3QFY2017 Result Update | Automobile

February 14, 2017

Hero MotoCorp

ACCUMULATE

CMP

`3,226

Performance Highlights

Target Price

`3,466

Y/E March (` cr)

2QFY17

2QFY16

% chg (yoy) 1QFY17

% chg (qoq)

Investment Period

12 Months

Net Sales

6,365

7,295

(12.8)

7,796

(18.4)

EBITDA

1,080

1,140

(5.3)

1,369

(21.1)

Stock Info

EBITDA margin (%)

17.0

15.6

(134 bps)

17.6

(59 bps)

Sector

Automobile

Adj PAT

772

796

(3.0)

1,004

(23.1)

Market Cap (` cr)

64,428

Source: Company, Angel Research

Net Debt (` cr)

-103

Beta

0.9

Result indicates demonetisation pain: Total volumes were at 14.73 lakh vehicles

52 Week High / Low

3,739/2,440

showing a yoy decline of 13%. On sequential basis, volumes declined by 19%.

Avg. Daily Volume

28,199

Net realization stood at `42,387 per vehicle vs. `42,059 in 2QFY17 and

Face Value (`)

2

`42,442 in 3QFY16. The company has maintained the upward trajectory in

BSE Sensex

28,352

contribution per vehicle which stood at `14,373 per vehicle against `13,552 in

Nifty

8,805

3QFY16. EBITDA came in at `1080cr vs. 1,140cr in 3QFY16. EBITDA margins

improved by ~140bps on yoy basis and declined by ~60bps on qoq basis. Gross

Reuters Code

HROM.BO

margins improved to 35.1% in 3QFY17 vs. 33.5% in 3QFY16. This is mainly due

Bloomberg Code

HMCL@IN

to the 6 month lag in the raw material prices. Net profit declined by 3% yoy from

`796cr in 3QFY16 to `772cr in 3QFY17.

Shareholding Pattern (%)

Outlook and valuation: The demonetisation has impacted HMCL’s volumes

Promoters

34.6

sharply with decline in all parameters. Company expects the volumes growth to

MF / Banks / Indian Fls

13.4

remain challenging in 4QFY17E and expects high single digit volume growth in

FII / NRIs / OCBs

42.9

FY18E. As automobile industry recovers, HMCL looks to be better positioned due

Indian Public / Others

9.1

to its higher market share in the motorcycle segment. The company also has rural

exposure and as budget sets tone for higher rural spending, HMCL is likely to

benefit. Company has lost ~50bps market share in the scooter segment. We

Abs. (%)

3m 1yr 3yr

forecast 6.8% and 9.5% volume growth in FY18E and FY19E. We also forecast

Sensex

2.9

19.3

39.3

top line and bottom line CAGR of 8.5% and 8.9% over FY17E-FY19E. Company

Hero MotoCorp

3.9

28.2

63.5

has indicated of ~50-60bps margin expansion in FY18E which is likely to take the

operating margins at 17% post which we don’t see any lever for expansion. The

3-year price chart

stock, at CMP, trades at 17.3x and 15.8x of FY18E and FY19E EPS respectively.

4,000

We value the stock at 17x of FY19E earrings to arrive at a price target of `3,466.

3,000

Key financials (Standalone)

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

FY2019E

2,000

Net Sales

27,351

28,160

28,083

30,096

33,071

1,000

% chg

8.9

3.0

(0.3)

7.2

9.9

Net Profit

2,541

3,132

3,432

3,734

4,072

0

% chg

13.1

31.3

9.6

8.8

9.0

OPM (%)

12.8

15.5

16.7

17.0

17.0

EPS (`)

119.5

156.9

171.8

187.0

203.9

Source: Company, Angel Research

P/E (x)

27.0

20.6

18.8

17.3

15.8

P/BV (x)

9.8

8.1

6.6

5.5

4.7

RoE (%)

35.3

33.9

30.1

27.9

25.8

RoCE (%)

42.3

44.9

38.8

35.8

33.3

Shrikant Akolkar

EV/Sales (x)

2.2

2.1

2.1

1.9

1.7

022-3935 7800 Ext: 6846

EV/EBITDA (x)

18.5

15.0

13.8

12.2

10.9

Source: Company, Angel Research; Note: CMP as of February 13, 2017

Please refer to important disclosures at the end of this report

1

Hero MotoCorp | 3QFY2017 Result Update

Exhibit 1: Quarterly financial performance (Standalone)

Y/E March (` cr)

3QFY17

3QFY16

% chg (yoy)

2QFY17

% chg (qoq)

9MFY17

9MFY16

% chg (yoy)

Total units sold

1,473,548

1,690,354

(12.8)

1,823,498

(19.2)

5,042,435

4,911,082

2.7

Net sales

6,365

7,295

(12.8)

7,796

(18.4)

21,560

21,009

2.6

Consumption of RM

4,128

4,883

(15.5)

5,183

(20.4)

14,277

14,360

(0.6)

(% of Sales)

64.9

66.9

66.5

66.2

68.4

Staff costs

374

345

8.6

357

4.7

1,068

966

10.6

(% of Sales)

5.9

4.7

4.6

5.0

4.6

Other expenses

783

927

(15.6)

887

(11.7)

2,537

2,405

5.5

(% of Sales)

12.3

12.7

11.4

11.8

11.4

Total Expenditure

5,285

6,155

(14.1)

6,427

(17.8)

17,881

17,731

0.8

Operating Profit

1,080

1,140

(5.3)

1,369

(21.1)

3,679

3,278

12.2

OPM

17.0

15.6

17.6

17.1

15.6

Depreciation

125

114

9.6

119

4.7

359

326

10.2

Other income

132

84

56.7

152

(13.4)

405

300

34.9

Finance cost

2

1

176.4

2

(1.9)

5

3

52.8

PBT (excl. Extr. Items)

1,085

1,110

(2.2)

1,400

(22.5)

3,719

3,249

14.5

Extr. Income/(Expense)

0.00

0.00

0.00

0.00

0.00

PBT (incl. Extr. Items)

1,085

1,110

(2.2)

1,400

(22.5)

3,719

3,249

14.5

(% of Sales)

17.1

15.2

18.0

17.3

15.5

Tax

313

314

(0.2)

396

(20.9)

1,060

919

15.3

(% of PBT)

28.9

28.3

28.3

28.5

28.3

Reported PAT

772

796

(3.0)

1,004

(23.1)

2,659

2,329

14.2

Adj PAT

772

796

(3.0)

1,004

(23.1)

2,659

2,329

14.2

Adj. PATM

12.1

10.9

12.9

12.3

11.1

Equity capital (cr)

40

40

40

40

40

Adjusted EPS (`)

38.7

39.9

(3.0)

50.3

(23.1)

133.2

116.6

14.2

Source: Company, Angel Research

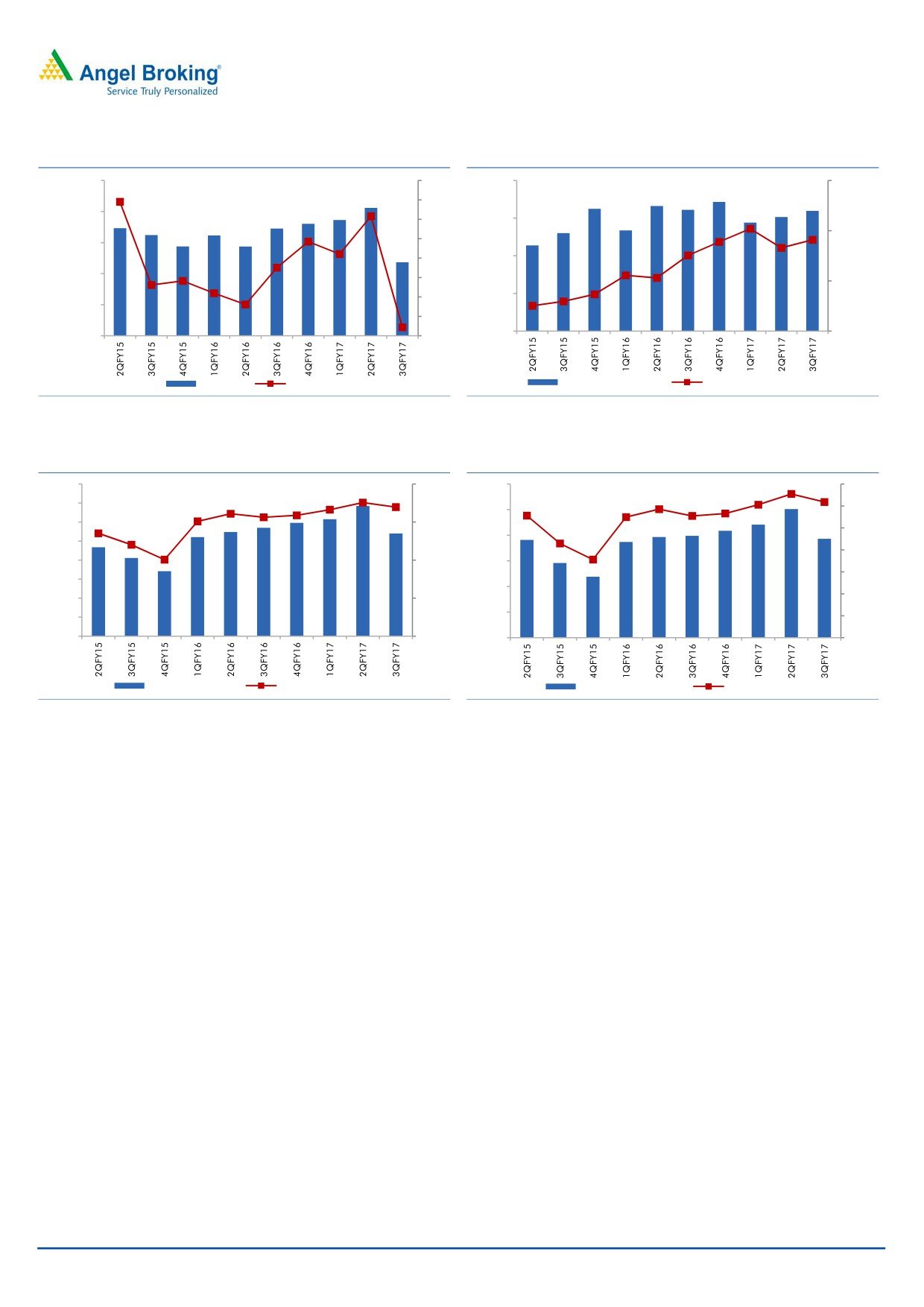

Total volumes were at 14.73 lakh vehicles showing a yoy decline of 13%. On

sequential basis, volumes declined by 19%.

Net realization stood at `42,387 per vehicle vs. `42,059 in 2QFY17 and

`42,442 in 3QFY16.

The company has maintained the upward trajectory in contribution per vehicle

which stood at `14,373 per vehicle against `13,552 in 3QFY16.

EBITDA came in at `1080cr vs. 1,140cr in 3QFY16.

EBITDA margins improved by ~140bps on yoy basis and declined by ~60bps

on qoq basis. Gross margins improved to 35.1% in 3QFY17 vs. 33.5% in

3QFY16. This is mainly due to the 6 month lag in the raw material prices.

Net profit declined by 3% yoy from `796cr in 3QFY16 to `772cr in 3QFY17.

February 14, 2017

2

Hero MotoCorp | 3QFY2017 Result Update

Exhibit 2: Volume growth at 8 quarter high

Exhibit 3: Realisations & contribution/vehicle improve

20,00,000

25

44,000

16,000

20

18,00,000

15

42,000

14,000

10

16,00,000

5

40,000

14,00,000

0

12,000

-5

38,000

12,00,000

-10

36,000

10,000

10,00,000

-15

Volumes

yoy growth (%)

Net realization (`)

Contribution / Vehicle (`)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 4: Consistent rise in EBITDA margins beat

Exhibit 5: PAT at record high

1,600

20.0

1,200

14.0

1,400

12.0

1,000

1,200

15.0

10.0

800

1,000

8.0

800

10.0

600

6.0

600

400

4.0

400

5.0

200

200

2.0

0

0.0

0

0.0

EBITDA (`cr)

EBITDA margins (%)

Net profit (`cr)

Net margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

Conference call - Key highlights

The company expects soft demand trajectory to continue until the first quarter

of next fiscal.

Feb and March 2017 volumes are expected to be flat however company

expects higher single digit growth in FY18

Company reported higher gross margins (35.1% in Q3FY17 vs. 33.06% in

Q3FY16 and 33.5% in Q2FY17). This was due to the increase of material cost

lag period from ~3 months to ~6 months.

The ongoing LEAP program is expected to improve its margins by 80-90bps in

FY17E and further 50-60bps in FY18E.

The Excise benefit at its Haridwar plant will end in FY18E.

While company gained market share in the motorcycle segment, in scooter

segment market remained flat. This will be addressed by new product

launches in this category.

Company has taken 0.5-1% hike in its models to absorb the raw material cost

impact.

February 14, 2017

3

Hero MotoCorp | 3QFY2017 Result Update

Investment arguments

Domestic vehicle demand to recover faster than expected: The automobile

demand in India impacted post demonetisation. The demand however is

slowly coming back to normalcy as liquidity in the country is improveing. From

March onwards, there will be no limit on cash withdrawals which will benefit

Automobile industry. The lower interest rates, government’s focus on rural

economy and cut in the entry level tax rates is expected to benefit the

automobile sector. Overall we expect the demand scenario to come back to

normalcy in 1QFY18E.

Hero Motocorp well positioned to gain from demand recovery: Hero Motocorp

(HMCL) is a well established brand and commands more than 50% market

share in the domestic 2W industry. It has a wide range of brands from entry

level to high end motorbikes. It also has strong presence in scooters segment

and it is a well recognized in brand in rural area. Push for rural economy and

tax rate cuts should benefit HMCL gong ahead.

Capacity expansion to meet higher demand: HMCL has total installed capacity

of ~8.2 million units. This capacity would further increase by ~0.750mn units

after commissioning of new capacity at Neemrana plant which is currently

under trial product run. Company is also developing a new capacity at Halol

in Gujarat (~1.8mn units), which is expected to be operational in FY2017,

thus taking the overall capacity to ~10.75 mn units. As a result of its capacity

expansion, HMCL remains well positioned to meet future demand. Its

Haridwar plant contributes ~35% of the total volumes and is currently running

at the capacity utilization of ~67% which gives enough room for volume

growth in short term.

Outlook and valuation

The demonetisation has impacted HMCL’s volumes sharply with decline in all

parameters. Company expects the volumes growth to remain challenging in

4QFY17E and expects high single digit volume growth in FY18E. As automobile

industry recovers, HMCL looks to be better positioned due to its higher market

share in the motorcycle segment. The company also has rural exposure and as

budget sets tone for higher rural spending, HMCL is likely to benefit. Company has

lost ~50bps market share in the scooter segment. We forecast 6.8% and 9.5%

volume growth in FY18E and FY19E. We also forecast top line and bottom line

CAGR of 8.5% and 8.9% over FY17E-FY19E. Company has indicated of ~50-

60bps margin expansion in FY18E which is likely to take the operating margins at

17% post which we don’t see any lever for expansion. The stock, at CMP, trades at

17.3x and 15.8x of FY18E and FY19E EPS respectively. We value the stock at 17x

of FY19E earrings to arrive at a price target of `3,466. .

February 14, 2017

4

Hero MotoCorp | 3QFY2017 Result Update

Exhibit 6: Key assumptions - Volumes

Y/E March

FY2014

FY2015

FY2016E

FY2017E

FY2018E

FY2019E

Total two-wheelers

6,245,960

6,631,826

6,632,322

6,631,198

7,078,838

7,749,013

Source: Company, Angel Research

Company background

Hero MotoCorp (HMCL) is a leading 2W manufacturer globally and the market

leader in the domestic motorcycle segment with more than 50% market share.

HMCL has four manufacturing facilities in India, located at Gurgaon, Dharuhera,

Haridwar and Neemrana. It has also a production facility in Colombia. Together it

has a capacity of ~8.2mn units/year as of September 2016. Over 2010-16,

HMCL recorded a strong volume CAGR of ~12%, backed by its strong brands

(Passion and Splendor) and a well-entrenched dealership network (~19,000),

which has a good presence across rural areas as well.

February 14, 2017

5

Hero MotoCorp | 3QFY2017 Result Update

Profit and loss statement (Standalone)

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

FY2019E

Total operating income

27,351

28,160

28,083

30,096

33,071

% chg

8.9

3.0

(0.3)

7.2

9.9

Total Expenditure

24,043

24,152

23,794

25,359

27,884

Cost of Materials

19,754

19,315

18,896

20,244

22,255

Personnel

1,173

1,320

1,418

1,434

1,560

Others Expenses

3,116

3,518

3,481

3,681

4,069

EBITDA

3,307

4,008

4,289

4,736

5,187

% chg

0.1

25.5

7.0

9.4

9.7

(% of Net Sales)

12.1

14.2

15.3

15.7

15.7

Depreciation& Amortisation

540

441

477

551

607

EBIT

2,768

3,567

3,811

4,185

4,580

% chg

21.3

28.9

6.9

9.8

9.4

(% of Net Sales)

10.1

12.7

13.6

13.9

13.8

Interest & other Charges

11

2

6

6

6

Other Income

493

391

527

581

605

(% of PBT)

15.2

9.9

12.2

12.2

11.7

Recurring PBT

3,249

3,956

4,332

4,760

5,178

% chg

19.6

21.7

9.5

9.9

8.8

Prior Period & Extraord. Exp./(Inc.)

-

-

-

-

-

PBT (reported)

3,249

3,956

4,332

4,760

5,178

Tax

943

1,262

1,372

1,499

1,634

(% of PBT)

29.0

31.9

31.7

31.5

31.6

PAT (reported)

2,306

2,694

2,960

3,261

3,544

Add: Share of earnings of asso.

-

-

-

-

-

Less: Minority interest (MI)

-

-

-

-

-

PAT after MI (reported)

2,306

2,694

2,960

3,261

3,544

ADJ. PAT

2,306

2,694

2,960

3,261

3,544

% chg

13.1

31.3

9.6

8.8

9.0

(% of Net Sales)

8.4

9.6

10.5

10.8

10.7

Basic EPS (`)

119.5

156.9

171.8

187.0

203.9

Fully Diluted EPS (`)

119.5

156.9

171.8

187.0

203.9

% chg

13.1

31.3

9.6

8.8

9.0

February 14, 2017

6

Hero MotoCorp | 3QFY2017 Result Update

Balance sheet statement (Standalone)

Y/E March (` cr)

FY2015

FY2016

FY2017E FY2018E

FY2019E

SOURCES OF FUNDS

Equity Share Capital

40

40

40

40

40

Reserves& Surplus

6,501

7,905

9,792

11,659

13,695

Shareholders’ Funds

6,541

7,945

9,832

11,699

13,735

Minority Interest

-

-

-

-

-

Total Loans

-

-

-

-

-

Deferred Tax Liability

6

239

239

239

239

Other Liabilities

97

119

119

119

119

Total Liabilities

6,645

8,303

10,191

12,058

14,094

APPLICATION OF FUNDS

Gross Block

8,114

9,397

10,697

11,797

12,997

Less: Acc. Depreciation

5,201

5,560

6,037

6,589

7,196

Net Block

2,913

3,837

4,660

5,208

5,801

Capital Work-in-Progress

713

605

680

780

780

Investments

3,154

4,266

4,266

4,266

4,266

Current Assets

3,669

3,632

4,739

6,334

8,310

Inventories

815

673

923

825

815

Sundry Debtors

1,390

1,283

1,385

1,402

1,540

Cash

159

131

774

2,212

3,871

Loans & Advances

627

601

646

752

827

Other Assets

677

944

1,011

1,144

1,257

Current liabilities

3,883

4,049

4,166

4,543

5,076

Net Current Assets

(215)

(417)

573

1,791

3,235

Deferred Tax Asset

80

11

11

11

11

Mis. Exp. not written off

-

-

-

-

-

Total Assets

6,645

8,303

10,191

12,058

14,094

Note: Cash includes cash with scheduled banks on dividend current accounts

February 14, 2017

7

Hero MotoCorp | 3QFY2017 Result Update

Cash flow statement (Standalone)

Y/E March (` cr)

FY2015E

FY2016

FY2017E FY2018E FY2019E

Profit before tax

3,329

4,395

4,804

5,233

5,706

Depreciation

540

441

477

551

607

Change in Working Capital

(337)

446

(347)

220

216

Interest / Dividend (Net)

(142)

(173)

6

6

6

Direct taxes paid

(1,000)

(1,103)

(1,372)

(1,499)

(1,634)

Others

(141)

(92)

-

-

-

Cash Flow from Operations

2,250

3,914

3,568

4,511

4,901

(Inc.)/ Dec. in Fixed Assets

0

0

(1,375)

(1,200)

(1,200)

(Inc.)/ Dec. in Investments

12

(2,271)

-

-

-

Cash Flow from Investing

12

(2,271)

(1,375)

(1,200)

(1,200)

Issue of Equity

-

1

-

-

-

Inc./(Dec.) in loans

0

0

0

0

0

Dividend Paid (Incl. Tax)

(1,897)

(1,398)

(1,544)

(1,867)

(2,036)

Interest / Dividend (Net)

(333)

(287)

(6)

(6)

(6)

Cash Flow from Financing

(2,231)

(1,684)

(1,550)

(1,873)

(2,042)

Inc./(Dec.) in Cash

32

(42)

642

1,438

1,659

Opening Cash balances

66

98

131

774

2,212

Closing Cash balances

98

56

774

2,212

3,871

February 14, 2017

8

Hero MotoCorp | 3QFY2017 Result Update

Key ratios

Y/E March

FY2015E

FY2016

FY2017E FY2018E FY2019E

Valuation Ratio (x)

P/E (on FDEPS)

27.0

20.6

18.8

17.3

15.8

P/CEPS

20.9

18.0

16.5

15.0

13.8

P/BV

9.8

8.1

6.6

5.5

4.7

Dividend yield (%)

1.9

2.2

2.4

2.9

3.2

EV/Sales

2.2

2.1

2.1

1.9

1.7

EV/EBITDA

18.5

15.0

13.8

12.2

10.9

EV / Total Assets

5.8

4.9

4.1

3.5

2.9

Per Share Data (Rs)

EPS (Basic)

119.5

156.9

171.8

187.0

203.9

EPS (fully diluted)

119.5

156.9

171.8

187.0

203.9

Cash EPS

154.3

179.0

195.7

214.6

234.3

DPS

60.0

72.0

77.3

93.5

101.9

Book Value

327.6

397.8

492.3

585.8

687.8

Returns (%)

ROCE

42.3

44.9

38.8

35.8

33.3

Angel ROIC (Pre-tax)

85.7

100.6

79.5

80.2

81.8

ROE

35.3

33.9

30.1

27.9

25.8

Turnover ratios (x)

Asset Turnover (Gross Block)

3.4

3.0

2.6

2.6

2.5

Inventory / Sales (days)

11

9

12

10

9

Receivables (days)

19

18

17

17

-

Payables (days)

38

38

39

40

41

WC cycle (ex-cash) (days)

(8)

(11)

(10)

(13)

(32)

February 14, 2017

9

Hero MotoCorp | 3QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Hero MotoCorp

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 14, 2017

10