Please refer to important disclosures at the end of this report

1

Angel Top Picks – March 2021

Indian equities rallied sharply on back of a bold budget by the Government –

Indian equities rallied by 6.6% in January post the 2.5% correction last month.

Markets rallied on back of the bold Union Budget with a clear focus on reviving

growth through deficit spending. FPI flows for February improved to `25,787 cr.

from ` 19472 cr in January.

Indian Economic activity back to pre-Covid levels in Q3FY21- GDP data

released by the Government points to significant improvement in the economy in

Q3FY21 led by recovery in the Industrial sector. Real GDP growth for Q3FY21

stood at 0.4% YoY as compared to contraction of 24.3% and 7.3% in Q1FY21 and

Q2FY21 respectively. With this positive growth rate, the Indian economy has now

returned to its pre Covid levels of activity. Growth in the manufacturing and

constructing sectors has rebounded strongly to 1.6% and 6.2% respectively in

Q3FY21 as compared to contraction of 35.9% and 49.4% in Q1FY21. However,

services sector witnessed a marginal contraction of 1.0% YoY for Q3 as compared

to a contraction of 21.4% in Q1. Agriculture growth remained stable at 3.9% for the

quarter as compared to 3.3% in Q1FY21.

High frequency indicators point to further improvement in the economy in the

fourth quarter - High frequency indicators like the manufacturing PMI, services

PMI and auto sales numbers point to continued improvement in the underlying

economy in line with the GDP report. Manufacturing PMI for February was very

strong at 57.5, well above the long-term average of 53.6. Services PMI of 52.8 for

January also points to an expansion though at a slower pace as compared to

manufacturing. Moreover, the services PMI also rose sharply to 55.3 in February

with output expanding at the sharpest rate in over a year.

Positive global sentiments leading to a broad-based rally - Currently the US

Government is working on a third fiscal stimulus package of USD 1.9tn currently

being discussed in their parliament. If the US Government is able to pass the USD

1.9tn stimulus package then it would be positive for global equities. Vaccination

programs globally are proceeding as per schedule which is positive. Mass

vaccination has already commenced globally and we should see significant

progress over the next couple of quarters. Given the continued improvement in the

economy, abundant global liquidity and strong earnings growth we remain positive

on the markets from a medium to long term horizon despite any short-term volatility.

Top Picks Performance

Return Since Inception (30th Oct, 2015)

Top Picks Return

124.9%

BSE 100

79.7%

Outperformance

45.2%

Source: Company, Angel Research

Exhibit 1: Top Picks

Company

CMP (₹)

TP (₹)

IT

HCL Technologies

941.3

1,161

Auto

GNA Axles

394.6

500

NRB Bearings

116.8

135

Escorts

1318

1,573

Banking

IDFC First Bank

66.8

77

Federal Bank

87.3

110

Shri.City Union

1519

1,800

Chemicals

Galaxy Surfact.

2360

2,750

Cement & Infra

JK Lakshmi Cement

428.2

470

PNC Infratech

268.4

302

Others

Carborundum Universal

502.9

600

PVR

1452.6

1800

Source: Company, Angel Research

Note: Closing price as on 5th March, 2021

Angel Top Picks | March 2021

March 8, 2021

2

Top Picks

Angel Top Picks | March 2021

March 8, 2021

3

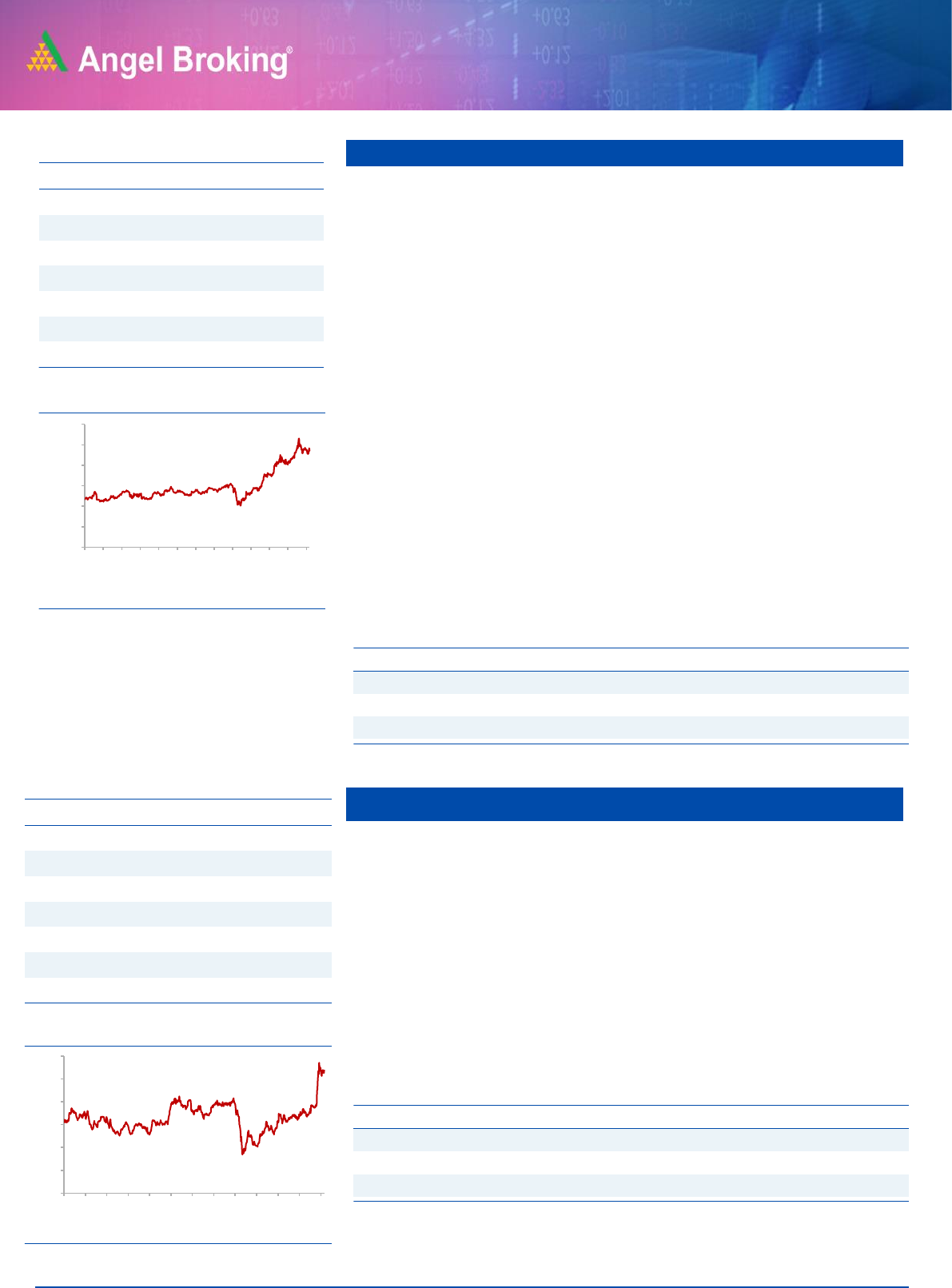

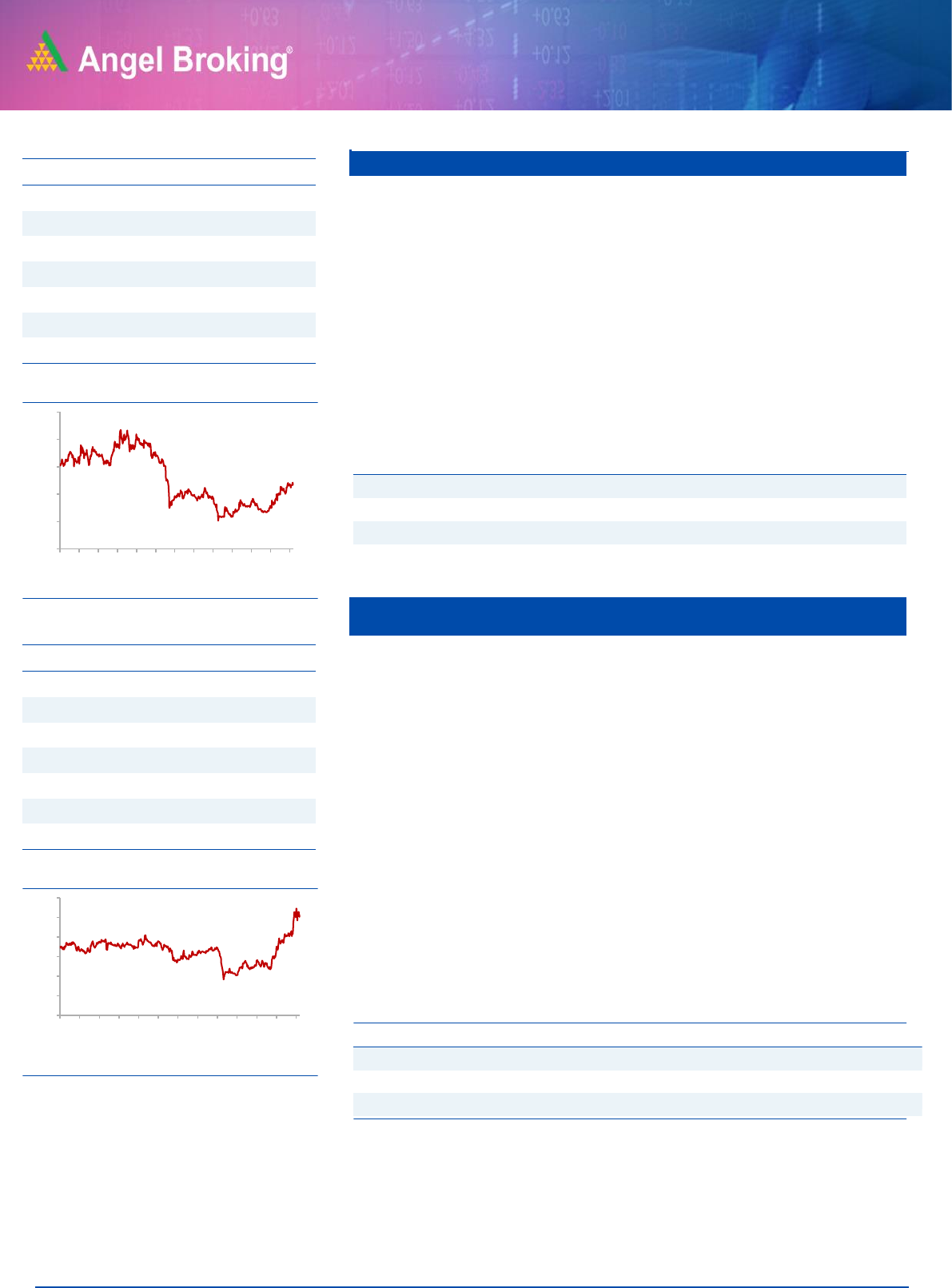

PNC Infratech

HCL Tech

HCL Tech is amongst the top four It services companies based out of India and

provides a vast gamut of services like ADM, Enterprise

solutions, Infrastructure management services etc. HCL Tech Q3FY21

revenues grew by 4.4% qoq. Operating profit for the quarter was up by 9.9%

qoq while EBIT margins were up by ~130bps qoq to 22.9%..

Net profit for the quarter was up by 26.3% qoq to ₹3,918 crore. While the

Q1FY21 numbers were marginally ahead of our estimates in terms of revenue

growth the expansion in margins despite wage hikes during the quarter was a

pleasant surprise. Management has highlighted that demand and supply

related issues are now over for the company and the deal pipeline has

improved significantly since September led by cloud related services.

Management has guided for 2.0-3.0% qoq growth in revenue in constant

currency terms for the rest of the year providing visibility. At CMP the stock is

trading at a P/E multiple of 17.0x FY22 EPS estimate which is at a significant

discount to the other large cap IT companies like Infosys and TCS and offers

tremendous value at current levels given market leader status in Infrastructure

management.

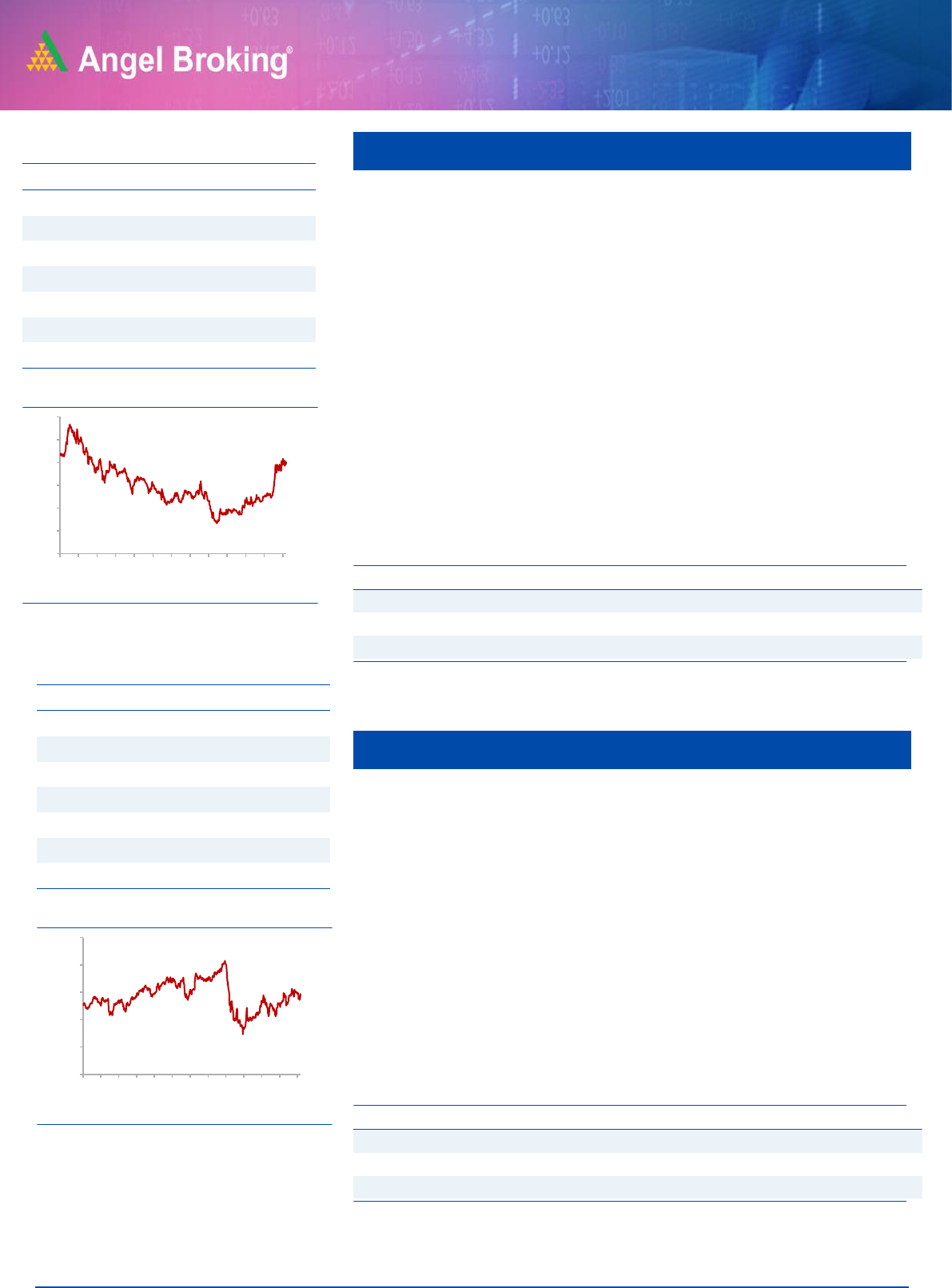

PNC Infratech is a mid-sized road EPC player. It has more than two decades

of experience in executing projects for marquee clients such as NHAI, UPEIDA,

MSRDC, UPPCL etc.

Company has a strong and healthy order book. On an F20 basis it has a book

to bill ratio of more than 3.5x. PNC has a track record of completing projects

ahead of timelines, as a result of which it is eligible for early completion bonus

from its clients.

Key Financials

Y/E

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

FY2021E

75806

21.8

13563

49.3

22.1

19.1

8.4

3.2

FY2022E

89736

22.4

15657

56.9

21.6

16.5

7.1

2.6

Source: Company, Angel Research

Key Financials

Y/E

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

FY2021E

4862

13.8

343

13.4

12.7

20.1

2.4

1.3

FY2022E

5574

14.1

445

17.4

14.5

15.5

2.1

1.2

Source: Company, Angel Research

Stock Info

CMP

268

TP

302

Upside

12.5%

Sector

Infra

Market Cap (` cr)

6885

Beta

0.86

52 Week High / Low

285/84

3 year-Chart

Source: Company, Angel Research

-

50

100

150

200

250

300

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

Stock Info

CMP

941.3

TP

1161

Upside

23.3%

Sector

IT

Market Cap (` cr)

255437

Beta

0.7487

52 Week High / Low

1062/405

3 year-Chart

Source: Company, Angel Research

-

200

400

600

800

1,000

1,200

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

Angel Top Picks | March 2021

March 8, 2021

4

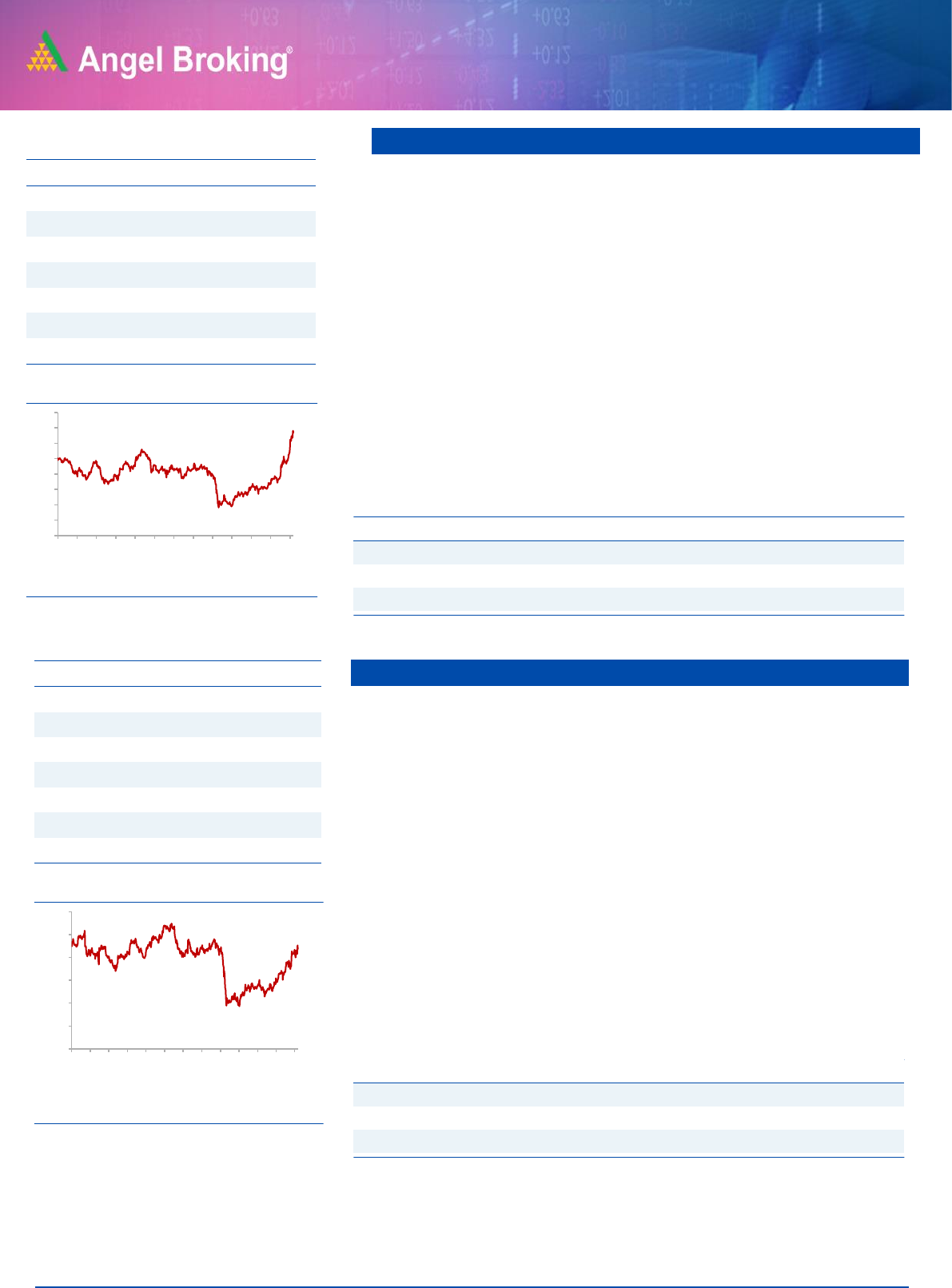

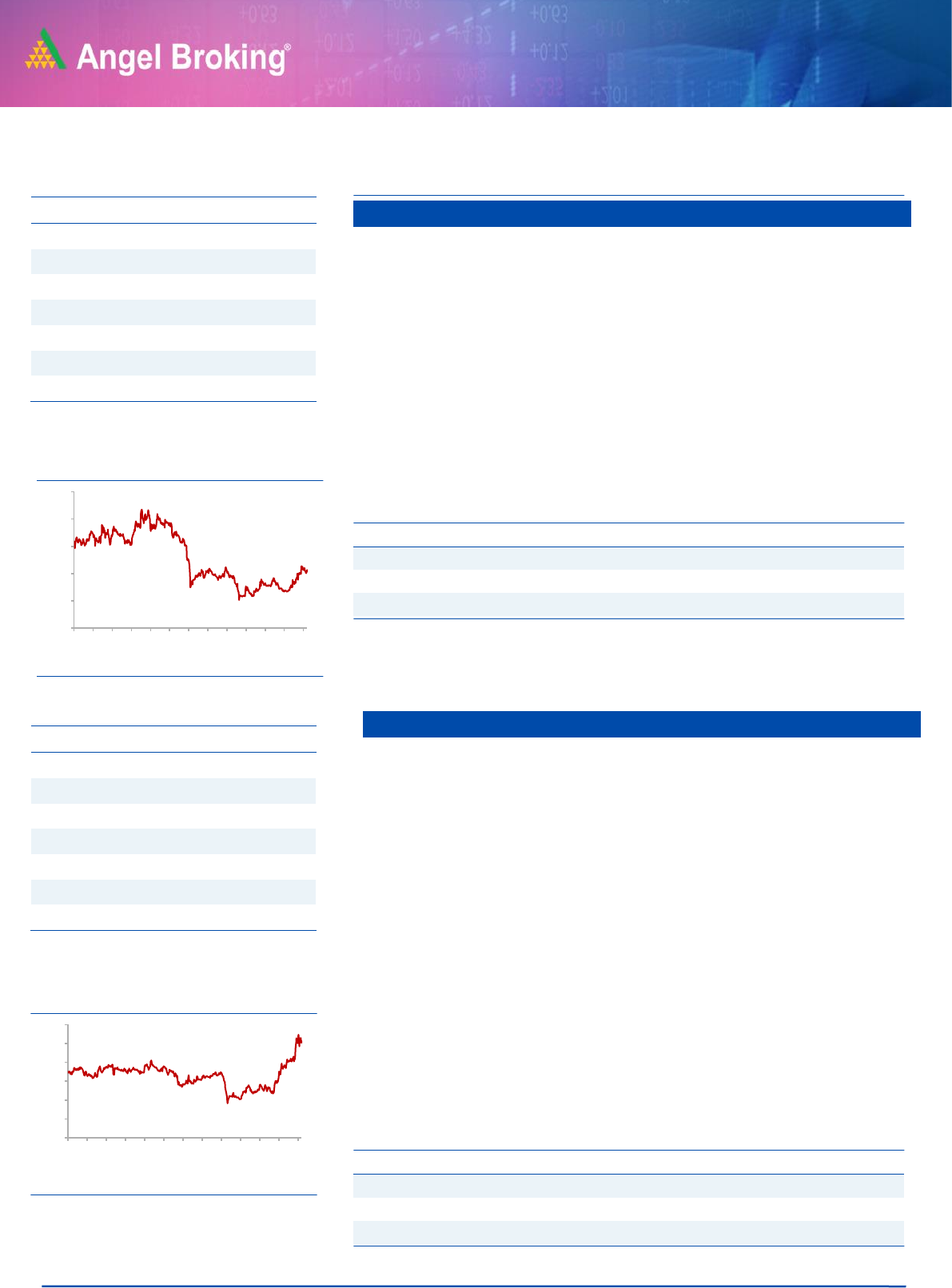

Federal Bank

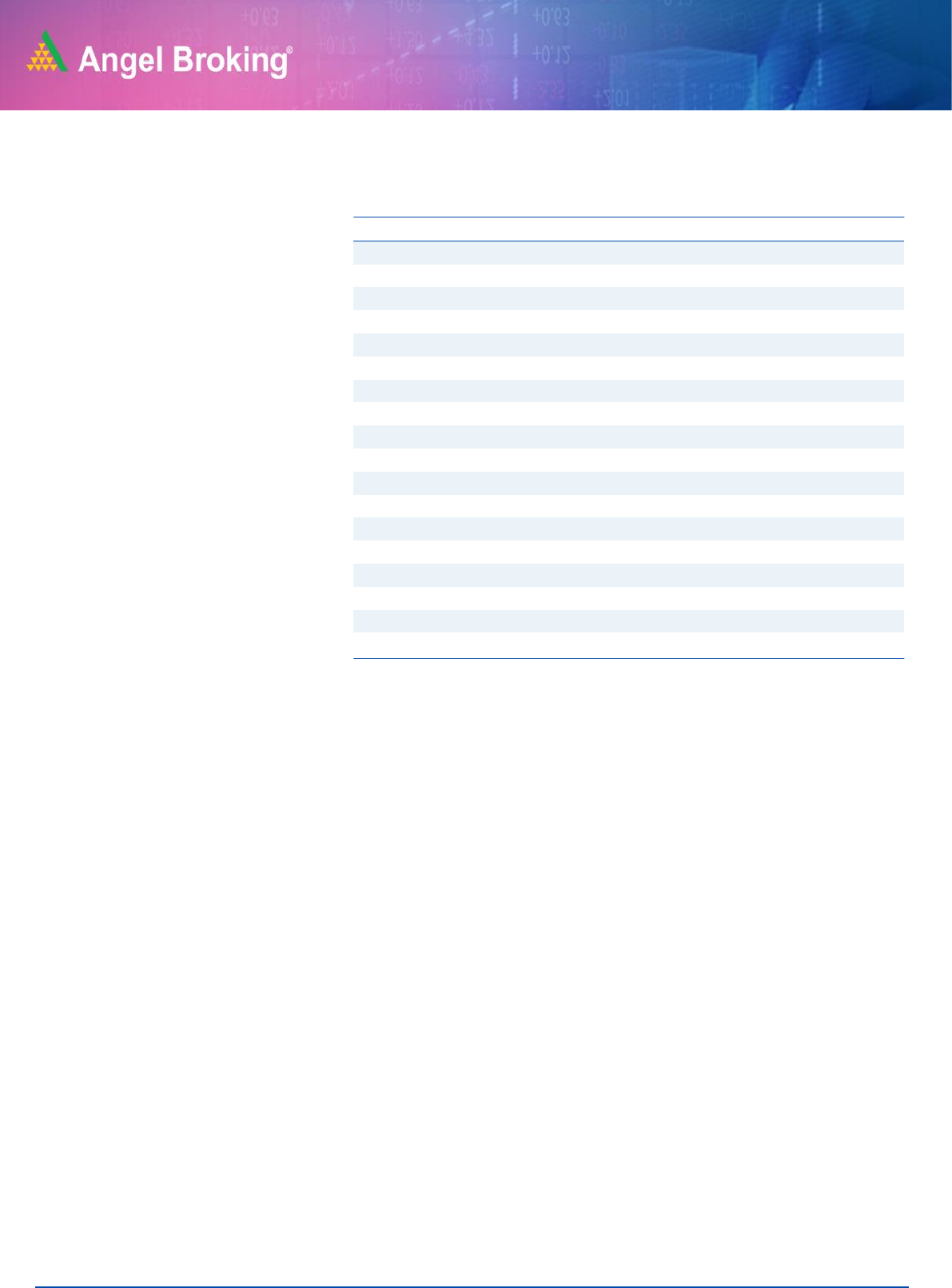

IDFC First Bank

The Ability to raise sufficient liquidity at Low cost would be The Key criteria for

banks to navigate the current situation, as asset side inflow would be limited.

IDFC Fist Bank, Post management change has clearly outperformed in building

liability franchise and retail lending.

Since new management took charge, every qtr. liability franchise has been

strengthened. CASA ratio improved from 10.4% in Q3FY19 to ~43% In

Q3FY21. NIM’s have also been stable for the bank despite interest reversals in

Q3FY21. Moreover, the bank is back on the growth path driven by strong

growth in Retail AUM.

The Bank had raised Rs. 2,000 crores of fresh equity capital during Q1FY21.

Post the capital raise, the company has been aggressively looking to expand

its retail book.

Federal bank is one of India’s largest old generation private sector banks. At

the end of FY2021 the bank had total assets of Rs. 1.9 lakh cr. with deposits of

Rs. 1.56 lakh cr. and a loan book of Rs. 1.2 lakh cr.

NPA's have remained steady for the bank over the past few years with GNPA

for Q3FY21 at 3.38% while NNPA ratio stood at 1.14%. PCR at the end of

Q3FY21 stood at ~67% which we believe is adequate. Restructuring book is

expected to be at Rs. 1,500-1,600 crore out of which Rs. 1,067 crore has

already been restructured. This is against earlier expectations of total

restructuring of Rs. 3,000-3,500 crore.

The company has posted a decent set of numbers for Q3FY21 as the loan book

grew by 6.0% YoY led by strong growth in retail portfolio. NIM's for the quarter

was up by 9bps QoQ to 3.22% while NII grew by a strong 24.4% YoY to Rs.

1,437 crore.

Key Financials

Y/E

NII

NIM

PAT

EPS

ABV

ROA

ROE

P/E

P/ABV

March

(` cr)

(%)

(` cr)

(`)

(`)

(%)

(%)

(x)

(x)

FY2021E

6,908

4.6

554

1.0

30

0.3

3.3

68

2.3

FY2022E

8,179

4.7

1,149

2.0

32

0.6

6.2

33

2.1

Source: Company, Angel Research

Stock Info

CMP

87.3

TP

110

Upside

26%

Sector

Banking

Market Cap (` cr)

17426

Beta

1.36

52 Week High / Low

90/37

3 year-Chart

Source: Company, Angel Research

Key Financials

Y/E

NII

NIM

PAT

EPS

ABV

ROA

ROE

P/E

P/ABV

March

(` cr)

(%)

(` cr)

(`)

(`)

(%)

(%)

(x)

(x)

FY2021E

5,911

3.1

1,428

7.2

73

0.8

9.4

12

1.2

FY2022E

7,064

3.4

1,940

9.7

83

0.9

11.5

9

1.1

Source: Company, Angel Research

-

20

40

60

80

100

120

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

Stock Info

CMP

66.8

TP

77.0

Upside

15.3%

Sector

Banking

Market Cap (` cr)

37899

Beta

1.16

52 Week High / Low

68/18

3 year-Chart

Source: Company, Angel Research

-

10

20

30

40

50

60

70

80

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

Angel Top Picks | March 2021

March 8, 2021

5

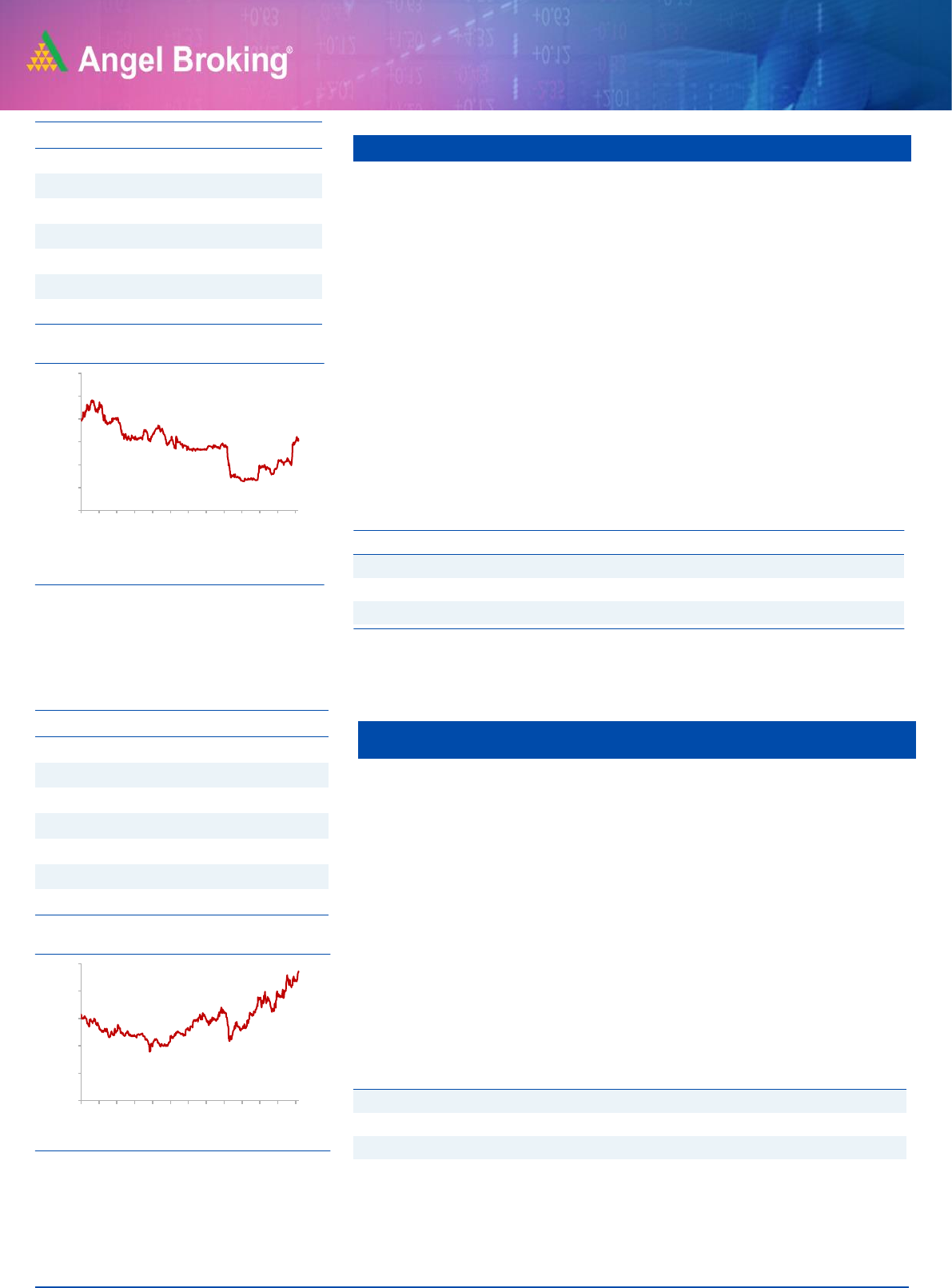

Shriram City Union

Galaxy Surfactants

Shriram City Union Finance is part of the Shriram group and is in the high

margin business of lending to small businesses which account for 57.3% of the

loan book as of end FY20. The company also provides auto, 2-wheeler, gold,

and personal loans. The company posted a good set of number s for the quarter

due to positive surprise on the asset quality front. NII for Q3FY21 was down by

1.3% YoY to Rs. 876.5 crore while PPOP was down by 2.2 YoY to Rs. 560

crores. provision during the quarter was down by 13% qoq to Rs. 175.5 crore

while profits were down by 5.7% yoy to Rs. 280 crores.

SCUF reported a strong 50% sequential growth in disbursement for the quarter

which led to a 3.7% qoq growth in AUM to ~ Rs. 28,500 crore. SCUF surprised

positively on the asset quality front Gross stage 3 loans decreased by 20bps

qoq to 6.5% in Q3FY21. Net stage 3 for the quarter was stable at 3.3% while

PCR ratio stood at 52.7%.

Galaxy Surfact.

Galaxy Surfactants is a market leader in oleochemical-based surfactants,

which is used in personal and home care products including skin care, oral

care, hair care, cosmetics, toiletries and detergent products.

The company has been increasing it’s share of high margin specialty care

products in it’s portfolio which now accounts for ~ 40% of it’s revenues while

the balance is accounted for by the performance surfactant business.

Company has very strong relationship with MNC clients like Unilever, P&G,

Henkel, Colgate-Palmolive and supplies raw materials to them not only in India

but also in US, EU and MENA region.

Y/E

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

FY2021E

2,737

16.3

295

83.1

21.9

28.4

6.5

3.1

FY2022E

3,204

16.2

344

97.2

22

24.3

5.3

2.6

Stock Info

CMP

1519

TP

1800

Upside

18.5%

Sector

Banking

Market Cap (` cr)

10023

Beta

0.51

52 Week High / Low

1610/632

3 year-Chart

Source: Company, Angel Research

Stock Info

CMP

2360

TP

2750

Upside

16.5%

Sector

Chemicals

Market Cap (` cr)

8368

Beta

0.57

52 Week High / Low

2360/1085

3 year-Chart

Source: Company, Angel Research

Key Financials

Y/E

NII

NIM

PAT

EPS

ABV

ROA

ROE

P/E

P/ABV

March

(` cr)

(%)

(` cr)

(`)

(`)

(%)

(%)

(x)

(x)

FY2021E

3,365

12

988

149.6

1,095

3.1

12.5

10

1.4

FY2022E

3,786

12.4

1,264

191.5

1,240

3.8

14

8

1.2

Source: Company, Angel Research

-

500

1,000

1,500

2,000

2,500

3,000

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

-

500

1,000

1,500

2,000

2,500

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

Angel Top Picks | March 2021

March 8, 2021

6

NRB Bearing

Escort

NRB is one of the leading supplier of bearings to Auto companies. The

company supplies bearings to two wheelers, PV, CV, Three wheelers and

tractors OEMs and has a wide customer base. The company has also been

focusing on exports markets in order to diversify its revenue base.

The company has posted a good set of numbers for Q2FY21 as revenues grew

by 4.6% YoY while PAT was up by 56% YoY. This was led by strong company.

With the Auto industry back on growth track and exports also doing well for the

company we expect the company to do well going forward. The management

has highlighted that exports growth should be in excess of 20% for FY21 driven

by demand from existing customers as well as new customers.

Y/E

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

FY2021E

697

12.2

33

3.4

6.8

34.3

2.4

1.9

FY2022E

898

15.5

72

7.4

13.2

15.8

2.1

1.5

Escorts is a prominent tractor player domestically with market share in excess

of 11%. The company’s brand of tractors is particularly strong in the northern

as well as the eastern belt of India.

With rural India relatively less impacted due to Covid-19, record food-grain

procurement by government agencies as well as better than expected Kharif

crop in 2020, we expect the tractor industry will continue to outperform the

larger automobile space in FY21 with Escorts a key beneficiary

Escorts in the recent past has also entered into a strategic partnership with

Kubota Corporation of Japan (one of the global leaders in farm machinery and

implements), which provides further visibility of growth for the company, going

forward. The company has been reporting strong growth in monthly sales

numbers so far in FY21 with sales growth of 12.5% YoY to 74,153 units in

9MFY21.

Stock Info

CMP

116.8

TP

135.0

Upside

15.6

Sector

Auto

Market Cap (` cr)

1132

Beta

0.65

52 Week High / Low

121/51

3 year-Chart

Source: Company, Angel Research

Stock Info

CMP

1318

TP

1573

Upside

19.3%

Sector

Auto

Market Cap (` cr)

17775

Beta

1.18

52 Week High / Low

1442/551

3 year-Chart

Source: Company, Angel Research

Key Financials

Y/E

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

FY2021E

6,562

16.1

801

59.4

15.7

23.3

3.5

2.9

FY2022E

7,415

15.6

873

64.6

14.9

21.4

3.0

2.5

Source: Company, Angel Research

-

50

100

150

200

250

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

-

100

200

300

400

500

600

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

Angel Top Picks | March 2021

March 8, 2021

7

GNA Axles

PVR

GNA Axles is one of the leading suppliers of rear axles to the Auto industry.

The company is a major supplier of rear axles to the CV industry and is

expected to be one of the biggest beneficiaries of the revival in the CV

cycle. The company derives 60% of its revenues from exports while the

balance 40% of the company’s revenues comes from the domestic markets.

GNA is expected to be one of the biggest beneficiaries of strong growth outlook

for truck sales in US and Europe markets which are witnessing strong recovery

in demand. US which accounts for almost 40% of the company's revenues has

been registering strong class 8 truck sales.

The venture into the SUV axle would provide the company with new growth

avenues while the recovery in the domestic CV cycle also bodes well for the

company. At current level the stock is trading at a P/E multiple of 9xFY23E EPS

estimate of Rs. 42 and offers value.

PVR is the largest multiplex chain in India with 800+ screens across

India. Multiplex screens are gaining ground in India at the expense of single

screens. Share prices have corrected significantly as most of the theaters are

operating at very low capacity utilization due to the lack of any major releases

due to the Covid-19 crisis.

However, with a significant decrease in Covid-19 cases over the past few

months we believe that it’s a matter of time before we see new releases by

production houses post April 2021 which should lead to significant increase in

business for the companies.

Stock Info

CMP

394.6

TP

500.0

Upside

26.7%

Sector

Auto

Market Cap (` cr)

847

Beta

0.55

52 Week High / Low

416/133

3 year-Chart

Source: Company, Angel Research

Stock Info

CMP

1452.6

TP

1800.0

Upside

23.9%

Sector

Other

Market Cap (` cr)

8930

Beta

0.78

52 Week High / Low

1683/732

3 year-Chart

Source: Company, Angel Research

Key Financials

Y/E

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(X)

(X)

(X)

FY2021E

841

15.2

51

23.8

10.4

16.6

1.7

1.1

FY2022E

1009

15.8

73

33.9

13.1

11.6

1.5

0.9

Source: Company, Angel Research

Key Financials

Y/E

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(X)

(X)

(X)

FY2021E

2,057

2.8

-209

-40.8

-11.9

-35.6

4.6

3.6

FY2022E

3,775

15.9

127

24.7

7.5

58.8

4.3

2.0

Source: Company, Angel Research

-

100

200

300

400

500

600

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

-

500

1,000

1,500

2,000

2,500

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

Please refer to important disclosures at the end of this report

8

Angel Top Picks – March 2021

Carborundum Universal

JK Lakshmi

Met

JK Lakshmi promoted by Singhania group is a predominantly north India

cement company with capacity of 13.3 Mn Mt.

Currently, north India is favorable location for the cement industry as it is

consolidated to a large extent as well as demand and supply outlook is better

compared to other locations. So far FY21 numbers of the company were better

compared to its peers due to favorable regional presence.

Power & fuel are important line items of cost for cement companies. Lower cost

inventory of petcock will help the company to report better margins for the

upcoming quarter on YoY basis.

Carborundum Universal (CUMI) is part of the Murugappa group and is

a leading manufacturer of abrasives, industrial ceramics, refractories, and

electro minerals in India having application across diversified user

industries. The company is expected to benefit from improving demand

scenarios across its end user industries such as auto, auto components,

engineering, basic metals, infrastructure, and power.

While demand from the Auto sector has been robust we expect demand from

metal industry pick up given increased economic activity. The company has

posted a robust set of numbers for Q3Fy21 with revenues increasing by

13.0% yoy to Rs. 730 crore driven by domestic growth.

Overseas operations were impacted due to the second wave of Covid-19.

EBIDTA for the quarter was up by 37.8% YoY to Rs. 123 crore while EBIDTA

margins also improved to 16.9%. Net profit for the quarter was up by

39.5% YoY to Rs. 87.7 crore.

Stock Info

CMP

428.2

TP

470.0

Upside

10%

Sector

Cement

Market Cap (` cr)

5039

Beta

0.67

52 Week High / Low

434/181

Key Financials

Y/E

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

FY2021E

4359

18.2

326

27.7

14.5

15.5

2.5

1.3

FY2022E

4729

17.2

357

30.3

17.5

14.2

2.2

1.1

Source: Company, Angel Research (Standalone nos.)

Stock Info

CMP

502.9

TP

600

Upside

19.3%

Sector

Other

Market Cap (` cr)

9530

Beta

0.64

52 Week High / Low

546/182

Key Financials

Y/E

Sales

OPM

PAT

EPS

ROE

P/E

P/BV

EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(X)

(X)

(X)

FY2021E

2638

15.5

280

14.8

13.6

34.0

4.6

3.5

FY2022E

3166

16.0

348

18.4

15.0

27.4

4.1

2.9

Source: Company, Angel Research

3 year-Chart

Source: Company, Angel Research

-

50

100

150

200

250

Feb-18

May-18

Jul-18

Oct-18

Jan-19

Apr-19

Jul-19

Oct-19

Jan-20

Apr-20

Jul-20

Oct-20

Jan-21

3 year-Chart

Source: Company, Angel Research

-

100

200

300

400

500

600

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

May-19

Aug-19

Nov-19

Feb-20

May-20

Aug-20

Nov-20

Feb-21

Angel Top Picks | March 2021

March 8, 2021

9

Changes in Recommendation

Stocks bought in last 6 months

Stock Name

Buy Call Date

Buy Price

Hindustan Aeronautics

9/3/2020

926

Atul

10/28/2020

6,072

Galaxy Surfactants

11/4/2020

1,664

Gujarat Gas

11/24/2020

329.70

Bandhan Bank

11/25/2020

365.5

Whirlpool India

12/16/2020

2,174

Narayana Hrudayalaya

12/17/2020

414.7

NRB Bearings

12/18/2020

95.7

Ashok Leyland

1/4/2021

100.4

Escorts

1/13/2021

1387.0

L&T Fin. Holdings

1/13/2021

105.0

MindTree

1/20/2021

1756.0

Federal Bank

1/21/2021

77.6

PNC Infratech

2/4/2021

230.6

Shri.City Union

08-02-2021

1468

HCL Technologies

11-02-2021

965

GNA Axles

17-02-2021

406

PVR

04-03-2021

1494

Source: Company, Angel Research

Angel Top Picks | March 2021

March 8, 2021

10

Stocks sold in last 6 months

Stock Name

Sell Date

Exit Price

Alembic Pharma

9/2/2020

921

Britannia Industries

9/14/2020

3,786

Chalet Hotels

9/28/2020

142

Zensar Technologies

10/30/2020

179

Reliance Industries

11/2/2020

1,912

Hindustan Aeronautics

11/3/2020

681

V I P Inds.

11/17/2020

311

Endurance Tech.

11/19/2020

1,036

Inox Leisure

12/17/2020

285.2

Cholamandalam Inv & Fin Comp

12/24/2020

376.3

Bandhan Bank

1/13/2021

387

Swaraj Engines

1/13/2021

1415

Gujarat Gas

1/15/2021

371

Persistent Sys

1/15/2021

1620

L&T Fin. Holdings

1/20/2021

104.5

Atul

2/1/2021

6470

Hawkins Cookers

2/4/2021

5,710

Whirlpool India

2/4/2021

2,465

Ashok Leyland

11-02-2021

134

Metropolis Healt

11-02-2021

2120

Narayana Hrudaya

03-03-2021

430

Angel Top Picks | March 2021

March 8, 2021

11

Research Team Tel: 022 - 39357800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited, Bombay

Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National Commodity &

Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and Investment Adviser

with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered entity with SEBI for

Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164. Angel or its

associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market.

Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of securities of the

company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits

and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate

the contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is

for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any

loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking

Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any

representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking

Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or

other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Disclosure of Interest Statement

Top Picks

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or

relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on Expected Returns: Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Over 12 months investment period) Reduce (-5% to -15%) Sell (< -15%)

Hold (Fresh purchase not recommended)