IPO Note | Media

March 1, 2017

Music Broadcast Limited

SUBSCRIBE

sue Open: March 06, 2017

Is

Playing the growth tune

Issue Close: March 08, 2017

Music Broadcast Limited (MBL) owns and operates FM radio stations under the

brand names Radio City and Radio Mantra. MBL has 39 radio stations and

operates in 37 Indian cities. The company has a strong listenership base in cities

Issue Details

like Mumbai, Delhi and Bangalore. Moreover it also has presence in the Internet

Radio Space with PlanetRadioCity.com - 40 web radio stations in 8 languages.

Face Value: `10

Strong leadership position in large markets: Radio City is ranked No. 1 in terms

Present Eq. Paid up Capital: `45.0cr

of number of listeners, total 49.6mn listeners across top 23 cities (according to a

survey conducted by AZ Research), whereas, its competitor, Entertainment

Offer for Sale: **0.26cr Shares

Network India Ltd (ENIL) is at 2nd place with 40.5mn listeners. Even in the metro

cities like Mumbai, Bangalore and Delhi, MBL enjoys a leadership position.

Fresh issue: `400 cr

Ability to charge premium advertising rates: Radio City’s wide listenership despite

Post Eq. Paid up Capital: `57cr

operating fewer stations has enabled the company to charge ~30% higher

advertising rates than its peers and 12-15% higher charges than its closest peer.

Issue size (amount): *`486cr -**489 cr

Owing to this, Radio City enjoys healthy 34% operating margin, much better than

ENIL’s ~30% margin in FY2016.

Price Band: `324-333

Volume growth outperforms peers as well as Industry: Radio City’s advertising

volumes have grown at a CAGR of ~12.5% over FY2011-16, while, ENIL

Lot Size: 45 shares and in multiple

reported ~9% CAGR in advertising volumes during the same period. Radio City’s

thereafter

advertising volumes have witnessed higher growth (CAGR of 10.4% over the

Post-issue implied mkt. cap: *`1,859cr -

same period) than the industry due to its higher listenership.

**`1,900cr

Higher revenue share despite operating lesser radio markets: Radio City operates

Promoters holding Pre-Issue: 96%

20 markets, while ENIL operates a total of 38 markets. Despite this, Radio City

Promoters holding Post-Issue: 71%

has 23% revenue share compared to 24% share of ENIL. We attribute this to its

dominant position in listenership and ability to charge premium advertising rates.

*Calculated on lower price band

Track record of healthy financial performance: Radio City, with ~19% CAGR in

** Calculated on upper price band

revenue, has outperformed its closest peer ENIL, which reported ~14% CAGR in

revenues over FY2013-16. In profitability too, Radio City, with ~54% CAGR in PAT over

Book Building

FY13-16, has performed much better than ENIL (~17% CAGR in PAT over FY2013-16).

QIBs

50% of issue

Outlook and Valuation: In terms of valuations, the pre-issue P/E works out to

25.2x its annualised 1HFY2017 earnings (at the upper end of the issue price

Non-Institutional

15% of issue

band), which is lower compared to its peers (ENIL is trading at 79.5x its

Retail

35% of issue

annualised 1HFY17 earnings). Also, MBL’s EV/sales multiple 6.2x, works out to be

at discount to ENIL’s 8.2x. On EV/EBITDA front too, Radio City’s issue appears to

be attractive 18.7x v/s. ENIL’s 37.4x. Moreover, MBL has a better margin and

Post Issue Shareholding Pattern

ROE profile than its comparable peers. Hence, considering the above positives

coupled with attractive valuations, we recommend a SUBSCRIBE on the issue.

Promoters

71%

Key Financials

Others

29%

Y/E March (` cr)

FY2014

FY2015

FY2016

1HFY17

Net Sales

154

201

232

137

% chg

11.7

30.3

15.7

-

Net Profit

24

47

43

30

% chg

109.4

93.5

(9.7)

-

OPM (%)

27.5

31.0

33.8

33.2

EPS (`)

5.4

10.4

9.4

6.6

P/E (x)

61.7

31.9

35.3

-

P/BV (x)

141.2

26.0

14.0

-

RoE (%)

229.0

81.7

39.6

-

RoCE (%)

23.6

13.6

17.0

-

Amarjeet S Maurya

EV/Sales (x)

10.2

8.6

7.4

-

+91 22 39357800 Ext: 6831

EV/EBITDA (x)

37.0

27.8

22.0

-

Source: Company, Angel Research; Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

Please refer to important disclosures at the end of this report

1

Music Broadcast | IPO Note

Company background

Music Broadcast Limited (MBL) owns and operates FM radio stations under the

brand names Radio City and Radio Mantra. The company has 39 radio stations

and operates its radio stations in 37 Indian cities. Radio City is present in 12 out of

the top 15 cities in India by population. Radio City has been ranked Number One

in Mumbai, Bangalore and Delhi in terms of number of listeners and has a total

number of 49.60mn listeners across all 23 cities (according to AZ Research). Music

Broadcast Limited operates as a subsidiary of Jagran Prakashan Limited. It also

operates 40 Web radio stations that offer Internet radio with live RJ hosted shows

through Planet Radio City in 8 languages. In addition, Music Broadcast Limited

operates 'Planet Radio City' mobile app that plays various stations such as 'Radio

City Freedom', 'Radio City Electronica', 'Radio City Metal', and 'Radio City Smaran'

in various languages on mobile and other smart devices.

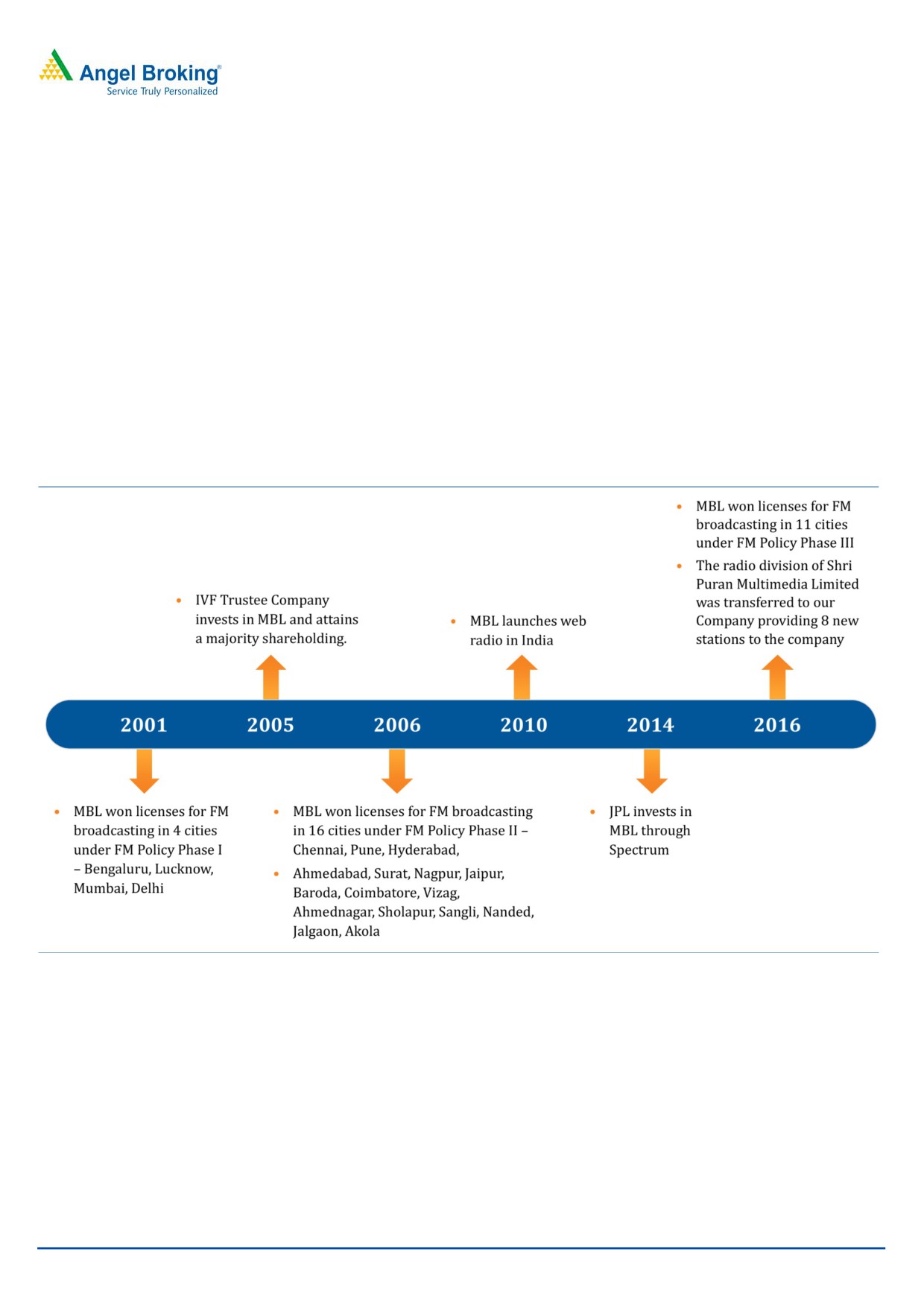

Exhibit 1: 15 years of Radio City - growing along with the FM industry’s liberalization curve

Source: Company, Angel Research

March 1, 2017

2

Music Broadcast | IPO Note

Issue details

The company is raising `400cr through a fresh issue of equity shares in the price

band of `324-333. The fresh issue will constitute 21.1% of the post-issue paid-up

equity share capital of the company, assuming the issue is subscribed at the upper

end of the price band. The company is offering 0.27cr shares that are being sold

by the promoter group.

Exhibit 2: Pre and Post-IPO shareholding pattern

No. of shares (Pre-issue)

(%) No. of shares (Post-issue)

(%)

Promoters

4,33,93,517

96%

4,07,34,999

71%

Others

16,49,250

4%

1,63,19,780

29%

4,50,42,767

100%

5,70,54,779

100%

Source: RHP, Angel Research

Note: Calculated on upper price band

Objects of the offer

Redemption of listed total NCDs of `200cr in phases. First trench of `50cr in

FY2017, next trench of `100cr in FY2018 and last trench of `50cr in FY2020.

Early redemption of the JPL NCDs and repayment/pre-payment of JPL ICDs of

`98.2cr in FY2018.

General corporate purpose.

March 1, 2017

3

Music Broadcast | IPO Note

Investment Rationale

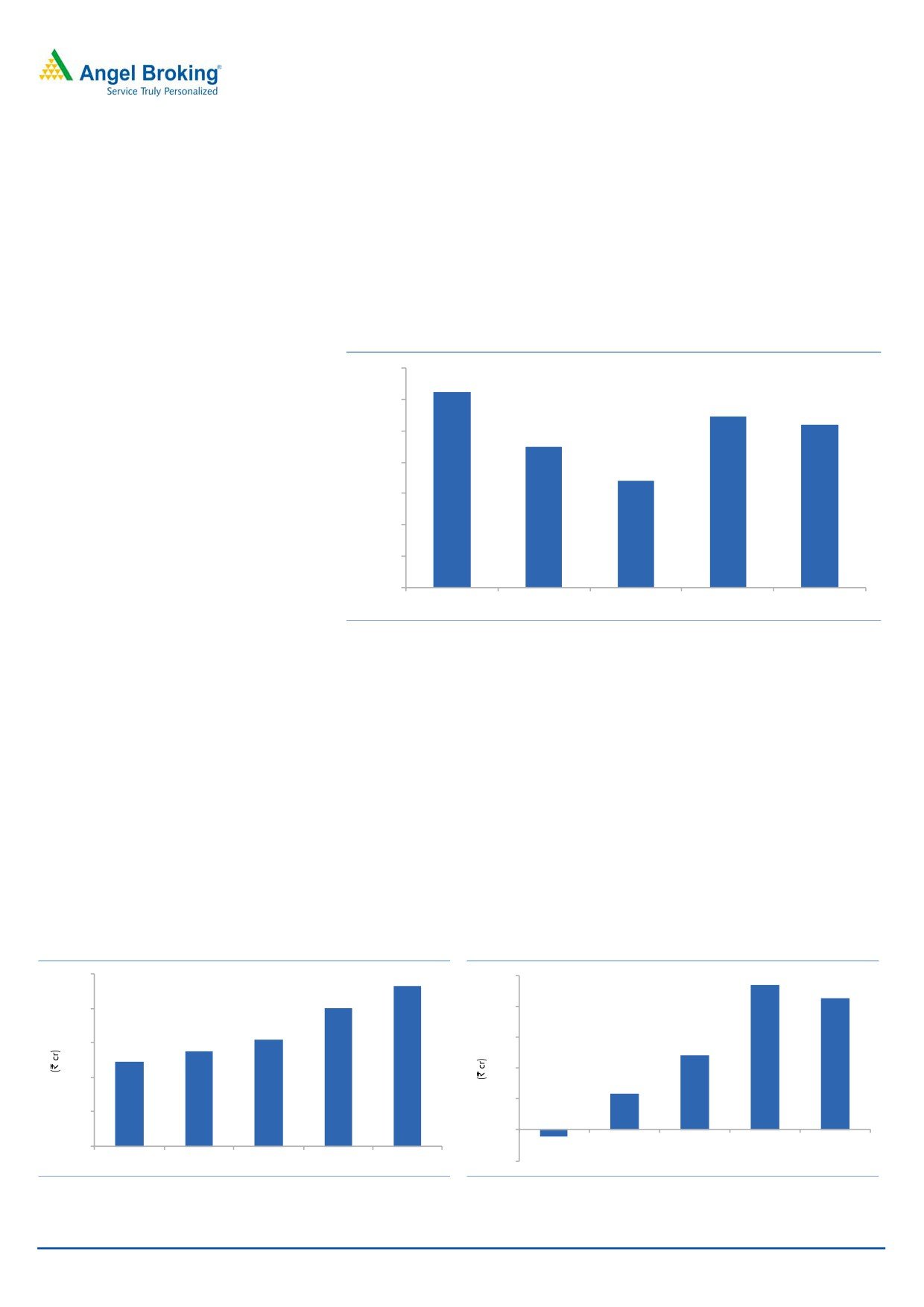

MBL has strong leadership position in large markets: Radio City is ranked No. 1 in

terms of number of listeners, total 49.6mn listeners across the 23 cities (its

competitor ENIL is at 2nd place with 40.5mn listeners). Even in the metro cities like

Mumbai, Bangalore and Delhi, MBL enjoys a leadership position.

According to a survey conducted by AZ Research in certain markets in which ‘Radio

City’ and ‘Radio Mantra’ operate, namely Delhi, Jaipur, Lucknow, Ahmedabad,

Vadodara, Surat, Mumbai, Pune, Nagpur, Ahmed Nagar, Hyderabad, Vizag,

Bengaluru, Chennai, Coimbatore, Ranchi, Varanasi, Agra, Bareilly, Gorakhpur,

Hissar, Jalandhar and Karnal, concluded that MBL has a listenership base of

49.6mn.

Exhibit 3: Listenership Across Markets

Exhibit 4: Listenership in Mumbai

60

9

8.0

49.6

8

50

7

40.5

5.8

5.5

40

6

5

30

25.3

22.9

4

3.0

20

3

2.0

10.1

1.6

7.6

2

10

1

0

0

Radio City

Radio

Big FM

Red FM

Fever

Radio One

Radio City

Big FM

Radio

Fever

Red FM

Radio One

Mirchi

Mirchi

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 5: Listenership in Delhi

Exhibit 6: Listenership in Bangalore

10

5

4.6

8.8

9

5

8.0

8

4

3.6

7.0

7

4

2.8

6

3

5.1

5.0

5

3

2.1

2.0

4

2

1.6

3

2

2

1

1

1

0

0

Radio City

Radio Mirchi

Red FM

Big FM

Fever

Radio City

Big FM Radio Mirchi Fever

Radio One Red FM

Source: Company, Angel Research

Source: Company, Angel Research

March 1, 2017

4

Music Broadcast | IPO Note

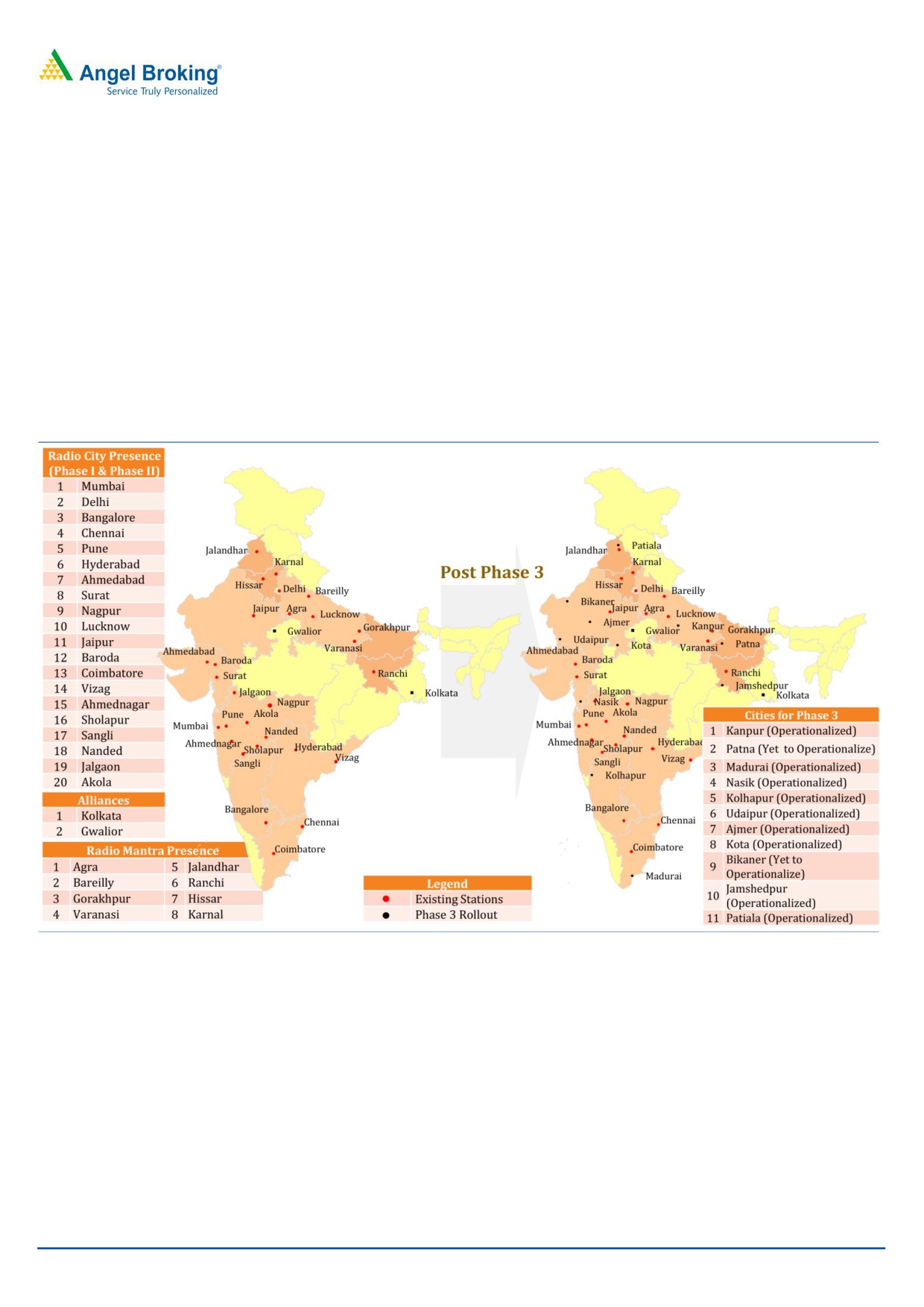

Pan-India presence to propel growth

The company operates total 39 radio stations out of which 29 are through ‘Radio

City’ brand, 8 radio stations are through ‘Radio Mantra’ brand and for the

remaining

2, the company has two sales alliances with ITM Software &

Entertainment Private Ltd., which operates ‘Suno Lemon’ in Gwalior and Ananda

Offset Private Ltd., which operates ‘Friends FM’ in Kolkata. MBL also expects to

operationalize two new Radio City Stations, namely Bikaner and Patna, by

March/ April 2017. Further, the company is in the process of re-branding the

Radio Mantra Stations as ‘Radio City’ stations. In this regards, it has made an

application dated January 11, 2017 to MIB for approval of rebranding the Radio

Mantra Stations as ‘Radio City’ stations.

Exhibit 7: Pan-India Presence in the Right Markets

Source: Company, Angel Research

Ability to charge premium advertising rates

Radio City’s wide listenership despite operating fewer stations has enabled the

company to charge ~30% higher advertising rates than its peers and 12-15%

higher charges than its closest peer. Owing to this, Radio City enjoys healthy 34%

operating margin, much better than ENIL’s ~30% margin in FY2016.

March 1, 2017

5

Music Broadcast | IPO Note

Volume growth outperforms peers as well as Industry

Radio City’s advertising volumes have grown at a CAGR of ~12.5% over

FY2011-16, while, ENIL reported ~9% CAGR in advertising volumes during the

same period. Radio City’s advertising volumes have witnessed higher growth

(CAGR of 10.4% over the same period) than the industry due to its higher

listenership.

Exhibit 8: Strong leadership in listener base over FY2011-16 aided

higher growth in advertisements

14.0%

12.5%

12.0%

10.9%

10.4%

10.0%

9.0%

8.0%

6.8%

6.0%

4.0%

2.0%

0.0%

Radio City

Radio Mirchi

Big FM

Red FM

Industry

Source: Company, Angel Research

Higher revenue share despite operating lesser radio markets

Radio City operates 20 markets, while ENIL operates a total of 38 markets. Despite

this, Radio City has 23% revenue share compared to 24% share of ENIL. We

attribute this to its dominant position in listenership and ability to charge premium

advertising rates.

Track record of healthy financial performance

Radio City, with 19% CAGR in revenue, has outperformed its closest peer ENIL,

which reported 14% CAGR in revenues over FY2013-16. In profitability too, Radio

City, with 54% CAGR in PAT over FY2013-16, has performed much better than

ENIL (17% CAGR in PAT over FY2013-16).

Exhibit 9: Historical revenue trend

Exhibit 10: Historical PAT trend

250

232

50

47

43

201

200

40

154

138

30

150

24

122

20

100

12

10

50

(2)

0

FY2012

FY2013

FY2014

FY2015

FY2016

0

FY2012

FY2013

FY2014

FY2015

FY2016

-10

Source: Company, Angel Research

Source: Company, Angel Research

March 1, 2017

6

Music Broadcast | IPO Note

Outlook and Valuation

In terms of valuations, the pre-issue P/E works out to 25.2x its annualised

1HFY2017 earnings (at the upper end of the issue price band), which is lower

compared to its peers (ENIL is trading at 79.5x its annualised 1HFY17 earnings).

Also, MBL’s EV/sales multiple 6.2x, works out to be at discount to ENIL’s 8.2x. On

EV/EBITDA front too, Radio City’s issue appears to be attractive 18.7x v/s. ENIL’s

37.4x. Moreover, MBL has a better margin and ROE profile than its comparable

peers. Hence, considering the above positives coupled with attractive valuations,

we recommend a SUBSCRIBE on the issue

Key risks

Slowdown in Indian economy would impact overall ad spends

A slowdown in the economy could affect the spending from the clients, which in

turn would affect the company’s overall earnings.

Increase in content price

Inability to effectively source music content from third party music production

entities/associations can increase the input cost for the company, and hence, may

result in the dip in margins.

March 1, 2017

7

Music Broadcast | IPO Note

Income Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

1HFY17

Total operating income

138

154

201

232

137

% chg

13.0

11.7

30.3

15.7

-

Total Expenditure

104

112

139

154

91

License fees

8

8

9

17

9

Personnel

35

36

43

52

32

Others Expenses

62

67

86

85

50

EBITDA

34

42

62

79

46

% chg

30.3

25.1

47.1

26.1

(% of Net Sales)

24.5

27.5

31.0

33.8

33.2

Depreciation& Amortisation

20

15

16

17

9

EBIT

14

27

47

61.9

37

% chg

450.9

92.5

73.4

32.8

(% of Net Sales)

10.1

17.4

23.2

26.6

26.7

Interest & other Charges

5

6

6

19

8

Other Income

2

3

7

13

1

(% of PBT)

21.1

12.8

14.2

31.0

4.4

Extraordinary Items

-

-

-

14

-

Share in profit of Associates

-

-

-

-

-

Recurring PBT

12

24

47

43

30

% chg

109.4

93.5

(9.7)

Tax

-

-

-

-

-

PAT (reported)

12

24

47

43

30

% chg

109.4

93.5

(9.7)

(% of Net Sales)

8.4

15.8

23.4

18.3

21.7

Basic & Fully Diluted EPS (`)

2.6

5.4

10.4

9.4

6.6

% chg

109.4

93.5

(9.7)

March 1, 2017

8

Music Broadcast | IPO Note

Balance Sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

1HFY17

SOURCES OF FUNDS

Equity Share Capital

39

39

39

39

42

Reserves& Surplus

(53)

(28)

19

68

98

Shareholders Funds

(14)

11

58

107

140

Total Loans

118

103

285

256

250

Total Liabilities

104

114

342

363

390

APPLICATION OF FUNDS

Net Block

42

32

19

230

222

Capital Work-in-Progress

1

0

0

66

69

Investments

0

0

0

14

16

Current Assets

127

138

379

175

221

Inventories

-

-

-

-

-

Sundry Debtors

65

63

77

95

114

Cash

22

34

54

16

30

Loans & Advances

32

36

234

60

73

Other Assets

9

6

13

4

4

Current liabilities

66

56

55

122

137

Net Current Assets

61

82

323

53

83

Mis. Exp. not written off

-

-

-

-

-

Total Assets

104

114

342

363

390

March 1, 2017

9

Music Broadcast | IPO Note

Cash Flow Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

1HFY17

Profit before tax

12

24

47

56

30

Depreciation

20

15

16

17

9

Change in Working Capital

0

(8)

(5)

11

1

Interest / Dividend (Net)

5

6

6

19

8

Direct taxes paid

(2)

(0)

1

(11)

(3)

Others

(0)

(1)

1

(26)

(2)

Cash Flow from Operations

34

36

65

66

42

(Inc.)/ Dec. in Fixed Assets

(3)

(4)

(3)

(286)

(16)

(Inc.)/ Dec. in Investments

1

(1)

(198)

217

(6)

Cash Flow from Investing

(2)

(5)

(201)

(69)

(23)

Issue of Equity

0

0

0

0

0

Inc./(Dec.) in loans

2

0

200

83

0

Others

(29)

(26)

(40)

(111)

(14)

Cash Flow from Financing

(27)

(26)

160

(28)

(14)

Inc./(Dec.) in Cash

6

6

24

(31)

5

Opening Cash balances

8

13

19

43

13

Closing Cash balances

13

19

43

13

18

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016

Valuation Ratio (x)

P/E (on FDEPS)

129.1

61.7

31.9

35.3

P/CEPS

47.6

37.7

23.9

25.3

P/BV

-

141.2

26.0

14.0

EV/Sales

11.6

10.2

8.6

7.4

EV/EBITDA

47.1

37.0

27.8

22.0

EV / Total Assets

15.3

13.8

5.1

4.8

Per Share Data (`)

EPS (Basic)

2.6

5.4

10.4

9.4

EPS (fully diluted)

2.6

5.4

10.4

9.4

Cash EPS

7.0

8.8

13.9

13.1

Book Value

-

2.4

12.8

23.8

Returns (%)

ROCE

13.4

23.6

13.6

17.0

Angel ROIC (Pre-tax)

17.0

33.7

16.2

18.6

ROE

-

229.0

81.7

39.6

Turnover ratios (x)

Inventory / Sales (days)

-

-

-

-

Receivables (days)

171

149

140

149

Payables (days)

77

55

62

62

WC cycle (ex-cash) (days)

93

94

79

87

Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

March 1, 2017

10

Music Broadcast | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

March 1, 2017

11