4QFY2016 Result Update | Textile

May 23, 2016

Siyaram Silk Mills

BUY

CMP

`1,058

Performance Highlights

Target Price

`1,354

Y/E March (` cr)

4QFY16

4QFY15

% chg. (yoy)

3QFY16

% chg. (qoq)

Investment Period

12 Months

Net Sales

505

480

5.2

416

21.5

Stock Info

Operating profit

60

58

3.2

47

28.8

Sector

Textile

OPM (%)

11.9

12.2

(23bp)

11.3

68bp

Market Cap (` cr)

992

Adj. PAT

32

32

(0.3)

21

53.6

Net debt (` cr)

334

Source: Company, Angel Research

Beta

1.0

52 Week High / Low

1400 / 896

Siyaram Silk Mills (SSML)’ results for 4QFY2016 have come in below our

Avg. Daily Volume

2,453

estimates. The company has reported a lower top-line growth and a flattish

Face Value (`)

10

bottom-line. During the quarter, the company acquired Balkrishna Synthetics Ltd,

BSE Sensex

25,302

which is involved in the business of processing synthetic fabrics, for a

Nifty

7,750

consideration of ~`45cr. This acquisition will help SSML enhance its product

Reuters Code

SIYR.BO

portfolio.

Bloomberg Code

SIYA IN

Tepid top-line growth: The top-line for the quarter grew by 5% yoy to `505cr. The

top-line growth was soft owing to lower volume growth.

Shareholding Pattern (%)

Promoters

67.1

Underperformance at the EBITDA level: The EBITDA for the quarter grew by

MF / Banks / Indian Fls

6.3

~`3cr yoy to `60cr and the EBITDA margin contracted by 23bp yoy to 11.9% due

FII / NRIs / OCBs

0.6

to higher employee cost and other expenditure.

Indian Public / Others

26.0

Strong PAT growth: During the quarter, the net profit came in flat yoy at `32cr

due to lower sales growth and poor operating margin.

Abs.(%)

3m 1yr

3yr

Outlook and Valuation: Going forward, we expect SSML to report a net sales

Sensex

6.7

(9.1)

25.8

CAGR of ~12% to ~`2,040cr and adj.net profit CAGR of ~14% to `115cr over

SSML

7.9

(3.6)

300.8

FY2016-18E. The same would be on the back of market leadership in blended

fabrics, strong branding, wide distribution channel, strong presence in tier II and

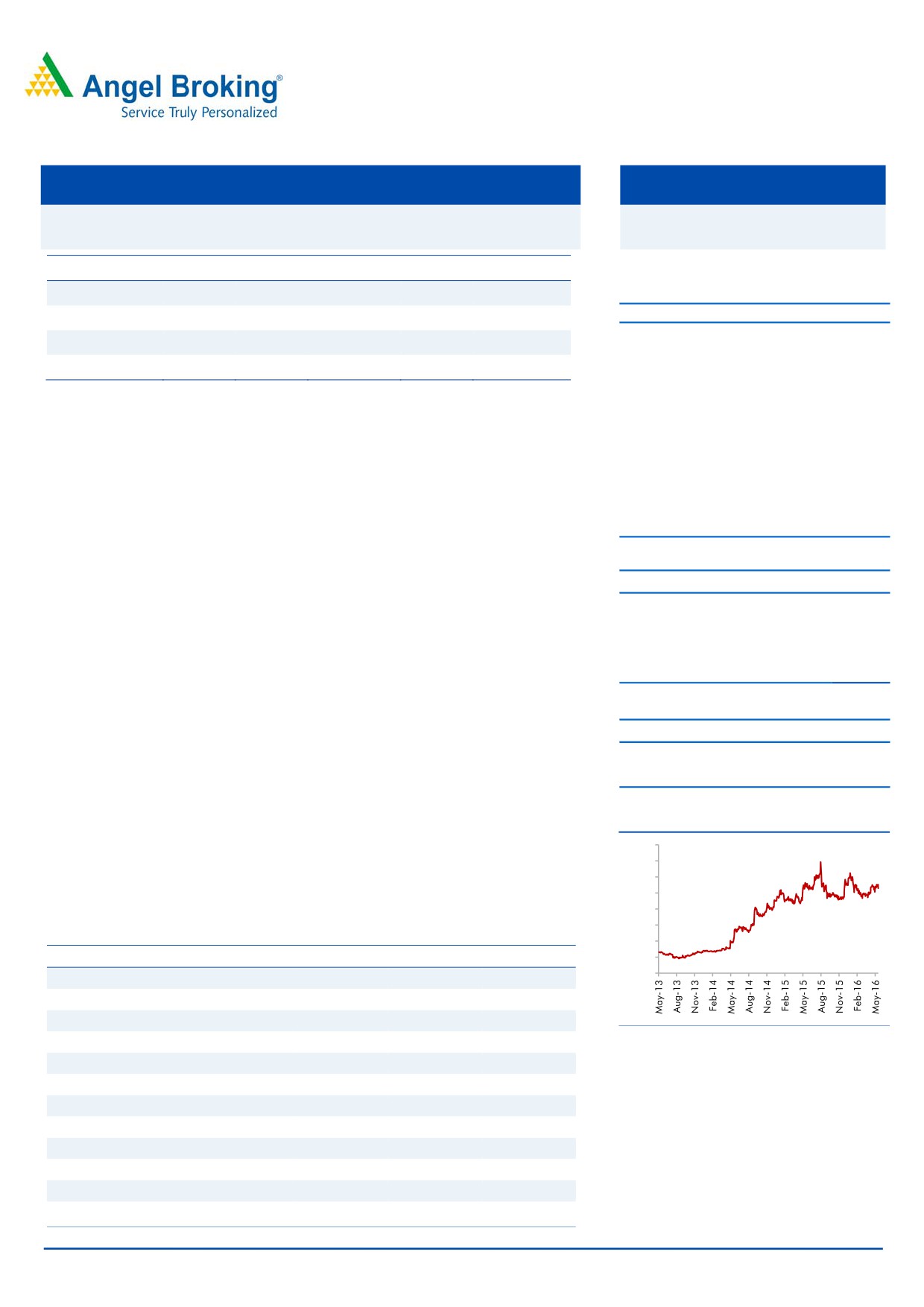

3-Year Daily price chart

tier III cities and emphasis on latest designs at affordable pricing points. At the

1,600

current market price, SSML trades at an inexpensive valuation (at a P/E of 8.6x its

1,400

FY2018E earnings). We have a Buy rating on the stock and target price of

1,200

1,000

`1,354.

800

600

Key financials

400

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

200

0

Net Sales

1,510

1,619

1,799

2,040

% chg

15.9

7.2

11.1

13.4

Net Profit

79

88

98

115

Source: Company, Angel Research

% chg

78.8

87.6

98.3

114.7

OPM (%)

11.5

11.6

11.6

11.7

EPS (`)

84.1

93.5

104.9

122.4

P/E (x)

12.6

11.3

10.1

8.6

P/BV (x)

2.3

1.9

1.7

1.4

RoE (%)

18.1

17.1

16.4

16.4

RoCE (%)

17.9

16.3

16.5

17.7

Amarjeet S Maurya

EV/Sales (x)

0.9

0.8

0.7

0.7

022-39357800 Ext: 6868

EV/EBITDA (x)

7.4

7.1

6.4

5.6

Source: Company,Angel Research; Note: CMP as of May 20, 2016,

Please refer to important disclosures at the end of this report

1

Siyaram Silk Mills | 4QFY2016 Result Update

Exhibit 1: Quarterly performance

Y/E March (` cr)

4QFY16

4QFY15

% chg. (yoy)

2QFY16

% chg. (qoq)

FY2016

FY2015

% chg

Net Sales

505

480

5.2

416

21.5

1,619

1,510

7.2

Net raw material

267

278

(4.0)

212

25.8

810

794

2.0

(% of Sales)

52.9

58.0

(509)

51.1

182

50.0

52.6

Employee Cost

43

33

30.8

34

26.7

144

123

16.8

(% of Sales)

8.5

6.8

166

8.1

35

8.9

8.2

Other Expenses

135

111

21.9

123

9.8

478

419

14.1

(% of Sales)

26.7

23.0

366

29.6

(285)

29.5

27.7

Total Expenditure

445

422

5.5

369

20.5

1,432

1,336

7.2

Operating Profit

60

58

3.2

47

28.8

188

174

8

OPM (%)

11.9

12.2

(23)

11.3

68

11.6

11.5

6

Interest

8

7

23.9

8

3.0

30

31

(0.3)

Depreciation

11

10

5.8

10

0.9

42

41

1.6

Other Income

4

4

12.8

5

(9.8)

17

16

5.5

PBT

46

45

0.4

33

38.5

133

119

11.6

(% of Sales)

9.0

9.5

7.9

8.2

7.9

Tax

14

13

2.0

12

12.3

45

40

12.5

(% of PBT)

29.7

29.2

36.6

34.0

33.8

Reported PAT

32

32

(0.3)

20

53.6

88

79

11.1

PATM (%)

6.3

6.7

5.0

5.4

5.2

Source: Company, Angel Research

May 23, 2016

2

Siyaram Silk Mills | 4QFY2016 Result Update

Investment arguments

Leadership in blended fabric to support growth

Revenue to grow at a CAGR of 12%

SSML is the largest manufacturer of blended high fashion suitings, shirtings and

over FY2016-18E to `2,040cr

apparels in the country. A portfolio of strong and value-for-money brands like

Siyaram’s, J Hampstead and Mistair in the fabric segment place SSML in a sweet

spot. The company has launched two new premium cotton brands - Zenesis and

Moretti, and has penetrated further into new growth areas like cotton shirting,

linen fabrics etc.

SSML has been able to differentiate itself from unorganized and organized

competitors in a highly fragmented market. The offerings of the company are

available at various price points in the low and mid-range which enable it to

compete with brands like Raymond, Reid & Taylor, Grasim, Digjam, and Gwalior,

which offer similar products. Shifting preference of consumers from unbranded

fabrics to branded blended fabrics would likely aid the company’s growth

prospects. With a strong market position, pan-India presence and high brand

recognition, along with increasing diversification in revenue profile, we expect the

company’s revenue to grow at a CAGR of 12% over FY2016-18E to `2040cr.

Rigorous advertisement and retail expansion to push demand

SSML has built a strong brand presence in the country through continuous

advertisement and brand-building efforts. Its emphasis on latest fabrics, innovative

and latest designs and affordable pricing points give it an edge over competition.

Every brand of the company holds a distinct position in the consumers’ minds

which has helped the company in creating a niche for itself in a highly competitive

industry.

Additionally, the company has been spending rigorously on advertising for the

recognition of its brands. The company has signed up celebrities like M S Dhoni

(Siyaram’s, MSD), Saif Ali Khan (Oxemberg) and Hrithik Roshan (J. Hampstead) as

brand ambassadors for its products.

Moreover, SSML has one of the largest distribution networks in the country with

over 1,600 dealers and 500 agents supplying to more than 40,000 outlets across

India. This enables the company to launch new products with a high success ratio

and low marketing cost, giving it an edge over competition. In order to expand its

retail footprint, the company continues to add stores through the franchise model.

The company plans to increase the number of stores through franchisees to 500 by

FY2017E.

Venturing into women’s segment - a long term growth driver

Company has roped in celebrities like

The company has ventured into the salwar kameez and ethnic women’s wear

Parineeti Chopra and Karishma Kapoor

segment with its brand - Siya. The Siya brand comprises of semi-stitched cotton,

to endorse Siya

polyester and embroidered designer fabrics, with prices ranging from `700 to

`7,000. For FY2015, the company generated a revenue of ~`38cr from the

segment and it plans to grow it to `500cr in the coming four to five years as there

are hardly any national-level mass brands in the category. SSML has roped in

celebrities Parineeti Chopra and Karishma Kapoor to endorse the brand. As per

industry reports (Technopak study in 2011), salwar kameez and ethnic women’s

May 23, 2016

3

Siyaram Silk Mills | 4QFY2016 Result Update

wear is a `20,690cr category, growing at a CAGR of 10%, which gives immense

opportunity to the company.

Outlook and valuation

Going forward, we expect SSML to report a net sales CAGR of ~12% to

~`2,040cr and adj.net profit CAGR of ~14% to `115cr over FY2016-18E. The

same would be on the back of market leadership in blended fabrics, strong

branding, wide distribution channel, strong presence in tier II and tier III cities and

emphasis on latest designs at affordable pricing points. At the current market

price, SSML trades at an inexpensive valuation (at a P/E of 8.6x its FY2018E

earnings). We have a Buy rating on the stock and target price of `1,354.

Concerns

Decline in rural spending: Unseasonal rains and deficient rainfall in the rural

areas may result in lower agriculture output. This in turn could result in lower

discretionary spending among rural consumers which could impact the company’s

overall sales.

Competition from the unorganized sector: SSML, being in a sector that’s highly

unorganized, faces intense competition from unorganized players as they usually

sell their products at a much cheaper rate compared to it. However, due to strong

branding efforts, huge distribution network and affordable price points, the

company is easily able to differentiate its products from those of competitors.

Fluctuation in raw material prices: SSML operates in a highly price-sensitive

market. Any fluctuation in raw-material prices can lead to margin compression, as

the company may not be able to pass on the entire increase to the end-user.

May 23, 2016

4

Siyaram Silk Mills | 4QFY2016 Result Update

Company background

SSML is the largest manufacturer of blended fabrics in India. The company enjoys

a strong brand presence across the country, with brands such as Siyaram’s,

Mistair, MSD, J. Hampstead and Oxemberg in its kitty. The company has also

launched three premium brands - Royal Linen (linen fabrics for men and women),

Moretti (cotton shirting) and Zenesis (cotton suitings). SSML has built a strong

brand presence in the country through continuous advertisement and brand-

building efforts over the past 30 years. The company has created a niche for itself

in a highly competitive industry.

It has a wide distribution network comprising 1,600 dealers and 500 agents

supplying to more than 40,000 outlets across India and has ~160 franchise

stores. The company operates four plants - one at Tarapur near Mumbai for

weaving and yarn dyeing, two at Daman for garments and one at Silvassa for

weaving.

May 23, 2016

5

Siyaram Silk Mills | 4QFY2016 Result Update

Profit and loss statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017E

FY2018E

Total operating income

1,041

1,303

1,510

1,619

1,799

2,040

% chg

13.7

25.2

15.9

7.2

11.1

13.4

Total Expenditure

931

1,163

1,336

1,432

1,590

1,801

Cost of Materials

532

671

794

810

948

1,077

Personnel

89

108

123

144

151

173

Others Expenses

310

384

419

478

491

550

EBITDA

110

140

174

188

209

240

% chg

(5.4)

27.1

24.3

7.8

11.2

14.8

(% of Net Sales)

10.6

10.7

11.5

11.6

11.6

11.7

Depreciation& Amortisation

22

29

41

42

44

45

EBIT

88

111

133

146

165

194

% chg

(6.1)

25.5

20.1

9.6

12.9

17.6

(% of Net Sales)

8.5

8.5

8.8

9.0

9.2

9.5

Interest & other Charges

25

29

31

30

35

40

Other Income

19

16

16

17

17

17

(% of PBT)

22.6

16.1

13.6

12.9

11.7

10.0

Share in profit of Associates

-

-

-

-

-

-

Recurring PBT

82

98

119

133

147

171

% chg

0.7

19.8

21.4

11.6

10.5

16.7

Prior Period & Extraord. Exp./(Inc.)

-

-

-

-

-

-

PBT (reported)

82

98

119

133

147

171

Tax

27

34

40

45

48

57

(% of PBT)

32.7

35.1

33.8

34.0

33.0

33.0

PAT (reported)

55

64

79

88

98

115

Add: Share of earnings of asso.

-

-

-

-

-

-

ADJ. PAT

55

64

79

88

98

115

% chg

55.0

63.6

78.8

87.6

98.3

114.7

(% of Net Sales)

5.3

4.9

5.2

5.4

5.5

5.6

Basic EPS (`)

58.7

67.8

84.1

93.5

104.9

122.4

Fully Diluted EPS (`)

58.7

67.8

84.1

93.5

104.9

122.4

% chg

(3.0)

15.6

23.9

11.1

12.3

16.7

May 23, 2016

6

Siyaram Silk Mills | 4QFY2016 Result Update

Balance sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E FY2018E

SOURCES OF FUNDS

Equity Share Capital

9

9

9

9

9

9

Reserves& Surplus

305

360

426

503

589

690

Shareholders Funds

314

370

435

512

599

699

Minority Interest

-

-

-

-

-

-

Total Loans

278

314

309

386

400

400

Deferred Tax Liability

22

26

23

23

23

23

Total Liabilities

614

709

767

920

1,021

1,122

APPLICATION OF FUNDS

Gross Block

499

570

589

609

639

659

Less: Acc. Depreciation

194

220

258

299

343

388

Net Block

305

349

332

310

297

271

Capital Work-in-Progress

16

3

7

7

7

7

Investments

0

0

0

46

46

46

Current Assets

466

543

638

773

900

1,054

Inventories

222

225

238

326

384

447

Sundry Debtors

200

260

335

368

419

486

Cash

3

6

5

6

7

8

Loans & Advances

33

39

45

57

72

92

Other Assets

8

13

15

16

18

20

Current liabilities

176

190

214

221

234

262

Net Current Assets

290

353

424

551

666

792

Deferred Tax Asset

3

3

4

4

4

4

Mis. Exp. not written off

-

-

-

-

-

-

Total Assets

614

709

767

920

1,021

1,122

May 23, 2016

7

Siyaram Silk Mills | 4QFY2016 Result Update

Cash flow statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E FY2018E

Profit before tax

82

98

119

133

147

171

Depreciation

22

29

41

42

44

45

Change in Working Capital

(28)

(87)

(120)

(127)

(113)

(125)

Interest / Dividend (Net)

17

19

21

30

35

40

Direct taxes paid

(25)

(34)

(40)

(45)

(48)

(57)

Others

1

41

38

-

-

-

Cash Flow from Operations

68

65

58

33

64

76

(Inc.)/ Dec. in Fixed Assets

(70)

(61)

(23)

(112)

(30)

(20)

(Inc.)/ Dec. in Investments

3

-

-

(46)

-

-

Cash Flow from Investing

(73)

(61)

(23)

(66)

(30)

(20)

Issue of Equity

-

0

-

-

-

-

Inc./(Dec.) in loans

-

-

-

76

14

-

Dividend Paid (Incl. Tax)

(7)

(7)

(7)

11

12

14

Interest / Dividend (Net)

14

5

(30)

(52)

(59)

(68)

Cash Flow from Financing

7

(2)

(38)

35

(33)

(54)

Inc./(Dec.) in Cash

2

3

(2)

2

1

2

Opening Cash balances

2

3

5

3

6

7

Closing Cash balances

3

5

3

6

7

8

May 23, 2016

8

Siyaram Silk Mills | 4QFY2016 Result Update

Key ratios

Y/E March

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

18.0

15.6

12.6

11.3

10.1

8.6

P/CEPS

58.8

67.9

84.2

93.5

105.0

122.5

P/BV

3.2

2.7

2.3

1.9

1.7

1.4

Dividend yield (%)

0.7

0.7

0.9

1.0

1.1

1.3

EV/Sales

1.2

1.0

0.9

0.8

0.7

0.7

EV/EBITDA

11.5

9.3

7.4

7.1

6.4

5.6

EV / Total Assets

1.6

1.4

1.3

1.2

1.1

1.0

Per Share Data (`)

EPS (Basic)

58.7

67.8

84.1

93.5

104.9

122.4

EPS (fully diluted)

58.7

67.8

84.1

93.5

104.9

122.4

Cash EPS

18.0

15.6

12.6

11.3

10.1

8.6

DPS

7.0

7.5

9.4

10.5

11.8

13.8

Book Value

335.2

394.5

464.2

546.4

638.8

746.5

Returns (%)

ROCE

14.9

16.2

17.9

16.3

16.5

17.7

Angel ROIC (Pre-tax)

15.0

16.4

18.0

17.3

17.4

18.6

ROE

17.5

17.2

18.1

17.1

16.4

16.4

Turnover ratios (x)

Asset Turnover (Gross Block)

2.1

2.3

2.6

2.7

2.8

3.1

Inventory / Sales (days)

78

63

58

74

78

80

Receivables (days)

70

73

81

83

85

87

Payables (days)

42

34

34

34

34

34

WC cycle (ex-cash) (days)

106

102

105

123

129

133

May 23, 2016

9

Siyaram Silk Mills | 4QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitian Stock Exchange of India Limited. It is also registered as a Depository Participant

with CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private

Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration

number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for

accessing /dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial

interest/beneficial ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any

compensation / managed or co-managed public offering of securities of the company covered by Analyst during the past twelve

months. Angel/analyst has not served as an officer, director or employee of company covered by Analyst and has not been engaged in

market making activity of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Siyaram Silk Mills

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

May 23, 2016

10