3QFY2016 Result Update | Plastic Products

February 1, 2016

Nilkamal

NEUTRAL

CMP

`1,346

Performance Update

Target Price

-

Y/E March (` cr)

3QFY2016 3QFY2015

% chg (yoy) 2QFY2016

% chg (qoq)

Investment Period

-

Net sales

428

421

1.8

482

(11.0)

Stock Info

EBITDA

46

31

49.2

50

(7.6)

Sector

Plastic Products

EBITDA margin (%)

10.8

7.4

345bp

10.4

40bp

Market Cap (` cr)

1,749

Net debt (` cr)

173

Adjusted PAT

20

8

138.6

26

(21.6)

Beta

1.5

Source: Company, Angel Research

52 Week High / Low

1,631 / 375

Nilkamal (NILK) reported an in-line set of numbers for 3QFY2016. The top-line

Avg. Daily Volume

32,319

Face Value (`)

10

reported a modest growth of 1.8% yoy to `428cr. The raw material cost as a

percentage of sales declined by 738bp yoy to 54.8% owing to declining in

BSE Sensex

24,871

polymer prices. However, the employee cost and other expenses increased by

Nifty

7,564

Reuters Code

NKML.BO

176bp yoy and 217bp yoy to 8.6% of sales and 25.8% of sales, respectively, thus

Bloomberg Code

NILK IN

partially offsetting the benefits of lower raw material costs. The EBITDA margin

expanded by 345bp yoy to 10.8%. Aided by lower raw material cost and lower

interest outgo, the net profit grew by 138.6% yoy to `20cr.

Shareholding Pattern (%)

Promoters

64.1

Plastics division to benefit from revival in economy: After witnessing volume

de-growth in FY2014, the Plastics division witnessed volume growth of 10% in

MF / Banks / Indian Fls

1.6

FY2015 and is estimated to have posted a volume growth of ~5% for 9MFY2016.

FII / NRIs / OCBs

3.6

With the fourth quarter tending to be the best in terms of volume, the growth for

Indian Public / Others

30.6

FY2016E is likely to be ~7%. Material Handling and Moulded Furniture segments

of the Plastics division are directly impacted by the macro environment and we

Abs.(%)

3m 1yr

3yr

expect them to maintain steady growth rate due to the positive economic outlook. The

Sensex

(7.3)

(16.2)

24.4

company has sufficient capacity in place and we do not foresee any substantial capex in

NILK

31.0

191.0

528.2

the near future.

Stable raw material cost to aid in maintaining margins: Polymer prices declined

3 year daily price chart

by ~16% in 3QFY2016 on a yoy basis, thus leading to lower raw material costs.

1,800

With crude likely to be range bound, we expect polymer prices to remain at current

1,600

1,400

levels and increase by ~5% from here on, which should enable NILK in maintaining

1,200

its margins over FY2016E-2018E.

1,000

800

Outlook and Valuation: We expect the company’s Plastics business to post a

600

400

CAGR of 8.3%, with an upturn in the economy, over FY2015-2018, which will aid

200

the company to post revenue CAGR of 7.5%, over the same period, to `2,220cr.

-

The EBITDA margin is expected to be at 10.3% in FY2018E. The company is

expected to be net debt free by FY2018E which will lead to higher profitability.

Consequently, the company would more than double its PAT to `116cr in FY2018E

Source: Company, Angel Research

from `42cr in FY2015, as per our estimates. At the current market price, the stock is

trading at FY2018E PE of 17.3x. We have a Neutral rating on the stock.

Financials (Standalone)

Y/E

Sales OPM PAT EPS RoE P/E P/BV EV/BITDA

EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2016E

1,871

10.7

94

63.2

17.6

21.3

3.5

10.5

1.1

Milan Desai

FY2017E

2,031

10.5

104

69.8

16.6

19.3

3.0

9.5

1.0

022-4000 3600 Ext.: 6846

FY2018E

2,220

10.3

116

78.0

15.9

17.3

2.6

8.4

0.9

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Nilkamal | 3QFY2016 Result Update

Exhibit 1: 3QFY2016 performance

Y/E March (` cr)

3QFY16

3QFY15

yoy chg (%)

2QFY16

qoq chg (%)

9MFY16

9MFY15

% chg

Net Sales

428

421

1.8

482

(11.0)

1,367

1,296

5.5

Net raw material

235

262

(10.3)

282

(16.6)

786

828

(5.1)

(% of Sales)

54.8

62.2

(738)bp

58.5

(366)bp

57.5

63.8

(638)bp

Staff Costs

37

29

28.1

32

13.2

100

84

18.8

(% of Sales)

8.6

6.8

176bp

6.7

183bp

7.3

6.5

83bp

Other Expenses

110

99

11.1

117

(5.8)

333

294

13.2

(% of Sales)

25.8

23.6

217bp

24.3

143bp

24.3

22.7

165bp

Total Expenditure

382

390

(2.0)

431

(11.4)

1,219

1,206

1.1

Operating Profit

46

31

49.2

50

(7.6)

149

90

64.7

OPM

10.8

7.4

345bp

10.4

40bp

10.9

7.0

390bp

Interest

4

9

(53.2)

4

(8.1)

13

24

Depreciation

12

14

(11.2)

13

(3.1)

37

42

(10.8)

Other Income

0.2

2.8

(93.7)

3.8

(95.3)

6

4

49.4

PBT

30

12

162.1

37

(18.0)

105

29

12.6

(% of Sales)

7.1

2.8

7.7

7.6

2.2

Tax

10

3

11

33

8

(% of PBT)

33.6

27.1

30.6

31.1

29.3

Reported PAT

20

8

138.6

26

(21.6)

71

21

242.9

PATM

4.7

2.0

5.3

5.2

1.6

Source: Company, Angel Research

Exhibit 2: Actual vs. Angel estimates (3QFY2016)

Actual (` cr)

Estimate (` cr)

Var (%)

Total Income

428

456

(6.0)

EBIDTA

46

46

0.8

EBIDTA margin (%)

10.8

10.1

74bp

Adjusted PAT

20

21

(2.6)

Source: Company, Angel Research

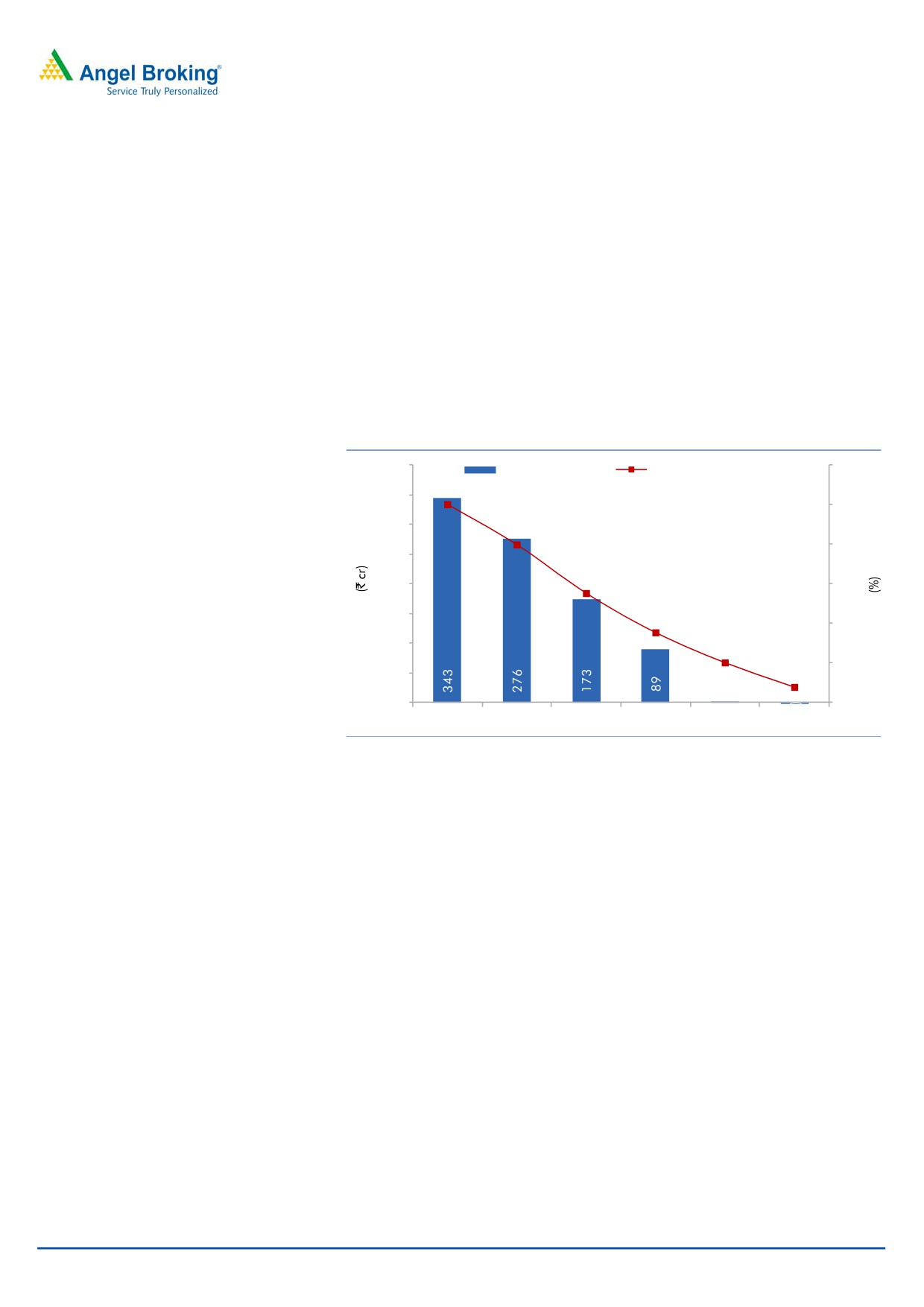

Top-line below expectation, EBITDA and Net Profit in-line

NILK’s standalone top-line line grew by 1.8% yoy to `428cr, which is below our

estimate of `456cr. As per the Management, the Plastics division witnessed a

volume de-growth of ~1% on a yoy basis in 3QFY2016 and as a result both

Material Handling and Moulded Furniture businesses are likely to have

experienced flattish volumes during the quarter.

February 1, 2016

2

Nilkamal | 3QFY2016 Result Update

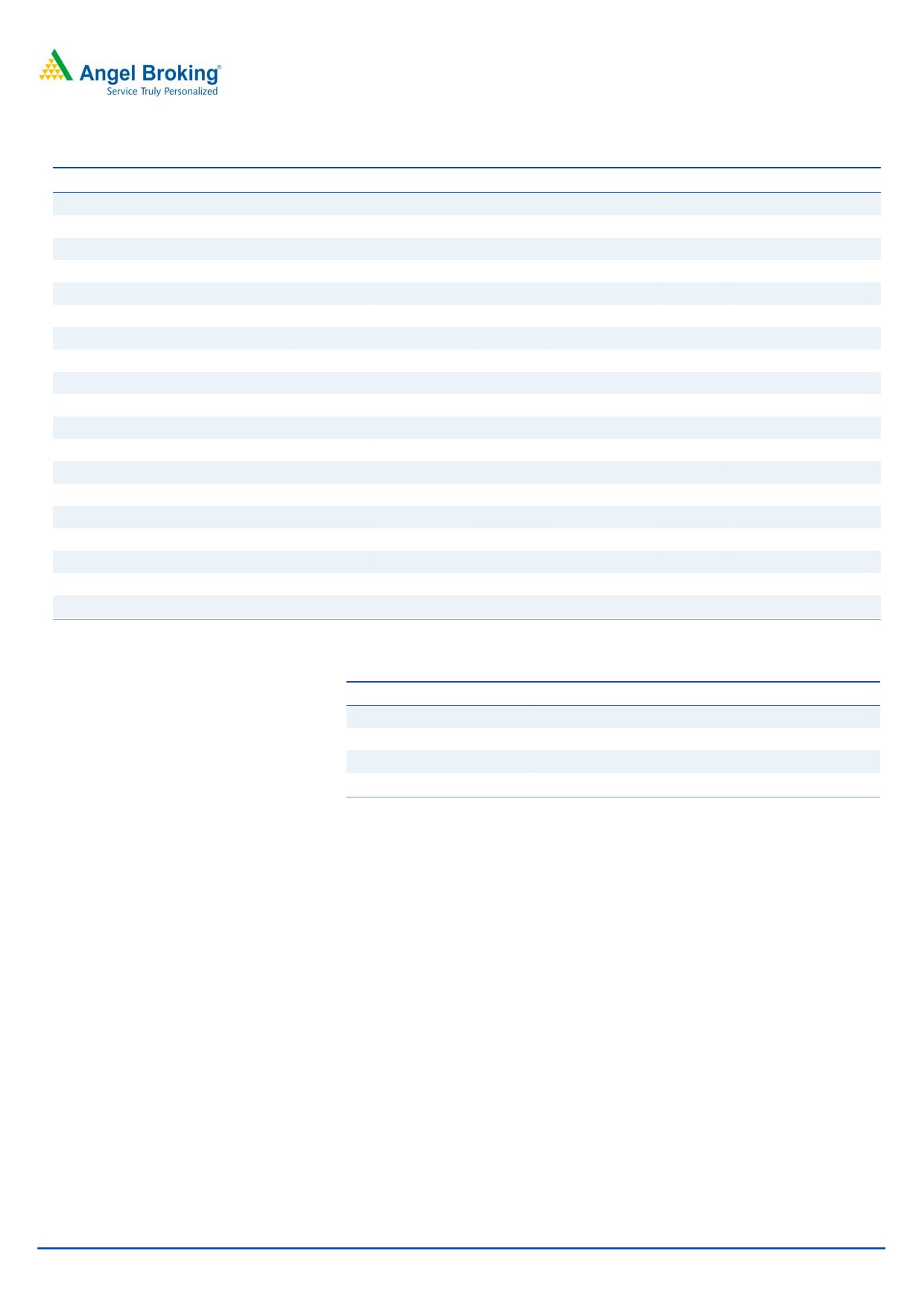

Exhibit 3: yoy revenue growth subtle due to flattish volumes

11.2

600

12.0

9.6

8.3

10.0

500

7.0

8.0

400

6.5

5.1

6.0

4.2

4.0

300

2.0

1.

8

200

-

(2.0)

100

(4.0)

(3.6)

-

(6.0)

Revenue (LHS)

yoy growth (RHS)

Source: Company, Angel Research

Aided by a sharp decline in raw material prices, the EBITDA grew by an impressive

49.2% yoy to `46cr, which is in-line with our estimate. As per our reckoning,

average polyethylene prices declined by 15.7% on a yoy basis (7.8% decline on a

qoq basis) during the quarter resulting in raw material costs declining by 738bp

yoy to 54.8% of sales. However, the employee cost and other expenses increased

by 176bp yoy and 217bp yoy to 8.6% and 25.8% of sales, respectively.

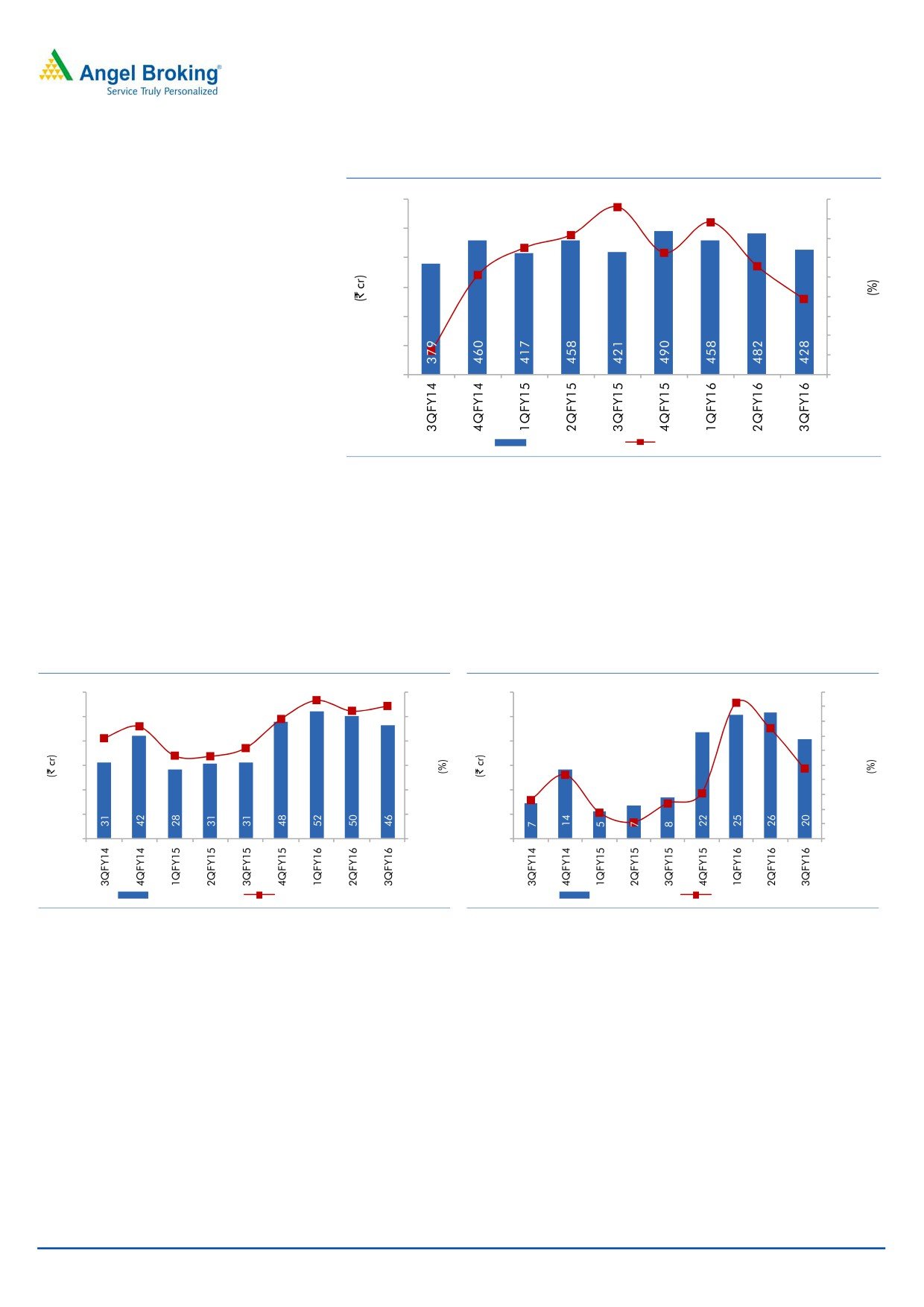

Exhibit 4: Lower RM leads to Margin expansion...

Exhibit 5: ... and bottom-line growth

11.3

10.8

362.8

60

10.4

12.0

30

400.0

9.8

9.2

276.1

350.0

50

10.0

25

8.2

300.0

7.4

138.6

40

6.8

6.7

8.0

20

250.0

200.0

116.8

30

6.0

15

150.0

100.0

30.5

19.0

20

4.0

10

(12.4)

(45.5)

53.6

50.0

-

10

2.0

5

(50.0)

-

-

-

(100.0)

EBITDA (LHS)

EBITDA Margin (RHS)

PAT (LHS)

yoy growth (RHS)

Source: Company, Angel Research

Source: Company, Angel Research

The EBITDA margin expanded by 345bp yoy to 10.8% against our estimate of

10.1%. The company has been continuously reducing its debt over the past six

quarters and as result, the interest cost declined by 53.2% yoy to `4cr. Aided by a

better operational performance and lower interest outgo, the net profit grew by

138.6% yoy to `20cr which is in-line with our estimate of `21cr.

February 1, 2016

3

Nilkamal | 3QFY2016 Result Update

Exhibit 6: Segment wise performance

Y/E March (` cr)

3QFY16

3QFY15

% chg (yoy) 2QFY16

% chg (qoq)

Total Revenue

A) Plastics

365

364

0.3

409

(10.8)

B) Lifestyle

60

53

13.4

68

(12.0)

C) Others

9

8

9.4

8

5.1

Total

433

424

2.1

485

(10.7)

Less: Inter-Segmental Rev.

4

3

4

Net Sales

430

421

2.1

482

(10.7)

Segmental Profit

A) Plastics

45

21

109.6

45

(1.2)

B) Lifestyle

(2)

(1)

46.2

1

(267.9)

C) Others

(0.8)

0

(257.6)

(1)

(3.0)

Segmental Margin (%)

A) Plastics

12.3

5.9

641bp

11.1

120bp

B) Lifestyle

(2.9)

(2.2)

(65)bp

1.5

(441)bp

C) Others

(8.6)

6.0

(1460)bp

(9.3)

72bp

Source: Company, Angel Research

As far as segmental performance is concerned, the Plastics division witnessed a

0.3% yoy revenue growth to `365cr and the margins for the segment improved by

641bp yoy to 12.3%. As of 9MFY2016, the Plastics division is estimated to have

posted volume growth of ~5.7%.

The Lifestyle segment’s revenues grew by 13.4% yoy to `60cr while the segment

reported a loss of `2cr for the quarter. Others, which includes the Mattress

business, saw a revenue growth of 9.4% on a yoy basis to `9cr while the segment

reported a loss of `0.8cr for the quarter.

February 1, 2016

4

Nilkamal | 3QFY2016 Result Update

Investment Arguments

Plastics division to benefit from revival in Economy

The Plastics business, accounting for ~86% of the company’s total revenue, is the

primary business of the company. Owing to a poor macro environment, the

division had witnessed volume de-growth in FY2014. However, it rebounded well

in FY2015, posting a volume growth of 10% and it has posted volume growth of

~5% in 9MFY2016 (4Q tends to be the best quarter in terms of volumes). We

expect both the segments of the division, viz Material Handling and Moulded

Furniture, to benefit from an expected improvement in the macro conditions in the

country.

The Material Handling segment is B2B in nature and is an important part of

industrial activity. NILK is a ’One Stop Shop’ for material handling solutions, with

the company being the largest manufacturer of plastic crates and other products

like pallets, metal storage racks, and material handling equipment for various

industries. As per an industry report, Supreme Industries, which is the second

largest Material Handling player, is very small compared to NILK in terms of size

of its Material Handling business with revenue of ~`240cr against ~`900cr for

NILK.

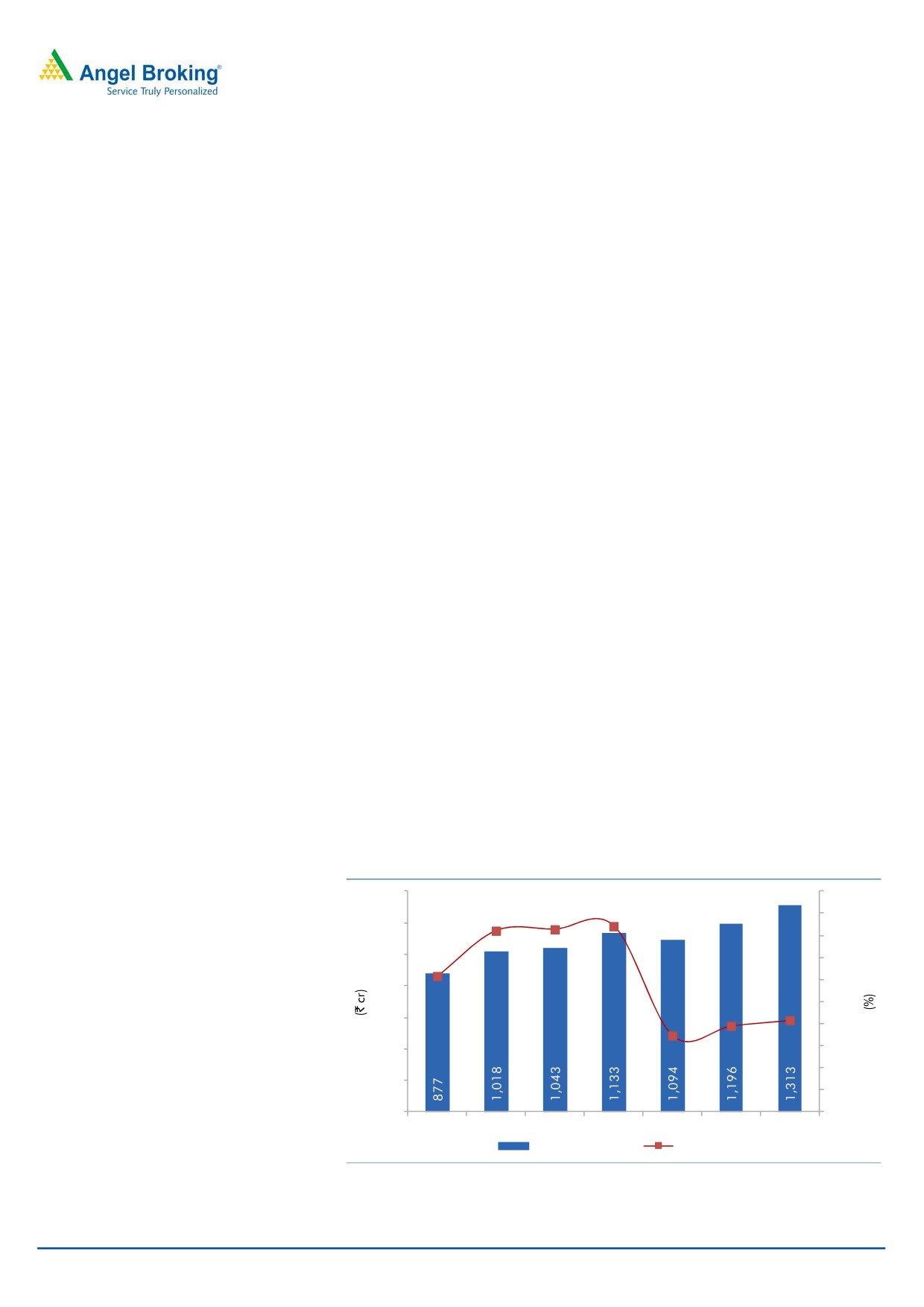

Stable raw material prices to lead to sustainable margins going

ahead

Tracing the decline in crude prices, polymer (the main raw material for the plastic

industry) prices have declined as well, thereby improving margins of plastic

products manufactures. The price of crude has corrected significantly from

US$112/barrel in July 2014 to the current level of US$33/barrel; down by ~71%

during the period. This correction has resulted in average polyethylene prices

declining by

~26% over the same period. Going forward, crude as well

as polyethylene prices are expected to stabilize or surge by

~3-5% over

FY2016E-18E.

Exhibit 7: Stable RM prices to help margins

1,400

65.0

63.2

63.3

64.0

1,200

63.4

63.0

1,000

62.0

61.1

61.0

800

60.0

58.9

59.1

600

58.5

59.0

400

58.0

57.0

200

56.0

-

55.0

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E FY2018E

Net Raw Material

As % of Sales

Source: Company, Angel Research

February 1, 2016

5

Nilkamal | 3QFY2016 Result Update

Strong Balance Sheet

NILK’s balance sheet is stress free with its net-debt/equity maintained below the

1.0x mark over the past three years. The debt level of the company has declined

significantly in FY2015 and the company continues to further reduce the overall

debt. The benefits of this are evident in the decline in interest expense over the past

three quarters which are adding directly to the bottom-line. As on FY2015, the net

debt to equity stood at 0.4x; with the current reduction in loans we expect the same

to decline to 0.2x level by FY2016E and be net debt free by FY2018E.

The asset turnover (Gross Block) is expected to increase from 2.5x in FY2015 to

2.8x in FY2018E due to sales CAGR of 7.5% over FY2015-18E and gross block

CAGR of 4.0%.

Exhibit 8: Net debt to equity to decline

400

1.0

Net Debt (LHS)

Net debt to equity (RHS)

350

0.8

0.8

300

0.6

0.6

250

200

0.4

0.4

150

0.2

0.2

100

0.0

-

50

(0.1)

-

(0.2)

FY2013

FY2014

FY2015E FY2016E FY2017E FY2018E

Source: Company, Angel Research

February 1, 2016

6

Nilkamal | 3QFY2016 Result Update

Financials

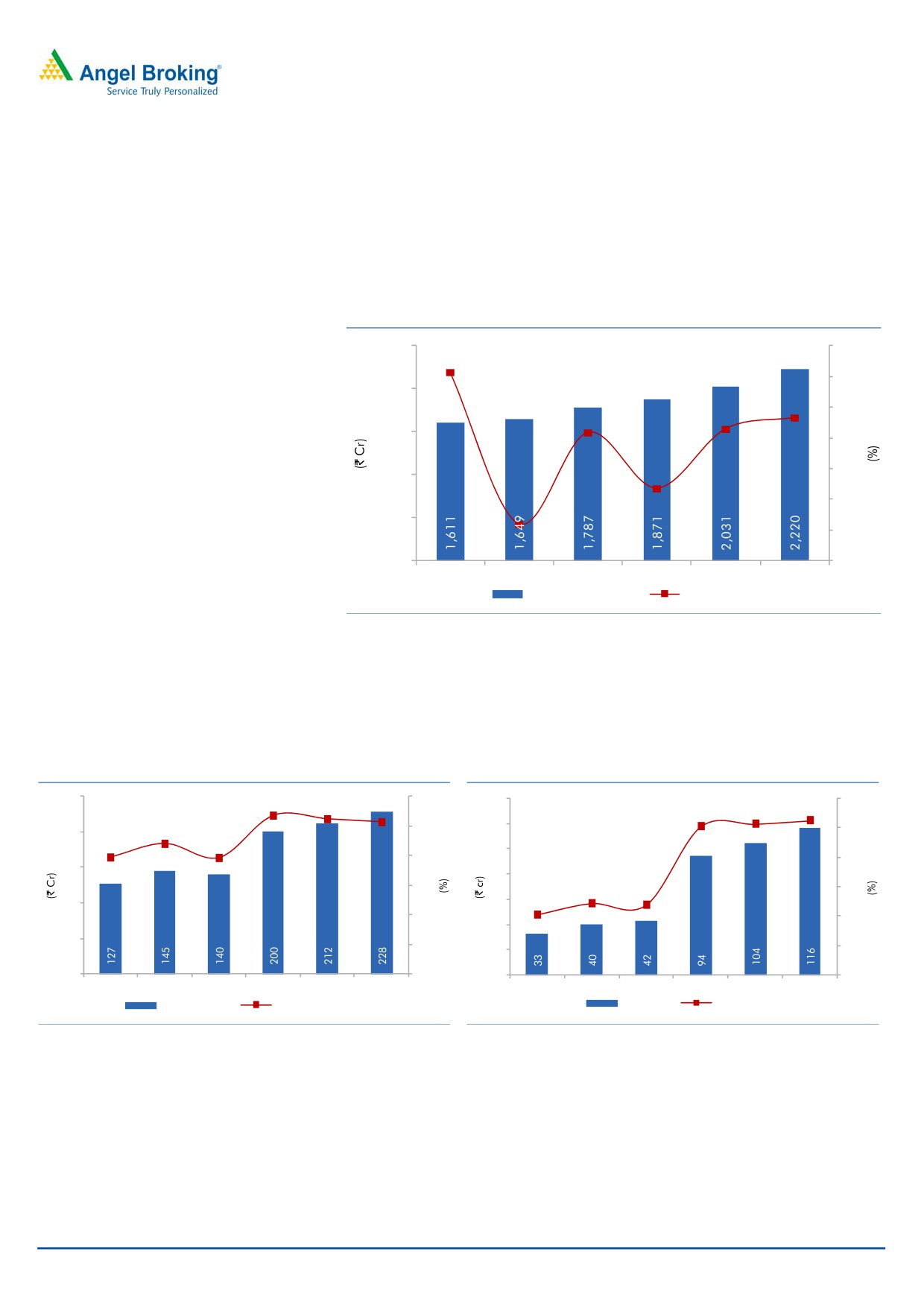

Revival in Indian economy to aid revenue growth

We are estimating the company’s Plastics division to post a revenue CAGR of 8.3%

over FY2015E-18E resulting in the overall top-line registering a CAGR of 7.5%

over FY2015-2018E to `2,220cr in FY2017E.

Exhibit 9: Revenue to improve by 7.5% CAGR over FY2015-17E

2,500

14.0

12.3

12.0

2,000

9.3

8.6

10.0

8.3

1,500

8.0

6.0

1,000

4.7

4.0

500

2.4

2.0

-

0.0

FY2013

FY2014

FY2015

FY2016E FY2017E FY2018E

Revenue (LHS)

Growth (RHS)

Source: Company, Angel Research

We expect the EBITDA margin to improve by 241bp over FY2015-2018E to 10.3%.

The company continues to reduce its debt level and is expected to be net debt free

by FY2018E and as a result, its bottom-line in our view should more than double

to `116cr in FY2018E from `42cr in FY2015.

Exhibit 10: EBITDA margin to rebound

Exhibit 11: PAT trajectory

250

10.7

12.0

140

6.0

10.5

10.

3

5.0

5.1

5.2

8.8

10.0

120

5.0

200

7.9

7.8

100

8.0

4.0

150

80

6.0

3.0

2.4

60

100

2.0

4.0

2.4

2.0

40

50

2.0

1.0

20

0

0.0

0

0.0

FY2013

FY2014

FY2015

FY2016E FY2017E FY2018E

FY2013

FY2014

FY2015

FY2016E FY2017E FY2018E

EBITDA (LHS)

EBITDA Margin (RHS)

PAT (LHS)

PATM (RHS)

Source: Company, Angel Research

Source: Company, Angel Research

February 1, 2016

7

Nilkamal | 3QFY2016 Result Update

Exhibit 12: Relative valuation (Trailing twelve months)

Company

Mcap

Sales

OPM

PAT

EPS

RoE

P/E

P/BV

EV/BITDA

EV/Sales

(` cr)

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

Nilkamal

2,008

1,866

10.6

93

62.3

16.5

21.6

3.6

10.4

1.1

Supreme Industries

9,393

4,211

16.7

347

27.3

29.0

27.0

7.9

13.7

2.3

Source: Company, Angel Research

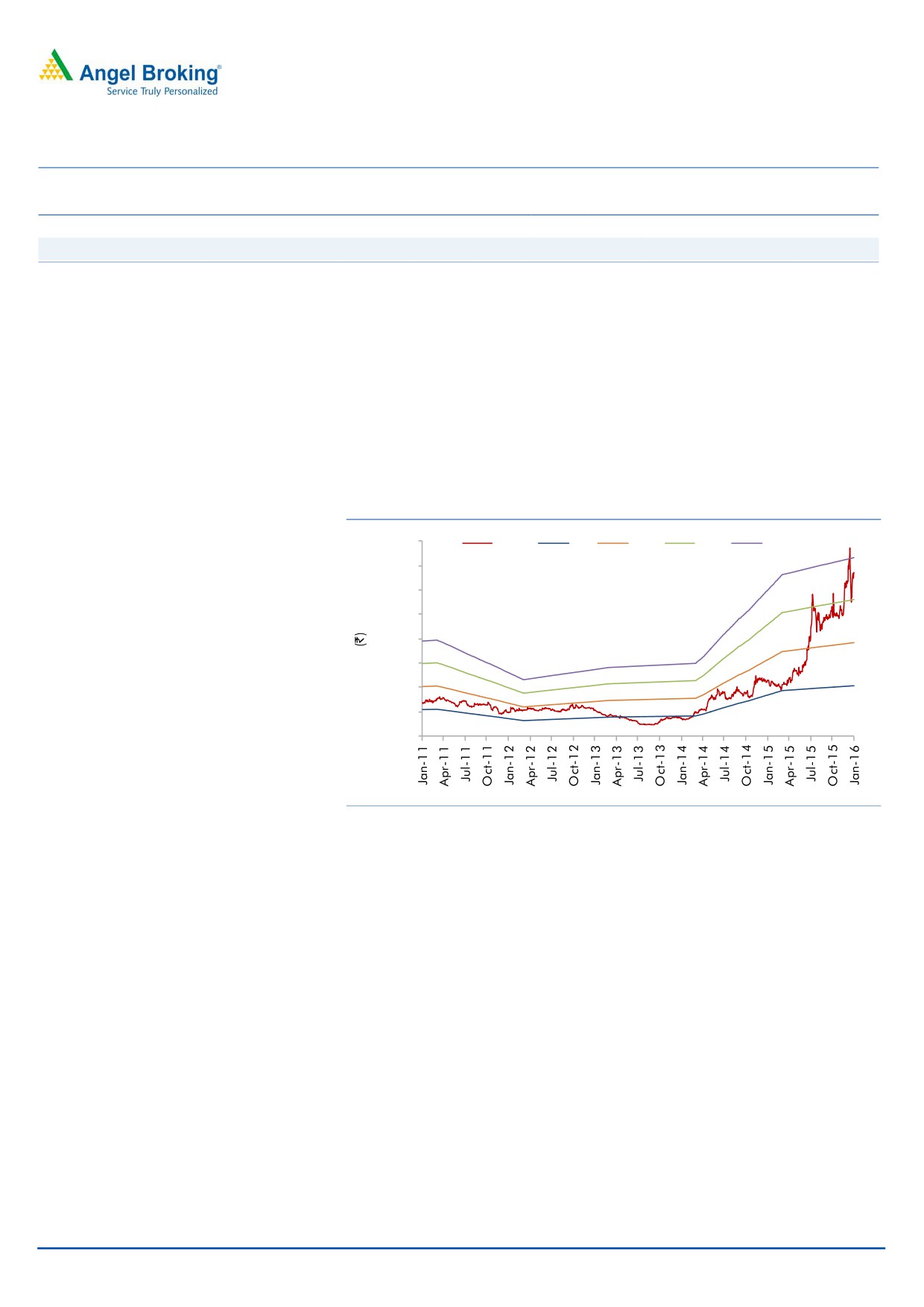

Outlook and Valuation

We expect the Material Handling segment of the Plastics division to be the main

beneficiary from an expected up-turn in the economy. We have built in a revenue

CAGR of 7.5% over FY2015-18E to `2,220cr. The EBITDA margin is expected to

be at 10.3% in FY2018E and the net profit is expected to be at `1161cr in

FY2018E. At the current market price, the stock is trading at FY2018E PE of 17.3x.

We have a Neutral rating on the stock.

Exhibit 13: One-year forward PE chart

1,600

Price

6x

11x

16x

21x

1,400

1,200

1,000

800

600

400

200

-

Source: Company, Angel Research

Concerns

Volatile raw material prices: Raw materials account for 63% of net sales. High

volatility in crude and raw material prices could have a negative impact on the

company’s performance.

Economic slowdown: Economic slowdown will have a negative impact on the

performance of the company as both plastics and @home are dependent on the

economic scenario.

Competition from the unorganized segment: Availability of low priced furniture

from the unorganized segment poses a threat as it is able to undercut prices by

compromising on quality.

February 1, 2016

8

Nilkamal | 3QFY2016 Result Update

Exhibit 14: Crude and Polypropylene price fluctuation

130

8,500

120

7,500

110

6,500

100

90

5,500

80

86

4,500

70

3,500

60

2,500

50

2,469

40

1,500

Avg Polyethylene Prices (LHS)

Brent Prices INR (RHS)

Source: Company, Angel Research

Company background

Incorporated in 1985, Nilkamal Ltd (NILK) is a market leader in moulded plastic

products. The company has three divisions, viz Plastics, Lifestyle Furniture, &

Furnishings and Accessories. The products of these divisions are sold through the

company’s retail chain “@home”; further, the company has recently forayed into

the mattress business. The company’s manufacturing plants are located at Barjora

in West Bengal, Hosur in Tamil Nadu, Jammu, Kharadapada and Vasona in

Dadra & Nagar Haveli, Noida in UP, Sinnor and Nashik in Maharashtra and in

Pudducherry.

NILK is a market leader in the Material Handling segment, backed by its ability to

directly reach a very diverse set of industrial customers through

400+

self-employed sales people operating from 39 regional sales offices across India.

The Moulded Furniture segment of the company enjoys a ~39% market share in its

category. NILK has 26 small format stores along with a strong network of 40+

depots and 1000+ channel partners on a pan India basis, thus enabling it to serve

the remotest rural markets. Its retail store chain

“@home”, operates

18 stores across 13 cities covering a retail space of over 3.15 lakh sq. ft.

February 1, 2016

9

Nilkamal | 3QFY2016 Result Update

Profit and loss statement (standalone)

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

FY2018E

Total operating income

1,649

1,787

1,871

2,031

2,220

% chg

2.4

8.3

4.7

8.6

9.3

Net Raw Materials

1,043

1,133

1,094

1,196

1,313

% chg

2.5

8.6

(3.5)

9.4

9.8

Power and Fuel

40

41

45

49

51

% chg

(15.8)

3.4

9.8

8.6

4.8

Personnel

105

113

136

146

160

% chg

3.7

7.2

20.1

7.8

9.3

Other

316

360

397

428

468

% chg

(0.4)

14.0

10.2

7.8

9.6

Total Expenditure

1,504

1,647

1,671

1,819

1,993

EBITDA

145

140

200

212

228

% chg

14.3

(3.4)

42.9

6.2

7.2

(% of Net Sales)

8.8

7.8

10.7

10.5

10.3

Depreciation & Amortisation

49

54

50

54

56

EBIT

96

86

150

158

172

% chg

16.5

(10.2)

73.5

5.9

8.3

(% of Net Sales)

5.8

4.8

8.0

7.8

7.7

Interest & other Charges

41

32

20

15

12

Other Income

4

6

9

10

12

(% of Net Sales)

0.2

0.3

0.5

0.5

0.5

Recurring PBT

55

54

130

143

159

% chg

38.3

(0.6)

138.6

10.3

11.3

PBT (reported)

58

61

139

153

171

Tax

18

18

44

49

55

(% of PBT)

31.1

29.8

32.0

32.0

32.0

PAT (reported)

40

42

94

104

116

Extraordinary Expense/(Inc.)

-

-

-

-

-

ADJ. PAT

40

42

94

104

116

% chg

21.7

6.1

122.1

10.4

11.8

(% of Net Sales)

2.4

2.4

5.0

5.1

5.2

Basic EPS (`)

26.8

28.5

63.2

69.8

78.0

Fully Diluted EPS (`)

26.8

28.5

63.2

69.8

78.0

% chg

21.7

6.1

122.1

10.4

11.8

Dividend

7

8

8

8

8

Retained Earning

33

35

87

96

109

February 1, 2016

10

Nilkamal | 3QFY2016 Result Update

Balance sheet (Standalone)

Y/E March (`cr)

FY2014

FY2015

FY2016E

FY2017E

FY2018E

SOURCES OF FUNDS

Equity Share Capital

15

15

15

15

15

Reserves& Surplus

448

478

564

660

769

Shareholders’ Funds

463

492

579

675

784

Total Loans

320

207

163

136

109

Other Long Term Liabilities

33

37

37

37

37

Long Term Provisions

7

7

7

7

7

Deferred Tax (Net)

24

16

16

16

16

Total Liabilities

847

759

802

871

953

APPLICATION OF FUNDS

Gross Block

717

716

745

774

805

Less: Acc. Depreciation

385

432

483

537

593

Less: Impairment

-

-

-

-

-

Net Block

333

284

262

238

213

Capital Work-in-Progress

2

1

1

1

1

Investments

26

26

26

26

26

Long Term Loans and adv.

56

52

52

52

52

Other Non-current asset

0

1

1

1

1

Current Assets

579

557

617

724

848

Cash

18

8

48

108

175

Loans & Advances

43

40

41

42

43

Inventory

301

277

292

319

351

Debtors

218

232

235

255

279

Other current assets

-

-

-

-

-

Current liabilities

149

161

158

171

188

Net Current Assets

430

395

459

553

660

Misc. Exp. not written off

-

-

-

-

-

Total Assets

847

759

802

871

953

February 1, 2016

11

Nilkamal | 3QFY2016 Result Update

Cash flow statement (Standalone)

Y/E March (`cr)

FY2014

FY2015

FY2016E FY2017E FY2018E

Profit before tax

58

61

139

153

171

Depreciation

49

54

50

54

56

Change in Working Capital

28

25

(24)

(34)

(40)

Direct taxes paid

(18)

(27)

(44)

(49)

(55)

Others

(4)

(6)

(9)

(10)

(12)

Cash Flow from Operations

113

106

112

114

120

(Inc.)/Dec. in Fixed Assets

(34)

2

(29)

(30)

(31)

(Inc.)/Dec. in Investments

(0)

0

0

0

0

(Incr)/Decr In LT loans & adv.

(5)

4

-

-

-

Others

4

6

9

10

12

Cash Flow from Investing

(36)

12

(19)

(20)

(19)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

(74)

(109)

(44)

(27)

(26)

Dividend Paid (Incl. Tax)

(7)

(8)

(8)

(8)

(8)

Others

(3)

(11)

-

-

-

Cash Flow from Financing

(84)

(128)

(52)

(35)

(34)

Inc./(Dec.) in Cash

(7)

(10)

40

59

67

Opening Cash balances

25

18

8

48

108

Closing Cash balances

18

8

48

108

175

February 1, 2016

12

Nilkamal | 3QFY2016 Result Update

Key Ratios (Standalone)

Y/E March

FY2014

FY2015

FY2016E

FY2017E

FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

50.2

47.3

21.3

19.3

17.3

P/CEPS

22.6

20.9

13.9

12.7

11.6

P/BV

4.3

4.1

3.5

3.0

2.6

Dividend yield (%)

0.3

0.4

0.4

0.4

0.4

EV/Net sales

1.4

1.2

1.1

1.0

0.9

EV/EBITDA

15.8

15.6

10.5

9.5

8.4

EV / Total Assets

2.8

2.9

2.7

2.4

2.0

Per Share Data (`)

EPS (Basic)

26.8

28.5

63.2

69.8

78.0

EPS (fully diluted)

26.8

28.5

63.2

69.8

78.0

Cash EPS

59.6

64.5

97.0

105.9

115.6

DPS

4.6

4.5

4.5

4.5

4.5

Book Value

310.1

330.0

388.0

452.6

525.4

DuPont Analysis

EBIT margin

5.8

4.8

8.0

7.8

7.7

Tax retention ratio

0.7

0.7

0.7

0.7

0.7

Asset turnover (x)

2.1

2.4

2.6

2.8

3.0

ROIC (Post-tax)

8.3

8.1

14.3

15.1

16.0

Cost of Debt (Post Tax)

8.0

8.5

7.4

7.1

6.9

Leverage (x)

0.6

0.4

0.2

0.0

(0.1)

Operating ROE

8.6

8.0

15.4

15.1

15.0

Returns (%)

ROCE (Pre-tax)

11.4

11.0

19.6

19.3

19.1

Angel ROIC (Pre-tax)

12.1

11.6

21.1

22.1

23.6

ROE

9.0

8.9

17.6

16.6

15.9

Turnover ratios (x)

Asset TO (Gross Block)

2.4

2.5

2.6

2.7

2.8

Inventory / Net sales (days)

67

59

56

55

55

Receivables (days)

50

46

46

46

46

Payables (days)

36

34

34

34

34

WC cycle (ex-cash) (days)

94

82

78

77

77

Solvency ratios (x)

Net debt to equity

0.6

0.4

0.2

0.0

(0.1)

Net debt to EBITDA

1.9

1.2

0.4

0.0

(0.4)

Int. Coverage (EBIT/ Int.)

2.3

2.7

7.4

10.2

13.8

February 1, 2016

13

Nilkamal | 3QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Nilkamal

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

February 1, 2016

14