2QFY2016 Result Update | Metals/Mining

November 20, 2015

Hindalco

NEUTRAL

CMP

`78

Performance Highlights

Target Price

-

Investment Period

-

Standalone (` cr)

2QFY16

2QFY15

yoy%

1QFY16

qoq%

Revenue

8,925

8,554

4.3

8,575

4.1

Stock Info

EBITDA

603

466

29.4

877

(31.3)

Sector

Metals/Mining

Margin (%)

6.8

5.4

131bp

10.2

(348)bp

Market Cap (` cr)

16,210

Reported PAT

103

79

31.1

107

(3.7)

Net Debt (` cr)

21,959

Source: Company, Angel Research

Beta

1.3

For 2QFY2016, Hindalco Industries (Hindalco)’ standalone revenues came in 3%

52 Week High / Low

176/68

ahead of our expectations, but the EBITDA disappointed, coming in 16% below

Avg. Daily Volume

96,20,715

our estimate. Net sales increased 4.3% yoy to `8,841cr, vs our expectation of a

Face Value (`)

1

2.5% yoy decline, led by strong increase in aluminium volumes and higher credits

BSE Sensex

25,842

from by-products in the copper division. The strong growth in volumes was diluted

Nifty

7,843

substantially by the sharp slide in commodity prices. Aluminum segment revenue

Reuters Code

HALC.BO

increased 26% yoy whereas copper segment revenue declined 10% yoy. Copper

Bloomberg Code

HNDL IN

volume growth also partially offset the decline in realizations.

Sharp jump in employee and other expenses resulted in the EBITDA margin

Shareholding Pattern (%)

coming in 180bp below our expectations at 6.8%. The EBITDA however increased

Promoters

37.0

29% yoy to `603cr, led by lower than expected material costs. Depreciation and

MF / Banks / Indian Fls

18.0

finance costs jumped sharply yoy and came in marginally ahead of our

FII / NRIs / OCBs

21.5

expectation. However, a sharp jump in other income on account of dividend

Indian Public / Others

23.6

received from subsidiaries and a one-off of `119cr, led the net profit to increase

by 31% yoy to `103cr, well ahead of our expectation of `57cr.

Abs. (%)

3m 1yr

3yr

Outlook and valuation: We expect aluminium prices to remain under pressure led

Sensex

(7.5)

(7.8)

40.9

by the huge oversupply situation and the Chinese slowdown. Pressure on

Hindalco

(9.0)

(49.3)

(27.2)

realizations would continue to offset benefits from volume growth in the

aluminium business. The stock is currently trading at EV/EBITDA of 8x on an

3-year price chart

FY2017E basis and the valuations are currently looking expensive. We remain

250

Neutral on the stock.

200

Key financials (Consolidated)

150

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

100

Revenue

80,193

87,695

1,04,281

1,08,125

1,15,206

50

% chg

(0.8)

9.4

18.9

3.7

6.5

0

Adj. net profit

2,751

2,202

(1,905)

1,132

1,827

% chg

(19.4)

(20.0)

(186.5)

(159.4)

61.4

Adj. EPS (`)

14.4

10.7

(9.2)

5.5

8.8

Source: Company, Angel Research

OPM (%)

9.8

9.4

8.6

8.2

8.8

P/E (x)

5.0

7.4

19.0

14.3

8.9

P/BV (x)

0.4

0.4

0.4

0.4

0.4

RoE (%)

9.0

5.7

2.2

2.9

4.6

RoCE (%)

6.0

4.8

5.0

4.4

5.4

Rahul Dholam

EV/Sales (x)

0.9

0.9

0.8

0.8

0.7

Tel: 022- 3935 7800 Ext: 6847

EV/EBIDTA

8.7

9.2

8.9

9.3

8.0

Source: Company, Angel Research; Note: CMP as of November 19, 2015

Please refer to important disclosures at the end of this report

1

Hindalco | 2QFY2016 Result Update

Exhibit 1: 2QFY2016 performance (Standalone)

(` cr)

2QFY16

2QFY15

yoy%

1QFY16

qoq%

1HFY15

1HFY14

yoy%

Net Sales

8,841

8,473

4.3

8,517

3.8

17,358

16,403

5.8

Other operating income

84

81

2.9

58

44.4

142

147

(3.6)

Revenue

8,925

8,554

4.3

8,575

4.1

17,500

16,550

5.7

Raw material

5,301

5,309

(0.2)

4,889

8.4

10,190

10,456

(2.5)

% of net sales

59.4

62.1

57

58.2

63.2

Employee Cost

446

397

12.4

380

17.3

827

745

10.9

% of net sales

5.0

4.6

4

4.7

4.5

Other expenditure

2,574

2,382

8.1

2,428

6.0

5,003

4,135

21.0

% of net sales

28.8

27.8

28

28.6

25.0

Total expenditure

8,322

8,089

2.9

7,698

8.1

16,020

15,336

4.5

% of net sales

93.2

94.6

90

91.5

92.7

EBITDA

603

466

29.4

877

(31.3)

1,480

1,214

21.9

Margin (%)

6.8

5.4

10

8.5

7.3

112bp

Interest

616

386

59.7

602

2.4

1,218

723

68.3

Depreciation

296

196

50.9

332

(10.9)

628

383

63.9

Other income

418

223

86.9

194

114.8

612

440

39.2

Exceptional items

0

0

0

0

0

Profit before tax

109

107

1.1

138

(21.4)

247

547

14.7

% of net sales

1.2

1.3

2

1.4

3.3

Tax

5

29

(81.4)

31

(82.8)

36

141

(74.4)

% of PBT

4.9

26.6

22

14.7

25.8

Adj. PAT

103

79

31.1

107

(3.7)

210

406

(48.2)

Source: Company, Angel Research

Exhibit 2: 2QFY2016 Actual vs. estimates

(` cr)

Actual

Estimates

Variation (%)

Revenue

8,841

8,336

3.1

EBITDA

603

720

(16.3)

EBITDA margin (%)

6.8

8.6

(180bp)

Net profit

103

57

82.4

Source: Company, Angel Research

Result highlights

Revenue and EBITDA below our estimate

For 2QFY2016, Hindalco Industries (Hindalco)’ standalone revenues came in 3%

ahead of our expectations, but the EBITDA disappointed, coming in 16% below our

estimate. Net sales increased 4.3% yoy to `8,841cr, vs our expectation of a 2.5%

yoy decline, led by strong increase in aluminium volumes and higher credits from

by-products in the copper division. The strong growth in volumes was diluted

substantially by the sharp slide in commodity prices. Aluminum segment revenue

increased 26% yoy whereas copper segment revenue declined 10% yoy. Copper

volume growth also partially offset the decline in realizations.

November 20, 2015

2

Hindalco | 2QFY2016 Result Update

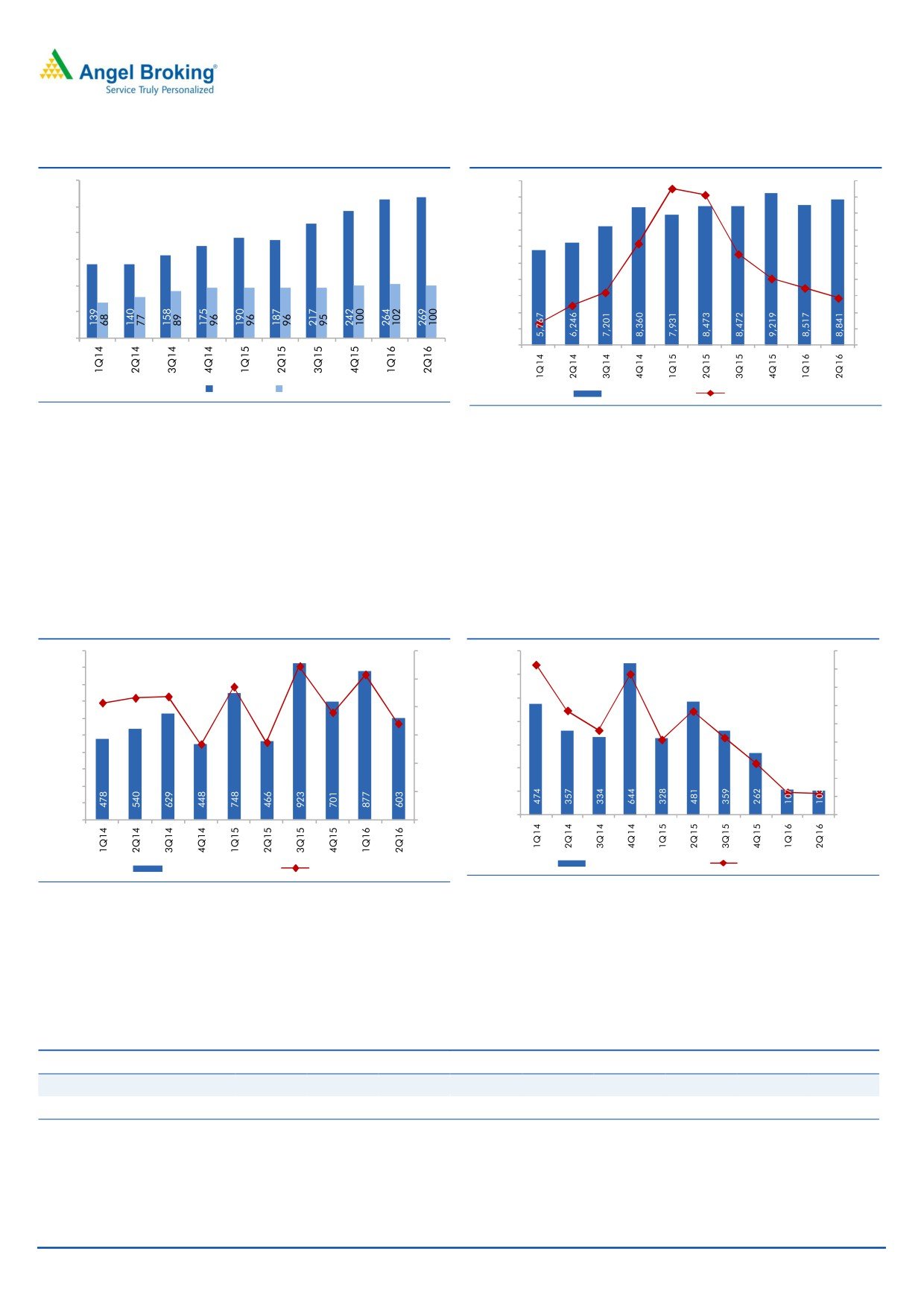

Exhibit 3: Production volumes (kt)

Exhibit 4: Sales growth continues to decline

300

10,000

40

9,000

35

250

8,000

30

200

7,000

25

6,000

20

150

5,000

15

4,000

10

100

3,000

5

50

2,000

0

1,000

(5)

-

0

(10)

Aluminium

Copper

Revenue (` cr)

yoy change (%)

Source: Company, Angel Research

Source: Company, Angel Research

Sharp jump in employee and other expenses resulted in the EBITDA margin

coming in 180bp below our expectations at 6.8%. The EBITDA however increased

29% yoy to `603cr, led by lower than expected material costs. Depreciation and

finance costs jumped sharply yoy and came in marginally ahead of our

expectation. However, a sharp jump in other income on account of dividend

received from subsidiaries and a one-off of `119cr, led the net profit to increase

by 31% yoy to `103cr, well ahead of our expectation of `57cr.

Exhibit 5: EBITDA margin dips sequentially

Exhibit 6: Net profit margin near its recent lows

1,000

10.9

12.0

700

8.2

9.0

10.3

7.7

900

9.4

8.0

600

8.6

8.7

10.0

800

8.3

7.0

7.6

500

5.7

5.7

700

8.0

6.0

6.8

4.6

600

400

4.1

4.2

5.0

5.4

5.5

500

6.0

300

2.8

4.0

400

4.0

3.0

300

200

1.3

1.2

2.0

200

2.0

100

1.0

100

-

0.0

-

0.0

Net Profit (` cr)

Margin (%)

EBITDA (` cr)

Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

Novelis recorded a strong growth in rolled shipments in 2QFY2016 to 788kt led

by a ramp-up in auto sheets. The Management indicated that demand continues to

remain strong. EBITDA/tonne increased sharply to $302, an increase of 3% yoy

and 9% qoq.

Exhibit 7: Quarterly Performance Trend - Novelis

2QFY14

3QFY14

4QFY14

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

Rolled Shipments (kt)

713

721

753

770

765

757

758

768

788

EBITDA/Tonne ($)

315

290

305

308

293

304

283

276

302

Source: Company, Angel Research

November 20, 2015

3

Hindalco | 2QFY2016 Result Update

Investment arguments

Aluminium prices to remain under pressure

Aluminium and Copper prices have continued to slide over the last year led by a

meltdown in overall commodity prices. As per the Management, while the

aluminium market continues to increase at 4-5%, over-supply issues led by

slowdown in Chinese demand continue to affect prices. With strong supply growth

in China, global aluminum market is likely to be in a large surplus of over a

million ton in the coming quarters. The Management believes that ~25% of global

capacity is incurring cash losses at current realizations and the supply side has not

adjusted to the global turmoil. Led by the oversupply and slow closure of smelters,

we expect aluminium prices to continue to remain weak.

Novelis business remains stable

Novelis continues to see a steady ramp-up in shipments, led by its focus on the

auto segment. The strategy of focusing on reducing weights of automobiles/cars

has paid strong dividends to Novelis. The auto segment end user demand

witnessed a 59% yoy growth for the quarter. We expect Novelis’ volumes to

continue to remain stable led by this focus. The recent expansion at Novelis is also

progressing well, which is resulting in higher volumes. The company is also

focusing on inventory rationalization which should help reduce working capital

significantly and drive free cash flows for the company.

November 20, 2015

4

Hindalco | 2QFY2016 Result Update

Outlook and valuation

We expect aluminium prices to remain under pressure led by the huge oversupply

situation and the Chinese slowdown. Pressure on realizations would continue to

offset benefits from volume growth in the aluminium business. The stock is

currently trading at EV/EBITDA of 8x on an FY2017E basis and the valuations

currently look expensive. We remain Neutral on the stock.

Company background

Hindalco Industries is an integrated player in the non-ferrous space with

operations comprising bauxite mining, alumina refining and aluminum smelting to

downstream rolling, extrusions, foils, along with captive power plants and coal

mines. The company operates in two segments: Aluminium and Copper. The

Aluminium segment consists of hydrate and alumina, aluminium and aluminium

products. The Copper segment consists of continuous cast copper rods, copper

cathode, sulphuric acid, DAP and complexes, gold, and silver. The company’s

projects include Greenfield as well as Brownfield projects. Its Greenfield expansion

projects include Mahan Aluminum Project, Aditya Alumina and Aluminum Project,

Utkal Alumina Project and Jharkhand Aluminum Project. Its Brownfield projects

include primary metal and Alumina capacity.

November 20, 2015

5

Hindalco | 2QFY2016 Result Update

Profit & Loss Statement (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

Net Sales

80,193

87,695

1,04,281

1,08,125

1,15,206

% chg

(0.8)

9.4

18.9

3.7

6.5

Total Expenditure

72,356

79,409

95,336

99,292

1,05,019

Raw Materials

48,545

53,388

64,932

67,325

71,734

Power & Fuel Cost

5,251

6,725

8,464

8,776

9,351

Employee Cost

6,526

6,745

7,906

8,197

8,734

Other Expenses

12,034

12,552

14,035

14,994

15,200

EBITDA

7,837

8,286

8,945

8,832

10,187

% chg

(4.3)

5.7

7.9

(1.3)

15.3

(% of Net Sales)

9.8

9.4

8.6

8.2

8.8

Depreciation& Amortisation

2,861

3,553

3,591

4,021

4,142

EBIT

4,976

4,733

5,354

4,811

6,045

% chg

(6.5)

(4.9)

13.1

(10.1)

25.7

(% of Net Sales)

6.2

5.4

5.1

4.4

5.2

Interest & other Charges

2,079

2,702

4,178

4,387

4,563

Other Income

1,012

1,017

1,105

1,050

1,060

Exceptional items

0

(396)

(1,940)

0

0

Profit before tax

3,909

2,653

340

1,473

2,542

% chg

(10.0)

(32.1)

(87.2)

333.0

72.6

Tax Expense

886

525

256

516

890

(% of PBT)

22.7

19.8

75.4

35.0

35.0

Recurring PAT

3,023

2,128

84

958

1,652

Minority Interest

(20)

20

(596)

0

0

Share of associates

15.8

(66.8)

(174.7)

(174.7)

(174.7)

Reported PAT

3,027

2,175

854

1,132

1,827

Adjusted PAT

2,751

2,202

(1,905)

1,132

1,827

% chg

(19.4)

(20.0)

(186.5)

(159.4)

61.4

(% of Net Sales)

3.4

2.5

(1.8)

1.0

1.6

November 20, 2015

6

Hindalco | 2QFY2016 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E

SOURCES OF FUNDS

Equity Share Capital

191

206

207

207

207

Reserves & Surplus

35,139

40,398

38,122

38,831

40,234

Shareholders Funds

35,330

40,605

38,329

39,037

40,441

Minority Interest

1,759

1,781

956

956

956

Total Loans

56,951

64,756

68,468

71,468

71,468

Deferred Tax Liability

3,468

3,175

2,555

2,761

3,117

Other Long term liabilities

7,024

6,972

7,377

7,746

8,133

Total Liabilities

1,04,533

1,17,288

1,17,685

1,21,969

1,24,115

APPLICATION OF FUNDS

Gross Block

60,054

87,914

1,01,940

1,07,037

1,09,178

Less: Acc. Depreciation

22,126

26,750

29,982

34,003

38,145

Net Block

37,929

61,163

71,959

73,034

71,033

Capital Work-in-Progress

33,834

23,059

14,111

14,817

14,965

Goodwill

0

0

0

0

0

Investments

12,601

12,961

12,346

12,768

13,198

Current Assets

32,307

37,575

40,632

43,748

47,003

Cash

3,775

5,021

5,309

5,522

5,752

Inventories

14,332

16,694

18,451

19,190

20,968

Debtor

8,952

9,235

9,186

10,927

11,642

Other

5,247

6,625

7,685

8,109

8,640

Current liabilities

16,057

20,694

24,061

25,231

25,057

Net Current Assets

16,250

16,881

16,571

18,517

21,945

Other Assets

3,919.5

3,223.2

2,697.7

2,832.6

2,974.2

Total Assets

1,04,533

1,17,288

1,17,685

1,21,969

1,24,115

November 20, 2015

7

Hindalco | 2QFY2016 Result Update

Cash flow statement (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E FY2017E

Profit before tax

3,909

2,653

340

1,473

2,542

Depreciation

2,813

3,322

3,459

4,021

4,142

Change in Working Capital

(3,874)

962

(86)

(1,733)

(3,199)

Others

1,477

1,977

4,558

409

420

Direct taxes paid

(1,348)

(959)

(1,128)

(309)

(534)

Cash Flow from Operations

2,977

7,956

7,143

3,861

3,372

(Inc.)/ Dec. in Fixed Assets

(11,871)

(9,424)

(5,978)

(5,803)

(2,289)

(Inc.)/ Dec. in Investments

(1,562)

532

1,051

(596)

(605)

Others

657

689

508

Cash Flow from Investing

(12,776)

(8,202)

(4,418)

(6,399)

(2,894)

Issue of Equity

8

1,630

5

-

-

Inc./(Dec.) in loans

14,336

4,869

2,832

3,000

-

Dividend Paid (Incl. Tax)

(398)

(315)

(249)

(249)

(249)

Others

(3,668)

(4,691)

(5,025)

Cash Flow from Financing

10,278

1,493

(2,437)

2,751

(249)

Inc./(Dec.) in Cash

479

1,246

288

213

229

Opening Cash balances

3,296

3,775

5,021

5,309

5,522

Closing Cash balances

3,775

5,021

5,309

5,522

5,752

November 20, 2015

8

Hindalco | 2QFY2016 Result Update

Key ratios

Y/E March

FY2013

FY2014

FY2015

FY2016E

FY2017E

Per Share Data (`)

Reported EPS

15.8

10.5

4.1

5.5

8.8

Adjusted EPS

14.4

10.7

(9.2)

5.5

8.8

Cash EPS

30.7

27.7

21.5

25.0

28.9

DPS

1.6

1.0

1.0

1.0

1.0

Book Value

184.5

196.7

185.6

189.0

195.8

Valuation Ratio (x)

P/E (on FDEPS)

5.0

7.4

19.0

14.3

8.9

P/CEPS

2.5

2.8

3.6

3.1

2.7

P/BV

0.4

0.4

0.4

0.4

0.4

Dividend yield (%)

2.0

1.3

1.3

1.3

1.3

EV/Sales

0.9

0.9

0.8

0.8

0.7

EV/EBITDA

8.7

9.2

8.9

9.3

8.0

EV/Total Assets

0.7

0.6

0.7

0.7

0.7

Returns (%)

ROCE

6.0

4.8

5.0

4.4

5.4

ROE

9.0

5.7

2.2

2.9

4.6

Turnover ratios (x)

Asset Turnover (Gross Block)

1.4

1.2

1.1

1.0

1.1

Inventory (days)

62.8

64.6

61.5

63.5

63.6

Receivables (days)

38.6

37.8

32.2

33.9

35.8

Payables (days)

73.9

76.5

78.3

83.2

79.7

WC cycle (ex-cash) (days)

47.6

50.6

40.5

40.9

46.2

Solvency ratios (x)

Net debt to equity

1.5

1.5

1.6

1.7

1.6

Net debt to EBITDA

0.9

0.9

0.9

0.9

0.9

Interest Coverage (EBIT / Interest)

2.4

1.8

1.3

1.1

1.3

November 20, 2015

9

Hindalco | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Hindalco

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 20, 2015

10