn-8.3bn) for the tower portfolio. The company plans to

use the IPO proceeds for installation of

4,813 towers, upgradation and

replacement of existing towers and for green initiatives at tower sites.

Exhibit 2: Objects of the issue

Particulars

Amount (` cr)

Installation of 4,813 new towers

1,086

Upgradation and replacement of existing towers

1,214

Green initiatives at tower sites

639

Source: RHP, Angel Research

Exhibit 3: Shareholding Pattern

Pre-Issue

Post-Issue

Particulars

No. of shares

(%)

No. of shares

(%)

Promoter and promoter group

1,500,000,000

86.1

1,500,000,000

79.4

Total public holding

242,408,730

13.9

388,642,842

22.3

Total

1,742,408,730

100

1,888,642,842

100

Source: Source: RHP, Angel Research

December 7, 2012

3

O Note

Investment arguments

Largest player in the sector

Bharti Infratel is one of

the largest tower infrastructure providers in terms of no. of

towers own

and operated by a company on a

consolidated basis. Given the

nationwide

network of towers we believe the company is well placed to gain an

advantage over their ex

isting and potential comp

etitors. The

costs of establishing

a tower infrastructure

business includes huge

capital expenditure required to

acquire an

d develop to

wers, high costs incurred

to comply

with local laws and

entering in

to long-term

contracts between tower

providers and wireless

service

providers.

Additionally,

a sharing operator who

requests the

creation of

a new

tower by a

nother tower

infrastructure provider will incur higher rental expense,

operating c

osts and ene

rgy costs as

the sole ope

rator at that

site, compared with

the lower r

ent and oper

ating costs of sharing an existing tower of Bharti Infratel or

Indus. Goi

ng forward,

we believe that the capacity available

on Bharti Infratel’s

and Indus’

tower portfo

lios positions them well

to capitalize

on an increase in

tower shari

ng in India.

Exhibit 4:

Installed to

wer base (As on FY2012)

00

4,0

Indus Towers

10,000

8,00

0

BSNL/MNTNL

33,000

109,000

42,000

RTIL

GTL Infra

Viom Networks

33,000

Bharti Infratel

69,

000

ATC

50,000

Tower Vision

Ascend Teelcom

Source: RHP, Angel Research

Extensive

presence

across India

Bharti Inf

ratel has

a pan India presence with operations

in all

22 telecom

munications

circles in India, with Bhart

i Infratel’s and Indus’ operations

overlappin

g in four tele

communications Circles.

The company has a significant

presence i

n B-category

and C-category telecom

munications

circles, while

Indus

operates in the metros a

nd A-category and B-cate

gory telecommunications circles.

The B-cate

gory and C-c

ategory circles have an u

ntapped consumer potential for

voice servic

es and will a

lso see increasing deman

d for data services. In addition,

rural areas

in India cur

rently suffer

from low pe

netration of

telecommunications

services, an

d we believe

that these areas offer p

otential for growth of voice and,

over time,

data service

s. Further, demand for d

ata services

increases, wireless

telecommu

nications serv

ice providers in the metro

s and A-cate

gory circles will seek

to expand

their existing

networks to

accommodat

e the roll ou

t of 3G services, as

well as new

er technolog

ies such as

4G. Given th

e absence o

f extensive wire-line

services in rural areas along with growing demand for data services in metros; we

December 7, 2012

4

Bharti Infratel | IPO Note

believe that Bharti Infratel’s and Indus’ existing portfolios of towers, will stand to

benefit as it provide customers with operational efficiencies such as strategically

located towers and faster time to market.

Long term contracts provides revenue visibility

Bharti Infratel has entered into master service agreements (MSAs) with the leading

wireless telecommunications service providers in India. This includes long-term

contracts which set out the terms on which access is provided to Bharti Infratel

towers. All of the service provided is being offered substantially at the same terms

and receiving equal treatment at towers where they have installed their active

infrastructure. This helps in co-locations and encourages telecommunications

service providers in India to use the tower infrastructure of Bharti Infratel. Bharti

Infratel has

27,276 co-locations as of June

30,

2012 from wireless

telecommunications service providers other than Bharti Airtel. We believe long term

contract agreement and the adverse consequences of contract termination provide

stability to Bharti Infratel business throughout the term of the MSAs thereby

providing comfortable visibility of future revenues.

Comfortable balance sheet

The costs of establishing a tower infrastructure business includes huge capital

expenditure required to acquire and develop towers. The balance sheet is relatively

unlevered with 2QFY2013 net debt/EBITDA at 0.8x. This leaves room for inorganic

expansion in India and abroad. Given its strong balance sheet and ready access to

capital we believe Bharti Infratel has the ability to expand their tower portfolio at

the rate, in the manner and within the constraints required by wireless

telecommunications service providers.

Strong relationship with parental

The Bharti group has been one of India’s leading business conglomerates, with

operations in the telecommunications, retail, insurance and real estate sectors.

Over more than decade, company created a strong brand and credibility which we

believe Bharti Infratel can leverage to its advantage in growing its business.

Further, pursuant to a letter agreement dated September 8, 2012, Bharti Airtel has

granted Bharti Infratel a right of first refusal in relation to all of Bharti Airtel’s new

tower and co-location requirements. We believe that this strong relationship with

Bharti Airtel is a significant advantage, and that Bharti Infratel will continue to

benefit from it as Bharti Airtel expands its operations across India.

December 7, 2012

5

Bharti Infratel | IPO Note

Key concerns

Decline in demand can lead to lower revenue

The business of Bharti Infratel consists of building, acquiring, owning and

operating tower and related infrastructure and providing access to these towers

primarily to wireless telecommunications service providers. Factors such as

(a)decrease in consumer demand, (b)deterioration in the financial condition of

wireless telecommunications service providers owing to declining tariffs, media

convergence or other factors or their access to capital adversely, (c)decrease in the

overall growth rate of wireless telecommunications and (d)ability and willingness of

wireless telecommunications service providers to maintain or increase capital

expenditures affects the demand for tower space in India which may adversely

affect operating results of these operators.

High dependence on factors affecting telecommunication

industry

Bharti Infratel performance is directly related to the performance of the Indian

wireless telecommunications industry and is therefore affected by factors that

generally affect that industry. The wireless telecommunications industry is sensitive

to factors such as consumer demand and wireless telecommunications service

providers’ debt levels, their ability to service their debt and other obligations and

general economic conditions. In addition, the Indian telecommunications industry

may face policy changes in response to recent industry developments. We believe

such adverse industry conditions and increased cost pressure on customers may

result in Bharti Infratel having to reduce rents or in co-location exits in excess of

those permitted under the MSAs affecting profitability of the company going

forward.

Competition may lead to margin compression

The tower infrastructure business in India is highly competitive in nature. The

company faces strong competition in the market from the tower infrastructure

provided by wireless telecommunications service providers, tower infrastructure

companies backed by wireless telecommunications service providers and

independent tower infrastructure companies. Increasing competition in the tower

industry and increasing tariff pressures on Bharti Infratel may create pricing

pressures that may adversely affect operating performance of the company.

Policy paralysis could hamper growth

The Indian telecommunications industry may face policy changes in response to

recent industry developments, including the cancellation of 2G licenses’ issued to

certain wireless telecommunications service providers. Also the standardization of

telecommunications tower designs could result in Bharti Infratel having to make

modifications to their existing towers, which may be costly and could have an

adverse effect on their cash flows and profitability.

December 7, 2012

6

Bharti Infratel | IPO Note

Outlook and valuation

Bharti Infratel has registered a 3.4% and 9.6% CAGR in towers and tenancies,

respectively over the last three years. The company posted 15.9% and 21.0%

revenue and EBITDA CAGR over FY2010-12. In terms of valuation, the current IPO

price band of `210-240 implies a June 2012 annualized EV/EBITDA of 11-13x,

EV/tower of `0.5-0.56cr; P/E of 45-53x, and P/BV of 2.7-3.0x, which we believe is

at a premium. In addition, low asset turnover and minimal use of leverage in a

capital intensive industry have resulted in low RoE for Bharti Infratel over the past

three years. Bharti Infratel’s RoE has remained in the range of 4.0-5.2 in the past

couple of years. Also, the overcapacity in the industry is expected to limit the

demand for rollout of new towers. Further, regulatory changes and the resultant

uncertainty pose a risk to telecom players as their network rollout plans could be

hampered. Hence, we recommend Avoid to the issue on account of its premium

valuations.

December 7, 2012

7

O Note

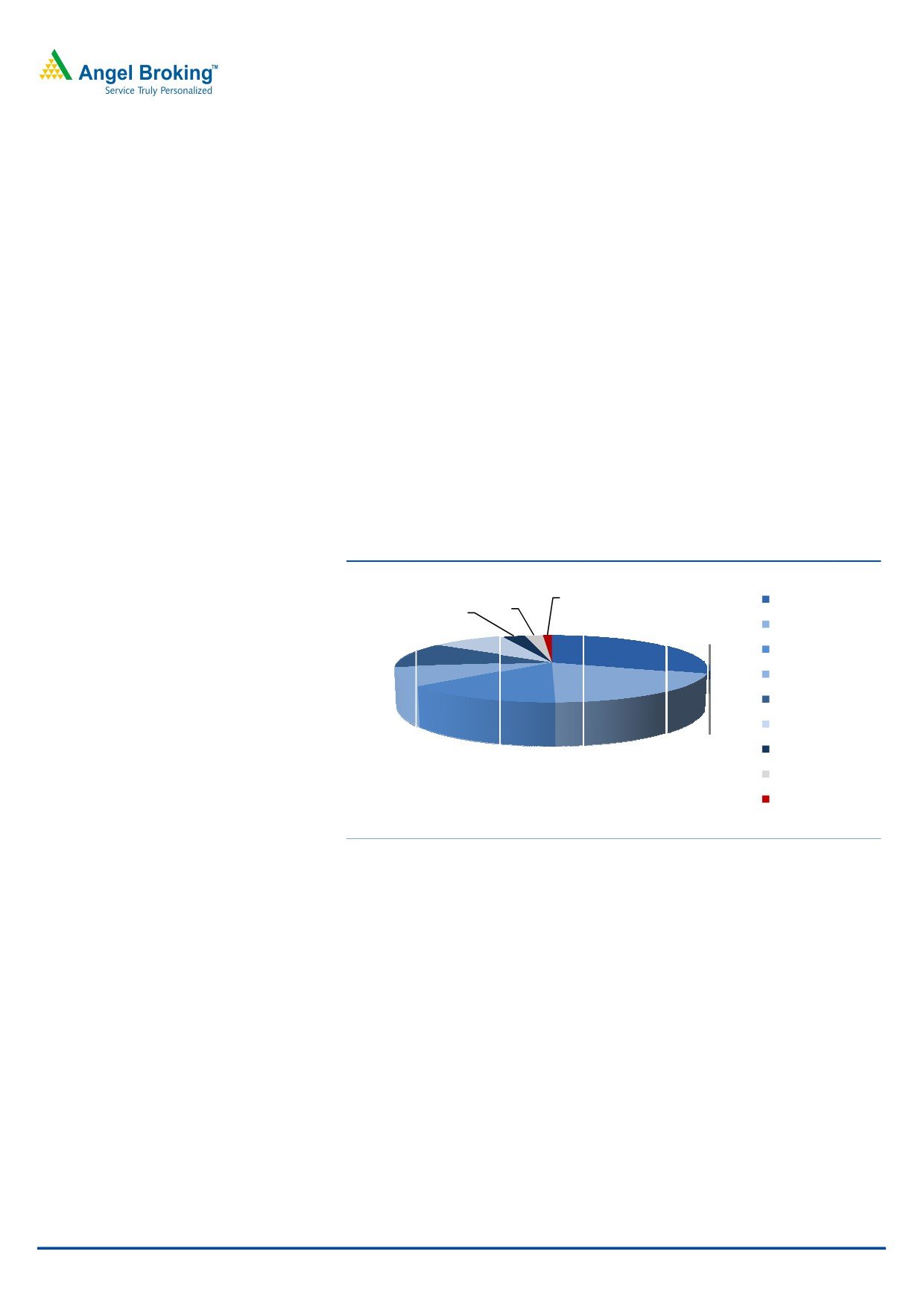

Industry

Overview

Indian w

ireless telecommunication serv

ices sector

The focus

of Indian operators in the

last ten year

s or so has

been to develop an

affordable

mass market telecommuni

cations servic

e model whi

ch allows for service

availability

across India’

s urban and

rural areas at affordable prices. Over t

he five-

year period 2005-2010, the wireless telecommuni

cations servic

es sector has grown

rapidly (So

urce: CRISIL.)

. Industry rev

enue reached

`1,361bn at the end of

March

2012 (Sour

ce: Analysys

Mason.), and

the mobile su

bscriber base rose to arou

nd 919

million at the end of Ma

rch 2012 fro

m 99mn at th

e end of 2005-2006. The Indian

telecommu

nications industry is one o

f the most c

ompetitive gl

obally with o

ver ten

operators e

xisting in the

market. How

ever, the bul

k of the reve

nue market s

hare is

concentrate

d amongst th

e top three o

perators.

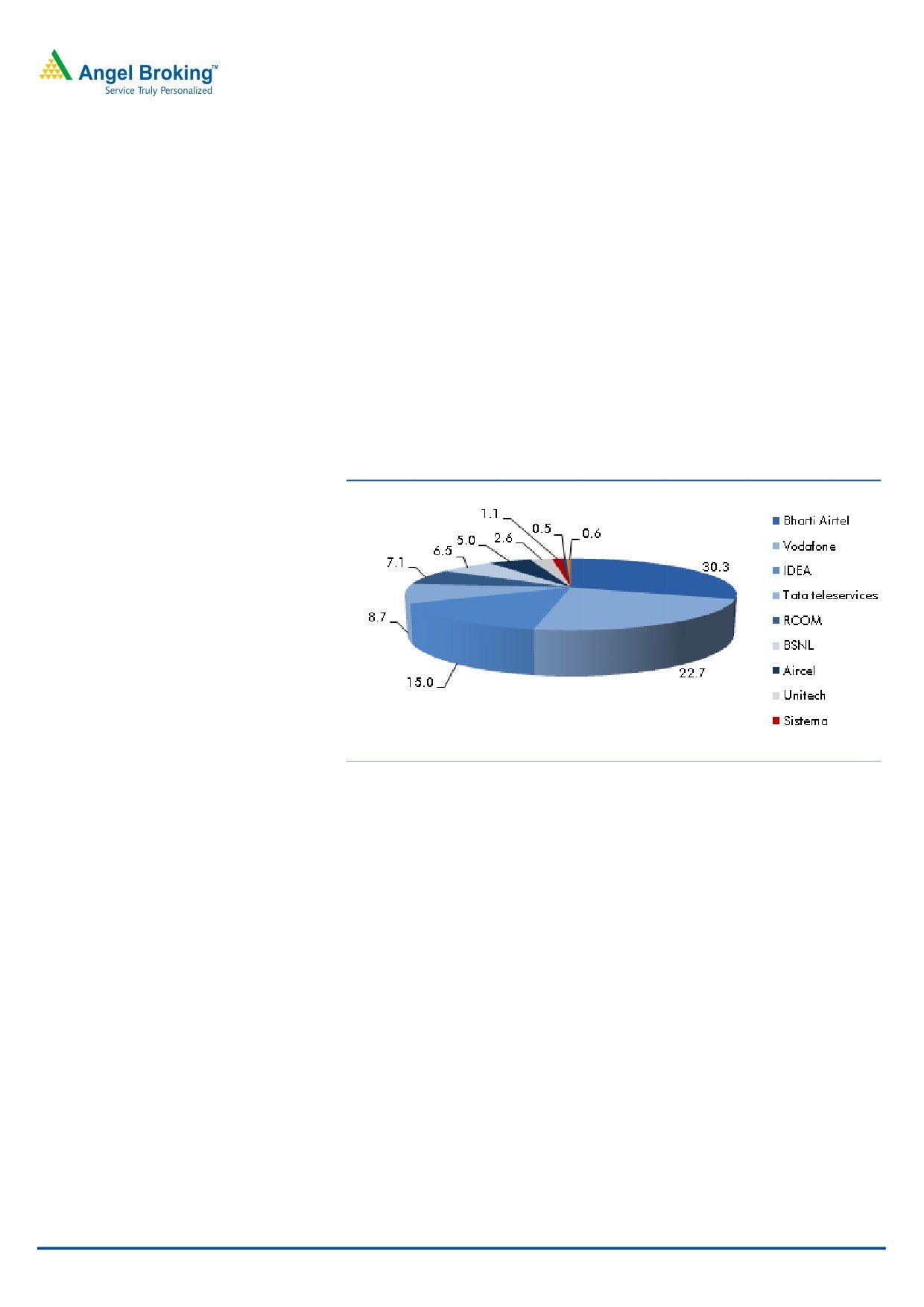

Exhibit 5:

Market Sha

re in terms

Revenue (%) (As on Ju

ne 30,2012

)

Source: RHP, Angel Research

; Note: Others includes Loop Mobile, Loop Te

lecom, Videoco

n, HFCL,

Etisalat, S-Tel

Trend in

mobile su

bscribers (

historical)

for 2G and

3G servic

es

In the case

of 2G sub

scribers, the

availability a

nd affordab

ility of servic

es has

resulted in

a significant

increase in th

e wireless us

er base. This subscriber ba

se has

risen from

261 million

in the fiscal

year 2008 t

o 868 millio

n in the fisc

al year

2012. Ther

e are an esti

mated 640,0

00 2G instal

led base stat

ions in India across

operators

and Circles,

translating i

nto around

1,360 2G su

bscribers pe

r base

station. (So

urce: Analys

ys Mason.) T

he penetratio

n of 3G ha

s remained l

imited,

due to limi

ted device p

enetration, in

itial glitches

in the user e

xperience ow

ing to

coverage i

ssues and m

ore importa

ntly service p

ricing relativ

e to the pri

cing of

GPRS / ED

GE. With de

clining price

s of 3G serv

ices in India

, the adoptio

n and

traffic has i

ncreased acr

oss telecomm

unications C

ircles and is e

xpected to c

ontinue

to grow w

ith increasin

gly good ser

vice and de

vice afforda

bility and co

verage

expansion.

Indian to

wer indus

try

Wireless tel

ecommunica

tions service

providers hav

e made cons

iderable inve

stment

in building

network in

frastructure t

o address t

he high sub

scriber grow

th and

consequent increase in traffic. The extent and spread of infrastructure a

nd the

December 7, 2012

8

Bharti Infratel | IPO Note

number of subscribers supported by the infrastructure created by operators is

dependent upon the subscriber base, usage per subscriber, stage of network

rollout by the operator, technology platform, frequency band of operation and

spectrum availability. Typically, for a GSM operator providing 2G services, the

number of subscribers that are served by a base transceiver station (“BTS”) is 850

to 1,200. This number could vary based on the technology, the spectrum and

other factors. (Source: CRISIL.)

Trend in number of tenancies (historical) for 2G and 3G

Industry tenancy has grown from 1.05 in 2007-2008 to 1.70 in 2011-2012.

Tower tenancy currently stands at 1.70 times for 2G towers, of which tenancies for

telco-owned tower companies are estimated at around 1.94 times and tenancies

for independent telcos are estimated at around 1.46 times. Consolidation among

tower companies will further increase the tenancy ratio; consolidation among

tower companies will lower the proportion of operator-owned tower assets.

(Source: Analysys Mason.) The tenancy metrics vary by tower Company and reflect

the genesis of these tower companies. Large tower companies such as Indus

towers were formed by a carve-out of the tower portfolio of multiple operators,

and hence have a high captive tenancy.

Exhibit 6: Tenancies for telco owned tower companies

Exhibit 7: Tenancies for independent tower companies

2.50

2.38

2.38

2.50

1.94

1.94

2.00

1.84

1.82

2.00

1.84

1.82

1.50

1.50

1.00

1.00

1.00

0.50

0.50

0.00

0.00

Viom Networks Indus towers

RTIL

Bharti Infratel BSN/MTNL

ATC

Tower Vision

Ascend Towers

GTL Infra

Sharing ratio for captive towers

Sharing ratio for captive towers

Source: RHP, Angel Research

Source: RHP, Angel Research

December 7, 2012

9

Bharti Infratel | IPO Note

Income statement

Y/E March (` cr)

FY2008 FY2009 FY2010 FY2011 FY2012

Revenue from operations

705

5,051

7,039

8,508

9,452

Other income

1

127

90

118

145

Total income

706

5,177

7,129

8,626

9,597

Power and fuel expenses

258

1,946

2,525

3,015

3,358

Rent

71

527

880

977

1,058

Employee benefit expenses

18

131

240

285

298

Other expenses

100

936

975

1,101

1,199

Total expenses

447

3,540

4,620

5,379

5,913

EBITDA

258

1,510

2,418

3,129

3,539

Dep. and amortization exp.

203

1,477

1,996

2,245

2,371

EBIT

55

33

423

884

1,168

Less: Adjustment

(40)

(240)

(234)

(226)

(225)

Finance expenses

34

114

354

433

407

PBT

62

285

393

795

1,131

Tax

Current tax

7

45

80

169

305

Less: MAT credit

(7)

(45)

(80)

(113)

(64)

Deferred tax

21

89

140

187

139

Fringe benefit tax

0

1

-

-

-

PAT

40

195

253

551

751

December 7, 2012

10

Bharti Infratel | IPO Note

Balance Sheet

Y/E March (` cr)

FY2008

FY2009

FY2010

FY2011

FY2012

Non-current assets

Tangible assets

11,539

16,227

17,552

17,634

16,701

Intangible assets

-

4

23

33

27

Capital WIP

402

953

365

288

186

Deferred tax assets

1

38

21

-

-

Long term loans and advances

295

475

698

1,081

1,130

Other non-current assets

29

224

605

944

1,217

Current assets

Current investments

3,193

287

395

246

336

Trade receivables

86

405

901

699

683

Cash and bank balances

148

209

681

14

48

Short-term loans and advances

375

1,612

790

1,926

2,568

Other current assets

0

292

480

426

579

Total assets

16,066

20,728

22,512

23,289

23,474

Non-current liabilities

Long term borrowings

3,026

1,377

3,966

3,717

2,389

Deferred tax liabilities

180

306

429

596

735

Other long term liabilities

149

860

1,404

1,773

1,852

Long term provisions

522

999

577

499

514

Current liabilities

Short term borrowings

109

1,207

325

547

770

Trade payables

256

92

419

221

402

Other current liabilities

1,568

5,532

1,757

1,932

2,279

Short term provisions

1

3

8

10

10

Total liabilities

5,811

10,376

8,885

9,294

8,950

Total sharecapital

0

541

581

581

581

Securities premium account

2,017

1,595

4,759

4,759

4,759

Stock option outstanding account

-

23

76

122

137

General rReserve

8,198

7,958

7,724

7,494

7,258

Net surplus (profit and loss)

40

236

489

1,039

1,790

Total Reserves and surplus

10,255

9,811

13,047

13,414

13,943

Net worth

10,255

10,352

13,628

13,995

14,524

Total equity and liabilities

16,066

20,728

22,512

23,289

23,474

December 7, 2012

11

Bharti Infratel | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

December 7, 2012

12

Bharti Infratel | IPO Note

6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai- 400 093. Tel: (022) 39357800

Research Team

Fundamental:

Sarabjit Kour Nangra

VP-Research, Pharmaceutical

Vaibhav Agrawal

VP-Research, Banking

Bhavesh Chauhan

Sr. Analyst (Metals & Mining)

Viral Shah

Sr. Analyst (Infrastructure)

Sharan Lillaney

Analyst (Mid-cap)

V Srinivasan

Analyst (Cement, Power, FMCG)

Yaresh Kothari

Analyst (Automobile)

Ankita Somani

Analyst (IT, Telecom)

Sourabh Taparia

Analyst (Banking)

Bhupali Gursale

Economist

Vinay Rachh

Research Associate

Amit Patil

Research Associate

Shareen Batatawala

Research Associate

Twinkle Gosar

Research Associate

Tejashwini Kumari

Research Associate

Technicals:

Shardul Kulkarni

Sr. Technical Analyst

Sameet Chavan

Technical Analyst

Sacchitanand Uttekar

Technical Analyst

Derivatives:

Siddarth Bhamre

Head - Derivatives

Institutional Sales Team:

Mayuresh Joshi

VP - Institutional Sales

Hiten Sampat

Sr. A.V.P- Institution sales

Meenakshi Chavan

Dealer

Gaurang Tisani

Dealer

Akshay Shah

Sr. Executive

Production Team:

Tejas Vahalia

Research Editor

Dilip Patel

Production Incharge

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE: INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP /

December 7, 2012

13