2QFY2016 Result Update | Automobiles

November 17, 2015

Competent Auto

NEUTRAL

CMP

`144

Performance Highlights

Target Price

-

Y/E March (` cr)

2QFY16 2QFY15

% chg (yoy) 1QFY16

% chg (qoq)

Investment Period

-

Net sales

220

196

12.2

237

(7.2)

EBITDA

6

5

16.2

6

(6.4)

Stock Info

EBITDA Margin (%)

2.7

2.6

9bp

2.7

2bp

Adjusted PAT

2.6

2.1

21.6

2.3

9.8

Sector

Automobiles

Source: Company, Angel Research

Market Cap (` cr)

89

For 2QFY2016, Competent Auto (Competent) reported a decent set of numbers.

Net Debt

(10.5)

The top-line for the quarter grew by 12.2% yoy to `220cr, which is slightly lower

Beta

1.2

than our estimate of `226cr. The revenue growth is in-line with growth reported

by Maruti Suzuki in 2QFY2016, where its top-line grew by 13.1% yoy largely

52 Week High / Low

240 / 78

owing to 10% volume growth. The EBIDTA for the quarter came in at `6cr as

Avg. Daily Volume

8,196

against `5cr in the corresponding quarter a year ago. The EBIDTA margin for the

Face Value (`)

10

quarter improved by 9bp yoy to 2.7% as against 2.6% in 2QFY2015. The interest

BSE Sensex

25,760

expense for the quarter grew by 40% yoy to `1.6cr as against `1.2cr in 2QFY2015.

Consequently, the net profit came in at `2.6cr, growing by 21.6% on a yoy basis.

Nifty

7,807

Reuters Code

CPA.BO

Proxy play on Maruti’s growth: The top-line performance of the company is

closely linked to the performance of Maruti Suzuki (MSIL). We expect MSIL to post

Bloomberg Code

CPA.IN

robust volume growth in the domestic market going ahead on back of new

launches which will be replicated by Competent. Also, we expect the market share

Shareholding Pattern (%)

of the company to remain stable/improve, as entry of a new dealer seems to be

Promoters

74.9

commercially unviable with property prices having soared significantly in the Delhi

region. Further, higher vehicle sales would likely get converted into greater demand

MF / Banks / Indian Fls

0.0

for after sale services, thus bringing in additional revenue for the company.

FII / NRIs / OCBs

0.0

Scalable business model with healthy balance-sheet: The company has a scalable

Indian Public / Others

25.1

business model which will enable it to report sustainable revenue growth going

ahead. The company has increased its short term debt in 1HFY2016E ahead of

Abs.(%)

3m 1yr

3yr

the festive season mainly utilizing the funds for inventory. We expect the debt level

to return to normal levels by the year end.

Sensex

(7.6)

(8.6)

40.7

Competent

(16.6)

79.4

167.0

Outlook and Valuations: We believe that Competent will continue to benefit from

its established position in the automobile dealership market in Delhi, Haryana,

and Himachal Pradesh, and from its conducive relationship with its principal,

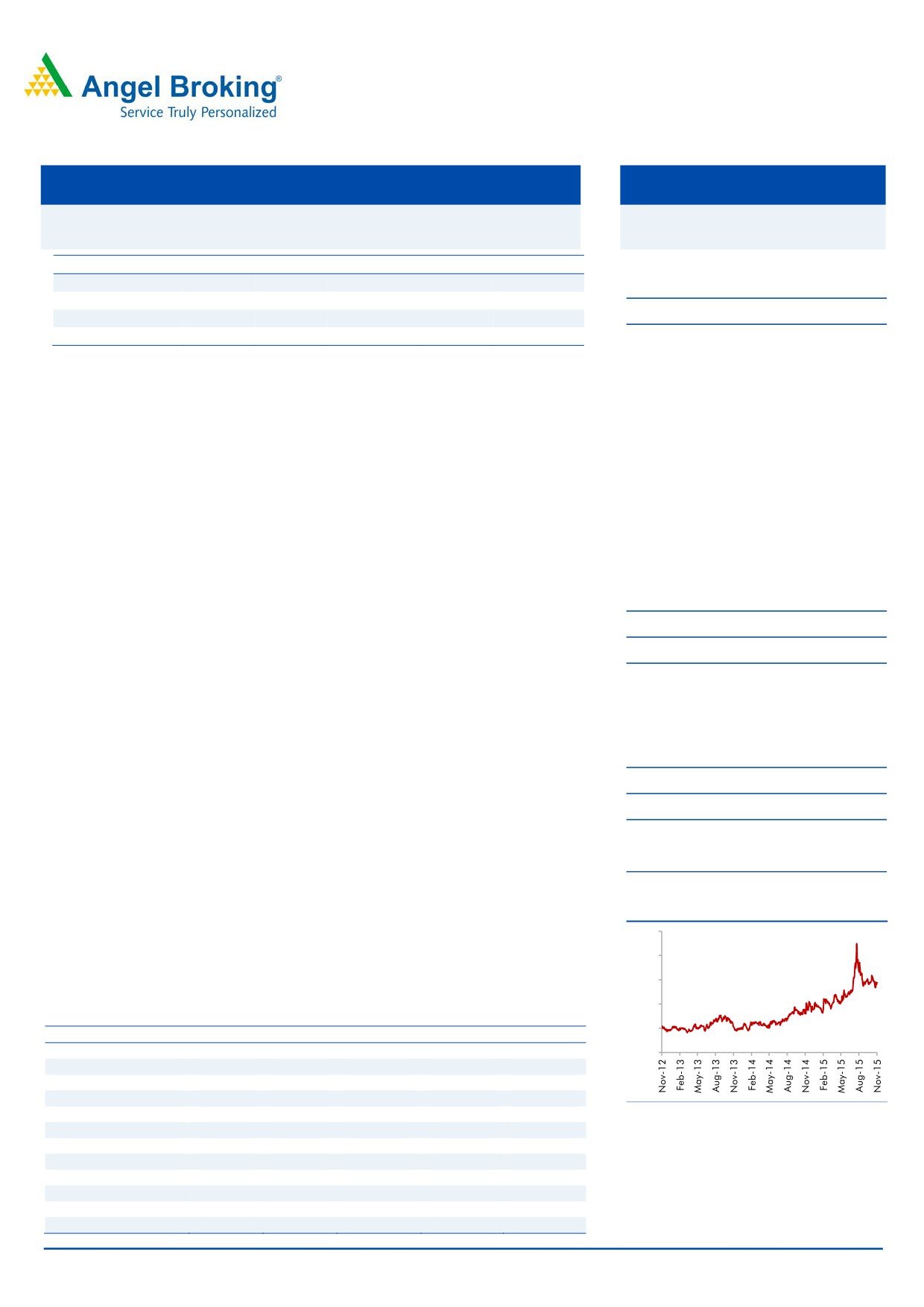

3-Year Daily Price Chart

MSIL. During FY2015-17, we expect the company to register a top-line and

250

bottom-line CAGR of 10.9% and 21.7%, to `1,137cr and `17cr, respectively.

200

Currently, the stock trades at 5.1x its FY2107E earnings. We have a Neutral

150

rating on the stock.

100

Key financials

50

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

Net Sales

788

808

924

1040

1137

-

% chg

11.2

2.6

14.4

12.5

9.3

Net Profit

8

9

12

16

17

% chg

7.0

17.6

26.6

36.3

8.7

EBITDA Margin (%)

2.5

2.5

2.8

3.2

3.1

Source: Company, Angel Research

FDEPS (`)

12.7

14.9

18.9

25.7

28.0

P/E (x)

11.4

9.6

7.6

5.6

5.1

P/BV (x)

1.2

1.1

1.0

0.8

0.7

RoE (%)

10.8

11.4

12.7

15.0

14.3

RoCE (%)

16.3

15.3

16.0

20.7

19.6

Milan Desai

EV/Sales (x)

0.1

0.1

0.1

0.1

0.1

+91 22 3935 3600 Ext: 6846

EV/EBITDA (x)

5.4

5.0

3.0

2.2

1.8

Source: Company, Angel Research; Note: CMP as of November16, 2015

Please refer to important disclosures at the end of this report

1

Competent Auto | 2QFY2016 Result Update

Exhibit 1: 2QFY2016 performance highlights

Y/E March (` cr)

2QFY16

2QFY15

% chg (yoy)

1QFY16

% chg (qoq)

1HFY16

1HFY15

% chg

Total operating income

220

196

12.2

237

(7.2)

457

405

12.7

Purchase of Stock in Trade

193

174

10.7

211

(8.7)

403

362

11.5

(% of Sales)

87.6

88.8

(115)bp

89.0

(140)bp

88.3

89.3

(94)bp

Employee cost

7

6

23.6

7

7.8

14

12

18.6

(% of Sales)

3.2

2.9

30bp

2.8

45bp

3.0

2.8

15bp

Other Expenses

14

11

27.1

13

8.3

27

22

25.1

(% of Sales)

6.5

5.7

76bp

5.6

93bp

6.0

5.4

60bp

Total expenditure

214

191

12.1

231

(7.2)

444

395

12.5

EBITDA

5.9

5.1

16.2

6

(6.4)

12

10

21.6

EBITDA Margin (%)

2.7

2.6

9bp

2.7

2bp

2.7

2.5

20bp

Interest

1.6

1.2

40.0

1.6

5.5

3

2

45.0

Depreciation

1

1

(17.5)

2

(46.0)

2

2

23.7

Other income

0.3

0.3

(9.1)

0.3

(16.6)

1

0

14.2

PBT

4

3

15.9

4

4.8

7

6

12.4

(% of Sales)

1.7

1.6

1.5

1.6

1.6

Tax

1.1

1.1

4.7

1.2

(5.1)

2

2

7.0

(% of PBT)

30.5

33.8

33.7

32.0

33.6

Reported PAT

2.6

2.1

21.6

2.3

9.8

5

4

15.1

Exceptional items

0

0

0

0

0

Adjusted PAT

2.6

2.1

21.6

2.3

9.8

5

4

15.1

PATM (%)

1.2

1.1

1.0

1.1

1.0

Source: Company, Angel Research

Exhibit 2: Actual v/s Angel’s estimates

Actual v/s Angel's Estimates

Actual (`cr)

Estimate (` cr)

% variation

Total Income (`cr)

220

226

(2.7)

EBITDA (`cr)

5.9

7.5

(21.0)

EBITDA Margin (%)

2.7

3.3

70bp

Adjusted PAT (`cr)

2.6

3.6

(28.8)

Source: Company, Angel Research

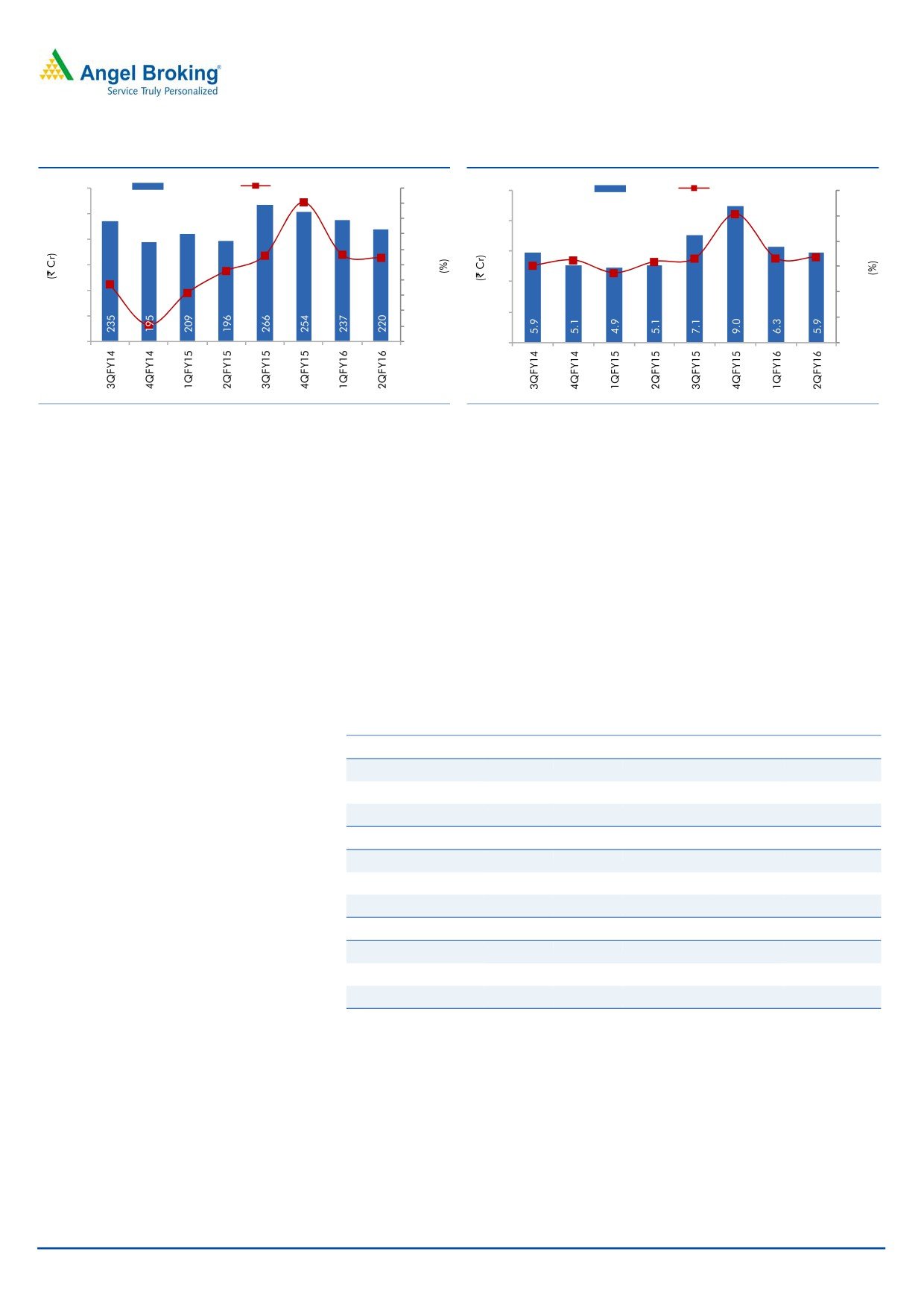

Strong performance continues

For 2QFY2016, Competent reported a decent set of numbers. The top-line for the

quarter grew by 12.2% yoy to `220cr, which is slightly lower than our estimate of

`226cr. The revenue growth is in-line with domestic revenue growth reported by

Maruti Suzuki in 2QFY2016, where the revenue grew by 17.5% yoy largely owing

to 12.4% volume growth. The EBIDTA for the quarter came in at `6cr as against

`5cr in the corresponding quarter a year ago. The EBIDTA margin for the quarter

improved by 9bp yoy to 2.7% as against 2.6% in 2QFY2015. The interest expense

for the quarter grew by 40% yoy to `1.6cr as against `1.2cr in 2QFY2015.

Consequently, the net profit came in at `2.6cr, growing by 21.6% on a yoy basis.

November 17, 2015

2

Competent Auto | 2QFY2016 Result Update

Exhibit 3: Sales growth continues

Exhibit 4: Operating performance

300

Net Sales

Sales yoy growth

35.0

EBIDTA

EBIDTA margins

10

4.0

30.3

30.0

3.5

250

3.5

25.0

8

20.0

2.7

200

2.7

3.0

2.5

15.0

2.6

2.6

13.2

6

2.4

2.7

12.9

12

.2

150

10.0

2.5

7.9

5.0

4

3.5

100

2.0

0.7

-

(9.7)

(5.0)

2

50

1.5

(10.0)

-

(15.0)

-

1.0

Source: Company, Angel Research

Source: Company, Angel Research

Segmental performance

For 2QFY2016, Showroom revenues grew by 12.2% yoy to `197cr. EBIT for the

segment came in at `2.5cr, an increase of 8.6% yoy. The segment’s EBIT margin at

1.3% remained flat on both yoy and qoq basis. During the same period, MSIL

reported a 17.5% yoy revenue growth in the domestic market. MSIL’s volumes

grew 12.4% on a yoy basis coupled with realization growth of ~4.5% yoy during

the quarter.

For 2QFY2016, Services and spares revenue grew by 12.3% yoy to `23cr. EBIT

improved to `2.6cr, a 46.1% increase on a yoy basis, with EBIT margin improving

to 11.2% as against 8.6% in 2QFY2015.

Exhibit 5: Segment-wise performance

Y/E Mar (` cr)

2QFY16

2QFY15

% chg (yoy) 1QFY16

% chg (qoq)

Total Revenue

Showroom

197

175

12.2

213

(7.8)

Services and Spares

23

20

12.3

23

(2.1)

Total

254

195

30.3

266

(4.4)

EBIT

Showroom

2.5

2.3

8.6

2.9

(13.5)

Services and Spares

2.6

1.8

46.1

2

36.9

Total

5.4

4.2

29.4

6.2

(11.8)

EBIT Margin (%)

Showroom

1.3

1.3

70.6

1.3

(8)bp

Services and Spares

11.2

8.6

374.3

8.0

319bp

Source: Company, Angel Research

November 17, 2015

3

Competent Auto | 2QFY2016 Result Update

Investment Rationale

Proxy play to Maruti: The top-line performance of the company is closely linked to

the performance of MSIL. We expect MSIL to post robust volume CAGR of 12.6%

over FY2015-17E, which will translate to better top-line for Competent. Also, we

expect Competent’s market share to remain stable/improve, as entry of a new

dealer seems to be commercially unviable with property prices having soared

significantly in the Delhi region. Competent is also likely to benefit from MSIL’s

plan to launch new products in the new segments in order to outgrow the market.

With lower fuel prices scenario prevailing, we expect Competent to benefit from

favorable outlook for MSIL.

Further, higher vehicle sales would likely get converted into greater demand for

after sale services, thus bringing in additional revenue for Competent. All these

factors augur well for Competent’s future financial performance.

Scalable business model with healthy balance sheet: The company

operates in two segments, namely Showroom and Services & Spares. The

Showroom segment deals with purchase and sale of vehicles manufactured by

MSIL. The Service and Spares segment includes servicing of Maruti vehicles and

sale of their spare parts. The business model being scalable enables the company

to sustain its revenue growth trajectory. Further, the company is increasing focus

on its Service & Spares business where the margins are higher than the Showroom

business. The company has increased its short term debt in the 1HFY2016E ahead

of the festive season mainly utilizing the funds for inventory. We expect the

company to reduce this debt level by year end. With profitability expected to

improve due to decent revenue growth and improvement in margins, the return

ratios are expected to improve going ahead.

Exhibit 6: Return Ratios to improve...

23

20.7

19.6

19

16.3

15.8

15.9

16.0

15.3

15

15.0

14.3

11

12.7

12.1

11.2

11.4

10.8

7

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

ROE

ROCE (Pre-tax)

Source: Company, Angel Research

November 17, 2015

4

Competent Auto | 2QFY2016 Result Update

Company Financials

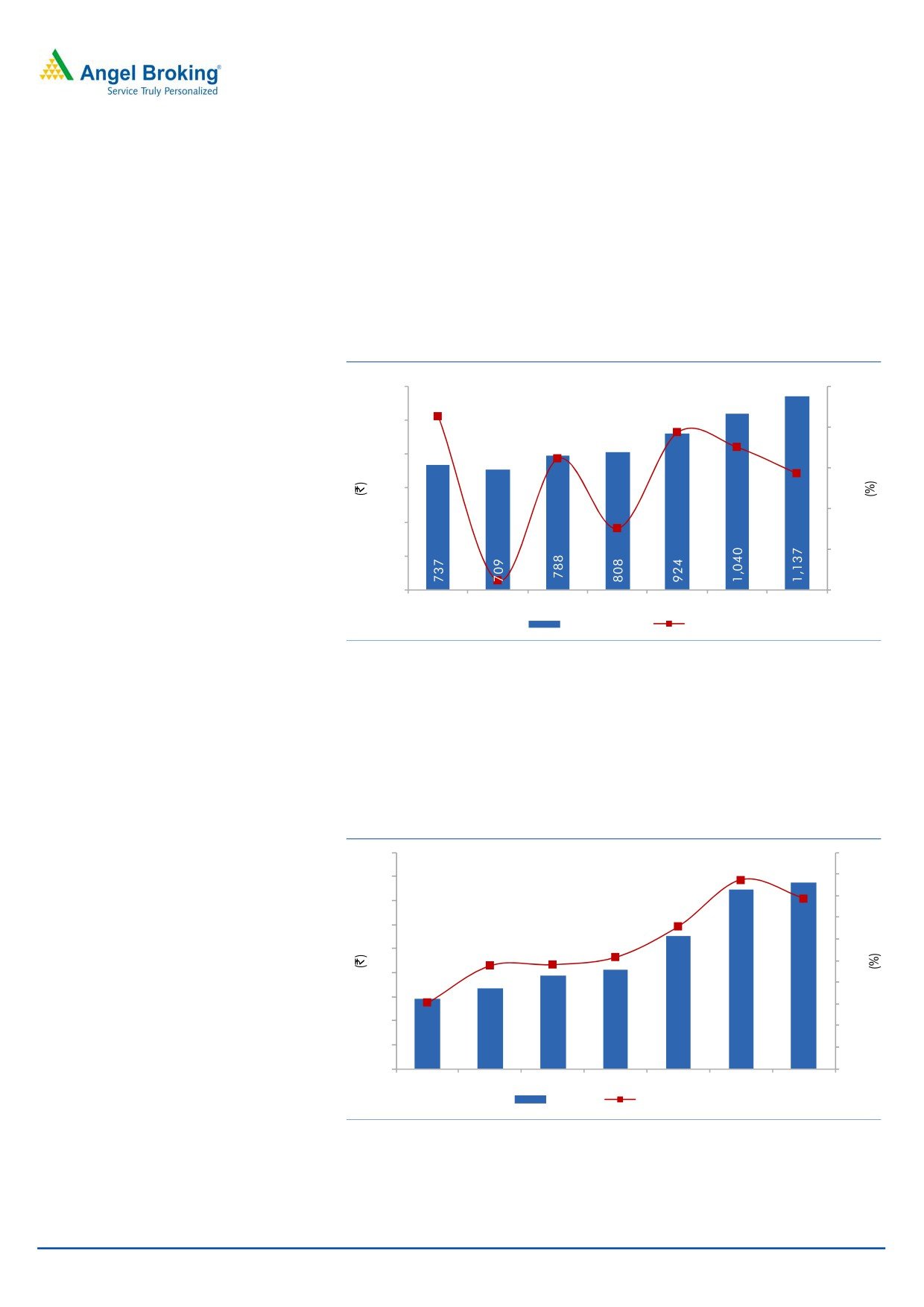

Net sales expected to post 10.9% CAGR over FY2015-17E

The top-line performance of the company is closely linked to the performance of

MSIL. We expect MSIL to post strong sales growth going ahead on account of new

product launches scheduled over the next one year. As a result, we expect

Competent to post a 10.9% CAGR in revenue over FY2015-17E to `1,137cr in

FY2017E.

Exhibit 7: Net sales and net sales growth

12.5

1,200

9.3

20.0

16.3

1,000

14.4

15.0

11.2

2.6

800

10.0

600

5.0

400

-

200

(3.8)

0

(5.0)

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

Net Sales

Sales growth

Source: Company, Angel Research

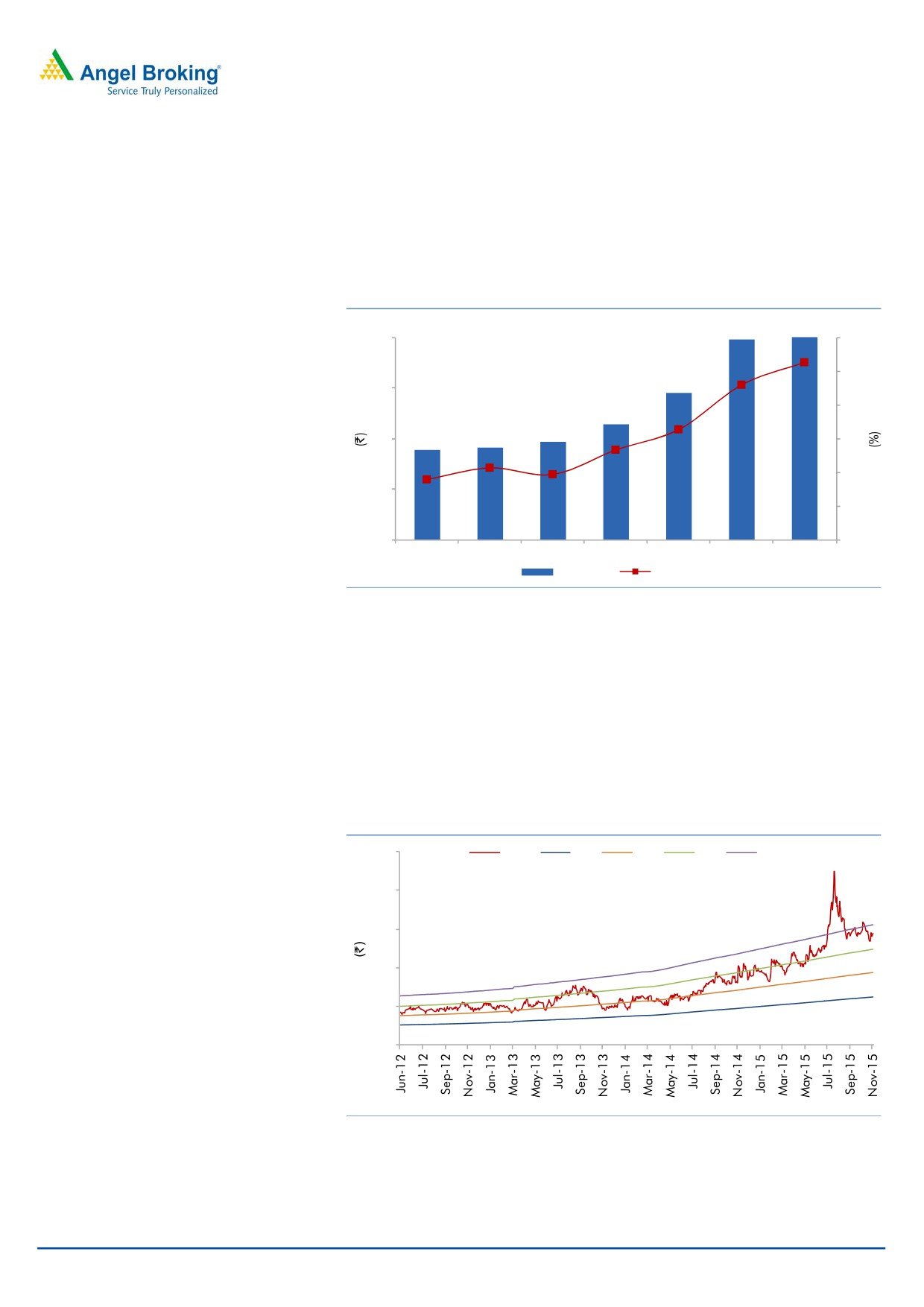

EBITDA to post 15.9% CAGR over FY2015-17

The company’s EBITDA is expected to rise from `26cr in FY2015 to `35cr in

FY2017. The EBITDA margin is expected to improve from 2.8% in FY2015 to 3.1%

in FY2017.

Exhibit 8: EBIDTA and EBIDTA margins to improve

40

3.5

3.2

3.1

3.3

36

3.1

32

2.8

2.9

28

2.5

2.7

24

2.5

2.5

2.5

20

2.1

2.3

16

2.1

12

1.9

8

1.7

16

17

19

20

26

34

35

4

1.5

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

EBIDTA

EBIDTA margins

Source: Company, Angel Research

November 17, 2015

5

Competent Auto | 2QFY2016 Result Update

Net profit to grow at 21.7% CAGR over FY2015-17

The company’s bottom-line is expected to get a boost from an estimated

improvement in its EBIDTA and EBIDTA margins; the bottom-line is expected to

grow at a CAGR of 21.7% over FY2015-17 to `17cr. As a result, the PAT margins

are expected to improve from 1.3% in FY2014 to 1.7% in FY2017.

Exhibit 9: PAT and PAT margins to improve

1.7

1.5

16

1.8

1.6

12

1.3

1.4

1.1

8

1.0

1.0

1.2

1.0

1.0

4

0.8

7

7

8

9

12

16

17

-

0.6

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E FY2017E

ADJ. PAT

PAT margins

Source: Company, Angel Research

Outlook and Valuation: We believe that Competent will continue to benefit

from its established position in the automobile dealership market in Delhi,

Haryana, and Himachal Pradesh, and from its conducive relationship with its

principal, MSIL. During FY2015-17, we expect the company to register a top-line

and bottom-line CAGR of 10.9% and 20.8%, to `1,137cr and `17cr, respectively.

Currently, the stock trades at 5.1x its FY2107E earnings. We have a Neutral rating

on the stock.

Exhibit 10: One-year forward P/E band

250

Price

2 x

3 x

4 x

5 x

200

150

100

50

0

Source: Company, Angel Research

November 17, 2015

6

Competent Auto | 2QFY2016 Result Update

Company Background

Competent Automobiles is mainly in the business of trading and servicing of

Maruti Suzuki (MSIL) vehicles. The company operates in two segments, namely,

Showroom and Services & Spares. The Showroom segment deals with sale of

vehicles manufactured by MSIL. Competent Automobiles has 14 Maruti Showroom

Network spread across Delhi NCR, Haryana and Himachal with State of Art facility

and customer support team at each dealership.

Key Risks

Unsatisfactory utilization of funds - Further diversion of cash in unrelated

business. The company invested `7.5cr (as on March 2014) in Raj Chopra &

Company Pvt Ltd, which is owned by Mr. Raj Chopra (CMD). As of 1HFY2016,

it appears that the company has invested additional amount taking the non-

current investment figure to `34cr for the period.

Increased competition due to entry of new players and appointment of new

dealers by MSIL. Launch of new models by competing OEMs to Maruti have

also increased market competition.

Higher inflation and interest rates coupled with significant increase in fuel

prices could hurt vehicle sales.

November 17, 2015

7

Competent Auto | 2QFY2016 Result Update

Profit and loss statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

Net Sales

788

808

924

1,040

1,137

Other operating income

-

-

-

-

-

Total operating income

788

808

924

1,040

1,137

% chg

11.2

2.6

14.4

12.5

9.3

Purchase of Stock in Trade

712

729

831

926

1014

% chg

14.5

2.4

13.9

11.4

9.5

Power and Fuel costs

2

2

2

4

5

% chg

(20.9)

33.8

3.3

73.0

9.3

Personnel

19

21

24

30

33

% chg

13.2

8.5

17.5

23.3

9.3

Other

35

35

41

46

51

% chg

(29.5)

0.8

14.8

14.3

9.5

Total Expenditure

768

788

898

1,007

1,102

EBITDA

19.4

20.5

26.0

33.7

34.9

% chg

11.5

5.4

27.2

29.6

3.5

EBITDA Margin

2.5

2.5

2.8

3.2

3.1

Depreciation & Amortisation

4

4

6

5

5

EBIT

15

17

20

29

30

% chg

12.2

8.7

17.1

46.2

3.3

(% of Net Sales)

2.0

2.1

2.1

2.8

2.6

Interest & other Charges

5

5

5

7

5

Other Income

1

1

1

1

1

(% of Net Sales)

0.1

0.2

0.1

0.1

0.1

Recurring PBT

11

12

15

22

24

% chg

9.0

12.7

21.0

50.7

9.3

PBT (reported)

11

14

16

24

26

Tax

4

4

4

8

8

(% of PBT)

32

33

28

33

33

PAT (reported)

8

9

12

16

17

Extraordinary Expense/(Inc.)

-

-

-

-

-

ADJ. PAT

8

9

12

16

17

% chg

7.0

17.6

26.6

36.3

8.7

(% of Net Sales)

1.0

1.1

1.3

1.5

1.7

Basic EPS (`)

12.7

14.9

18.9

25.7

28.0

Fully Diluted EPS (`)

12.7

14.9

18.9

25.7

28.0

% chg

7.0

17.6

26.6

36.3

8.7

November 17, 2015

8

Competent Auto | 2QFY2016 Result Update

Balance sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016E

FY2017E

SOURCES OF FUNDS

Equity Share Capital

6

6

6

6

6

Preference Capital

-

-

-

-

-

Reserves& Surplus

66

74

85

99

114

Shareholders’ Funds

72

80

91

106

120

Minority Interest

-

-

-

-

-

Total Loans

23

30

33

35

33

Other long term liabilities

0

0

0

0

0

Net Deferred tax liability

(0.6)

(0.4)

(1.4)

(1.4)

(1.4)

Total Liabilities

95

110

123

139

152

APPLICATION OF FUNDS

Gross Block

73

75

80

84

88

Less: Acc. Depreciation

29

32

38

43

48

Net Block

44

43

42

41

40

Capital Work-in-Progress

6

9

12

9

7

Lease adjustment

-

-

-

-

-

Goodwill

-

-

-

-

-

Investments

0

8

12

34

34

Other non-current assets

0

1

1

1

1

Current Assets

84

94

123

119

135

Cash

7

8

32

16

24

Loans & Advances

3

5

1

1

1

Other current assets

0

0

4

4

4

Current liabilities

45

51

73

72

74

Net Current Assets

39

43

50

46

62

Mis. Exp. not written off

-

-

-

-

-

Total Assets

95

110

123

139

152

November 17, 2015

9

Competent Auto | 2QFY2016 Result Update

Cash Flow Statement

Y/E March (` cr)

FY2013 FY2014 FY2015E FY2016E FY2017E

Profit before tax

11

14

16

24

26

Depreciation

4

4

6

5

5

(Inc.)/ Dec. in Working Capital

(1)

(1)

(1)

(1)

(1)

Less: Other income

(3)

(3)

17

(13)

(7)

Direct taxes paid

(4)

(4)

(4)

(8)

(8)

Cash Flow from Operations

8

9

34

7

14

(Inc.)/ Dec. in Fixed Assets

(12)

(5)

(7)

(1)

(2)

(Inc.)/ Dec. in Investments

3

(10)

(5)

(23)

(1)

Other income

1

1

1

1

1

Cash Flow from Investing

(8)

(13)

(11)

(23)

(1)

Issue of Equity

-

-

-

-

-

Inc./(Dec.) in loans

1

7

2

2

(2)

Dividend Paid (Incl. Tax)

(1)

(1)

(1)

(2)

(2)

Others

(1)

(1)

-

-

-

Cash Flow from Financing

(1)

5

2

0

(5)

Inc./(Dec.) in Cash

(0)

1

24

(16)

8

Opening Cash balances

7

7

8

32

16

Closing Cash balances

7

8

32

16

24

November 17, 2015

10

Competent Auto | 2QFY2016 Result Update

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

11.4

9.6

7.6

5.6

5.1

P/CEPS

7.6

6.9

4.9

4.3

4.0

P/BV

1.2

1.1

1.0

0.8

0.7

Dividend yield (%)

0.8

0.8

0.9

1.8

2.7

EV/Sales

0.1

0.1

0.1

0.1

0.1

EV/EBITDA

5.4

5.0

3.0

2.2

1.8

EV / Total Assets

1.1

0.9

0.6

0.5

0.4

Per Share Data (`)

EPS (Basic)

12.7

14.9

18.9

25.7

28.0

EPS (fully diluted)

12.7

14.9

18.9

25.7

28.0

Cash EPS

19.1

20.8

29.1

33.7

36.4

DPS

1.0

1.0

1.0

2.0

3.0

Book Value

117.5

131.0

148.6

171.7

195.8

Dupont Analysis

EBIT margin

2.0

2.1

2.1

2.8

2.6

Tax retention ratio

0.7

0.7

0.7

0.7

0.7

Asset turnover (x)

9.6

9.4

13.6

12.9

13.1

ROIC (Post-tax)

12.9

13.2

20.9

24.0

22.9

Cost of Debt (Post Tax)

13.7

10.5

10.7

12.6

11.1

Leverage (x)

0.2

0.2

(0.1)

(0.1)

(0.2)

Operating ROE

12.7

13.7

19.8

22.4

20.4

Returns (%)

ROCE (Pre-tax)

16.3

15.3

16.0

20.7

19.6

Angel ROIC (Pre-tax)

18.9

19.6

29.1

35.8

34.2

ROE

10.8

11.4

12.7

15.0

14.3

Turnover ratios (x)

Asset Turnover (Gross Block)

10.7

10.8

11.6

12.4

12.9

Inventory / Sales (days)

23

27

25

24

24

Receivables (days)

8

8

8

8

8

Payables (days)

21

23

24

25

24

WC cycle (ex-cash) (days)

14

15

11

9

11

Solvency ratios (x)

Net debt to equity

0.2

0.2

(0.1)

(0.1)

(0.2)

Net debt to EBITDA

0.8

0.7

(0.4)

(0.4)

(0.7)

Interest Coverage (EBIT / Int.)

3.3

3.7

4.0

4.4

5.5

November 17, 2015

11

Competent Auto | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Competent Auto

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

November 17, 2015

12