Initiating coverage | Dairy products

April 16, 2018

Parag Milk Foods Limited

BUY

CMP

`249

Evolving into a dairy FMCG brand story..

Target Price

`333

Parag Milk Foods (PARAG) is one of the leading dairy products companies in

Investment Period

12 Months

India. The company has been successful in creating strong brands like GO,

Gowardhan and in introducing new products like Whey Protein. It has become

Stock Info

the 2nd player in processed cheese (after Amul) in a short span of 10 years and

Sector

Dairy Products

commands 33% market share. Rising revenue share of high-margin value added

Market Cap (` cr)

2,092

products (VAP) is likely to boost its margins in coming years.

Net Debt (` cr)

162

Favorable market dynamics: Indian dairy industry is valued at

~`600000 cr,

growing at 10%+CAGR which presents a strong opportunity for the organized

Beta

1.1

sector (currently contributes ~22%). Driven by rising awareness and income level,

52 Week High / Low

319/206

organized players share’s is expected to increase to 26% by 2020. PARAG is likely

Avg. Daily Volume

2,12,755

to be one of the key beneficiaries of this shift.

Face Value (`)

10

Product portfolio shifting towards high margin products: VAP like cheese, whey

BSE Sensex

34,192

protein enjoy higher gross margins of 25-45% versus 6-8% entailed in liquid milk.

Nifty

10,480

VAP forms ~66% to its revenue (the highest among the listed players versus 25-

30% for others). With rising health awareness, its whey protein brand (Avvataar)

Reuters Code

PAMF.NS

could be a >`150 crore brand in next 2-3 years. Driven by recently launched

Bloomberg Code

PARAG.IN

products and higher share of VAP, its operating margins would improve to 10-

11% in next few years.

Shareholding Pattern (%)

Reducing leverage and improving return ratios: PARAG is likely to incur a capex

Promoters

48.7

of ~`150 cr over FY2017-20 which is to be internally funded. With regular debt

repayments, DE ratio is also likely to go down. With improving margins, its return

MF / Banks / Indian Fls

13.0

ratios would normalize to 14-15% after making a temporary dip in FY2017.

FII / NRIs / OCBs

17.5

Outlook and valuation: We expect PARAG to report net revenue/PAT CAGR of

Indian Public / Others

20.9

13%/27% respectively over FY2018-20E. The stock currently trades at a P/E of

14.9x FY2020E EPS. It is increasingly becoming a stable brand strory while it is

still valued as commodity business. We feel that the company should somewhere

Abs. (%)

3m 1yr 3yr

start enjoying the valuation of FMCG companies. We initiate coverage on the

Sensex

(1.4)

15.0

16.7

stock with a BUY recommendation and Target Price of `333 (20x FY2020E EPS),

PARAG

(13.4)

1.5

-

an upside of 34% from the current levels.

Key Financials (Consolidated)

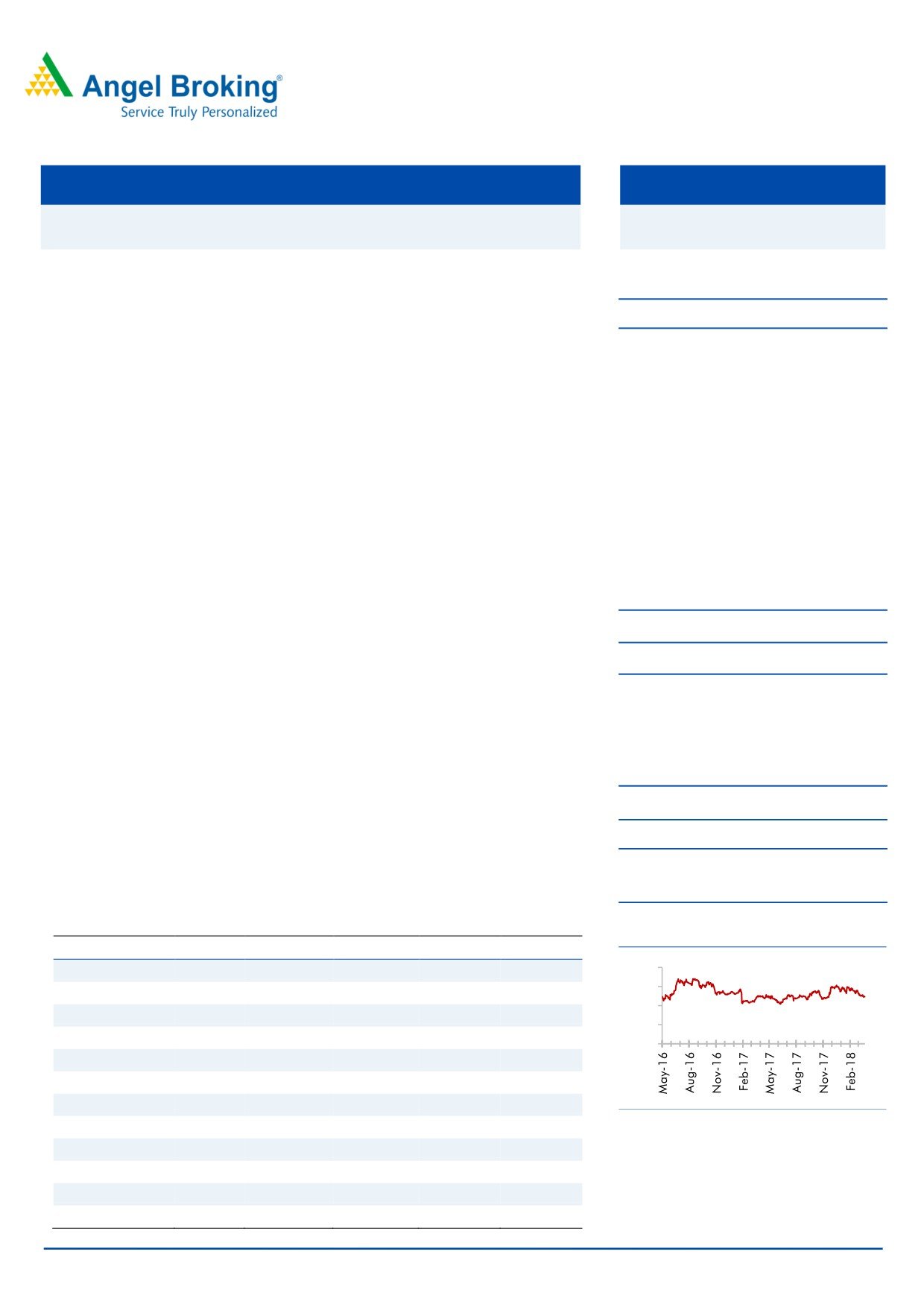

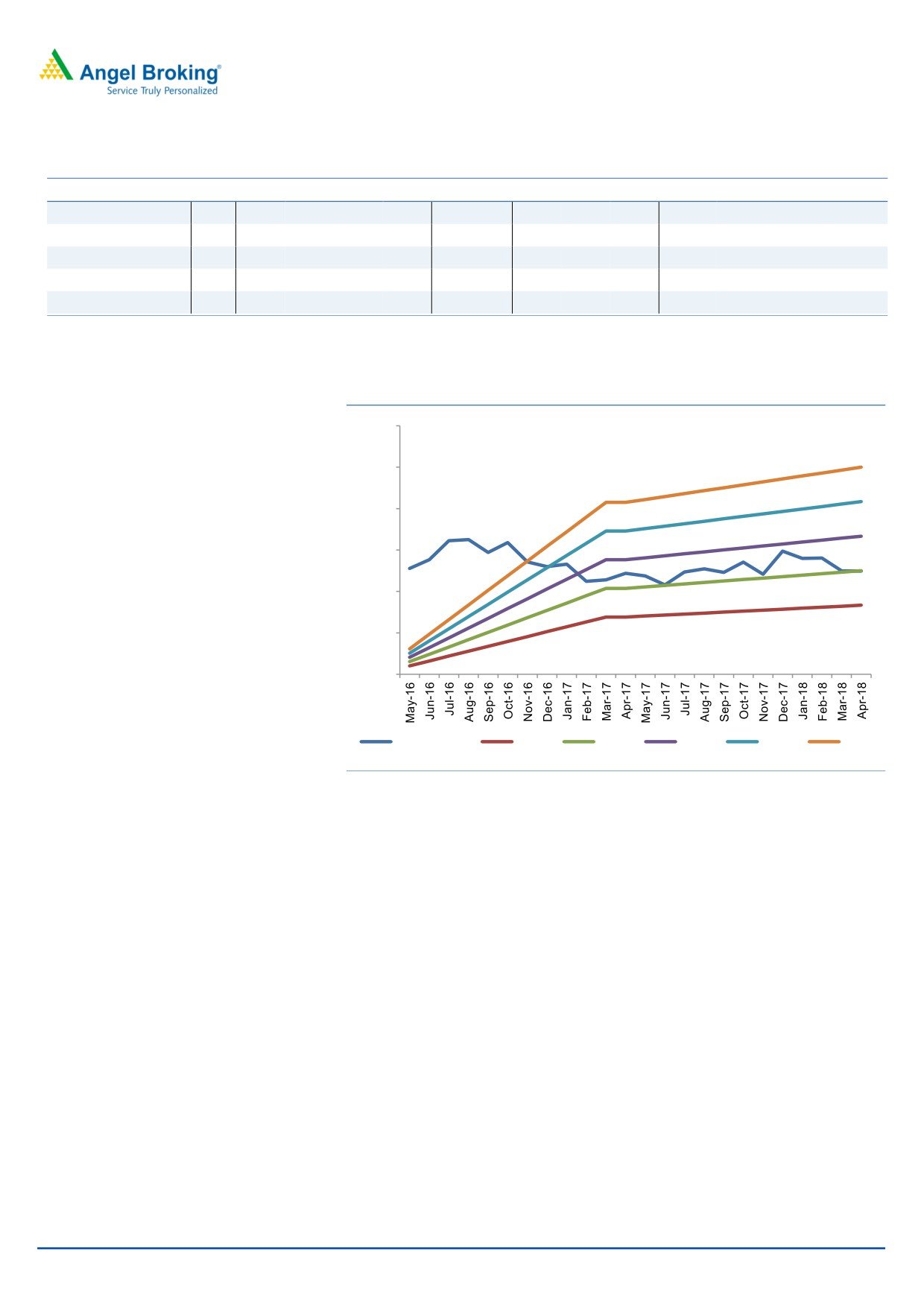

Price Chart

Y/E March (Rs cr)

FY2016

FY2017E

FY2018E

FY2019E

FY2020E

400

Net Sales

1,645

1,731

1,957

2,214

2,498

300

% chg

13.9

5.2

13.1

13.1

12.9

200

Net Profit

49.4

35.9

86.7

116.3

140.2

100

% chg

33.0

(27.2)

141.4

34.1

20.5

0

OPM (%)

9.0

5.1

9.7

10.4

10.6

EPS (Rs)

5.9

4.3

10.3

13.8

16.7

P/E (x)

42.4

58.3

24.1

18.0

14.9

Source: Company, Angel Research

P/BV (x)

5.8

3.2

2.8

2.4

2.1

RoE (%)

13.6

5.5

11.7

13.5

14.0

Nidhi Agrawal

RoCE (%)

15.3

4.3

14.3

16.6

18.0

022 - 3935 7800 Ext: 6872

EV/Sales (x)

1.5

1.3

1.1

1.0

0.9

EV/EBITDA (x)

16.7

25.4

11.7

9.6

8.2

Source: Company, Angel Research; Note: closing price of April 13 , 2018

Please refer to important disclosures at the end of this report

1

Initiating coverage | Menon Bearings

Parag Milk Foods in charts

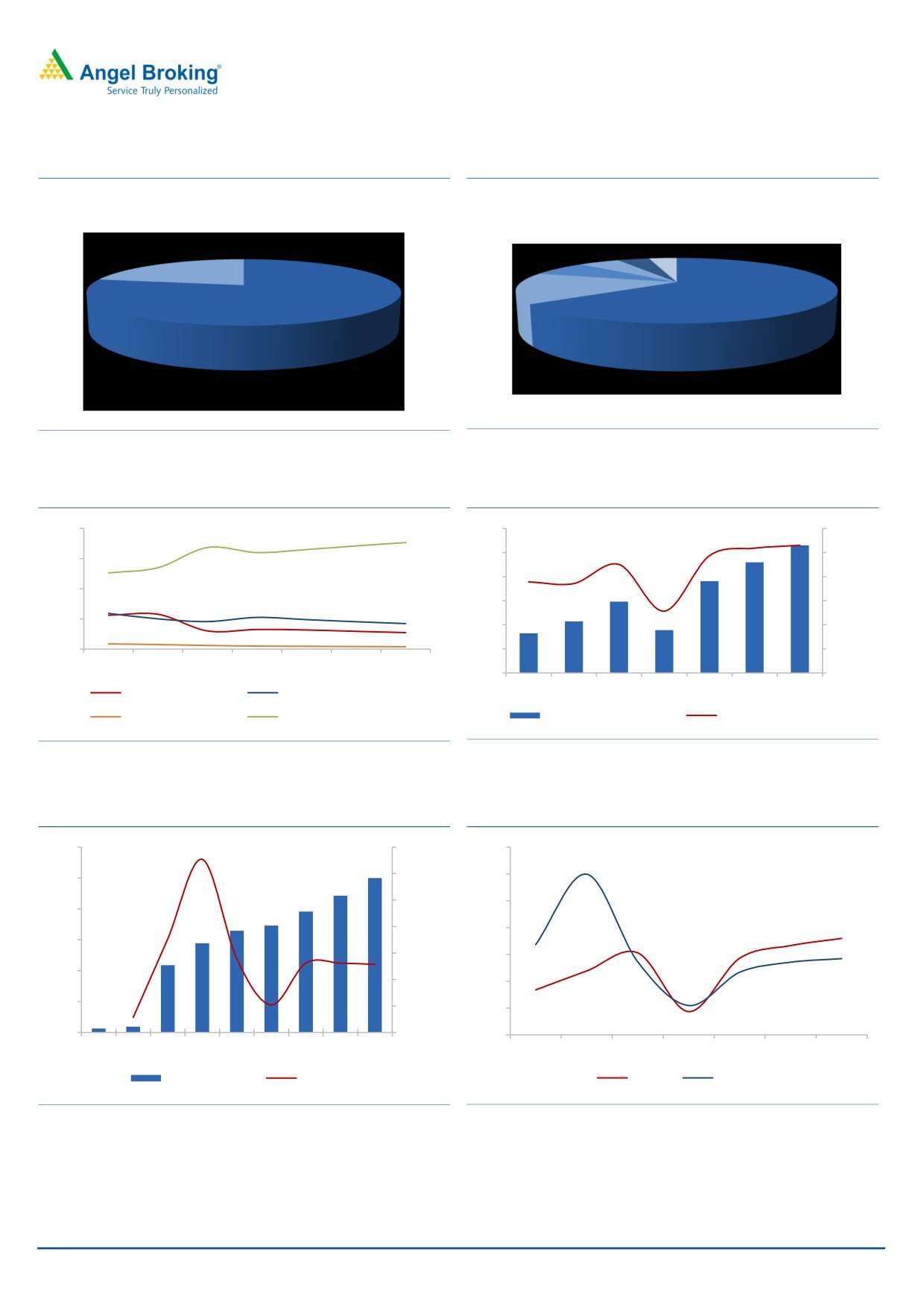

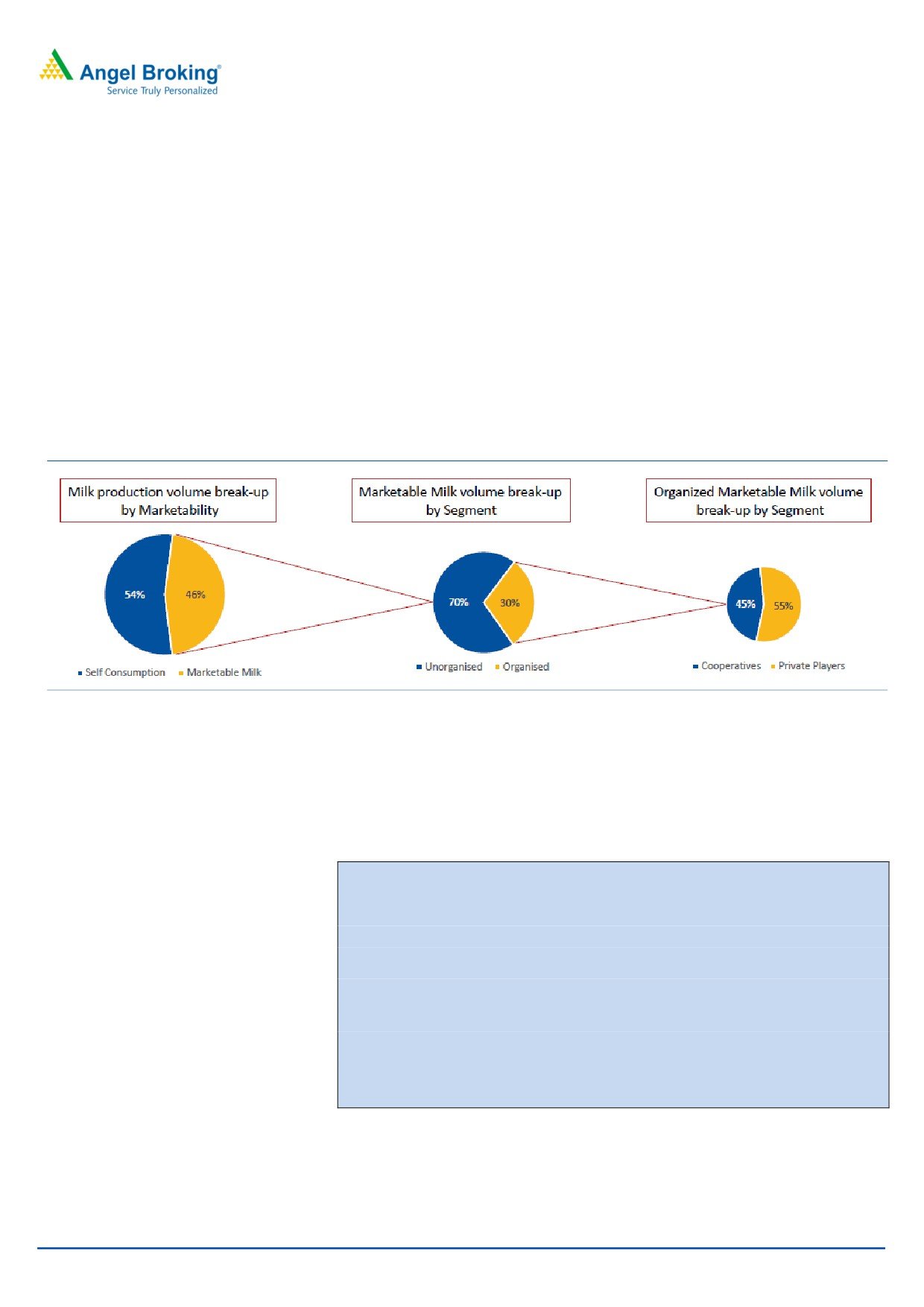

Exhibit 1: Organised dairy industry forms only 22%

Exhibit 2: Liquid Milk forms the biggest chunk

Unorganised

Liquid Milk

Curd Butter Others

Organised

78%

5%

4%

4%

65%

22%

Paneer

7%

Ghee

15%

Source: Company, Angel Research

Source: Company, Angel Research

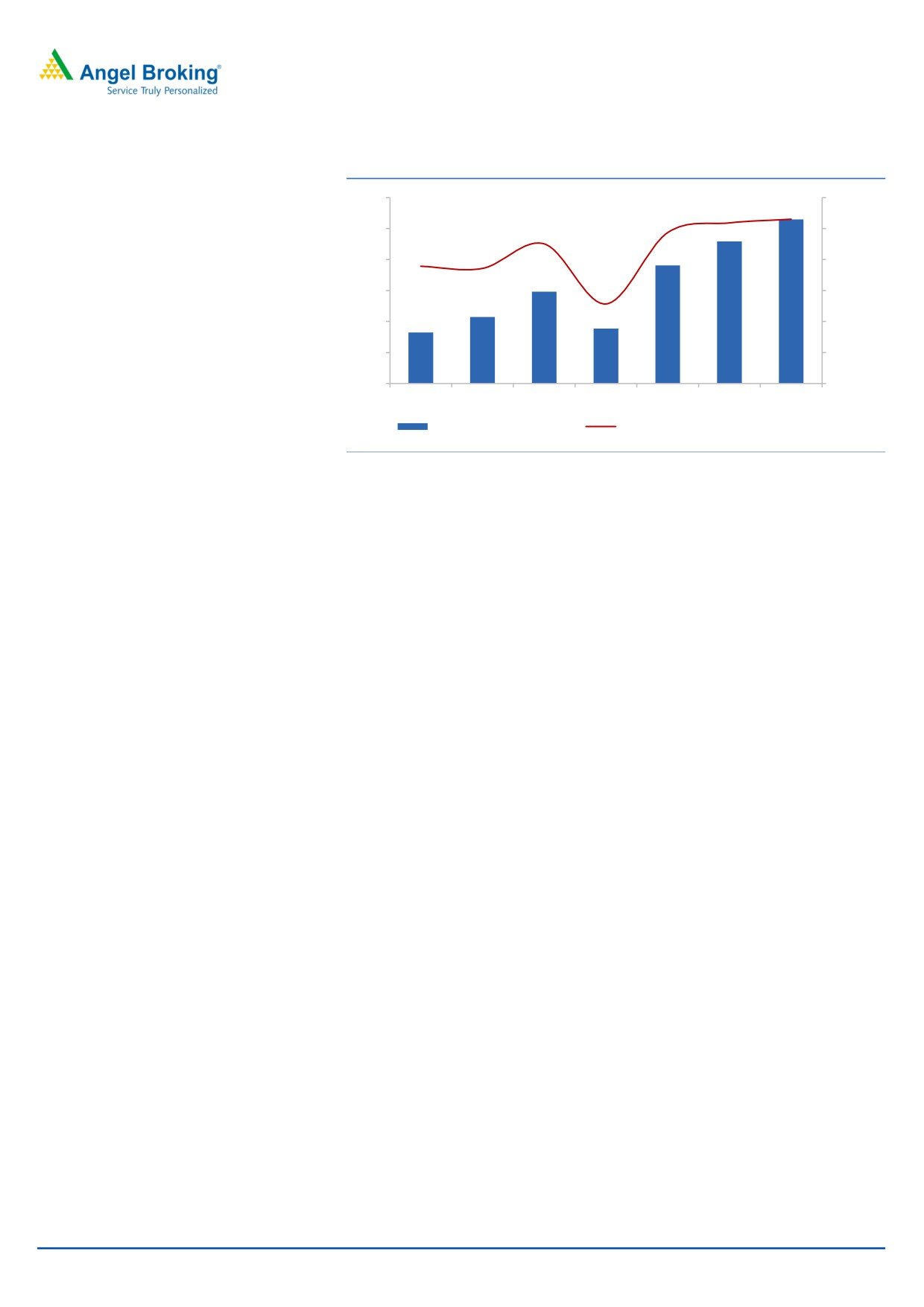

Exhibit 3: Share of VAP to go up for Parag

Exhibit 4: Improving its margin profile

80%

300

12.0%

250

10.0%

60%

200

8.0%

40%

150

6.0%

20%

100

4.0%

0%

50

2.0%

FY14 FY15 FY16 FY17 FY18 FY19 FY20

0

0.0%

FY14 FY15 FY16 FY17 FY18 FY19 FY20

Skimmed Milk Powder

Liquid Milk

Others-Job Work

Value added products

Operating profit (` cr)

Operating margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 5: Revenue to grow well for next few years

Exhibit 6: Return ratios normalising after FY2017 dip

3000

35%

35

30

30%

2500

25%

25

2000

20%

20

1500

15%

15

1000

10%

10

500

5%

5

0

0%

-

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

FY14

FY15

FY16

FY17

FY18

FY19

FY20

Net Sales- ` cr

YoY chg (%)

ROE %

ROCE %

Source: Company, Angel Research

Source: Company, Angel Research

April 16, 2018

2

Initiating coverage | Parag Milk Foods

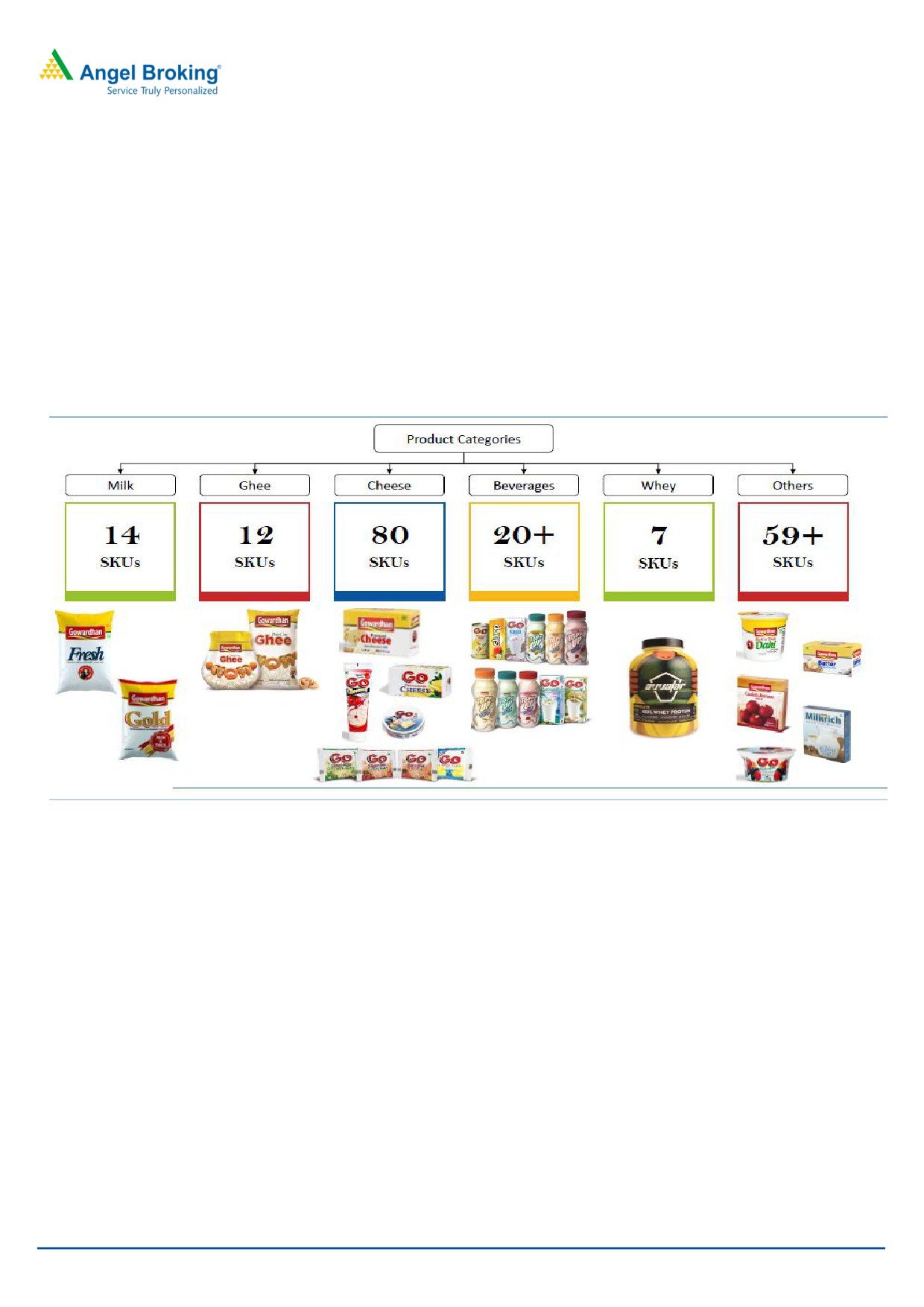

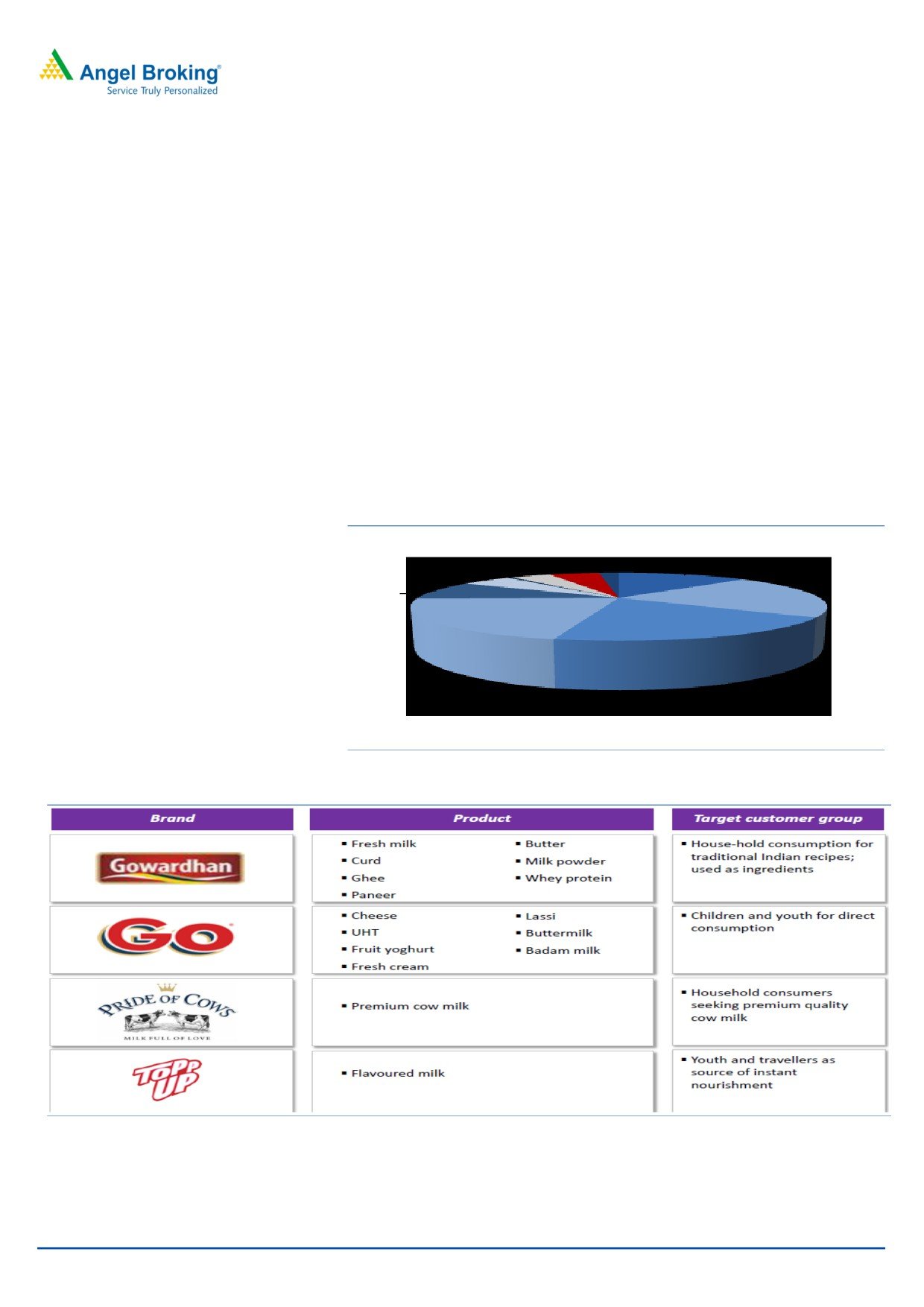

Company background

PARAG started in 1992 to help farmers by collecting milk on milk holidays

during Operation Flood. Back then, PARAG was primarily involved in the

distribution and collection of milk. In 1998, the company set up Bhagyalaxmi

Dairy Farm - India’s most modern dairy farm with the finest international

equipments. It manufactures a diverse range of products including cheese,

ghee (clarified butter), fresh milk, whey proteins, paneer, curd, yoghurt, milk

powders and dairy based beverages. ‘Gowardhan’ and ‘Go’, its flagship

brands, are among the leading ghee, cheese and other value added product

brands in India. It also supply farm-to-home premium fresh milk from

Bhagyalaxmi Dairy Farm, which it market and sell under ‘Pride of Cows’ brand

in Mumbai and Pune.

Exhibit 7: Well diversified branded portfolio

Source: Company

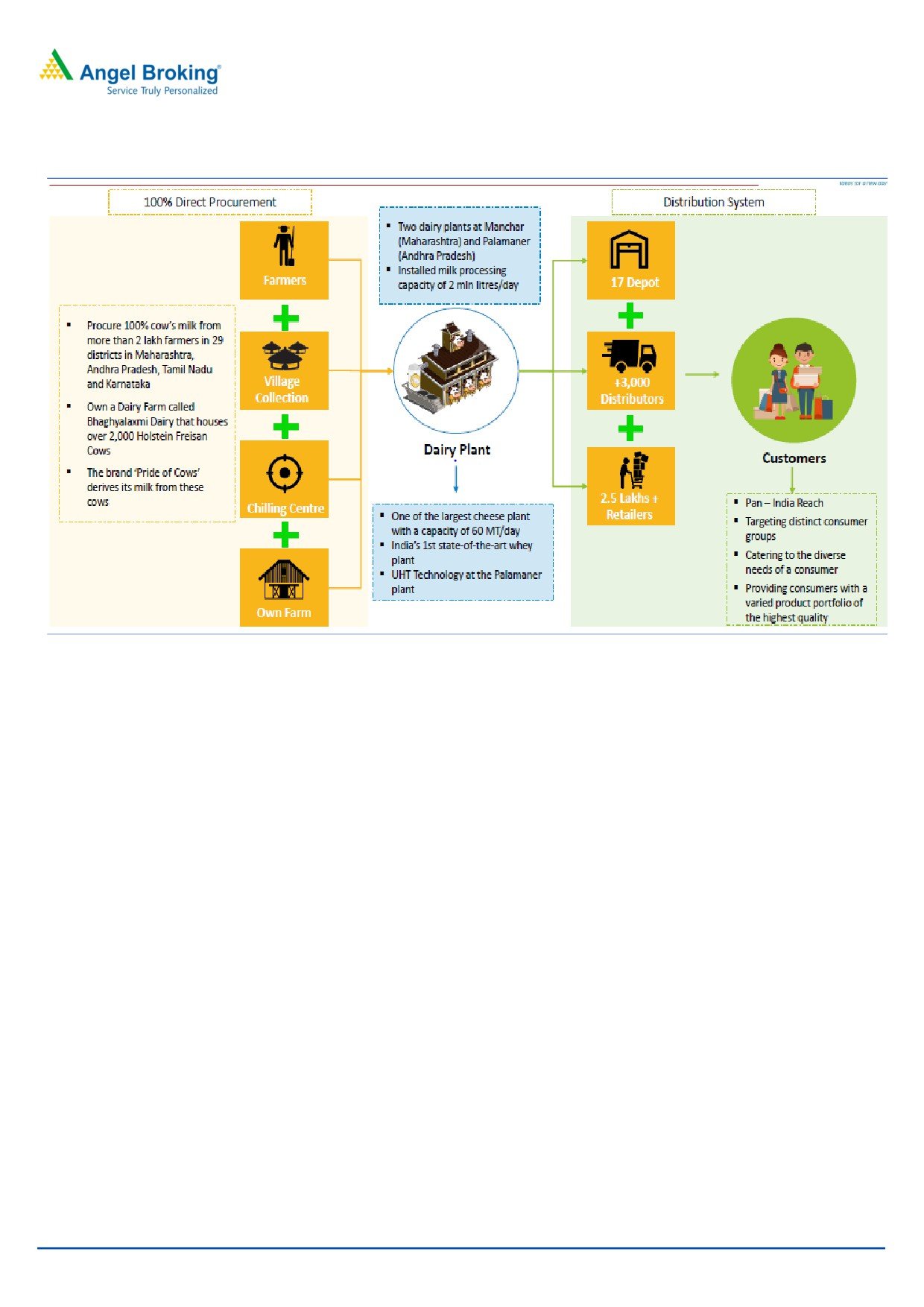

Milk procurement and processing capabilities

Its 3-tier milk procurement system involves over 2,00,000 farmers from 29 districts

of Maharashtra, Andhra Pradesh, Karnataka and Tamil Nadu through more than

3,400 village-level milk collection centres collecting nearly 1.2 million litres of milk

every day. It has two manufacturing plants at Manchar in Maharashtra and

Palamaner in Andhra Pradesh. Its current processing capacity is 2 million litres per

day between two plants. It cheese capacity has been increased from 40 MT to 60

MT per day. It also has the first-of-its-kind whey processing plant and a fully

automated Paneer plant with capacity of 20 MT per day.

April 16, 2018

3

Initiating coverage | Parag Milk Foods

Exhibit 8: Procurement and distribution system of PARAG

Source: Company, Angel Research

April 16, 2018

4

Initiating coverage | Parag Milk Foods

Investment Rationale

Favorable market dynamics:

1. Shift from unorganized to organized

Indian dairy industry is valued at

`600000 cr+, growing at ~10%+ CAGR. This

growth presents a strong opportunity for the organized sector which currently

contributes ~22%. In India, over 80% of milk is consumed in the liquid form, as

opposed to developed countries that consume a large portion of milk in the form

of dairy products/VAP. Driven by rising awareness, new products launch,

aggressive marketing (by leading players) and income level, organized players

share’s is expected to increase to 26% by 2020. PARAG is likely to be one of the

key beneficiaries of this shift.

Exhibit 9: Currently >10% of the milk production is marketed by private players

Source: Company, Angel Research

2. Increasing health awareness and innovation

Consumers are increasingly health conscious and are preferring nutritious, low-

carb, high-protein meals. They are experimenting with niche categories and

therefore demand is fast growing for products like milk-based juice drinks, sports

nutrition like whey protein, amongst others. ~31% of Indian population is

vegetarian, for whom milk is a important source of vital nutrients.

Over the past decade, VAPs have been rapidly growing due to:

1) Rising income levels due to a rising middle class and working population

2) Rising number of dual income households through increase in the number of

working women

3) Increase in urban population

4) Rapidly expanding food service industry (Rise in HORECA - Hotels, Restaurants

& Caterers segment)

5) Aggressive spending on advertisement and sales promotions by organised

players to create awareness among consumers

3. Changing Dietary Patterns

Over the years, the consumption trend has changed with people shifting from

home-made dahi, ghee and paneer to branded products due to convenience in

April 16, 2018

5

Initiating coverage | Parag Milk Foods

buying and higher assurance of quality. This has promoted the growth in demand

for dairy and VAP.

Product portfolio shifting towards high margin products

Well established brands and diversified product portfolio

PARAG has well recognized brands like ‘Gowardhan’ and ‘Go’ in its portfolio. It

markets dairy products (milk, ghee, paneer, butter, etc) and processed cheese

blocks under the ‘Gowardhan’ brand. It has launched a wide range of cheese

products, UHT, fresh cream etc, since 2008 under the ‘Go’ brand which have

gained good traction since their launches. ‘Gowardhan’ has been recognized as

the most trusted brand in the food products category and ‘Go’ has been

acknowledged as the “Most Promising Brand” in the FMCG category. ‘Go’ cheese

has been competing with products of the established market leader- Amul and has

grabbed 33% of market share in a short span of 10 years. It has other brands like

‘Pride of Cows‘ (premium quality cow milk) and ‘Topp Up‘ (beverages).

Exhibit 10: FY2017 revenue break-up

Flavoured

Others-Job

Skimmed

Whey

Curd

Work

UHT and

Milk

Milk Powder

4%

5%

2%

chass lassi

0%

13%

5%

Butter

Liquid Milk

9%

21%

Cheese/ Paneer

Ghee

21%

20%

Source: Company

Exhibit 11: Differentiated brand and product portfolio

Source: Company

April 16, 2018

6

Initiating coverage | Parag Milk Foods

Product portfolio shifting towards high margin products

Value Added Products (VAP) like paneer, whey protein and cheese enjoy higher

gross margins of 25-45% as compared to 6-8% margins entailed in liquid milk.

VAP currently contributes ~66% to its revenue (highest in the industry as against

25-30% for other leading players). This is likely to touch 75% in next 2-3 years.

Increasing VAP’s revenue share will almost double its margins from 5.4% in

FY2017 to 10.6% in FY2020. In M9FY2018, the company has registered a OPM

of 9.6%, increased from 2.4% in M9FY2017.

Exhibit 12: Product-wise revenue contribution and margins

Source: Company

Exhibit 13: Rising revenue share of VAP would boost margins

FY20

FY19

FY18

FY17

FY16

FY15

FY14

0%

20%

40%

60%

80%

100%

120%

Skimmed Milk Powder Liquid Milk Others-Job Work Value added products

Source: Company, Angel Research

April 16, 2018

7

Initiating coverage | Parag Milk Foods

Exhibit 14: Improving margin profile

300

12.0%

250

10.0%

200

8.0%

150

6.0%

100

4.0%

50

2.0%

0

0.0%

FY14

FY15

FY16

FY17

FY18

FY19

FY20

Operating profit (` cr)

Operating margin (%)

Source: Company, Angel Research

New category holding good potential

Whey protein under Avvatar brand

Avvatar is the first Indian whey protein powder which is pure vegetarian and is

derived from milk protein only and is soya free and sugar free. It is generated

as a by-product during the manufacture of cheese. 1 kg cheese generates 50%

(i.e 500 gms) of whey. This is a very good source of protein and is most sought

after protein drink in the sports nutrition category. Till recently, the company

was selling whey in crude form to the institutional segment. However, it has

recently launched whey protein in retail under the Avvatar brand, which is sold

directly to end consumers. The product is being distributed via tie ups with

premium sports gyms, nutrition outlets and e-portals like Amazon.

Whey protein market dominated by imports- PARAG can substitute

Currently, the market is dominated by imported brands that constitute around 80-

90% of the overall pie. The market size is estimated at `1500 cr, growing at 12-

13% CAGR. The market is dominated by imported brands that dominates over

80% of the market as there is no domestic brand in the market. Hence, with

introduction of Avvatar, Parag has become first mover in this category and can

capture this high margin segment (40%) as the imported products become little

dated while Avvatar being a local brand offers a fresher and effective substitute.

Avvatar’s revenue are expected to touch

`20cr in FY2018. With a better

distribution and marketing strategy, the product sale is expected to touch `100 cr

in FY2019 and could be `150cr brand in another 1-2 years.

April 16, 2018

8

Initiating coverage | Parag Milk Foods

Exhibit 15: Focus towards modern products which current forms only 10% of the organized market

Source: Company

Emerged as the leading player in cheese in a short span

Cheese accounts for 21% of its FY2017 revenue and has grown to command 33%

market share in Indian cheese market mainly driven by constant new product

launch and aggressive marketing. Indian processed cheese market is valued at

~` 1000 cr market in FY2017 and is growing in excess of 15% for past couple of

years. Amul is the market leader with 40% market share, Britannia-9% and

Dynamix - 7%. The Indian fast food market is growing rapidly and cheese is quite

popularly consumed with a number of fast foods such as Pizzas, Burgers, Garlic

breads, and Sandwiches. Apart from western dishes, cheese is also being added

as a taste enhancer in several traditional Indian recipes such as Dosas, Paratha,

Pav Bhaji, amongst others. These trends would keep the buoyant demand for

PARAG cheese segment.

Reducing leverage and improving return ratios

Demonetization and high raw milk procurement prices had led to poor

performance in FY2017. With improving margins, its return ratios would also

return to 14-15% from the temporary dip made in FY2017. Debt is expected to

reduce over the next three years from the stabilization of profitability since FY2018.

The company is likely to invest over `150 cr over FY2017-20 in its manufacturing

facilities which is to be funded by mix of IPO proceeds and internal accruals. The

company is likely to generate ~`100 cr+ annually as operating cash inflow which

would fund its annual capex plan of~ `50-60 cr.

April 16, 2018

9

Initiating coverage | Parag Milk Foods

Exhibit 16: Improving return ratios

Exhibit 17: Capex to be largely funded internally

35

200

30

150

25

100

20

15

50

10

0

FY14 FY15 FY16 FY17 FY18 FY19 FY20

5

(50)

-

FY14 FY15 FY16 FY17 FY18 FY19 FY20

Net Cash Flow From Operating Activities (` cr)

ROE %

ROCE %

Free cash flow generated (` cr)

Source: Company, Angel Research

Source: Company, Angel Research

Outlook

We expect PARAG to report net revenue/PAT CAGR of 13%/27% respectively over

FY2018-20E driven by new product launch in VAP and reduction in interest cost.

When compared with its peers, its revenue growth is largely in line. However, due

to increasing share of VAP ( which is already highest among the listed players), its

margin expansion will also be highest in the industry in FY2020.

Exhibit 18: Peer financial comparison

Revenue (` cr)

CAGR %

EBITDA (` cr)

EBITDA Margin %

Company name

FY17

FY18

FY19

FY20

FY18

FY19

FY20

FY18 FY19

FY20

Hatsun Agro

4190

4790

5850

6837

17.7%

445

445

445

9.3%

7.6%

6.5%

Heritage Foods

2573

2593

3022

3521

11.0%

142

197

252

5.5%

6.5%

7.2%

Prabhat

1410

1599

1822

2082

13.9%

139

139

139

8.7%

7.6%

6.7%

Parag

1731

1957

2214

2498

13.0%

191

229

265

9.7%

10.4%

10.6%

Source: Bloomberg , Angel Research

Valuation

The stock currently trades at a P/E of 14.9x its FY2020E EPS which looks very

attractive, looking its stable growth trajectory. The company is increasingly

becoming a stable brand play while it is still valued as a commodity business. We

feel that the company should somewhere start enjoying the valuation of FMCG

companies. When compared with peers also, the company is trading at substantial

discount to most of its peers. Hence ,we initiate coverage on the stock with a BUY

recommendation and Target Price of `333 (20x FY2020E EPS), an upside of 34%

from the current levels.

April 16, 2018

10

Initiating coverage | Parag Milk Foods

Exhibit 19: Peer valuation comparison

(`)

EPS (`)

EPS CAGR %

P/E (x)

ROE (%)

CMP

FY17 FY18 FY19 FY20

FY18 FY19 FY20

FY17

FY18

FY19

FY20

Hatsun Agro

737

8.8

9.9

15.0

20.5

32.4

74.8

49.3

36.0

46.4

34.1

38.9

38.8

Heritage Foods

750

14.4

14.2

20.9

28.9

26.1

52.7

35.9

25.9

24.7

20.8

24.4

25.3

Prabhat Dairy

177

3.5

4.9

6.9

9.4

39.3

36.4

25.6

18.8

7.0

6.5

8.7

10.8

Parag Milk Foods

249

4.3

10.3

13.8

16.7

57.4

24.1

18.0

14.9

5.5

11.7

13.5

14.0

Source: Company, Angel Research

Exhibit 20: Forward PE chart

600.0

500.0

400.0

300.0

200.0

100.0

0.0

Closing price

10.0 X

15.0 X

20.0 X

25.0 X

30.0 X

Source: Company, Angel Research

Risks and concerns

Inability to procure sufficient good quality raw milk at commercially viable

prices may adversely impact the operation as milk is a key raw material for all

dairy products.

The dairy industry is highly competitive with multiple players sourcing milk

from the same region and price war. Such competition can have an impact on

raw milk prices.

The company is subject to various regulations relating to product liability,

particularly relating to food safety of its products. Product contamination or

similar occurrences can result in regulatory actions against the company and

impact the business performance.

April 16, 2018

11

Initiating coverage | Parag Milk Foods

Income statement

Y/E March (` cr)

FY2016

FY2017

FY2018E FY2019E FY2020E

Total operating income

1,645

1,731

1,957

2,214

2,498

% chg

13.9

5.2

13.1

13.1

12.9

Total Expenditure

1,497

1,642

1,767

1,984

2,233

Raw Material

1,333

1,414

1,520

1,710

1,924

Personnel

67

79

86

93

105

Selling and Administration Expenses

82.4

113.1

121.4

137.2

154.9

Others Expenses

15

36

39

44

50

EBITDA

148

89

191

229

265

% chg

38.2

(40.1)

114.7

20.3

15.4

(% of Net Sales)

9.0

5.1

9.7

10.4

10.6

Depreciation& Amortisation

33

49

54

59

65

EBIT

115

40

136

170

200

% chg

44.1

(65.3)

242.9

24.5

17.7

(% of Net Sales)

7.0

2.3

7.0

7.7

8.0

Interest & other Charges

50

33

24

18

13

Other Income

2

11

5

5

5

(% of PBT)

2.3

62.7

4.3

3.2

2.6

Share in profit of Associates

-

-

-

-

-

Recurring PBT

67

18

117

157

192

% chg

94.9

(73.8)

569.1

34.1

22.2

Tax

19

0

30

41

52

(% of PBT)

29.2

2.3

26.0

26.0

27.0

PAT (reported)

47

17

87

116

140

Extraordinary Items

(2)

(19)

-

-

-

Less: Minority interest (MI)

0

0

0

0

0

PAT after MI (reported)

47

17

87

116

140

ADJ. PAT

49

36

87

116

140

% chg

33.0

(27.2)

141.4

34.1

20.5

(% of Net Sales)

3.0

2.1

4.4

5.3

5.6

Fully Diluted EPS (`)

5.9

4.3

10.3

13.8

16.7

% chg

33.0

(27.2)

141.4

34.1

20.5

Source: Company, Angel Research

April 16, 2018

12

Initiating coverage | Parag Milk Foods

Balance sheet

Y/E March (` cr)

FY2016

FY2017

FY2018E FY2019E FY2020E

SOURCES OF FUNDS

Equity Share Capital

70

84

84

84

84

Reserves& Surplus

291

573

659

775

914

Shareholders Funds

362

657

743

859

998

Equity Share Warrants

-

-

-

-

-

Total Loans

389

262

212

162

112

Deferred Tax Liability

-

-

-

-

-

Other liabilties

18.7

18.1

18.1

18.1

18.1

Total Liabilities

769

938

974

1,039

1,129

APPLICATION OF FUNDS

Gross Block

528

585

645

705

765

Less: Acc. Depreciation

183

226

280

340

404

Net Block

345

359

365

365

361

Capital Work-in-Progress

28

21

21

21

21

Investments

-

-

-

-

-

Current Assets

602

878

916

1,004

1,120

Inventories

272

429

456

515

582

Sundry Debtors

236

215

241

273

308

Cash

8

101

68

45

38

Loans & Advances

85

133

151

171

193

Other Assets

-

-

-

-

-

Current liabilities

211

382

411

462

520

Net Current Assets

391

496

505

542

600

Deferred Tax Asset

(11)

(10)

(11)

(12)

(12)

Total Assets

769

938

974

1,039

1,129

Source: Company, Angel Research

April 16, 2018

13

Initiating coverage | Parag Milk Foods

Cash flow statement

Y/E March (` cr)

FY2016

FY2017

FY2018E FY2019E FY2020E

Profit before tax

67

18

117

157

192

Depreciation

33

49

54

59

65

Change in Working Capital

0

0

(42)

(60)

(65)

Interest / Dividend (Net)

47

25

24

18

13

Direct taxes paid

(14)

(16)

(30)

(41)

(52)

Others

(75)

(11)

0

0

0

Cash Flow from Operations

59

64

123

134

152

(Inc.)/ Dec. in Fixed Assets

(27)

(97)

(60)

(60)

(60)

(Inc.)/ Dec. in Investments

(4)

6

(22)

(28)

(37)

Cash Flow from Investing

(31)

(91)

(82)

(88)

(97)

Issue of Equity

6

278

0

0

0

Inc./(Dec.) in loans

60

0

(50)

(50)

(50)

Dividend Paid (Incl. Tax)

0

0

0

0

0

Interest / Dividend (Net)

(55)

(31)

(24)

(18)

(13)

Cash Flow from Financing

(26)

123

(74)

(68)

(63)

Inc./(Dec.) in Cash

1

96

(33)

(22)

(7)

Opening Cash balances

4

5

101

68

45

Closing Cash balances

5

101

68

45

38

Source: Company, Angel Research

April 16, 2018

14

Initiating coverage | Parag Milk Foods

Key Ratios

Y/E March

FY2016

FY2017

FY2018E

FY2019E

FY2020E

Valuation Ratio (x)

P/E (on FDEPS)

42.4

58.3

24.1

18.0

14.9

P/CEPS

26.0

31.7

14.9

11.9

10.2

P/BV

5.8

3.2

2.8

2.4

2.1

Dividend yield (%)

0.1

0.2

0.0

0.0

0.0

EV/Sales

1.5

1.3

1.1

1.0

0.9

EV/EBITDA

16.7

25.4

11.7

9.6

8.2

EV / Total Assets

3.2

2.4

2.3

2.1

1.9

Per Share Data (`)

EPS (fully diluted)

5.9

4.3

10.3

13.8

16.7

Cash EPS

9.6

7.9

16.7

20.9

24.4

DPS

0.2

0.4

0.1

0.1

0.1

Book Value

43.0

78.2

88.4

102.1

118.7

Dupont Analysis

EBIT margin

7.0

2.3

7.0

7.7

8.0

Tax retention ratio

0.7

1.0

0.7

0.7

0.7

Asset turnover (x)

2.2

2.1

2.2

2.3

2.3

ROIC (Post-tax)

10.9

4.8

11.4

12.9

13.6

Cost of Debt (Post Tax)

0.1

0.1

0.1

0.1

0.1

Returns (%)

ROCE

15.3

4.3

14.3

16.6

18.0

Angel ROIC (Pre-tax)

15.5

4.9

15.4

17.4

18.7

ROE

13.6

5.5

11.7

13.5

14.0

Turnover ratios (x)

Asset Turnover (Gross Block)

3.1

3.0

3.0

3.1

3.3

Inventory / Sales (days)

60

90

85

85

85

Receivables (days)

52

45

45

45

45

Payables (days)

58

99

99

99

99

Working capital cycle (ex-cash) (days)

55

37

31

31

31

Solvency ratios (x)

Net debt to equity

1.1

0.2

0.2

0.1

0.1

Net debt to EBITDA

2.6

1.8

0.8

0.5

0.3

Interest Coverage (EBIT / Interest)

2.3

1.2

5.6

9.5

15.3

Source: Company, Angel Research; Note: closing price of April 13 , 2018

April 16, 2018

15

Initiating coverage | Parag Milk Foods

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager and Investment Adviser with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking

Private Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide

registration number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory

authority for accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or

co-managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Parag Milk Foods Ltd.

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

April 16, 2018

16