IPO Note | Capital Goods

July 31, 2017

Cochin Shipyard Ltd

SUBSCRIBE

sue Open: Aug 1, 2017

Is

A safe harbor for investments

Issue Close: Aug 3, 2017

Cochin Shipyard (CSL) is the largest Indian public sector shipyard and it received

“Miniratna” status in 2008. CSL operates a shipyard that provides shipbuilding

and ships repair services in both defence and non-defence spaces. CSL generates

Issue Details

74% from shipbuilding and 26% from ship repair.

Face Value: `10

Healthy order book indicates strong revenue visibility: CSL’s current order book

stands at `3,078cr (1.5x FY2017 revenue), this provides revenue visibility in the

Present Eq. Paid up Capital:

`113.28cr

near term. Defence sector consists of ~80% of order book (~70% for ship

building and ~10% for ship repair). CSL has received order for Indigenous

Offer for Sale: **1.13cr Shares

Aircraft Carrier (IAC) for the Indian Navy on nomination basis which shows its

Fresh issue: `979cr

capability of execution. It also participated in several tenders (~`12000cr) of

defence, and GOI flagship project .I.e. Sagarmala, Inland Waterways Transport.

Post Eq. Paid up Capital: `135.9cr

Ship repair segment to improve margins: CSL’s ship repair revenue has grown by

Issue size (amount): *`1416r -**1468

healthy CAGR of 17.5% over FY2013-17 and its contribution to total revenue has

cr

also increased from 17% in FY2013 to 26.4% in FY2017. Ship repair business

has 2x margins than ship building and CSL is the market leader in the ship repair

Price Band: `424-432

segment with 39% market share.

Lot Size: 30 shares and in multiple

Setting up Dry Dock and international ship repair: CSL is in the process of setting

thereafter

up two new docks ‘ship repair dock’ and ‘ship building dock’. This would require

Post-issue implied mkt. cap: *`5764cr -

capex of ~`2,700cr in next 3 years. Strong liquidity position, IPO proceeds and

**`5872cr

approvals in process would help them to finish expansion plan on time.

Promoters holding Pre-Issue: 100%

Strong financial performance coupled with healthy Balance sheet: Despite

Promoters holding Post-Issue: 75%

slowdown in shipbuilding industry CSL’s revenue and PAT grew at a CAGR of

*Calculated on lower price band

11% and 19%, respectively over FY2007-17. Margin has also expanded from

7.9% in FY2007 to 18.4% in FY2017. Its liquidity position is best amongst the

** Calculated on upper price band

listed players with negligible debt (`228cr) and cash & equivalent of ~`2,000cr

Book Building

as of FY2017. CSL has reported superior return ratios over FY2012-17 (reported

QIBs

50% of issue

average RoEs, ROCEs of 15.3%, 16.6% respectively).

Outlook & Valuation: In terms of valuation, pre- issue works out to 15.7x of

Non-Institutional

15% of issue

FY2017 EPS (at the upper end of the issue price band), which is reasonably priced

Retail

35% of issue

on the back of - (1) healthy order book with execution capability and experienced

management; (2) Average RoE & ROCE for last 5 years +15%; (3) Despite cyclical

business it has maintained net cash positive balance sheet; (4) easing working

Post Issue Shareholding Patter

capital cycle from >195 days in FY2012 to current 59 days. Considering the past

Promoters

75%

financial performance of CSL and strong visibility on future growth, we rate this

Others

25%

issue as SUBSCRIBE.

Key Financials

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

Net Sales

1,798

1,583

1,990

2,059

% chg

7

(12)

26

3

Net Profit

282

69

292

312

% chg

6

(75)

321

7

EBITDA (%)

23.2

5.6

19.7

18.5

EPS (Rs)

25

6

26

28

P/E (x)

17

71

17

16

P/BV (x)

3

3

3

2

RoE (%)

19

4

16

15

Jaikishan J Parmar

RoCE (%)

21

3

17

15

+022 39357600, Extn: 6810

EV/EBITDA

11

63

15

15

Source: RHP, Angel Research; Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

Please refer to important disclosures at the end of this report

1

Cochin Shipyard Ltd | IPO Note

Company background

Cochin Shipyard Ltd is the largest public sector shipyard in India in terms of dock

capacity, as of March 31, 2015, according to a CRISIL Report. The company caters

to clients engaged in the defence sector in India and in the commercial sector

worldwide. In addition to ship building and ship repair, CSL also offers marine

engineering training.

As of May 31, 2017, the company has two docks - dock number one, primarily

used for ship repair (“Ship Repair Dock”) and dock number two, primarily used for

ship building (“Ship building Dock”). The Ship Repair Dock is one of the largest in

India and enables it to accommodate vessels with a maximum capacity of 125,000

DWT. Further, Ship building Dock can accommodate vessels with a maximum

capacity of 110,000 DWT. CSL is also currently building India's first Indigenous

Aircraft Carrier (“IAC”) for the Indian Navy

CSL’s diversified offerings to the Indian clients engaged in the defence sectors and

commercial sectors worldwide, has allowed it to successfully adapt to the cyclical

fluctuations of the industry.

Exhibit 1: Revenue mix

Activity

FY15

FY16

FY17

Ship building (% of Grand Total)

87

82

74

Defence sector

1231

1503

1363

Commercial sector

133

118

151

Total

1364

1621

1514

Ship repair (% of Grand Total)

13

18

26

Defence sector

54

282

379

Commercial sector

144

82

165

Total

198

364

544

Grand Total

1562

1985

2057

Source: RHP, Angel Research

July 31, 2017

2

Cochin Shipyard Ltd | IPO Note

Issue Details

The company is raising `979cr through a fresh issue of equity shares in the price

band of `424-432. The fresh issue will constitute ~16.67% of the post-issue paid-

up equity share capital of the company, assuming the issue is subscribed at the

upper end of the price band. The company is offering 1.133cr shares that are

being sold by Government of India (GOI).

Exhibit 2: Pre and Post-IPO shareholding pattern

No of shares (Pre-issue)

% No of shares (Post-issue)

%

Promoter (GOI)

11,32,80,000 100%

10,19,52,000

75%

Other

0

0%

3,39,84,000

25%

11,32,80,000 100%

13,59,36,000

100%

Source: RHP, Angel Research; Note: Calculated on upper price band

Objects of the offer

Setting up of a new dry dock within the existing premises of the Company

(“Dry Dock”); Out of the proceeds, `443cr would be used for Dry dock.

Setting up of an international ship repair facility at Cochin Port Trust area

(“ISRF”); Out of the proceeds `229.5cr would be used for Dry dock.

General corporate purpose.

Key Management Personnel

Mr. Madhu S. Nair - Chairman and Managing Director, Mr. Nair is with the

company since 1988 and had joined as a management trainee. He holds

Bachelors of Technology in naval architecture and ship building from Cochin

University of Science and Technology, India, and a degree in naval architecture

and ocean engineering from Osaka University, Japan.

Mr. D. Paul Ranjan - Mr Paul is the director of finance & CFO, since May 1, 2014.

He holds Bachelors of Commerce and is a Chartered Accountant. He had joined

CSL as an executive trainee in December 17, 1984. He has approximately 32

years of work experience with the Company.

Mr. Suresh Babu N. V - Mr.Suresh is the Director (Operations) since April 26,

2016. He holds Bachelor of Engineering (Mechanical) from the University of

Kerala. He joined CSL as an executive trainee in February 1, 1985. He has

approximately 31 years of work experience with CSL

July 31, 2017

3

Cochin Shipyard Ltd | IPO Note

Healthy order book indicates strong revenue visibility

CSL’s current order book stands at `3,078cr (1.5x FY2017 revenue), this provides

revenue visibility in the near term. Defence sector consists of ~80% of order book

(~70% for ship building and ~10% for ship repair). CSL has received order for

Indigenous Aircraft Carrier (IAC) for the Indian Navy on nomination basis, which

shows its capability of execution. Additionally, it also participated in several tenders

(~`12,000cr) of defence, and GOI flagship project i.e. Sagarmala, Inland

Waterways Transport.

Exhibit 3: CSL's Ship building order book

Project/Vessel

Client

FPV

Indian Coast Guard

Confidential

GoI

IAC

Indian Navy

500 passenger cum 150 MT cargo vessel

A&N Administration

500 passenger cum 150 MT cargo vessel

A&N Administration

1200 passenger cum 1000 MT cargo vessel

A&N Administration

1200 passenger cum 1000 MT cargo vessel

A&N Administration

Double ended Ro Ro Ferry

Kochi Municipal Corporation

Double ended Ro Ro Ferry

Kochi Municipal Corporation

Revenue to be recognized in future (in Cr)

3,078.33

Source: RHP, Angel Research

Strong execution with ability to cater to commercial as well

defence sectors

CSL’s ability to cater to commercial as well defence ship building and repair, has

kept the company afloat since 2011 despite slowdown in commercial shipyard

business. We believe that CSL’s emphasis on quality of construction and timely

delivery have are the key factors to attract new customers and to retain existing

customers. For example, it recently delivered seven FPVs for the Indian Coast

Guard ahead of the contractual delivery schedule. The final FPV (in a series of 20)

was delivered on December 30, 2016, ahead of the scheduled delivery date of

March, 2017. Moreover, CSL has built two of India’s largest double hull oil

tankers, each of 92,000 DWT for SCI.

Exhibit 4: Client Wise revenue

FY15

FY16

FY17

Defence sector

82.3

89.9

84.6

Commercial sector

17.7

10.1

15.4

Source: RHP ,Angel Research

July 31, 2017

4

Cochin Shipyard Ltd | IPO Note

Government initiatives to support shipbuilding industry

Make in India Initiative

Gas Authority of India has signed contracts to buy LNG from suppliers in the US.

Transporting this gas will require large specialized LNG carriers. As part of the

‘Make in India’ campaign, the Government of India is keen that one-third of the

total number of ships should be built by Indian shipyards.

Sagarmala Project

According to the national perspective plan, the Sagarmala project aims to

transform existing ports and create new ones with world-class technology and

infrastructure. The project is also expected to integrate ports with industrial clusters

and the hinterland through rail, road, inland and coastal waterways. The

government is expected to invest US$16 billion for the project’s completion. The

project is expected to tackle underutilised ports by focussing on port

modernisation, efficient evacuation, and coastal economic development.

Development of inland waterways transport

Inland waterways transport will be an alternative for the existing mode of

transportation. The proposed 101 inland waterways will require an estimated

investment of US$5.5 billion over the next two years. Inland waterways account for

only 3% of India’s total transport, compared with 47% in China and 44% in the

European Union. The government’s initiative to develop inland waterways is a big

business opportunity for the Indian ship building industry in the form of future

orders building dredgers and small bulk carrier vessels.

Defence sector liberalisation

The Indian government has taken steps to encourage the domestic defence ship

building industry. In August 2014, the foreign direct investment limit was increased

from 26% to 49% to cut imports by indigenising defence production. India is

among the top ten defence spenders in the world and such a move to encourage

domestic manufacturing bodes well for Indian ship builders with a defence

presence.

July 31, 2017

5

Cochin Shipyard Ltd | IPO Note

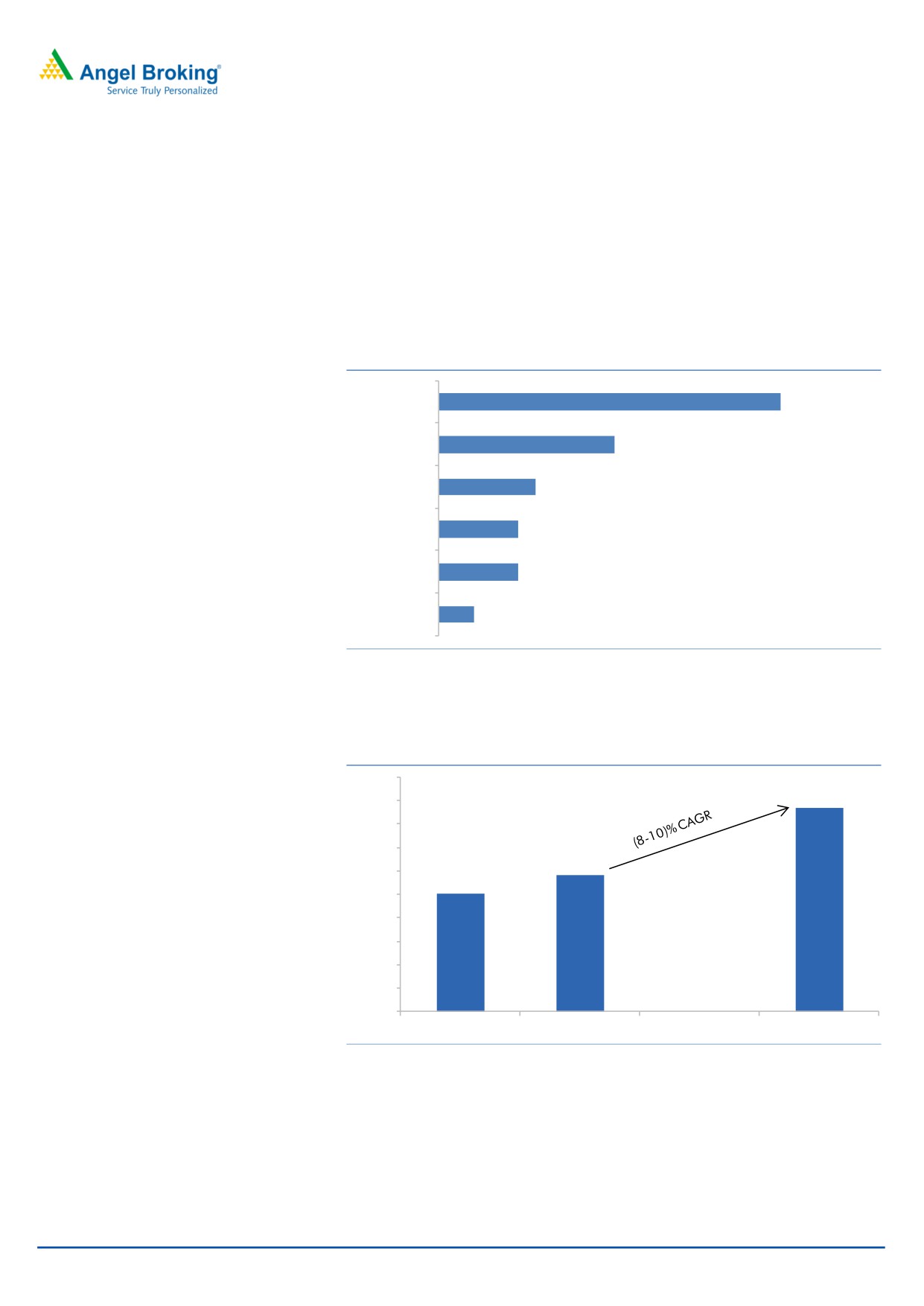

Ship repair segment to improve margins

CSL’s ship repair revenue has grown by healthy CAGR of 17.5% over FY2013-17;

ship repair contribution to revenue has also increased from 17% in FY2013 to

26.4% in FY2017. Ship repair business has 2x margins than ship building and CSL

is the market leader in ship repair business with 39% market share which is 2x of

its closest peer Goa Shipyard.

Exhibit 5: Market Share of ship repair is ~2x of the closest peer

CSL

39%

Goa Shipyard

20%

Kakinada

11%

Hindustan

9%

L&T

9%

ABG

4%

Source: RHP,, Angel Research

Exhibit 6: Market that is expected to grow at ~10% (` in Cr)

1000

820-

900

920

800

700

530-

600

630

540

500

400

300

200

100

0

FY15

FY16

FY21P

Source: RHP, CRISIL Research, Angel Research

July 31, 2017

6

Cochin Shipyard Ltd | IPO Note

Setting up Dry Dock and international ship repair (ISRF)

CSL is in the process of setting up two new docks i.e. ‘ship repair dock’ and ‘ship

building dock’. Once developed, we believe that these new facilities for

shipbuilding will expand CSL’s existing capabilities significantly and help it build

and repair a broader variety of vessels including new generation aircraft carriers

and oil rigs, which are expected to be key growth drivers in the short to near long

term and ISRF will allow the company to undertake repair of a broader range of

vessels. Currently, it undertakes repairs of almost all categories of ships (including

air craft carriers - INS Viraat and INS Vikramaditya).

This would require capex of ~`2,700cr in the next 3 years. Strong liquidity

position, IPO proceeds and approval in process would help CSL to finish

expansion plans on time.

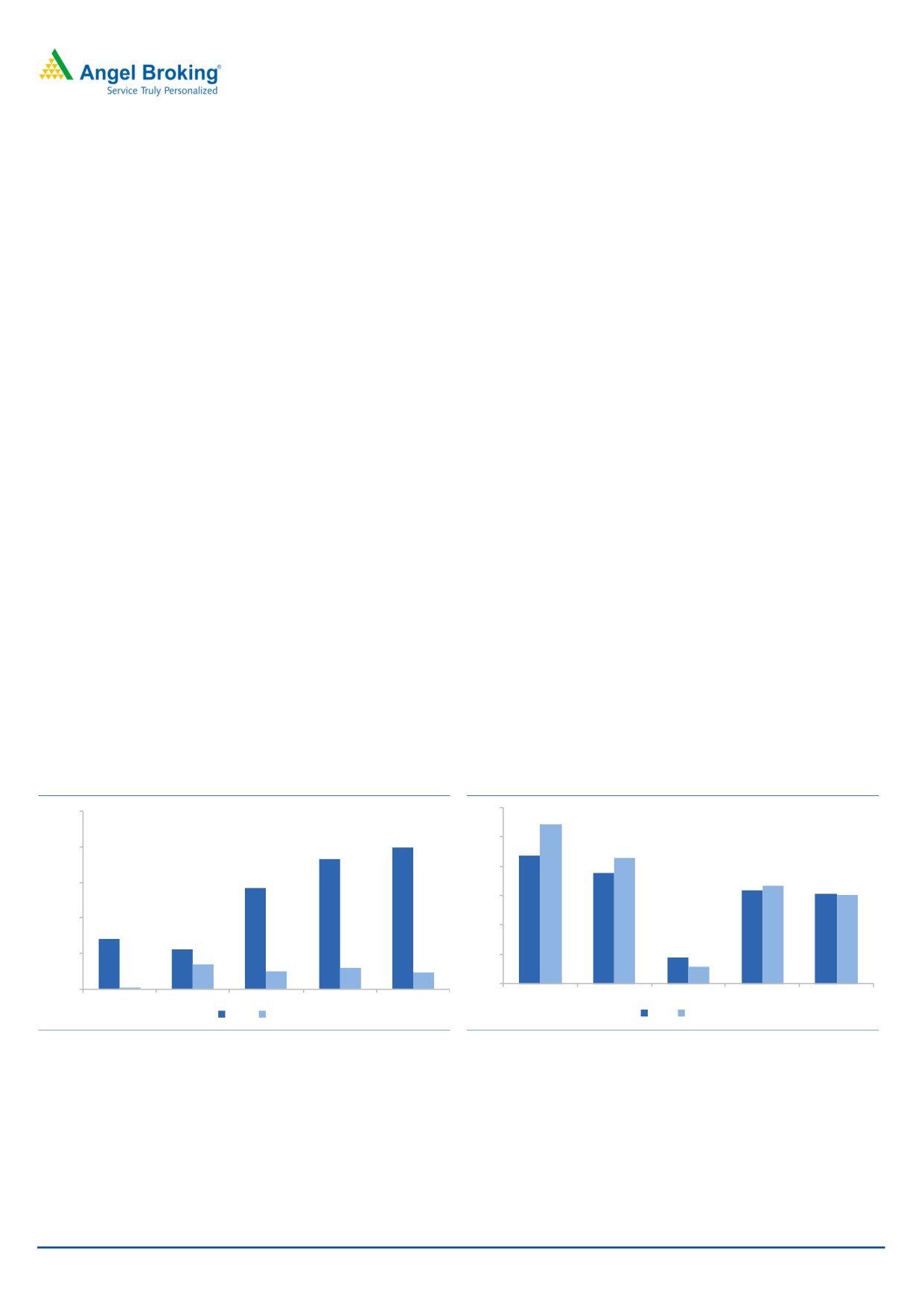

Strong financial performance, healthy Balance sheet

Despite global slowdown in commercial ship building, CSL has reported good set

of numbers during this period. It registered revenue and PAT CAGR of 11% and

19% respectively over FY2007-17. Margin has also expanded from 7.9% in

FY2007 to 18.4% in FY2017. Its liquidity position is best amongst the listed player

with negligible debt (`228cr) and cash & equivalent of ~`2,000cr as of FY2017.

CSL has posted superior return ratios over FY2012-17 (reported average RoEs,

ROCEs of 15.3%, 16.6% respectively).

However, private shipyards remain uncertain due to the stressed financial position

of major shipyards like ABG Shipyard, RDEL Shipyard and Bharati Defence and

Infrastructure Ltd.

Exhibit 7: Healthy Balance sheet (`in cr)

Exhibit 8: Return ratios

30%

2,500

27%

1,991

25%

2,000

1,820

22%

21%

19%

20%

1,419

16%17%

1,500

15%15%

15%

1,000

704

10%

556

4%

500

340

290

5%

3%

247

228

5

0%

0

FY13

FY14

FY15

FY16

FY17

FY13

FY14

FY15

FY16

FY17

Cash Debt

ROE ROCE

Source: RHP, Company

Source: RHP, Company

July 31, 2017

7

Cochin Shipyard Ltd | IPO Note

Outlook & Valuation

In terms of valuation, pre- issue works out to 15.7x of FY2017 EPS (at the upper

end of the issue price band), which is reasonably priced on the back of - (1)

healthy order book with execution capability and experienced management; (2)

Average RoE & ROCE for last 5 years +15%; (3) Despite cyclical business it has

maintained net cash positive balance sheet; (4) easing working capital cycle from

>195 days in FY2012 to current 59 days. Considering the past financial

performance of CSL and strong visibility on future growth, we rate this issue as

SUBSCRIBE.

Key Risk

High dependence on defence related projects

CSL’s defence related projects have contributed 87.7%, 82.5%, 89.9% and 73.2%

to its revenues from operations in FY14, FY15, FY16 and H1FY17 respectively.

Further, CSL is currently building India’s first Indigenous Aircraft Carrier for the

Indian Navy.

Cyclical nature of commercial ship building

Worldwide demand and pricing in the commercial ship building industry are highly

dependent upon global economic conditions. If the global economy fails to grow

at an adequate pace, it may adversely impact the commercial shipbuilding

industry, which may negatively affect CSL’s business, financial condition and

growth prospects.

Operations are based at a single shipyard at Kochi

The loss of, or shutdown of, operations at company’s shipyard in Kochi will have a

material adverse effect on the business, financial condition and results of

operations.

Volatility in price of raw materials

The major components of CSL’s expenditure include raw materials such as steel

and other materials, equipment and other components such as pumps, propellers

and engines. Any price escalation in the above materials may impact margin of

CSL.

July 31, 2017

8

Cochin Shipyard Ltd | IPO Note

Income Statement

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

Total operating income

1,798

1,583

1,990

2,059

% chg

7

(12)

26

3

Total Expenditure

1,381

1,494

1,598

1,679

Raw Material

990

1,141

1,230

1,314

Personnel

209

213

209

217

Others Expenses

182

140

159

148

EBITDA

417

89

392

380

% chg

18

(79)

339

(3)

(% of Net Sales)

23

6

20

18

Depreciation& Amortization

25

38

37

39

EBIT

391

52

355

342

% chg

17

(87)

588

(4)

(% of Net Sales)

22

3

18

17

Interest & other Charges

19

18

12

11

Other Income

61

77

107

149

(% of PBT)

14

70

24

31

Extraordinary Items

0

0

0

0

Share in profit of Associates

-

-

-

-

Recurring PBT

433

110

450

480

% chg

9

(74)

307

7

Tax

151

41

158

168

PAT (reported)

282

69

292

312

% chg

6

(75)

321

7

(% of Net Sales)

16

4

15

15

Basic & Fully Diluted EPS (Rs)

25

6

26

28

% chg

6

(75)

321

7

July 31, 2017

9

Cochin Shipyard Ltd | IPO Note

Balance Sheet

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

SOURCES OF FUNDS

Equity Share Capital

113

113

113

113

Reserves& Surplus

1376

1441

1711

1918

Shareholders Funds

1490

1554

1824

2031

Total Loans

340

247

290

228

Other Liab & Provision

18

19

19

21

Total Liabilities

1847

1820

2133

2280

APPLICATION OF FUNDS

Net Block

370

370

370

371

Capital Work-in-Progress

8

13

24

54

Investments

0

0

0

0

Current Assets

2155

2305

2506

2485

Inventories

396

303

232

186

Sundry Debtors

1203

583

454

307

Cash

556

1419

1820

1991

Loans & Advances

356

114

180

321

Other Assets

98

89

268

86

Current liabilities

1140

1071

1216

1036

Net Current Assets

1015

1234

1291

1448

Other Non Current Asset

Total Assets

1847

1820

2133

2280

July 31, 2017

10

Cochin Shipyard Ltd | IPO Note

Cash Flow Statement

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

Profit before tax

433

110

450

480

Depreciation

22

35

34

36

Change in Working Capital

(496)

738

173

362

Interest / Dividend (Net)

(51)

(54)

(99)

(131)

Direct taxes paid

(88)

(75)

(133)

(150)

Others

(404)

(92)

(385)

(385)

Cash Flow from Operations

(584)

663

40

212

(Inc.)/ Dec. in Fixed Assets

(151)

(35)

(35)

(40)

(Inc.)/ Dec. in Investments

166

50

81

105

Cash Flow from Investing

15

16

47

65

Issue of Equity

-

-

-

-

Inc./(Dec.) in loans

123

-

-

-

Others

148

(235)

(32)

(113)

Cash Flow from Financing

271

(235)

(32)

(113)

Inc./(Dec.) in Cash

(298)

444

55

165

Opening Cash balances

311

13

457

511

Closing Cash balances

13

457

511

676

Key Ratio

Y/E March

FY2013

FY2014

FY2015

FY2016

FY2017

P/E (on FDEPS)

18.4

17.4

70.6

16.8

15.7

P/CEPS

17.2

15.9

45.7

14.9

14.0

P/BV

4.0

3.3

3.1

2.7

2.4

EV/Sales

2.5

2.6

3.6

3.0

2.8

EV/EBITDA

11.9

11.2

63.2

15.3

15.2

EV / Total Assets

3.4

2.5

3.1

2.8

2.5

Per Share Data (`)

EPS (Basic)

23.5

24.9

6.1

25.8

27.6

EPS (fully diluted)

19.6

20.7

5.1

21.5

23.0

Cash EPS

25.2

27.1

9.4

29.0

31.0

DPS

1.5

1.5

1.5

1.5

1.6

Book Value

108.2

131.5

137.2

161.0

179.3

Returns (%)

ROCE

27.1

21.4

2.9

16.8

15.1

Angel ROIC (Pre-tax)

82

30

13

123

146

ROE

21.7

18.9

4.5

16.0

15.4

Turnover ratios (x)

Inventory / Sales (days)

77

80

70

42

33

Receivables (days)

149

244

134

83

54

Payables (days)

30

35

39

38

29

Working capital cycle (ex-cash) (days)

195

290

165

87

59

Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

July 31, 2017

11

Cochin Shipyard Ltd | IPO Note

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

July 31, 2017

12