2QFY2016 Result Update | Pharmaceutical

November 18, 2015

Dishman Pharmaceuticals

NEUTRAL

CMP

`329

Performance Highlights

Target Price

-

Y/E March (` cr)

2QFY2016 1QFY2016

% chg qoq 2QFY2015

% chg yoy

Investment Period

-

Net sales

374

400

(6.6)

392

(4.8)

Other income

15

5

226.4

8

92.6

Stock Info

Operating profit

84

104

(19.2)

81

3.8

Interest

24

32

(26.0)

18

34.8

Sector

Pharmaceutical

Net profit/(loss)

37

38

(3.3)

33

9.4

Market Cap (` cr)

1,322

Source: Company, Angel Research

Net Debt (` cr)

845

Beta

0.9

For 2QFY2016, Dishman Pharmaceuticals and Chemicals (Dishman) posted

52 Week High / Low

197 / 79

lower than expected results on the sales front while a higher other income aided

Avg. Daily Volume

272,877

the net profit to come in marginally higher than expected. Sales for 2QFY2016

declined 4.8% yoy to `374cr V/s an expected `429cr and V/s `392cr in

Face Value (`)

2

2QFY2015. The CRAMS segment (`269.6cr) posted a decline of 4.1% while the

BSE Sensex

29,320

other segment (`103.9cr) posted a dip of 6.4% yoy. On the operating front, the

Nifty

8,869

GPM came in at 75.8% V/s 72.3% expected and V/s 69.7% in 2QFY2015.

Reuters Code

DISH.BO

However, in spite of the same, the OPM came in at 22.5% V/s 22.0% expected

Bloomberg Code

DISH@IN

and V/s 20.5% in 2QFY2015. The net profit consequently came in at `36.5cr V/s

`35.6cr expected and V/s `33.4cr in 2QFY2015, a yoy growth of 9.4%. The

Shareholding Pattern (%)

other income during the period came in at `15.1cr V/s `7.8cr in 2QFY2015. We

Promoters

61.4

maintain our Neutral stance on the stock.

MF / Banks / Indian Fls

8.2

Results lower than expected on the sales front: Sales for 2QFY2016 declined

FII / NRIs / OCBs

13.5

4.8% yoy to `374cr V/s an expected `429cr and V/s `392cr in 2QFY2015. The

Indian Public / Others

17.0

CRAMS segment (`269.6cr) posted a decline of 4.1% while the other segment

(`103.9cr) posted a dip of 6.4% yoy. On the operating front, the GPM came in at

75.8% V/s 72.3% expected and V/s 69.7% in 2QFY2015. However, in spite of the

Abs. (%)

3m 1yr 3yr

same, the OPM came in at 22.5% V/s 22.0% expected and V/s 20.5% in

Sensex

4.1

42.1

60.3

2QFY2015. The net profit consequently came in at `36.5cr V/s `35.6cr expected

Dishman

15.1

104.3

165.1

and V/s `33.4cr in 2QFY2015, a yoy growth of 9.4%. The other income during

the period came in at `15.1cr V/s `7.8cr in 2QFY2015.

3-year price chart

Outlook and valuation: We expect Dishman’s net sales and net profit to grow at a

450

CAGR of 10.0% and 15.9%, respectively, over FY2015-17E. At current levels,

400

350

Dishman is trading at 16.5x its FY2017E earnings. We believe the current

300

250

valuations are fair, discounting the recovery well; hence, we maintain our Neutral

200

rating on the stock.

150

100

Key financials (Consolidated)

50

0

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

2

2

2

3

3

3

3

4

4

4

4

5

5

5

5

1

1

1

1

1

1

1

1

1

1

1

1

1

1

1

Net sales

y

g

v

b

y

g

v

b

y

g

v

b

y

g

v

1,373

1,575

1,733

1,906

a

u

o

e

a

u

o

e

a

u

o

e

a

u

o

M

A

N

F

M

A

N

F

M

A

N

F

M

A

N

% chg

8.3

14.7

10.0

10.0

Net profit

109.2

119.8

137.0

160.9

Source: Company, Angel Research

% chg

10.7

9.6

14.4

17.4

EPS (`)

13.5

14.8

17.0

19.9

EBITDA margin (%)

23.3

19.9

21.5

21.5

P/E (x)

24.3

22.2

19.4

16.5

RoE (%)

9.8

9.9

10.5

11.2

RoCE (%)

10.2

7.2

8.7

9.5

P/BV (x)

2.2

2.1

1.9

1.8

Sarabjit Kour Nangra

EV/Sales (x)

2.5

2.2

2.0

1.7

+91 22 3935 7800 Ext: 6806

EV/EBITDA (x)

10.9

11.0

9.4

8.0

Source: Company, Angel Research; Note: CMP as of November 19, 2015

Please refer to important disclosures at the end of this report

1

Dishman Pharmaceuticals | 2QFY2016 Result Update

Exhibit 1: 2QFY2016 performance (Consolidated)

Y/E March (` cr)

2QFY2016

1QFY2016

% chg qoq

2QFY2015

% chg yoy 1HFY2016 1HFY2015

% chg

Net sales

374

400

(6.6)

392

(4.8)

774

754

2.6

Other income

15

5

226.4

8

92.6

20

13

51.8

Total income

389

405

(3.9)

400

(2.8)

793

767

3.4

Gross profit

283

318

(10.8)

273

3.6

601

531

13.2

Gross margins

75.8

79.4

69.7

77.7

70.4

Operating profit

84

104

(19.2)

81

3.8

188

155

21.2

OPM (%)

22.5

26.0

20.6

24.3

20.6

Interest

24

32

(26.0)

18

34.8

55

38

45.8

Dep & amortisation

26

26

0.7

24

8.9

52

55

(4.6)

PBT

49

51

(2.7)

47

4.4

100

75

32.8

Provision for taxation

13

13

(0.7)

14

(7.5)

26

19

36.6

Reported net profit

37

38

(3.3)

33

9.4

74

57

29.9

Less : Exceptional items

-

-

-

-

-

-

Minority interest

-

-

-

0

0

PAT after exceptional items

37

38

(3.3)

33

9.4

74

57

29.9

Adj. PAT

37

38

(3.3)

33

9.4

74

57

29.9

EPS (`)

4.5

4.7

4.1

9.2

7.1

Source: Company, Angel Research

Exhibit 2: 2QFY2016 - Actual Vs Angel estimates

(` cr)

Actual

Estimates

Variation

Net sales

374

429

(12.9)

Other income

15

8

92.6

Operating profit

84

90

(6.7)

Interest

24

25

(5.6)

Tax

24

15

62.4

Net profit

37

36

2.6

Source: Company, Angel Research

Revenue below expectation: Sales for 2QFY2016 declined by 4.8% yoy to `374cr

V/s an expected `429cr and V/s `392cr in 2QFY2015. The CRAMS (`269.6cr)

segment posted a decline of 4.1%, while the other segment (`103.9cr) posted a

dip of 6.4% yoy.

Carbogen Amcis (CRAMS) (`188.4cr of revenue in 2QFY2016) de-grew by 5.4%

yoy, while the Indian CRAMS (`57.0cr of revenue in 2QFY2016) de-grew by 9.4%

yoy. Other CRAMS - UK (`24.3cr of revenue in 2QFY2016) posted a growth of

26.6% yoy. Carbogen Amcis’ revenues declined as a result of minimum inventory

build-up as required by the customers before actual sales. Hence the sales for the

quarter will be realized in 3QFY2016. Dishman India focused more on high

margin orders which resulted in lower revenues. CRAMS UK revenues witnessed

healthy growth driven by strong non-GMP orders from customers.

The MM segment posted sales of `104.0cr, a yoy de-growth of 6.4%. The Vitamin

D business grew by 7.9% yoy to `53cr, while others posted a de-growth of 17.8%

yoy during the period.

November 20, 2015

2

Dishman Pharmaceuticals | 2QFY2016 Result Update

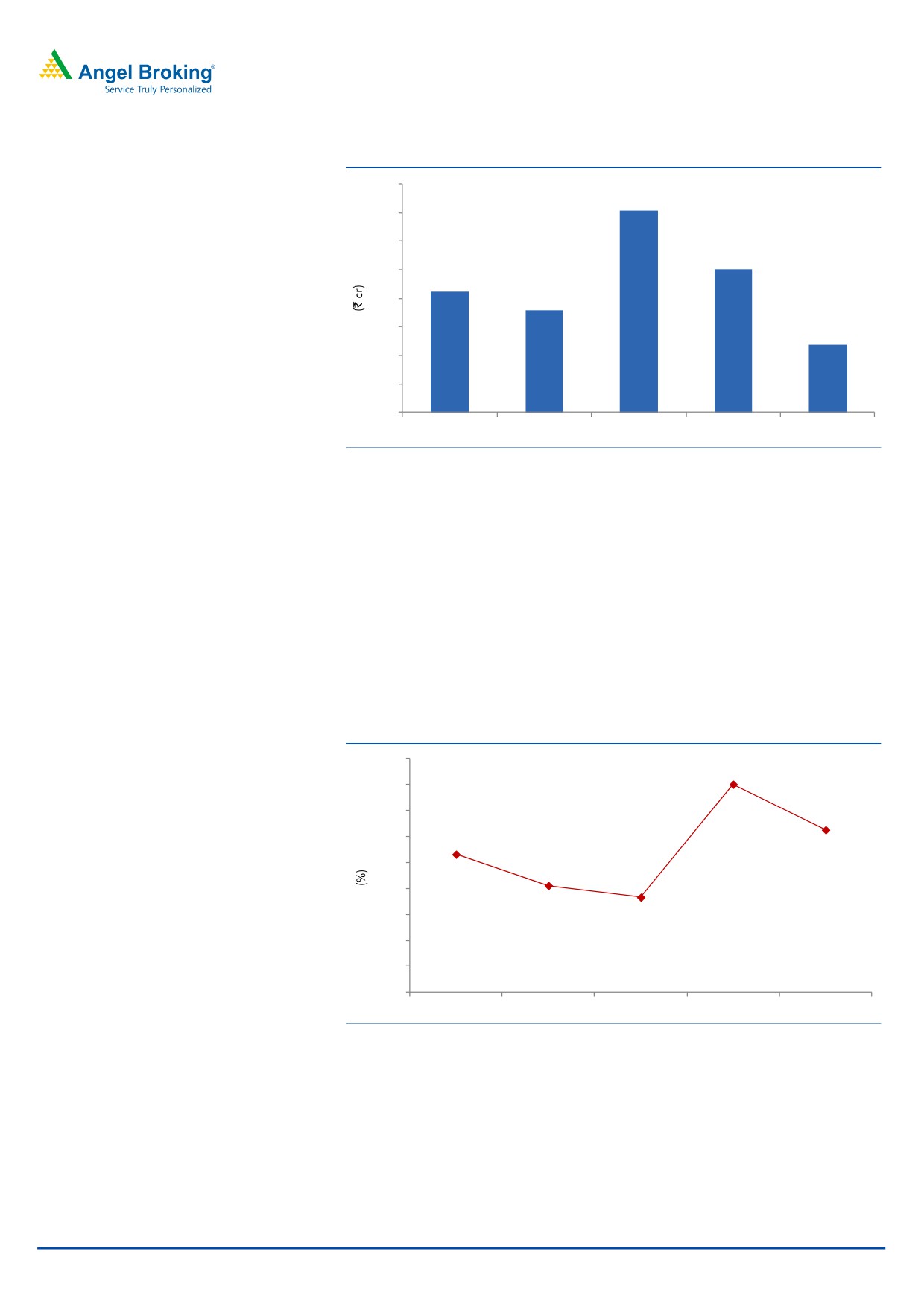

Exhibit 3: Sales trend

430

421

420

410

400

400

392

390

386

380

374

370

360

350

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

Source: Company, Angel Research

OPM above expectation: On the operating front, the GPM came in at 75.8% V/s

72.3% expected and V/s 69.7% in 2QFY2015. The OPM came in at 22.5% V/s

22.0% expected and V/s 20.5% in 2QFY2015. In terms of segments, CRAMS India

and Carbogen Amcis majorly focused on high margin orders.

The Vitamin D segment witnessed higher margins due to focus on high value

products like cholesterol and certain Vitamin D analogues. Further the segment

also benefitted from bulk purchase of raw materials at lower prices. The Others

segment witnessed healthy margins driven by profitable operations at the China

facility which recorded a 40% EBITDA margin during 2QFY2016.

Exhibit 4: OPM trend (%)

28.0

26.0

26.0

24.0

22.5

22.0

20.6

20.0

18.2

18.0

16.0

17.3

14.0

12.0

10.0

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

Source: Company, Angel Research

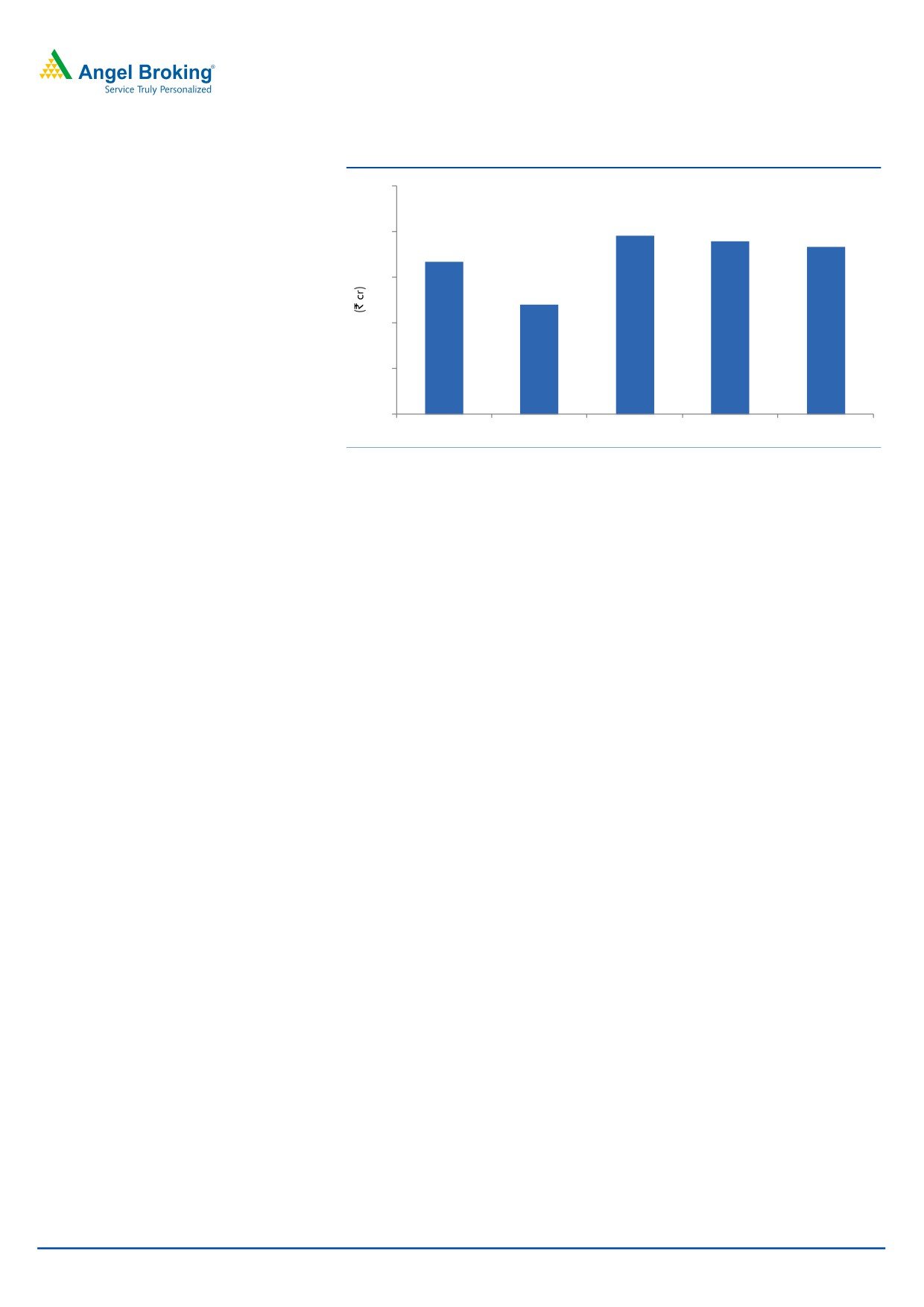

Net profit marginally higher than expectation: The net profit consequently came in

at `36.5cr V/s `35.6cr expected and V/s `33.4cr in 2QFY2015, a yoy growth of

9.4%. The other income during the quarter came in at `15.1cr V/s `7.8cr in

2QFY2015.

November 20, 2015

3

Dishman Pharmaceuticals | 2QFY2016 Result Update

Exhibit 5: Net profit trend

50

39

40

38

37

33

30

24

20

10

0

2QFY2015

3QFY2015

4QFY2015

1QFY2016

2QFY2016

Source: Company, Angel Research

Investment arguments

Focus on profitability: Dishman has been incurring a capex of around

~`100cr on an annual basis over the last couple of years. With the major

capex out, the company is now focused on improving the overall profitability

of the business. The same is evident in the improvement in OPM from 16.4%

in FY2011 to 23.3% in FY2014, thereby improving the overall profitability of

the company. The RoCE of the company improved from 5.5% in FY2011 to

10.2% in FY2014. Going forward, with focus on profitability, the company has

reduced its capex plans (~`30-50cr in FY2015) and lays focus on sweating its

assets and restructuring the business, which will lead to improvement in

profitability over the medium term. We expect the ROCE to improve to 9.5% in

FY2017E from 7.7% in FY2012.

CRAMS stabilizing: CRAMS, which contributes by around 65.1% to the overall

business has stabilised over the last two years, after a lull, posting a robust

growth of 14% in FY2012-14. As of March 2015, Carbogen Amcis has a

budgeted total order book of over `673cr for FY2016 and a part of the same

is in hands. In its Oncology Hippo Unit 9, the Management expects to book

more incremental revenues, where EBITDA margins are high at 40-50%. As

regards the Vitamin-D business, the Management expects to scale it up to

`300cr with a 20% EBITDA margin.

Outlook and valuation

We expect Dishman’s net sales and net profit to grow at a CAGR of 10.0% and

15.9%, respectively, over FY2015-17E. At current levels, Dishman is trading at

16.5x its FY2017E earnings. We believe the current valuations are fair, discounting

the recovery well; hence, we maintain our Neutral rating on the stock.

November 20, 2015

4

Dishman Pharmaceuticals | 2QFY2016 Result Update

Exhibit 6: One-year forward PE

600

500

400

300

200

100

-

2x

6x

10x

14x

Source: Company, Angel Research

Exhibit 7: Recommendation summary

Company

Reco

CMP Tgt. price Upside

FY2017E

FY15-17E

FY2017E

(`)

(`)

% PE (x) EV/Sales (x) EV/EBITDA (x) CAGR in EPS (%) RoCE (%) RoE (%)

Alembic Pharma

Neutral

653

-

-

27.3

3.9

19.2

26.1

30.3

30.2

Aurobindo Pharma Accumulate

817

872

6.7

18.7

3.0

13.1

15.6

23.5

30.2

Cadila Healthcare

Neutral

412

-

-

23.4

3.5

16.0

24.6

25.2

29.0

Cipla

Neutral

635

-

-

22.0

3.0

15.7

21.4

17.1

16.8

Dr Reddy's

Buy

3,287

3,933

19.7

18.4

2.8

11.9

17.2

19.1

20.6

Dishman Pharma

Neutral

329

-

-

16.5

1.7

8.1

15.9

9.5

11.7

GSK Pharma*

Neutral

3,145

-

-

46.0

8.0

36.3

6.6

33.7

34.3

Indoco Remedies

Neutral

306

-

-

22.5

2.4

13.4

23.0

19.7

19.7

Ipca labs

Buy

774

900

16.3

27.6

2.7

14.7

17.9

11.8

14.0

Lupin

Neutral

1,807

-

-

26.4

4.6

16.9

13.1

29.6

24.7

Sanofi India*

Neutral

4,483

-

-

29.6

3.9

18.6

33.1

27.9

25.5

Sun Pharma

Buy

743

950

27.9

27.6

4.8

15.7

8.4

15.8

16.6

Source: Company, Angel Research; Note: *December year ending

Background

Dishman commenced business in

1983 as a QUAT (Speciality Chemicals)

company and has since emerged to be a global leader in the segment. Since

1997, Dishman has diversified its interests towards the CRAMS segment. The

company has now established itself as a respected and preferred outsourcing

partner to various pharma majors, offering a portfolio of development, scale-up

and manufacturing services. The company caters to the customers' needs ranging

from chemical development to commercial manufacture and supply of APIs.

Dishman has large scale manufacturing facilities in India and China.

November 20, 2015

5

Dishman Pharmaceuticals | 2QFY2016 Result Update

Profit & Loss Statement (Consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Gross sales

1,127

1,273

1,387

1,582

1,750

1,925

Less: Excise duty

6

6

14

7

17

19

Net sales

1,121

1,268

1,373

1,575

1,733

1,906

Other operating income

3

5

12

44

44

44

Total operating income

1,124

1,272

1,385

1,619

1,776

1,950

% chg

13.4

13.2

8.9

16.9

9.7

9.8

Total expenditure

900

982

1,053

1,262

1,361

1,495

Net raw materials

384

376

373

535

485

515

Other mfg costs

83

95

103

77

130

143

Personnel

294

351

412

423

533

604

Other

139

161

164

227

213

233

EBITDA

222

285

320

314

372

411

% chg

36.7

28.7

12.2

(2.1)

18.6

10.4

(% of Net Sales)

19.8

22.5

23.3

19.9

21.5

21.5

Depreciation & amortisation

77

84

109

151

163

166

EBIT

145

202

212

163

209

245

% chg

55.4

38.8

5.0

(23.0)

28.5

16.9

(% of Net Sales)

13.0

15.9

15.4

10.3

12.1

12.8

Interest & other charges

73

79

92

90

95

99

Other Income

13

15

25

42

25

25

(% of PBT)

15.2

10.8

15.8

26.5

13.7

11.7

Share in profit of associates

-

-

-

-

-

-

Recurring PBT

88

143

156

159

183

215

% chg

(4.0)

61.4

9.5

1.8

14.7

17.4

Extraordinary expense/(Inc.)

0.4

(2.4)

0.2

PBT (reported)

88

145

156

159

183

215

Tax

31.2

45.0

47.1

39.4

45.7

53.6

(% of PBT)

35.4

31.0

30.1

24.8

25.0

25.0

PAT (reported)

57

100

109

120

137

161

Add: Share of earnings of asso.

-

0

0

-

-

-

Less: Minority interest (MI)

-

-

-

-

-

-

Prior period items

(0)

-

-

-

-

-

PAT after MI (reported)

57

100

109

120

137

161

ADJ. PAT

57

99

109

120

137

161

% chg

(28.7)

73.1

10.7

9.6

14.4

17.4

(% of Net Sales)

5.1

7.9

8.0

7.6

7.9

8.4

Basic EPS (`)

7.1

12.2

13.5

14.8

17.0

19.9

Fully Diluted EPS (`)

7.1

12.2

13.5

14.8

17.0

19.9

% chg

(28.7)

73.1

10.7

9.6

14.4

17.4

November 20, 2015

6

Dishman Pharmaceuticals | 2QFY2016 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

SOURCES OF FUNDS

Equity share capital

16

16

16

16

16

16

Share application money

2

4

4

-

-

-

Reserves & surplus

914

1,026

1,161

1,222

1,347

1,497

Shareholders funds

932

1,046

1,181

1,238

1,363

1,513

Minority interest

-

-

-

-

-

-

Total loans

850

800

880

836

900

900

Other Long Term Liabilities

66

10

0

73

73

73

Long Term Provisions

41

43

64

97

97

97

Deferred tax liability

45

58

68

63

63

63

Total liabilities

1,933

1,956

2,193

2,307

2,496

2,646

APPLICATION OF FUNDS

Gross block

1,264

1,686

1,946

2,019

2,049

2,099

Less: Acc. depreciation

440

524

688

813

976

1,142

Net block

824

1,162

1,258

1,206

1,073

957

Capital work-in-progress

418

97

79

142

142

142

Goodwill

209

211

247

235

235

235

Long-Term Loans and Adv.

26

25

25

38

38

38

Investments

155

123

182

188

230

253

Current Assets

626

673

760

1,000

1,208

1,529

Cash

24

21

35

36

49

254

Loans & Advances

146

241

269

299

327

360

Other

457

581

457

665

832

915

Current liabilities

326

335

361

502

430

508

Net Current Assets

301

338

399

498

778

1,021

Non CA

-

-

2

-

-

-

Total Assets

1,933

1,956

2,193

2,307

2,496

2,646

November 20, 2015

7

Dishman Pharmaceuticals | 2QFY2016 Result Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015 FY2016E FY2017E

Profit before tax

88

145

156

159

183

215

Depreciation

77

84

109

151

163

166

(Inc)/Dec in Working Capital

27

(178)

63

(103)

(310)

(60)

Less: Other income

13

15

25

42

25

25

Direct taxes paid

(31)

(45)

(47)

(39)

(46)

(54)

Cash Flow from Operations

173

144

179

180

181

182

(Inc.)/Dec.in Fixed Assets

(215)

(101)

(242)

(136)

(30)

(50)

(Inc.)/Dec. in Investments

0

-

-

-

-

-

Other income

13

15

25

42

25

25

Cash Flow from Investing

(201)

(85)

(217)

(94)

(5)

(25)

Issue of Equity

-

-

-

-

-

-

Inc./(Dec.) in loans

47

(105)

92

62

64

-

Dividend Paid (Incl. Tax)

(10)

(11)

(11)

(11)

(11)

(11)

Others

(27)

54

312

39

23

72

Cash Flow from Financing

10

(62)

393

90

76

61

Inc./(Dec.) in Cash

(18)

(3)

354

176

252

218

Opening Cash balances

43

24

21

35

36

49

Closing Cash balances

24

21

35

36

49

254

November 20, 2015

8

Dishman Pharmaceuticals | 2QFY2016 Result Update

Key Ratio

Y/E March

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

46.5

26.9

24.3

22.2

19.4

16.5

P/CEPS

19.9

14.4

12.2

9.8

8.9

8.1

P/BV

2.8

2.5

2.2

2.1

1.9

1.8

Dividend yield (%)

0.4

0.4

0.4

0.4

0.4

0.4

EV/Sales

3.1

2.7

2.5

2.2

2.0

1.7

EV/EBITDA

15.7

12.0

10.9

11.0

9.4

8.0

EV / Total Assets

1.8

1.8

1.6

1.5

1.4

1.2

Per Share Data (`)

EPS (Basic)

7.1

12.2

13.5

14.8

17.0

19.9

EPS (fully diluted)

7.1

12.2

13.5

14.8

17.0

19.9

Cash EPS

16.5

22.8

27.0

33.5

37.1

40.5

DPS

1.2

1.2

1.2

1.2

1.2

1.2

Book Value

115.5

129.6

146.4

153.4

169.0

187.5

Dupont Analysis

EBIT margin

13.0

15.9

15.4

10.3

12.1

12.8

Tax retention ratio

64.6

69.0

69.9

75.2

75.0

75.0

Asset turnover (x)

0.6

0.7

0.7

0.7

0.8

0.8

ROIC (Post-tax)

5.1

7.3

7.3

5.7

6.8

7.8

Cost of Debt (Post Tax)

5.5

6.6

7.7

7.9

8.3

8.3

Leverage (x)

0.9

0.8

0.7

0.7

0.6

0.5

Operating ROE

4.8

7.8

7.0

4.2

5.9

7.5

Returns (%)

ROCE (Pre-tax)

7.7

10.4

10.2

7.2

8.7

9.5

Angel ROIC (Pre-tax)

11.3

13.9

12.2

8.7

10.6

12.0

ROE

6.3

10.0

9.8

9.9

10.5

11.2

Turnover ratios (x)

Asset Turnover (Gross Block)

0.9

0.9

0.8

0.8

0.9

0.9

Inventory / Sales (days)

96

99

100

106

117

135

Receivables (days)

53

47

20

21

24

27

Payables (days)

48

46

34

36

34

28

WC cycle (ex-cash) (days)

90

85

90

93

122

140

Solvency ratios (x)

Net debt to equity

0.9

0.7

0.7

0.6

0.6

0.4

Net debt to EBITDA

3.7

2.7

2.6

2.5

2.3

1.6

Interest Coverage (EBIT / Int.)

2.0

2.6

2.3

1.8

2.2

2.5

November 20, 2015

9

Dishman Pharmaceuticals | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Dishman Pharmaceuticals

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 20, 2015

10