Company Update | Tyres

June 10, 2016

Goodyear India

BUY

CMP

`515

Company Update

Target Price

`631

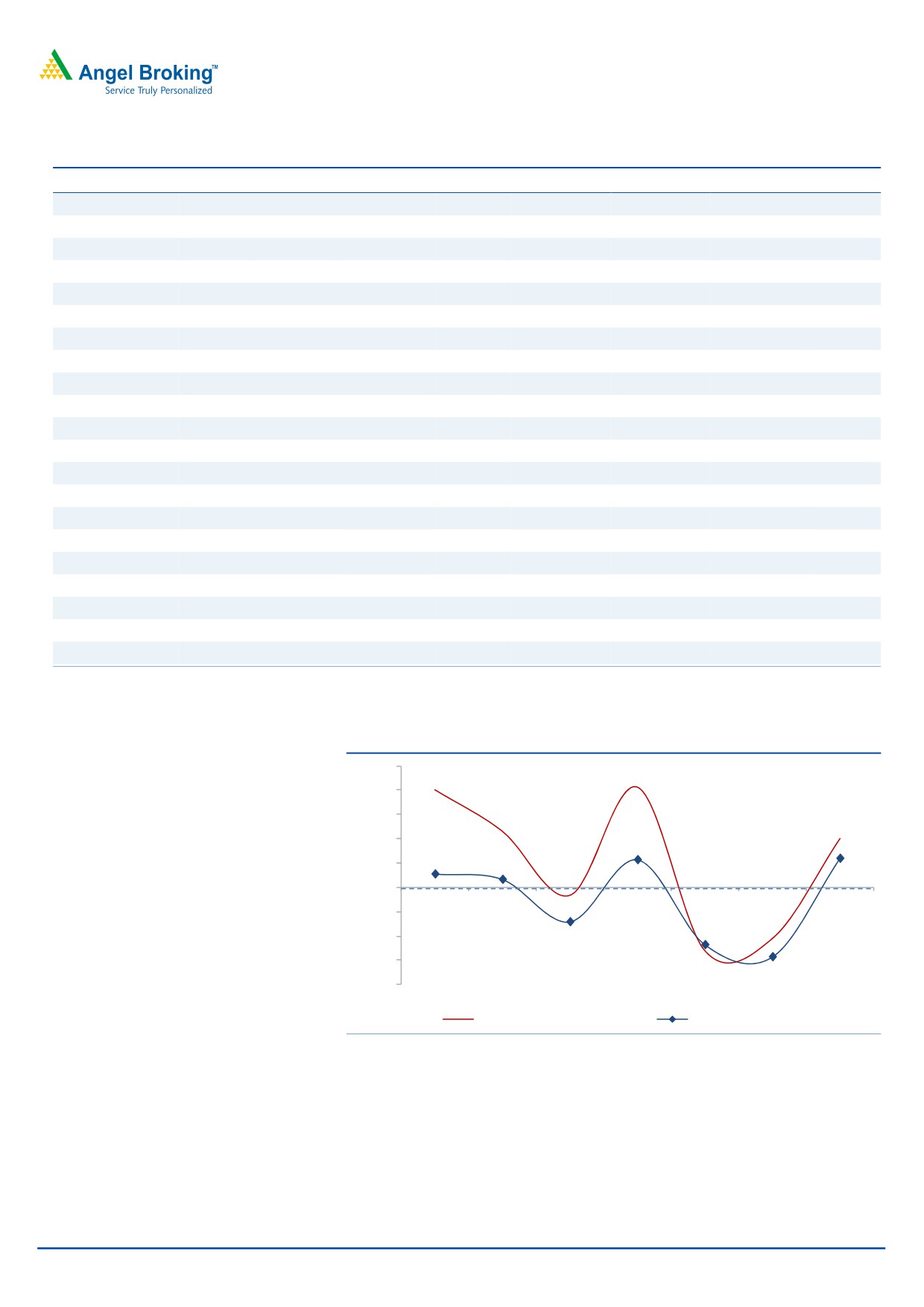

Expectation of normal monsoon to energize stagnant tractor demand: Goodyear

Investment Period

12 Months

India (GIL) is a leader in the farm tyre segment in India with it having strong tie-

ups with OEMs as well as a dominant presence in the replacement market. Farm

tyres account for ~50% of the company’s overall revenues; however, the segment

Stock Info

has been under pressure owing to poor monsoons and erratic rains in the past

Sector

Tyres

two years which has impacted tractor demand during the period. This has not

Market Cap (` cr)

1,188

only hurt OEM demand but also impacted the replacement market. Given that

tractor sales have strong correlation with monsoons, the expectation of a normal

Net Debt

(334)

monsoon this year should translate into higher tractor sales and resultantly higher

Beta

0.7

demand for tractor tyres. GIL being a market leader in tractor tyres segment should

stand to benefit on this account.

52 Week High / Low

662 / 443

Avg. Daily Volume

10,729

Expansion drive to lead to recovery in top-line: GIL has laid out plans to

significantly grow its presence in the passenger vehicle (PV) segment in India over

Face Value (`)

10

the next five years. The company aspires to be one of the top players in the mid to

BSE Sensex

26,763

premium and SUV sub-segments of PVs. It is also evaluating an entry into newer

segments; in order to reach its goal, the company is weighing organic as well as inorganic

Nifty

8,204

growth options. We believe that this increased focus on growing its presence in the PV

Reuters Code

GDYR.BO

segment and entry into newer segments will provide additional boost to the revenues.

Bloomberg Code

GDYR IN

Strong balance sheet with high RoIC: GIL is a debt free-cash rich company with

RoIC estimated at ~84% for FY2018. The company’s cash and equivalents are

`334cr for FY2016, which amount to ~28% of the current market cap. More

Shareholding Pattern (%)

importantly, GIL is one of the cheapest MNC stocks available to invest in, in the

Promoters

74.0

similar market cap range.

MF / Banks / Indian Fls

8.0

Quarterly performance: For 5QFY2016, GIL’s top-line grew by 7.3% yoy to

`295cr and the EBITDA margin stood more or less stable on a yoy basis at 9.3%

FII / NRIs / OCBs

0.0

(v/s 9.6% in the same quarter of the previous year). The margins witnessed a mild

Indian Public / Others

18.0

compression despite of a 97bp yoy decline in raw material cost/sales as other

expenses/sales expanded by 128bp yoy. Factoring this, the EBITDA grew by 3.5%

yoy to `27cr and the bottom-line remained flat at `16cr.

Abs. (%)

3m 1yr 3yr

Outlook and valuation: On an adjusted basis (for financial year end March), we

Sensex

8.3

(0.3)

37.7

expect the top-line to post a CAGR of 7.5% over FY2016-18E to `1,704cr mainly

GOODYEAR

8.0

(1.6)

60.6

on account of rebound in tractor tyre volumes. We have also considered higher

raw material costs and factored in a rubber price of ~`130/kg for FY2017E and

~`140/kg for FY2018E. As a result, the EBITDA margin is expected to be at

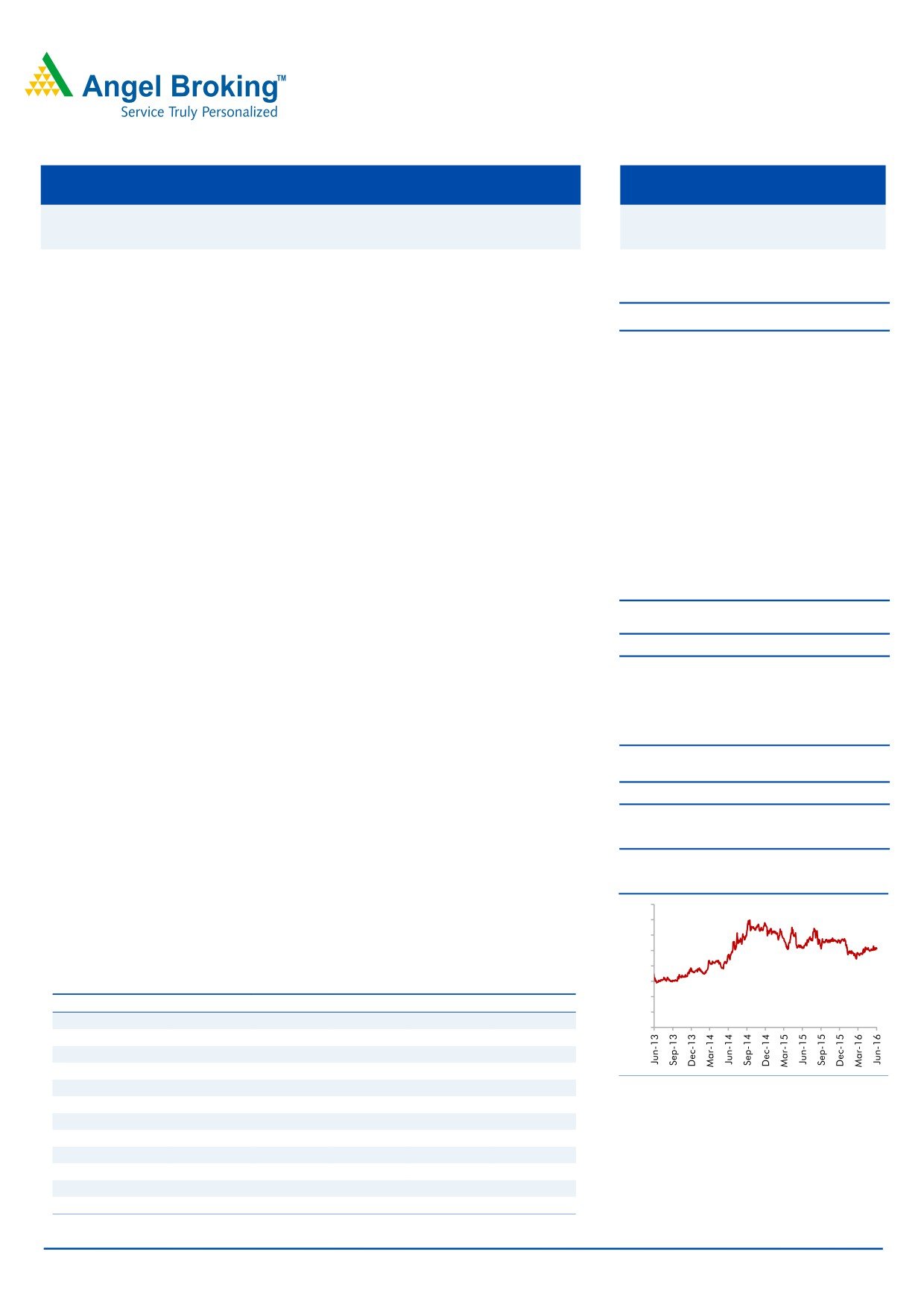

3-year Daily Price Chart

10.2% in FY2018E. Consequently, the net profit is estimated to be at `121cr in

800

FY2018E. At the current market price, the stock is trading at a PE of 9.8x its

700

600

FY2018E earnings. We maintain our Buy rating on the stock and assign a target

500

price of `631 based on a target PE of 12.0x for FY2018E.

400

Key Financials

300

200

Y/E Mar (` cr)

CY2014

FY2015 Adj FY2016 Adj

FY2017E

FY2018E

100

Net Sales

1,579

1,470

1,475

1,598

1,704

-

% chg

0.7

-

0.3

8.4

6.6

Net Profit

101

89

107

114

121

% chg

7.6

-

21.1

6.1

6.5

EBITDA (%)

9.7

9.6

11.5

10.4

10.2

Source: Company, Angel Research

EPS (`)

43.9

38.4

46.6

49.4

52.6

P/E (x)

11.7

13.4

11.1

10.4

9.8

P/BV (x)

2.4

2.3

2.0

1.8

1.6

RoE (%)

22.0

18.4

19.6

18.2

17.0

RoIC (%)

94.6

-

66.2

60.8

84.2

Milan Desai

EV/Sales (x)

0.5

-

0.6

0.4

0.3

+91- 22- 4000 3600 Ext: 6846

EV/EBITDA (x)

5.3

-

5.0

4.0

3.3

Source: Company, Angel Research; Note: *reporting changed from CY to FY starting January 2015;

FY15 & FY16 numbers have been adjusted to reflect four quarters

Please refer to important disclosures at the end of this report

1

Goodyear India | Company Update

Exhibit 1: 5QFY2016 performance

Y/E December (` cr)

5QFY16 1QCY15*

yoy chg (%)

4QFY16

qoq chg (%)

FY2016 Adj

FY2015 Adj

% chg

Net Sales

295

275

7.3

366

(19.2)

1,475

1,470

0.3

Net raw material

181

172

5.7

243

(25.2)

944

992

(4.8)

(% of Sales)

61.4

62.4

(97)bp

66.4

(493)bp

64.0

67.5

(347)bp

Staff Costs

27

25

7.7

30

(9.9)

113

102

11.0

(% of Sales)

9.0

9.0

3bp

8.1

93bp

7.7

7.0

74bp

Other Expenses

60

52

14.5

55

8.8

247

234

5.3

(% of Sales)

20.3

19.0

128bp

15.0

523bp

16.7

15.9

79bp

Total Expenditure

268

249

7.7

327

(18.1)

1,304

1,328

(1.8)

EBITDA

27

26

3.5

38

(28.7)

170

141

20.6

EBITDA margin (%)

9.3

9.6

(34)bp

10.5

(123)bp

11.5

9.6

194bp

Interest

1

1

6.7

1

(1.5)

3

3

(12.6)

Depreciation

8

9

(5.7)

8

7.8

32

31

3.5

Other Income

7

7

(0.6)

10.0

(34.3)

30

27

9.2

PBT

25

24

5.7

40

(37.5)

166

135

12.6

(% of Sales)

8.5

8.6

11.0

11.2

9.2

Tax

9

8

14

58

46

(% of PBT)

36.0

34.4

35.1

35.1

34.1

Reported PAT

16

16

3.1

26

(38.3)

107

89

21.1

PATM

5.4

5.7

7.1

7.3

6.0

Equity capital (cr)

23

23

23

23

23

EPS (`)

7

7

3.1

11

(38.3)

47

38

21.1

Source: Company, Angel Research; *reporting changed from CY to FY starting January 2015

Exhibit 2: Correlation between monsoon & tractor sales

25.0

20.0

15.0

10.0

5.0

-

(5.0)

(10.0)

(15.0)

(20.0)

FY11

FY12

FY13

FY14

FY15

FY16

FY17E

Tractor Sales Volumes yoy

Historical trend in Monsoon

Source: Company, Angel Research

June 10, 2016

2

Goodyear India | Company Update

Company Background

GIL is a subsidiary of Goodyear Orient Company (Private) Ltd (a wholly owned

subsidiary of Goodyear Tire and Rubber Company, USA), which holds a 74% stake

in the company. The Company manufactures automotive bias tyres viz. farm tyres

and commercial truck tyres at its Ballabgarh plant and also trades in “Goodyear”

branded tyres [including radial passenger and Off The Road (OTR) bias tyres]

manufactured by Goodyear South Asia Tyres Private Limited (GSATPL),

Aurangabad. The other products in which the Company markets and sells include

tubes, flaps and Radial OTR imported tyres. GIL is a leader in the farm tyre

segment in India with it having strong tie-ups with OEMs as well as a dominant

presence in the replacement market. Farm tyres account for ~50% of the

company’s overall revenues.

June 10, 2016

3

Goodyear India | Company Update

Profit & Loss Statement

Y/E December (` cr)

CY2014

FY2015 Adj.

FY2016 Adj.

FY2017E

FY2018E

Total operating income

1,579

1,470

1,475

1,598

1,704

% chg

0.7

-

0.3

8.4

6.6

Net Raw Materials

1,094

992

944

1,059

1,133

Personnel

99

102

113

120

127

Other

232

234

247

254

271

Total Expenditure

1,426

1,328

1,304

1,433

1,531

EBITDA

154

141

170

165

173

% chg

10.5

-

10.9

(2.8)

4.7

(% of Net Sales)

9.7

9.6

11.5

10.4

10.2

Depreciation

29

31

32

34

36

EBIT

125

111

139

131

137

% chg

9.9

-

10.7

(5.2)

4.1

(% of Net Sales)

7.9

7.5

9.4

8.2

8.0

Interest & other charges

3

3

3

1

1

Other Income

32

27

30

40

46

(% of sales)

2.0

1.8

2.0

2.5

2.7

PBT

154

135

166

170

181

% chg

8.2

-

7.8

2.8

6.5

Tax

52

46

58

56

60

(% of PBT)

34.0

34.1

35.1

33.0

33.0

PAT (reported)

101

89

107

114

121

Extraordinary (Exp)/Inc.

-

-

-

-

-

ADJ. PAT

101

89

107

114

121

% chg

7.6

-

22.4

6.1

6.5

(% of Net Sales)

6.4

6.0

7.3

7.1

7.1

Basic EPS (`)

43.9

38.4

46.6

49.4

52.6

Fully Diluted EPS (`)

43.9

38.4

46.6

49.4

52.6

% chg

7.6

-

22.4

6.1

6.5

Note: *reporting changed from CY to FY starting January 2015; FY15 & FY16 numbers have been

adjusted to reflect four quarters

June 10, 2016

4

Goodyear India | Company Update

Balance Sheet

Y/E December (` cr)

CY2013

CY2014

FY2016*

FY2017E

FY2018E

SOURCES OF FUNDS

Equity Share Capital

23

23

23

23

23

Preference Capital

-

-

-

-

-

Reserves& Surplus

400

474

559

645

739

Shareholders’ Funds

424

497

582

668

762

Minority Interest

-

-

-

-

-

Total Loans

-

-

-

-

-

Deferred Tax Liability

13

14

10

10

10

Other Long Term Liabilities

3

5

2

2

2

Long Term Provisions

20

21

19

17

18

Total Liabilities

459

536

613

697

792

APPLICATION OF FUNDS

Gross Block

430

481

517

553

592

Less: Acc. Depreciation

220

241

282

316

352

Net Block

210

240

235

237

239

Capital Work-in-Progress

32

17

14

10

10

Goodwill

-

-

-

-

-

Investments

-

-

-

-

-

Long Term Loans and adv.

17

19

22

22

22

Other non-current assets

0

1

1

1

1

Current Assets

600

617

649

822

942

Cash

317

365

334

520

624

Loans & Advances

10

6

17

16

17

Inventory

99

123

129

120

125

Debtors

165

112

158

154

164

Other Current Assets

9

10

12

12

12

Current liabilities

400

358

309

396

423

Net Current Assets

200

259

340

426

519

Misc. Exp. not written off

-

-

-

-

-

Total Assets

459

536

613

697

792

Note: *reporting changed from CY to FY starting January 2015

June 10, 2016

5

Goodyear India | Company Update

Cash Flow Statement

Y/E December (` cr)

CY2013

CY2014

FY2016* FY2017E FY2018E

Profit before tax

142

154

190

170

181

Depreciation

25

29

41

34

36

Change in Working Capital

29

(11)

(112)

100

12

Other income

(30)

(32)

(36)

(40)

(46)

Direct taxes paid

(48)

(52)

(66)

(56)

(60)

Others

14

12

-

-

-

Cash Flow from Operations

131

99

17

208

124

(Inc.)/Dec. in Fixed Assets

(46)

(36)

(34)

(32)

(39)

(Inc.)/Dec. in Investments

-

-

(4)

-

-

(Incr)/Decr In L.T. loan and adv.

2

(2)

(4)

-

-

Other income

30

32

36

40

46

Others

(18)

(17)

-

-

-

Cash Flow from Investing

(32)

(24)

(6)

8

7

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

-

2

(7)

(0)

0

Inc./(Dec.) in L.T. Pro. & Liab.

1

1

(2)

(2)

1

Dividend Paid (Incl. Tax)

(24)

(28)

(33)

(28)

(28)

Others

3

(2)

-

-

-

Cash Flow from Financing

(21)

(27)

(42)

(30)

(27)

Inc./(Dec.) in Cash

78

48

(31)

186

104

Opening Cash balances

238

317

365

334

520

Closing Cash balances

317

365

334

520

624

Note: *reporting changed from CY to FY starting January 2015

June 10, 2016

6

Goodyear India | Company Update

Key Ratios

Y/E December

CY2014

FY2015 Adj.

FY2016 Adj.

FY2017E

FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

11.7

13.4

11.1

10.4

9.8

P/CEPS

9.2

9.9

8.5

8.0

7.5

P/BV

2.4

2.3

2.0

1.8

1.6

Dividend yield (%)

1.9

-

2.3

1.9

1.9

EV/Sales

0.5

-

0.6

0.4

0.3

EV/EBITDA

5.4

-

5.0

4.1

3.3

EV / Total Assets

1.5

-

1.4

1.0

0.7

Per Share Data (`)

EPS (Basic)

43.9

38.4

46.6

49.4

52.6

EPS (fully diluted)

43.9

38.4

46.6

49.4

52.6

Cash EPS

56.3

51.8

60.3

64.2

68.4

DPS

10.0

-

12.0

10.0

10.0

Book Value

215.4

222.1

252.4

289.7

330.3

Returns (%)

ROCE (Pre-tax)

25.1

-

27.2

20.1

18.4

Angel ROIC (Pre-tax)

94.6

-

74.7

59.4

79.1

ROE

22.0

18.4

19.6

18.2

17.0

Turnover ratios (x)

Asset Turnover

3.5

-

2.9

3.0

3.0

Inventory / Sales (days)

26

-

31

29

27

Receivables (days)

32

-

33

33

33

Payables (days)

126

-

129

130

130

WC (ex-cash) (days)

(26)

-

(12)

(9)

(19)

Solvency ratios (x)

Net debt to equity

(0.7)

-

(0.6)

(0.8)

(0.8)

Net debt to EBITDA

(2.4)

-

(2.0)

(3.1)

(3.5)

Interest Coverage

36.7

36.6

52.5

111.6

108.9

Note: *reporting changed from CY to FY starting January 2015; FY15 & FY16 numbers have been

adjusted to reflect four quarters

June 10, 2016

7

Goodyear India | Company Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitian Stock Exchange of India Limited. It is also registered as a Depository Participant

with CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private

Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration

number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for

accessing /dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial

interest/beneficial ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any

compensation / managed or co-managed public offering of securities of the company covered by Analyst during the past twelve

months. Angel/analyst has not served as an officer, director or employee of company covered by Analyst and has not been engaged in

market making activity of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Goodyear India

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15%)

June 10, 2016

8