3QFY2017 Result Update | IT

February 1, 2017

Tech Mahindra

BUY

CMP

`452

Performance Highlights

Target Price

`600

(` cr)

3QFY17

2QFY17

% chg (QoQ)

3QFY16

% chg (YoY)

Investment Period

12 Months

Net revenue

7,558

7,167

5.4

6,701

12.8

EBITDA

1,187

1,070

10.9

1,135

4.5

Stock Info

EBITDA margin (%)

15.7

14.9

77bp

16.9

(124)bps

Sector

IT

Adj. PAT

845

645

31.0

759

11.2

Market Cap (` cr)

43,962

Source: Company, Angel Research;

Net Debt (` cr)

(6,370)

Beta

1.1

For 3QFY2017, Tech Mahindra posted results much better than expected on all

52 Week High / Low

564/405

fronts. The company posted sales of US$1,116mn (US$1,091mn expected) v/s

Avg. Daily Volume

218,321

US$1,072mn, a qoq growth of 4.1%. In Constant Currency (CC) terms, company

Face Value (`)

5

posted a 5.4% qoq growth. On EBIT front, the company posted EBIT of 12.4%

BSE Sensex

27,656

(12.1% expected) v/s 11.5% in 2QFY2016. The utilization levels improved to

83.0% v/s 82.0% in 2QFY2016. Consequently, PAT came in at `845cr (`733cr

Nifty

8,561

expected) v/s `645cr in 2QFY2016, growth of 31.0% qoq. The growth in the net

Reuters Code

TEML.BO

profit was aided by the lower taxes during the quarter, which dipped 25.1% yoy.

Bloomberg Code

TECHM@IN

We maintain our Buy rating on the stock.

Result highlights: The company posted sales of US$1,116mn (US$1,091mn

Shareholding Pattern (%)

expected) v/s US$1,072mn, a qoq growth of 4.1%. In Constant Currency (CC)

Promoters

36.2

terms, company posted a 5.4% qoq growth. The strong sales growth was aided by

MF / Banks / Indian Fls

17.2

ROW (which contributed around 23.9% v/s 22.0% of sales in 2QFY2017), while

FII / NRIs / OCBs

35.5

USA (which contributed 46.7% v/s 48.3% of sales in 2QFY2017) and Europe

Indian Public / Others

11.1

(which contributed 29.4% v/s 29.7% of sales in 2QFY2017). On EBIT front, the

company posted EBIT of 12.4% (12.1% expected) v/s 11.5% in 2QFY2016. The

utilization levels improved to 83.0% v/s 82.0% in 2QFY2016. Consequently, PAT

Abs.(%)

3m 1yr

3yr

came in at `845cr (`733cr expected) v/s `645cr in 2QFY2016, growth of 31.0% qoq.

Sensex

(1.0)

11.2

34.8

Tech Mahindra

2.8

(9.9)

0.9

Outlook and valuation: We expect a CAGR of 10.6% and 11.5% in USD and

INR revenue respectively over FY2016-18E. The PAT is expected to grow at a

CAGR of 11.4% over FY2016-18E. We maintain our Buy rating on the stock

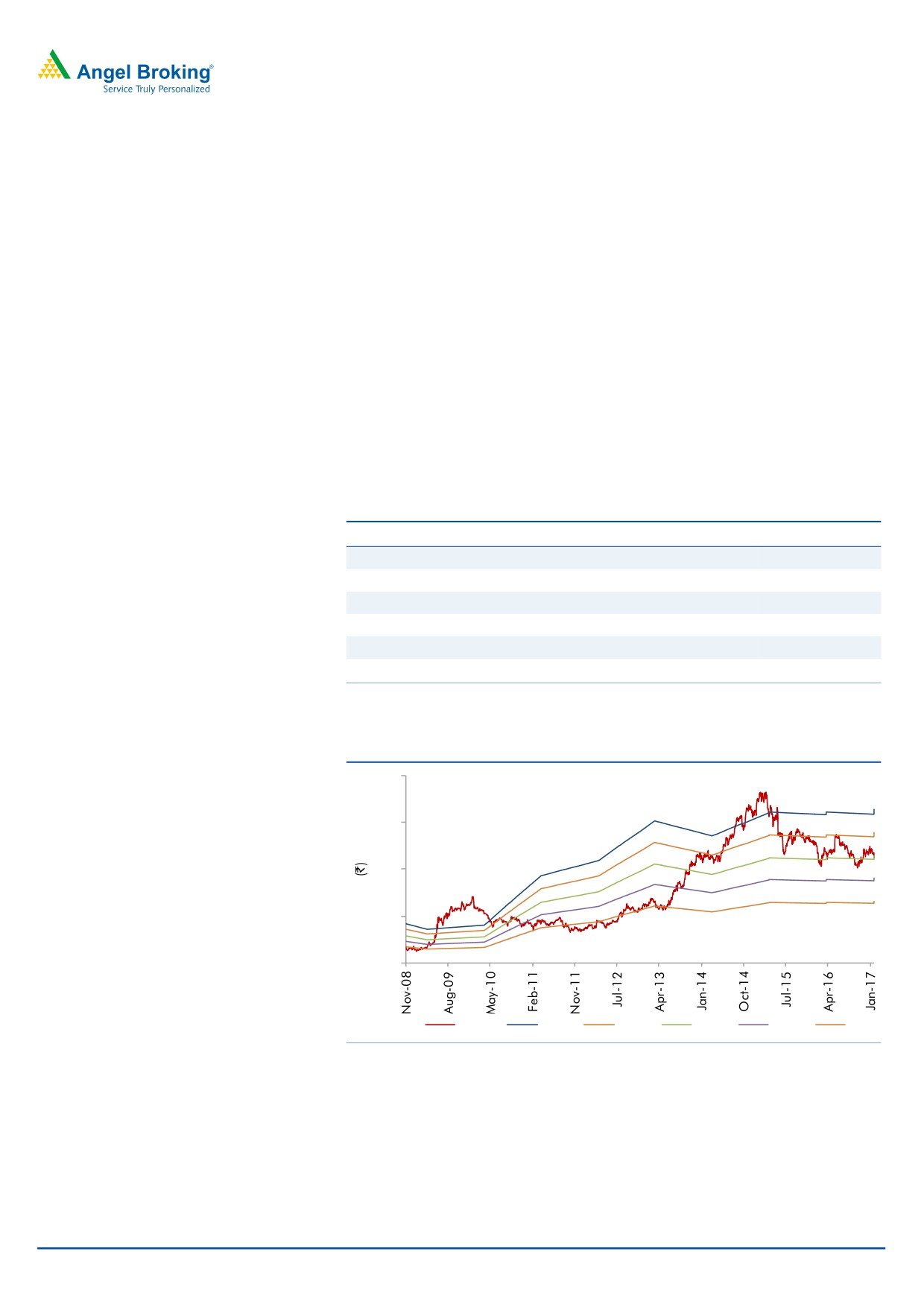

3-year price chart

with a Target Price of `600.

800

700

Key financials (Consolidated, Indian GAAP)

600

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

500

Net sales

22,621

26,494

29,673

32,937

400

300

% chg

20.1

17.1

12.0

11.0

200

Net profit

2,628

3,118

3,173

3,866

100

% chg

(10.4)

18.7

1.8

21.9

0

EBITDA margin (%)

18.4

16.3

15.5

17.0

EPS (`)

27.1

32.2

32.8

39.9

P/E (x)

16.6

14.0

13.8

11.3

Source: Company, Angel Research

P/BV (x)

3.6

3.0

2.7

2.3

RoE (%)

21.5

21.7

19.6

20.6

RoCE (%)

24.0

20.8

19.8

21.6

Sarabjit kour Nangra

EV/Sales (x)

1.9

1.5

1.3

1.1

+91 22 3935 7800 Ext: 6806

EV/EBITDA (x)

10.2

9.2

8.3

6.5

Source: Company, Angel Research; Note: CMP as of January 31, 2017

Please refer to important disclosures at the end of this report

1

Tech Mahindra | 3QFY2017 Result Update

Exhibit 1: 3QFY2017 performance (Consolidated, Indian GAAP)

(` cr)

3QFY17

2QFY17

% chg (qoq)

3QFY16

% chg (yoy)

9MFY17

9MFY16

% chg (yoy)

Net revenue

7,558

7,167

5.4

6,701

12.8

21,646

19,611

10.4

Cost of revenue

5,235

4,972

5.3

4,607

13.6

14,103

13,058

8.0

Gross profit

2,322

2,196

5.8

2,094

10.9

7,543

6,553

15.1

SG&A expense

1,136

1,126

0.9

959

18.4

4,258

3,433

24.0

EBITDA

1,187

1,070

10.9

1,135

4.5

3,286

3,120

5.3

Dep. and amortization

248

245

1.3

174

42.5

695

542

28.2

EBIT

939

825

13.7

962

(2.4)

2,591

2,579

0.5

Interest

35

35

1.2

24

99.3

97

63

53.7

Other income

155

139

11.9

64

59.0

540

284

90.0

PBT

1,059

930

13.9

1,002

5.7

3,034

2,800

8.4

Income taxes

214

286

(25.1)

233

12.4

747

638

17.1

PAT

845

644

31.2

769

9.8

2,287

2,162

5.8

Minority interest

0

(0)

-

10

(98.5)

-

1

PAT after minority interest

845

644

31.2

759

11.2

2,285

2,162

5.7

Profit from associates

-

-

-

-

-

Exceptional item

-

-

-

-

-

Reported PAT

845

644

31.2

759

11.2

2,285

2,162

5.7

Adj. PAT

845

645

31.0

759

11.2

2,285

2,162

5.7

Diluted EPS

8.8

6.7

31.0

7.9

11.2

23.8

22.5

5.7

Gross margin (%)

30.7

30.6

9bp

31.2

(52)bps

34.8

33.4

143bp

EBITDA margin (%)

15.7

14.9

77bp

16.9

(124)bps

15.2

15.9

(73)bp

EBIT margin (%)

12.4

11.5

90bp

14.4

(194bps

12.0

13.1

(118)bp

PAT margin (%)

11.3

9.0

233bps

11.3

0bps

10.6

11.0

(47)bp

Source: Company, Angel Research

Exhibit 2: 3QFY2017 - Actual Vs Angel estimates

(` cr)

Actual

Estimate

% Var

Net revenue

7,558

7,361

2.7

EBITDA margin (%)

15.7

15.6

10bps

PAT

845

733

15.2

Source: Company, Angel Research

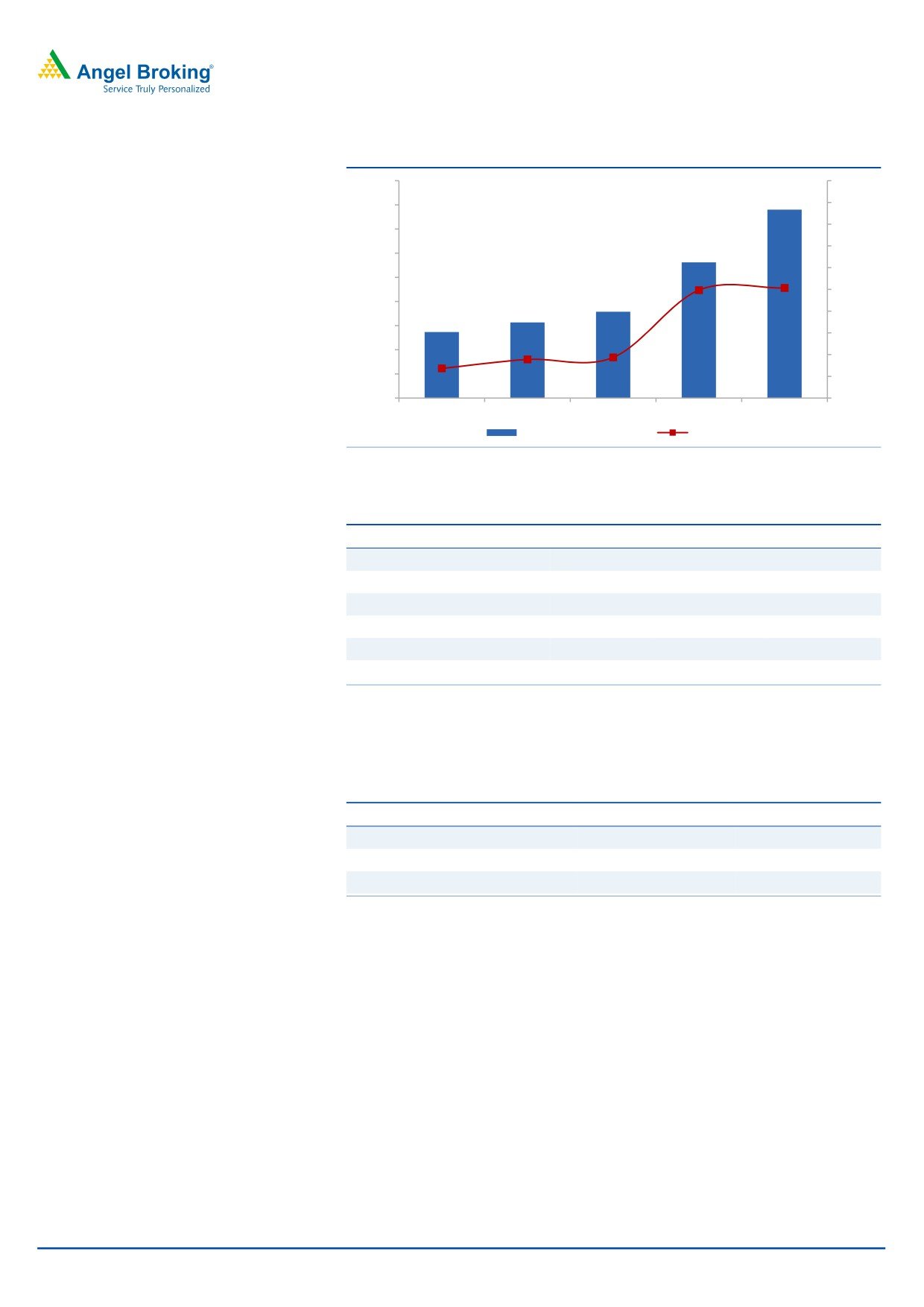

Revenue growth led by ROW

In sales, the company posted sales of US$1,116mn (US$1,091mn expected) v/s

US$1,072mn, a qoq growth of 4.1%. In Constant Currency (CC) terms, company

posted a 5.4% qoq growth. In Rupee terms, the company posted sales of `7,558cr

(`7,361cr expected) v/s `7,167cr in 2QFY2017, a qoq growth of 5.4%.

The strong sales growth was aided by the ROW (which contributed around 23.9%

v/s 22.0% of sales in 2QFY2017), while USA (which contributed 46.7% v/s 48.3%

of sales in 2QFY2017) and Europe (which contributed 29.4% v/s 29.7% of sales in

2QFY2017).

Vertical wise, BFSI (contributed around 13.1% v/s 11.7% in 2QFY2017), Retail,

transport & Logistics (contributed around 7.6% of sales V/s 6.8% of sales in

2QFY2017) performed well.

February 1, 2017

2

Tech Mahindra | 3QFY2017 Result Update

Exhibit 3: Trend in revenue growth

1,140

9.0%

1,116

1,120

8.0%

7.0%

1,100

1,072

6.0%

1,080

5.0%

1,060

4.1%

4.0%

4.0%

1,040

1,032

1,023

3.0%

1,015

1,020

2.0%

1,000

0.8%

1.0%

0.9%

980

0.4%

0.0%

960

-1.0%

3QFY16

4QFY16

1QFY17

2QFY17

3QFY17

Sales ( in US $mn)

qoq (%)

Source: Company, Angel Research

Exhibit 4: Growth in industry segments

Particulars

% to revenue

% growth (QoQ)

% growth (YoY)

Telecom

47.3

0.4

0.1

Manufacturing

18.4

(0.3)

18.3

TME

6.4

(7.5)

(4.9)

BFSI

13.1

18.6

47.0

RTL

7.6

16.3

22.9

Others

7.1

8.7

2.7

Source: Company, Angel Research

In terms of geographies, ROW posted a growth of 13.1% qoq, while Europe and

US posted a growth of 3.0% and 0.6% qoq respectively.

Exhibit 5: Growth trend in geographies

Particulars

% to revenue

% growth (QoQ)

% growth (YoY)

Americas

46.7

0.6

7.5

Europe

29.4

3.0

11.9

RoW

23.9

13.1

14.3

Source: Company, Angel Research

February 1, 2017

3

Tech Mahindra | 3QFY2017 Result Update

Hiring and client metrics

During the quarter, the company reported a net addition of 4,209 employees,

taking its overall headcount to 117,095. The BPO headcount currently stands at

29,372 and was the only division to witness additions. Attrition (on LTM basis) was

at 18%.

Exhibit 6: Employee metrics

Particulars

3QFY16

4QFY16

1QFY17

2QFY17

3QFY17

Software professionals

71,892

72,125

73,590

78,404

80,858

BPO professionals

28,279

27,254

27,326

27,669

29,372

Sales & support

6,966

6,053

6,300

6,813

6,865

Total employees

1,07,137

105,432

107,216

112,886

117,095

Attritions (%)

20

21

21

19

18

Source: Company, Angel Research

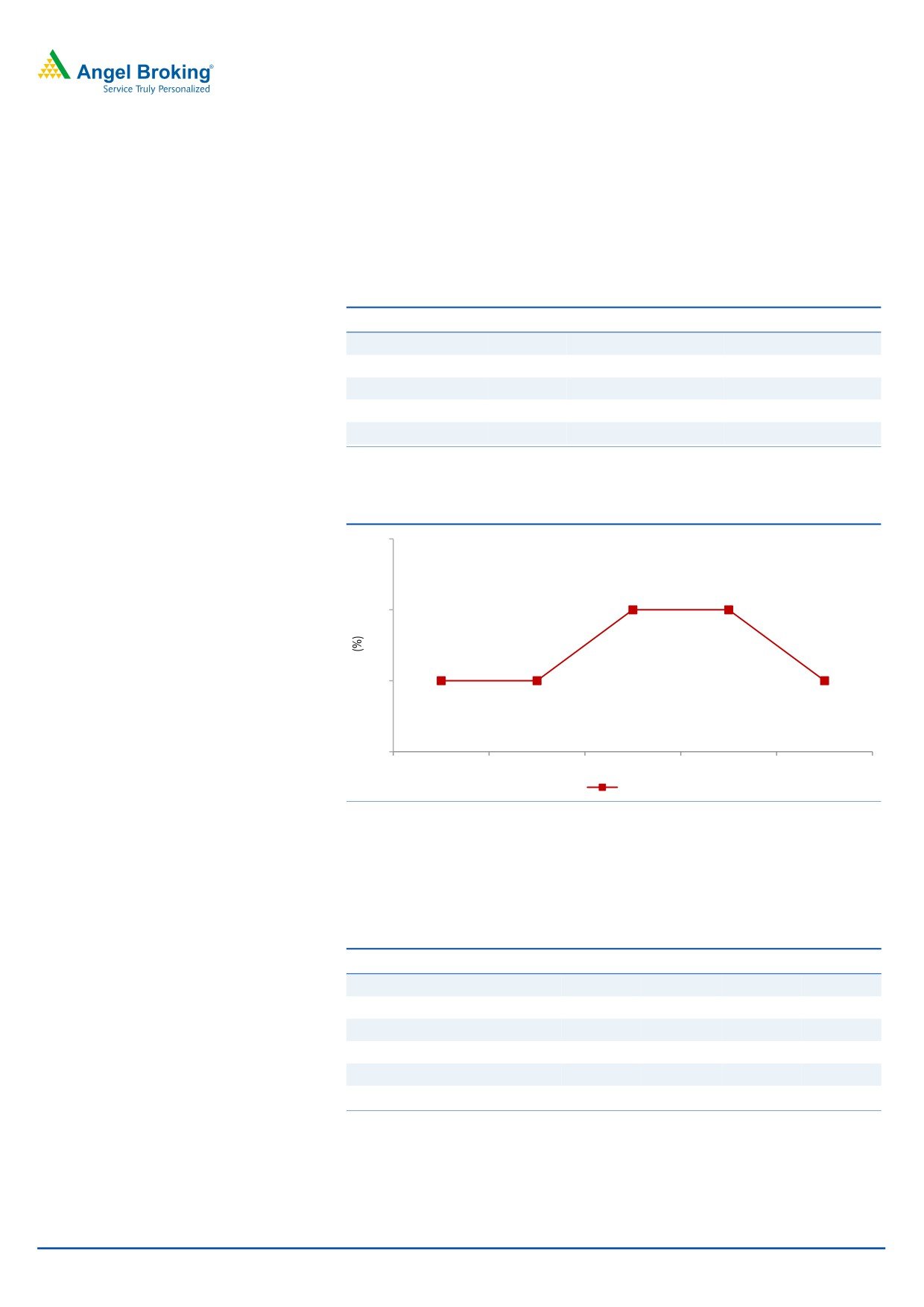

Exhibit 7: Trend in utilization rate

79

78

78

78

77

77

77

77

76

3QFY16

4QFY16

1QFY17

2QFY17

3QFY17

Utilization (%)

Source: Company, Angel Research

The company added 19 new clients during the quarter, taking the active client

base to 837 (v/s 818 in 2QFY2017), with 5 clients added in US$10mn-20mn+

bracket and other additions mainly in the US$5mn-10mn+ bracket.

Exhibit 8: Client metrics

Particulars

3QFY16

4QFY16

1QFY17

2QFY17

3QFY17

Total active clients

767

801

807

818

837

US$1mn-5mn

195

221

207

197

228

US$5mn-10mn

40

42

49

56

63

US$10mn-20mn

21

26

23

22

27

US$20mn-50mn

22

23

26

28

24

US$50mn+

13

14

14

14

14

Source: Company, Angel Research

February 1, 2017

4

Tech Mahindra | 3QFY2017 Result Update

Operating margin expands

On EBIT front, the company posted EBIT of 12.4% (12.1% expected) v/s 11.5% in

2QFY2016. In 2QFY2017, the company took a one-time hit of ~USD13m

(-100bps) i.e. expenses associated with restructuring. The absence of these costs in

3QFY2017 proved to be a tailwind for EBIT margin improvement. The utilization

levels improved to 83.0% v/s 82.0% in 2QFY2016.

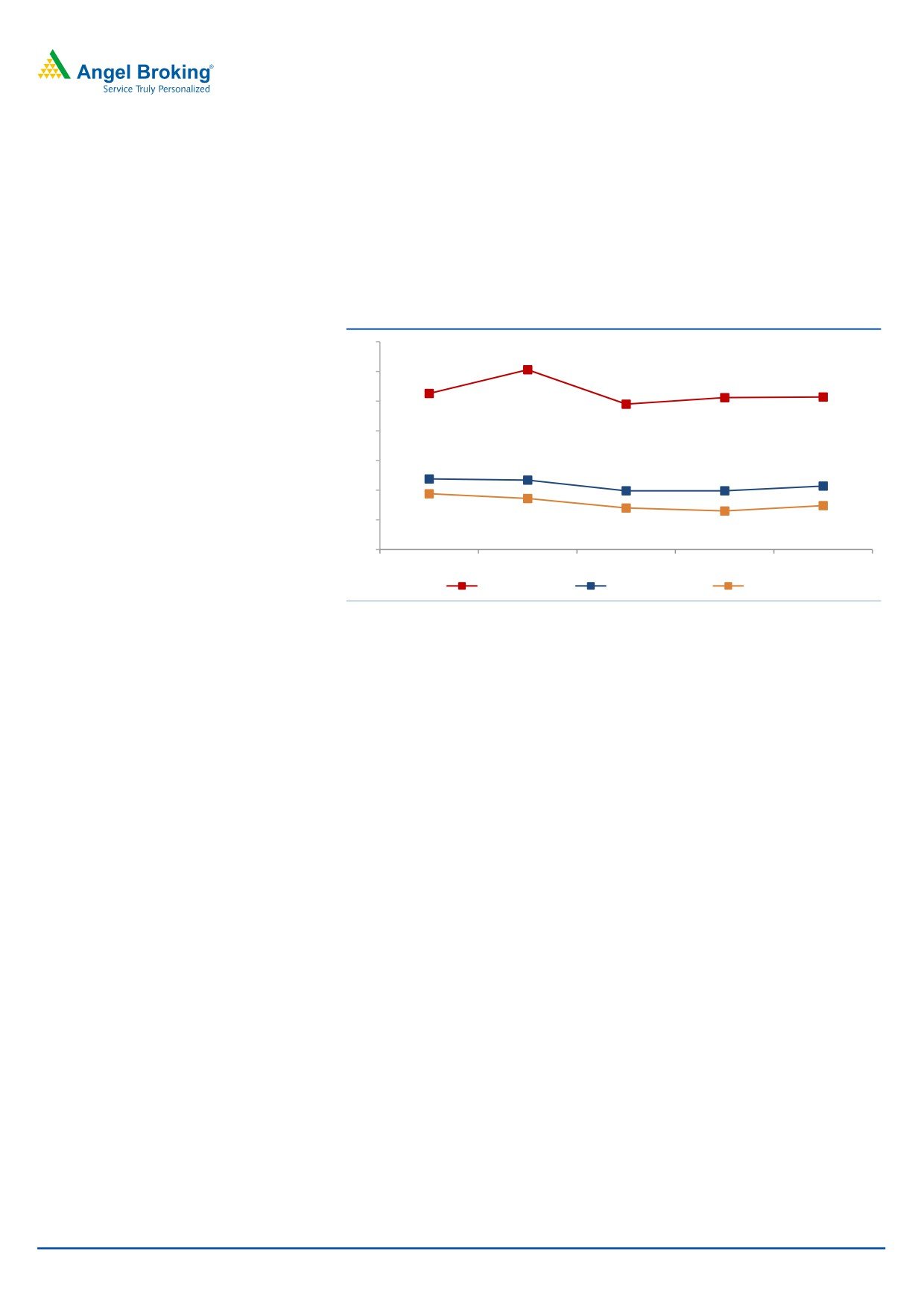

Exhibit 9: Margin trend (%)

40

35

35.3

30

31.3

30.6

30.7

29.5

25

20

16.9

16.7

15.7

14.9

14.9

15

14.4

10

13.6

12.0

11.5

12.4

5

3QFY16

4QFY16

1QFY17

2QFY17

3QFY17

Gross margin

EBITDA margin

EBIT margin

Source: Company, Angel Research

Investment arguments

Growth prospects decent: The Management is more optimistic about the

Communications vertical (excluding LCC, where a lot of portfolio rationalization

has taken place). Communication has been showing continued improvement in

both revenue growth and deal wins. We expect a CAGR of 10.6% and 11.5% in

USD and INR revenue respectively over FY2016-18E.

Deal pipeline healthy: Tech Mahindra remains confident of improving revenue

growth, citing healthy deal pipeline along with pick up in discretionary spending,

primarily in the US. The Management sounded confident of demand from BFSI,

Healthcare, Manufacturing and Retail. Tech Mahindra is following a two-pronged

strategy to expand its enterprise business i.e. providing end-to-end offerings in

leadership areas like manufacturing and following a niche offerings-led entry

strategy in areas like BFSI, where it is a challenger. Better cross-sell of services can

help grow marquee accounts post the recent acquisitions. We expect the enterprise

segment growth to be led by broader revival in the markets and deepening of

existing relationships. During 3QFY2017 the company won deals worth TCV of

US$350mn. The pipeline has been healthy and supported by a couple of large

deal wins in Telecom and BFSI.

Inorganic growth initiatives to augment well for company: The company has been

active in the M&A space, with it having acquired Satyam a few years back, to

acquiring LCC and Softgen recently. Softgen’s and LCC’s acquisition was

consolidated in 4QFY2015. LCC is one of the world’s largest independent global

providers of network engineering services to the telecommunications industry with

an estimated annual revenues of more than US$400mn (CY2014), with workforce

of over

5,700 network professionals across five continents and more than

February 1, 2017

5

Tech Mahindra | 3QFY2017 Result Update

50 countries. With this acquisition, Tech Mahindra will also be addressing a rapidly

growing market opportunity, as telecommunications companies and enterprises

accelerate their network upgrade cycle.

Outlook and valuation

Given the recent acquisitions and healthy order pipeline, the company is expected

to post a healthy US$ and INR CAGR of 10.6% and 11.5% respectively over

FY2016-18E. However, the acquisition of LCC will be margin dilutive in the near

term, leading the FY2016 EBDITA margin to drop to 16.3% from 22.2% in

FY2014. The company, given its success in turnaround of its earlier acquisition

(Satyam), believes it would be able to do the same with the recent acquisitions and

would be able to get close to achieving the 20% EBIT levels in future. Given the

favorable valuation on EV/sales front, where it trades at a significant discount to its

peers, we believe the stock should witness uptrend once the profitability returns to

its mean average. We maintain a Buy rating on the stock.

Exhibit 10: Key assumptions

FY2017E

FY2018E

Revenue growth (US$)

10.3

11.0

USD-INR rate (realized)

66.0

66.0

Revenue growth (`)

12.0

11.0

EBITDA margin (%)

15.5

17.0

Tax rate (%)

23.4

23.4

EPS growth (%)

1.8

21.9

Source: Company, Angel Research

Exhibit 11: One-year forward PE (x)

800

600

400

200

0

Price

20x

17x

14x

11x

8x

Source: Company, Angel Research. Note: P/E includes profits of Mahindra Satyam from FY2012

February 1, 2017

6

Tech Mahindra | 3QFY2017 Result Update

Exhibit 12: Recommendation summary

Company

Reco

CMP Tgt Price Upside

FY2018E FY2018E

FY2016-18E

FY2018E FY2018E

(`)

(`)

(%)

EBITDA (%)

P/E (x)

EPS CAGR (%)

EV/Sales (x)

RoE (%)

HCL Tech

Buy

809

1,000

23.6

20.5

12.6

9.6

1.8

17.9

Infosys

Buy

929

1,249

34.4

27.0

13.4

8.4

2.2

21.6

TCS

Accumulate

2,230

2,620

17.5

27.6

15.3

8.5

3.1

33.1

Tech Mahindra

Buy

452

600

32.8

17.0

11.3

11.4

1.1

20.6

Wipro

Buy

457

583

27.5

18.1

11.5

4.0

1.6

17.6

Source: Company, Angel Research.

Company Background

Tech Mahindra was founded in 1986 as a joint venture between Mahindra Group

and British Telecom (BT) to service the latter. Later on, the company started

servicing other external clients as well (solely in the telecom industry). In June

2009, Tech Mahindra acquired a 42.7% stake in erstwhile Satyam Computers

(now Mahindra Satyam) and now the latter is entirely merged with the company.

The company has recently acquired the companies - LCC and Softgen. These two

acquisitions have been consolidated in 4QFY2015. LCC is one of the world’s

largest independent global providers of network engineering services to the

telecommunications industry. LCC is estimated to have annual revenues of more

than US$400mn (CY2014), with workforce of over 5,700 network professionals

across five continents and more than 50 countries.

February 1, 2017

7

Tech Mahindra | 3QFY2017 Result Update

Profit and loss statement (Consolidated, Indian GAAP)

Y/E March (` cr)

FY2014 FY2015 FY2016

FY2017E

FY2018E

Net sales

18,831

22,621

26,494

29,673

32,937

Cost of revenues

12,427

15,920

18,323

20,177

22,068

Gross profit

6,404

6,701

8,172

9,495

10,869

% of net sales

34.0

29.6

30.8

32.0

33.0

SG&A expenses

2,220

2,549

3,853

4,896

5,270

% of net sales

11.8

11.3

14.5

16.5

16.0

EBITDA

4,184

4,153

4,318

4,599

5,599

% of net sales

22.2

18.4

16.3

15.5

17.0

Depreciation and amortization

522

611

762

861

955

% of net sales

2.8

2.7

2.9

2.9

2.9

EBIT

3,662

3,541

3,556

3,739

4,644

% of net sales

19.4

15.7

13.4

12.6

14.1

Interest expense

80

30

96

96

96

Other inc., net of forex gain/(loss)

233

106

557

557

557

Profit before tax

3,815

3,618

4,017

4,199

5,105

Provision for tax

752

960

860

983

1,194

% of PBT

19.7

26.5

21.4

23.4

23.4

PAT

3,063

2,659

3,157

3,217

3,910

Exceptional item

-

-

-

-

-

Minority interest

34

31

44

44

44

Reported PAT

3,029

2,628

3,118

3,173

3,866

Adjusted PAT

2,933

2,628

3,118

3,173

3,866

Fully diluted EPS (`)

30.3

27.1

32.2

32.8

39.9

February 1, 2017

8

Tech Mahindra | 3QFY2017 Result Update

Balance sheet (Consolidated, Indian GAAP)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017E

FY2018E

Equity capital

234

480

484

484

484

Preference capital

-

-

-

-

-

Share premium

-

-

-

-

-

Profit and loss

8,947

11,768

13,882

15,696

18,204

Other reserves

2

0

0

0

-

Net worth

9,182

12,249

14,367

16,181

18,688

Secured loans

309

621

806

806

806

Unsecured loans

54

54

54

55

56

Total debt

363

675

859

860

861

Other long term liability

376

376

376

377

377

Long-term provisions

414

414

414

415

415

Minority interest

144

160

203

145

145

Amount pending investigation

1,230

895

895

895

895

Total capital employed

11,709

14,768

17,114

18,872

21,380

Gross block

5,460

7,811

8,811

9,811

10,811

Accumulated dep.

(2,866)

(3,477)

(4,239)

(5,099)

(6,055)

Net block

2,594

4,334

4,572

4,712

4,757

Capital WIP

266

266

266

267

268

Total fixed assets

2,861

4,601

4,839

4,979

5,025

Investments

36

2,103

2,103

2,103

2,103

Long term loans and adv.

914

1,306

1,502

1,727

1,986

Interest in TML benefit trust

-

-

-

-

-

Deferred tax asset, net

383

390

390

390

390

Other non-current assets

16

-

-

-

-

Inventories

10

24

11

11

11

Sundry debtors

4,349

5,206

5,987

6,896

7,980

Cash and cash equv.

4,756

2,405

5,127

6,486

8,612

Loans and advances

2,616

3,813

2,998

2,999

2,999

Current investments

-

-

-

-

-

Unbilled revenue

-

-

-

-

-

Sundry creditors

(1,549)

(1,654)

(1,903)

(2,188)

(2,516)

Other liabilities

(1,415)

(1,627)

(1,871)

(2,152)

(2,474)

Provision

(1,267)

(1,799)

(2,068)

(2,379)

(2,736)

Working capital

7,500

6,368

8,280

9,673

11,876

Total capital deployed

11,709

14,768

17,114

18,872

21,380

February 1, 2017

9

Tech Mahindra | 3QFY2017 Result Update

Cash flow statement (Consolidated, Indian GAAP)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017E

FY2018E

Pre tax profit from operations

3,063

2,659

3,157

3,217

3,910

Depreciation

522

611

762

861

955

Exp. (deffered)/written off/others

-

-

-

-

-

Pre tax cash from operations

3,585

3,270

3,919

4,077

4,865

Other income/prior period ad

233

106

557

557

557

Net cash from operations

3,818

3,376

4,475

4,634

5,422

Tax

(752)

(960)

(860)

(983)

(1,194)

Cash profits

3,066

2,417

3,615

3,651

4,227

(Inc)/dec in

Sundry Debtors

(980)

(857)

(781)

(909)

(1,085)

Inventories

1

(15)

13

-

-

Loans and advances

(1,324)

(1,197)

815

(1)

-

Sundry creditors

692

105

248

285

328

Others

(623)

212

244

281

323

Net trade working capital

(2,233)

(1,752)

540

(344)

(434)

Cashflow from operating activities

832

665

4,155

3,307

3,794

(Inc)/dec in fixed assets

(369)

(1,740)

(238)

(140)

(46)

(Inc)/dec in investments

-

(2,067)

-

-

-

(Inc)/dec in other non current assets

104

16

-

-

-

Cashflow from investing activities

(265)

(3,791)

(238)

(140)

(46)

Inc/(dec) in debt

490

(311)

(185)

(1)

(1)

Inc/(dec) in deferred revenue

-

-

-

-

-

Inc/(dec) in equity/premium

(2)

1

-

-

0

Inc/(dec) in minority interest

(9)

(16)

(43)

59

-

Dividends

(231)

(679)

(1,359)

(1,359)

(1,278)

Others

479

1,781

392

(507)

(343)

Cashflow from financing activities

726

775

(1,195)

(1,808)

(1,622)

Cash generated/(utilised)

1,294

(2,351)

2,722

1,359

2,126

Cash at start of the year

3,463

4,756

2,405

5,127

6,486

Cash at end of the year

4,756

2,405

5,127

6,486

8,612

February 1, 2017

10

Tech Mahindra | 3QFY2017 Result Update

Key Ratios

Y/E March

FY2014

FY2015

FY2016

FY2017E

FY2018E

Valuation ratio (x)

P/E (on FDEPS)

14.9

16.6

14.0

13.8

11.3

P/CEPS

12.3

13.5

11.3

10.8

9.1

P/BVPS

4.8

3.6

3.0

2.7

2.3

Dividend yield (%)

1.1

1.1

2.7

2.7

2.7

EV/Sales

2.1

1.9

1.5

1.3

1.1

EV/EBITDA

9.5

10.2

9.2

8.3

6.5

EV/Total assets

13.8

9.2

8.2

7.7

7.2

Per share data (`)

EPS

30.3

27.1

32.2

32.8

39.9

Cash EPS

36.7

33.5

40.1

41.7

49.8

Dividend

5.0

5.0

12.0

6.0

7.0

Book value

94.9

126.6

148.4

167.2

193.1

Dupont analysis

Tax retention ratio (PAT/PBT)

0.8

0.7

0.8

0.8

0.8

Cost of debt (PBT/EBIT)

1.0

1.0

1.1

1.1

1.1

EBIT margin (EBIT/Sales)

0.2

0.2

0.1

0.1

0.1

Asset turnover ratio (Sales/Assets)

6.6

4.9

5.5

6.0

6.6

Leverage ratio (Assets/Equity)

0.3

0.4

0.3

0.3

0.3

Operating ROE (%)

33.0

21.5

21.7

19.6

20.7

Return ratios (%)

RoCE (pre-tax)

31.3

24.0

20.8

19.8

21.7

Angel RoIC

54.8

29.3

30.3

30.8

37.2

RoE

31.9

21.5

21.7

19.6

20.7

Turnover ratios( x)

Asset turnover (fixed assets)

6.6

4.9

5.5

6.0

6.6

Receivables days

78

92

89

90

93

Payable days

26

29

28

28

29

February 1, 2017

11

Tech Mahindra | 3QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Tech Mahindra

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 1, 2017

12