Initiating Coverage | NBFC

January 1, 2018

Capital First Ltd

BUY

CMP

`693

Target Price

`850

Capital First (CFL) is a non-deposit-taking NBFC primarily focusing on retail

Investment Period

12 Months

lending. Post management buyout

(2012), Mr Vaidynathan, the current

chairman, transformed the company’s focus from wholesale financier to

Stock Info

diversified retail financier. Warburg Pincus in 2012 acquired a majority stake in

Sector

NBFC

the company. Focused approached led to decline in wholesale financing to 7%

Market Cap (` cr)

6,872

now from 90% in FY2010 and stringent underwriting resulting into GNPA of

Beta

1.5

5.3% in FY2010 to 1% in FY2017.

52 Week High / Low

839/512

Strong AUM CAGR of 27.5% over FY2013-17: CFL registered strong AUM

Avg. Daily Volume

33,085

CAGR of 27.5% over FY13-17 post the new strategy adopted by the new

Face Value (`)

10

management. The aggressive focus towards retail loans and decreasing the

BSE Sensex

33,848

wholesale book augured well for CFL. While retail loans grew by 35%, wholesale

Nifty

10,478

loans de-grew by 8.2% over FY2013-17. The share of retail loans in the loan

Reuters Code

CAPF.NS

book went up to 93% (FY2017) from a level of 10% (FY2010). We expect AUM

Bloomberg Code

CAFL.IN

CAGR of 23.3% over FY2017-20.

Favorable Product mix change, lower bank borrowings to be margin accretive:

The management intends to increase the share of higher yielding consumer

Shareholding Pattern (%)

durable (CD)/ two wheeler (2W) financing from 13%/10% presently to 16-17%

Promoters

36.0

each by FY2019. CFL’s high dependence on bank borrowings has reduced to

MF / Banks / Indian Fls

13.1

58% (FY17) v/s. 85% (FY14). However, with better ratings & money market

FII / NRIs / OCBs

24.3

instruments becoming more attractive we expect overall cost of funds to decline,

Indian Public / Others

26.6

aiding NIM expansion by 80bps over FY17-19.

Impressive asset quality: High asset quality has been maintained due to stringent

underwriting process. About 38% of the total applications are disbursed after

Abs.(%)

3m 1yr 3yr

passing through several levels of scrutiny and checks, mainly centered on cash

Sensex

7.4

31.5

53.0

flow evaluation, credit bureau and reference checks. In FY2010, GNPA of CFL

Capital First

(9.6)

33.8

96.1

was 5.3%, which has lowered to 1.6% (Q2FY18) post the new management

taking charges.

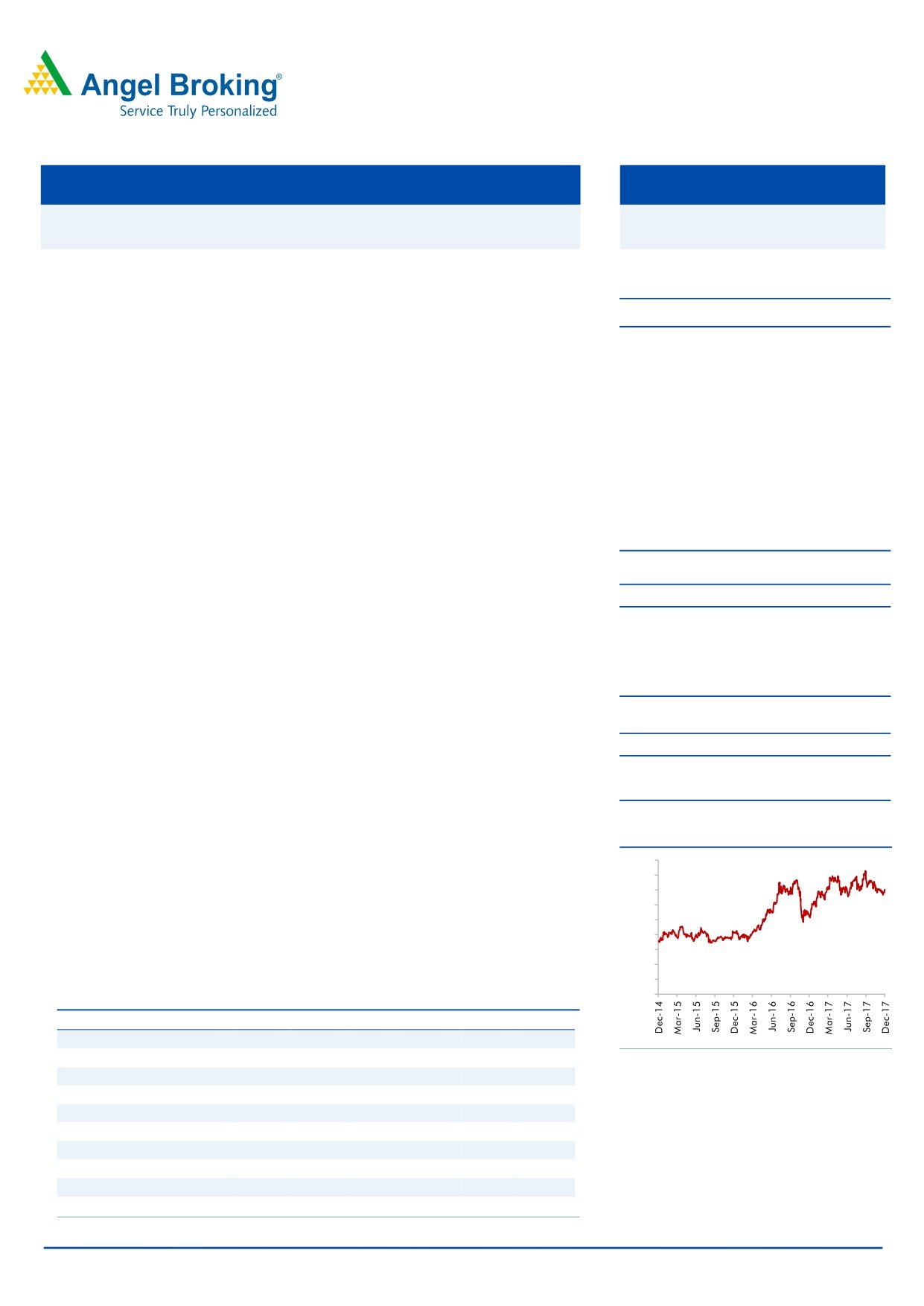

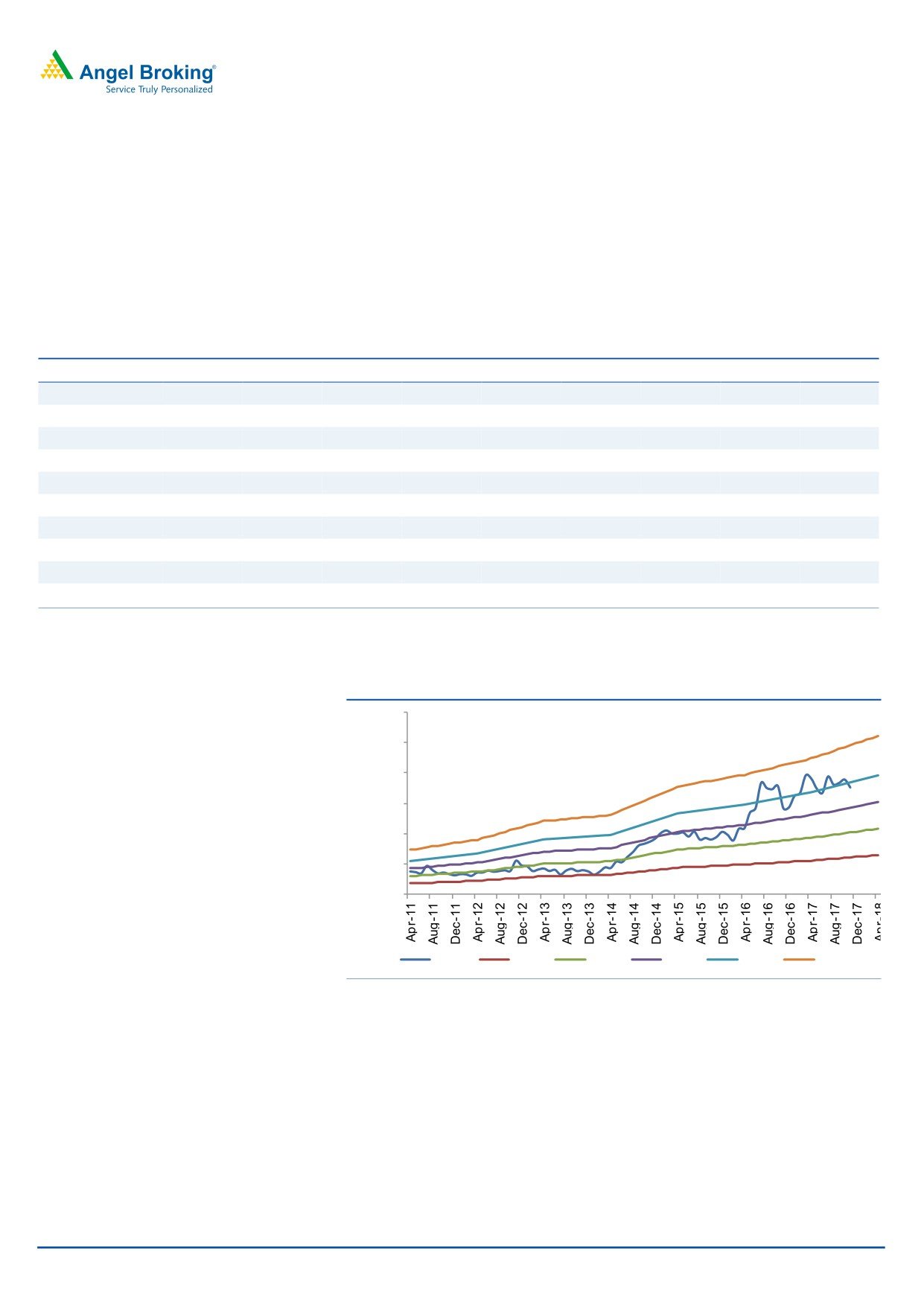

3-year price chart

Outlook and valuation: Strong capital adequacy and pick up in retail credit will

900

ensure 24% loan growth over FY2017-20. Favorable loan mix coupled with

800

expansion in NIM would drive 32% earnings CAGR over the same period. Given

700

600

improving return ratios we believe the stock is poised for further re-rating. The

500

stock is trading at 2.2x it FY2020 ABV. We have valued the stock at 2.7x its

400

300

FY2020E ABV and recommend BUY with a target price of `850 over the next 12

200

months.

100

0

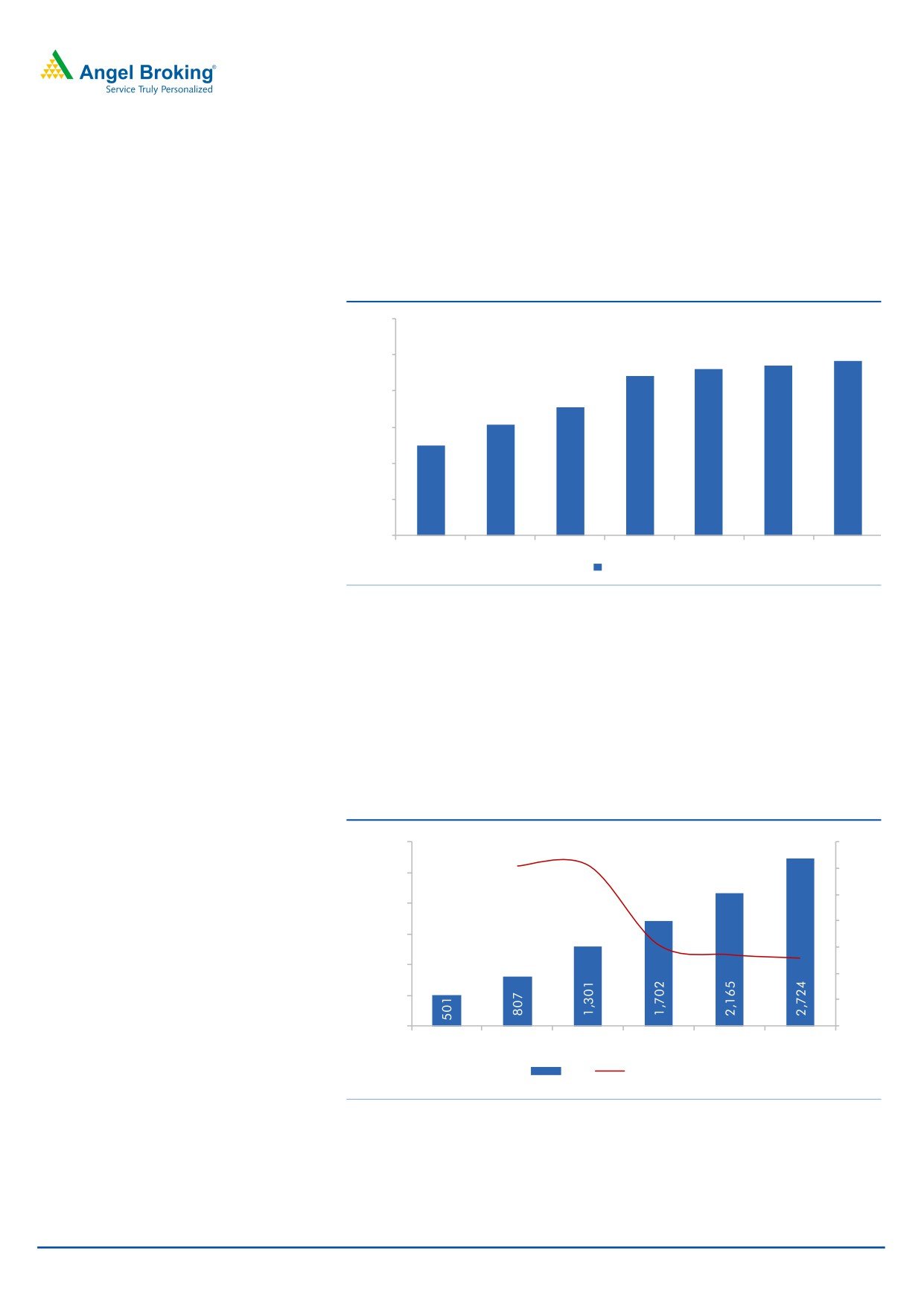

Key Financials (Standalone)

Y/E March (` cr)

FY15

FY16

FY17

FY18E FY19E FY20E

NII

501

771

1,228

1,571

2,008

2,536

% chg

53

54

59

28

28

26

Source: Company, Angel Research

Net profit

112

168

240

296

407

550

% chg

89

50

43

23

38

35

NIM (%)

6.1

7.1

8.8

9.2

9.4

9.7

EPS (`)

11.4

17.1

24.5

30.2

41.6

56.3

P/E (x)

60.5

40.3

28.2

22.9

16.6

12.3

P/ABV (x)

4.3

4.1

3.1

2.9

2.5

2.2

Jaikishan Parmar

ROA (%)

1.0

1.2

1.4

1.4

1.5

1.7

022 - 3935 7800 Ext: 6810

ROE (%)

8.1

10.2

12.0

12.2

14.9

17.4

Source :Company, Angel Research; Note: CMP as of December 29, 2017

Please refer to important disclosures at the end of this report

1

Capital First Ltd | Initiating Coverage

Company Background:

Capital First Ltd (CFL) is one of the leading financial institutions in India focused on

providing debt financing to MSMEs and consumers. Capital First Ltd was founded

in 2012 through a management buyout of an existing listed NBFC and equity

backing by a global private equity. With the help of contemporary scoring

solutions and sophisticated technology, the company provides finance to select

segments that are traditionally underserved by existing financial systems due to

small ticket sizes, difficulties in credit evaluation, collection issues, etc. The

company provides financing to salaried and self employed retail customers, which

is a growing category in India.

Exhibit 1: Key milestones

FY10 Wholesale NBFC+ Broking subsidiary

FY11 Launched durable financing business with credit scoring

FY12 Merged subsidiary NBFC with parent and launched two wheeler financing

FY13 Capital First was formed as a result of management buyout of an existing NBFC

FY13 Warburg Pincus acquires 70% stake in the company for `810cr in September 2012

FY14 Closed broking business, acquired HFC license via subsidiary

FY15 Closed gold loan business, AUM crosses `12,000 cr

FY16 AUM crosses `16,000 cr, no of customers financed since inception crosses 2.25 mn

FY17 AUM crosses ` 20,000 cr, no of customers financed since inception crosses 4 mn

Source: Company, Angel Research

Exhibit 2: Types of loans offered by CFL

Products

Ticket Size(` ) Tenor (Months)

Average Loan to Value Ratio

MSME Loans

9,60,000

60

42%

CFL provides long term loans to MSMEs after proper evaluation of

cash flows.

Backed by collateral of residential or commercial property.

Monthly amortizing products with no moratorium.

CFL also provides unsecured short tenure working capital loans to

the MSMEs.

Two Wheeler Loans

44,000

24

70%

CFL provides financing to salaried segment as well as self

employed individuals like small traders, shop keepers for

purchase of new two-wheelers.

Consumer Durables Loans

30,000

8

76%

CFL provides financing to salaried and self-employed customers

for purchasing of LCD/LED panels, Laptops, Air-conditioners

and other such white good products. They are also availed by

small entrepreneurs for official purposes.

Change in ownership & management brings new life to the company: The

company was first listed on Stock Exchanges in January 2008. Between 2010 to

2012, Mr Vaidyanathan acquired a stake in the company, changed the business

model to retail, and executed a Management Buyout of the company with equity

backing from Warburg Pincus for `810cr and changed the name to Capital First.

Post 2012, CFL raised `178cr from Warburb Pincus and HDFC Standard Life. AS

CFL was growing at 25%+ CAGR it raised `300cr through QIP in FY2015

subscribed by Goldman Sachs. In Q4FY2017, it raised `340cr through preferential

allotment to GIC, Singapore.

January 01, 2018

2

Capital First Ltd | Initiating Coverage

Transition from a wholesale financer to a retail financer: The new management led

by Mr Vaidyanathan focused more on the granular retail loan category, and thus

successfully transitioned as a retail lender. The share of wholesale finance has

been brought down to 7% by FY2017 from 90% in FY2010. CFL still has a high

dependency on the Loan against Property, 42% of the overall loan book, which it

intends to bring down to 33% by FY2019. Simultaneously, the company intends to

increase CD/2W financing from 13%/10% presently to 16-17% each by FY19. The

company also has an unsecured SME loan book accounting for ~18% of the total

loans.

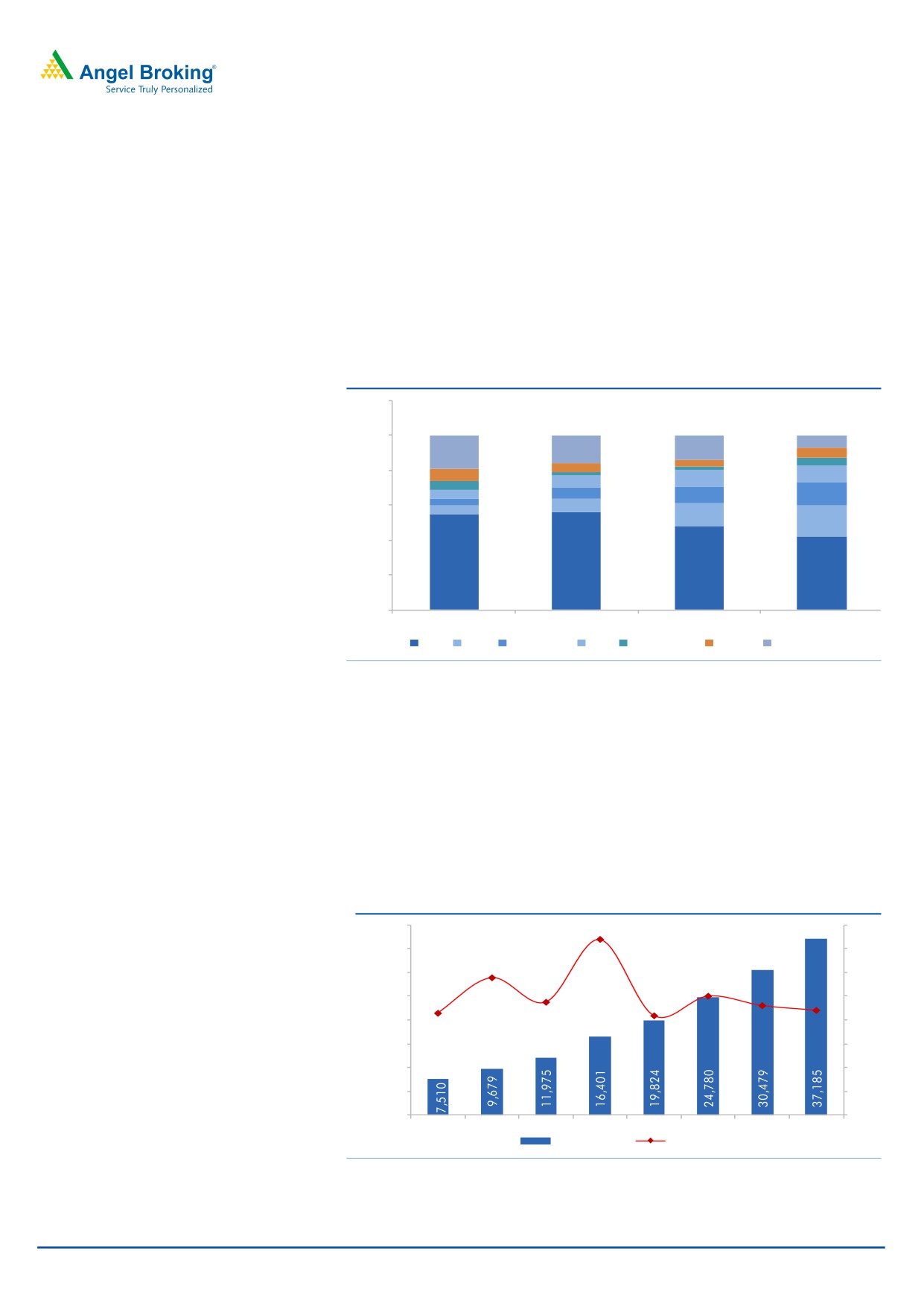

Exhibit 3: Loan book driven by new segments like 2W/CD

120

100

7

16

14

19

80

10

7

9

6

10

13

60

4

8

5

13

18

40

55

56

48

20

42

-

FY14

FY15

FY16

FY17

LAP SME Consumer 2W Home Loan Other WholeSale

Source: Company, Angel Research

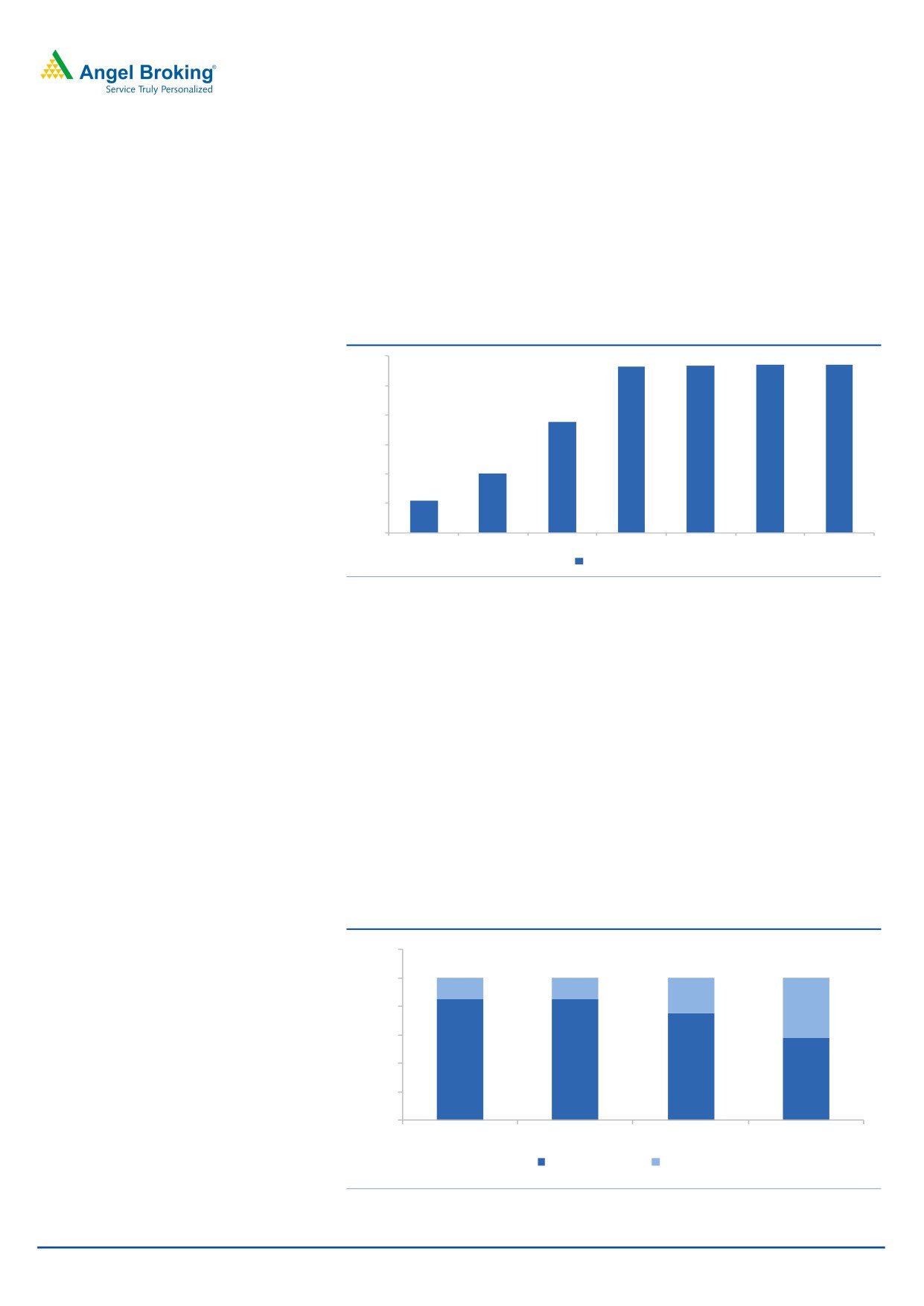

Strong AUM CAGR of 27.5% over FY2013-17, expect 23.3% CAGR over FY2017-

20: CFL registered strong AUM CAGR of 27.5% over FY13-17 post the new

strategy adopted by the new management. The aggressive focus towards retail

loans and decreasing the wholesale book augured well for CFL. While retail loans

grew by 35%, wholesale loans de-grew by 8.2% over FY2013-17. The share of

retail loans in the loan book went up to 93% (FY2017) from a level of 10%

(FY2010). We expect AUM CAGR of 23.3% over FY2017-20.

Exhibit 4: AUM Growth (%)

40,000

40%

37%

35,000

35%

29%

30,000

30%

25%

24%

23%

25,000

21%

22%

25%

21%

20,000

20%

15,000

15%

10,000

10%

5 ,000

5%

-

0%

FY13

FY14

FY15

FY16

FY17

FY18E FY19E FY20E

AUM (` Cr)

% Growth

Source: Company, Angel Research

January 01, 2018

3

Capital First Ltd | Initiating Coverage

Increasing number of MSME/ SME coming under the formal sector, opens newer

opportunities for the company: The Indian economy is going through a paradigm

shift, backed by new initiatives by the government. Further, measures like GST,

Aadhar card based e-KYC, etc. will have far reaching impact and enable

augmenting financial inclusion. Hence, NBFCs like CFL will be able to tap the vast

underserved individuals whose credit needs have been growing with the change in

aspirations and income levels. CFL is well placed to take advantage of these

opportunities going ahead.

Housing Finance, still small but has huge potential for CFL: in order to diversify the

loan book further, the management ventured into retail home loans in 2015, via

its wholly owned subsidiary, Capital First Home Finance Ltd. With an average ticket

size of ~`15 lakhs, the loans are targeted primarily to the self employed

professionals in the affordable housing segment. The opportunity of lending

towards self employed segment remains huge with very few players operating in

the segment. Within a short span of time the AUM in the housing finance has

reached a level of ~`800cr (~`600cr at the end of FY17) and we expect the

growth rate to be 40-50% over the next few years.

Despite higher share of LAP/ SME lending, the NPAs are largely under control:

The GNPA of the company was as high as 5.3% in FY2010, which was brought

down to 1% (FY2017). The CFL has started complying with RBI regulations

recognizing NPAs on 90 days overdue basis (90 DPD), at par with banks now.

Earlier it had migrated to 120 DPD in Q1FY17. Though the company migrated to

90 DPD it already had done adequate provisions.

Exhibit 5: Comparative NPA trend- On 90 DPD basis

2.00

1.74

1.71

1.72

1.80

1.65

1.63

1.59

1.52

1.60

1.40

1.21

1.13

1.20

1.04

0.97

1.00

1.00

1.00

1.00

0.80

0.60

0.40

0.20

-

Q4FY16

Q1FY17

Q2FY17

Q3FY17

Q4FY17

Q1FY18

Q2FY18

GNPA (%) NPA (%)

Source: Company, Angel Research

January 01, 2018

4

Capital First Ltd | Initiating Coverage

With 90 days NPA recognition norm, the credit cost is more comparable with

peers: The credit cost of CFL has gone up in FY17 partly due to demonetization

and impact of slowdown in the economy. Also, the nature of consumer lending in

retail space will have higher credit cost. However, we believe the company is at the

peak of its credit cost cycle and there could be a moderation in the same going

ahead. We have factored in 280bps credit cost in FY2018E/FY2019E/FY2020E

each.

Exhibit 6: Credit cost trend (%)

3.0

2.8

2.8

2.8

2.8

2.5

2.0

1.9

1.5

1.0

1.0

0.6

0.5

-

FY14

FY15

FY16

FY17

FY18E

FY19E

FY20E

Credit Cost (%)

Source: Company, Angel Research

Reducing dependence on bank borrowings, to help lower cost of funds:

Historically, CFL had high dependency on bank borrowings for its business. The

share of bank borrowings in its sources of funds was as high as 85% in FY2014,

which has gradually been brought down to 58% by FY2017. The management

expects the share of bank borrowings to reduce to ~40% of total by FY2019. With

overall softening of interest rates and G-Sec yields, the cost of borrowings via

money market instruments have become attractive, and hence, the share of

borrowings from the same source has gone up to 42% from 15% (FY15). The

NBFC has a AA+ rating for it borrowings from CARE and based on the current

spread between AA+ and 10 Yr G-Sec yield, we believe there is further scope for

re-pricing its high cost bank borrowings as well as re-pricing of old NCDs with

fresh NCDs at a much attractive rate.

Exhibit 7: Changing funding profile

120%

100%

15%

15%

25%

80%

42%

60%

40%

85%

85%

75%

58%

20%

0%

FY14

FY15

FY16

FY17

Bank Borrowings

Others

Source: Company, Angel Research

January 01, 2018

5

Capital First Ltd | Initiating Coverage

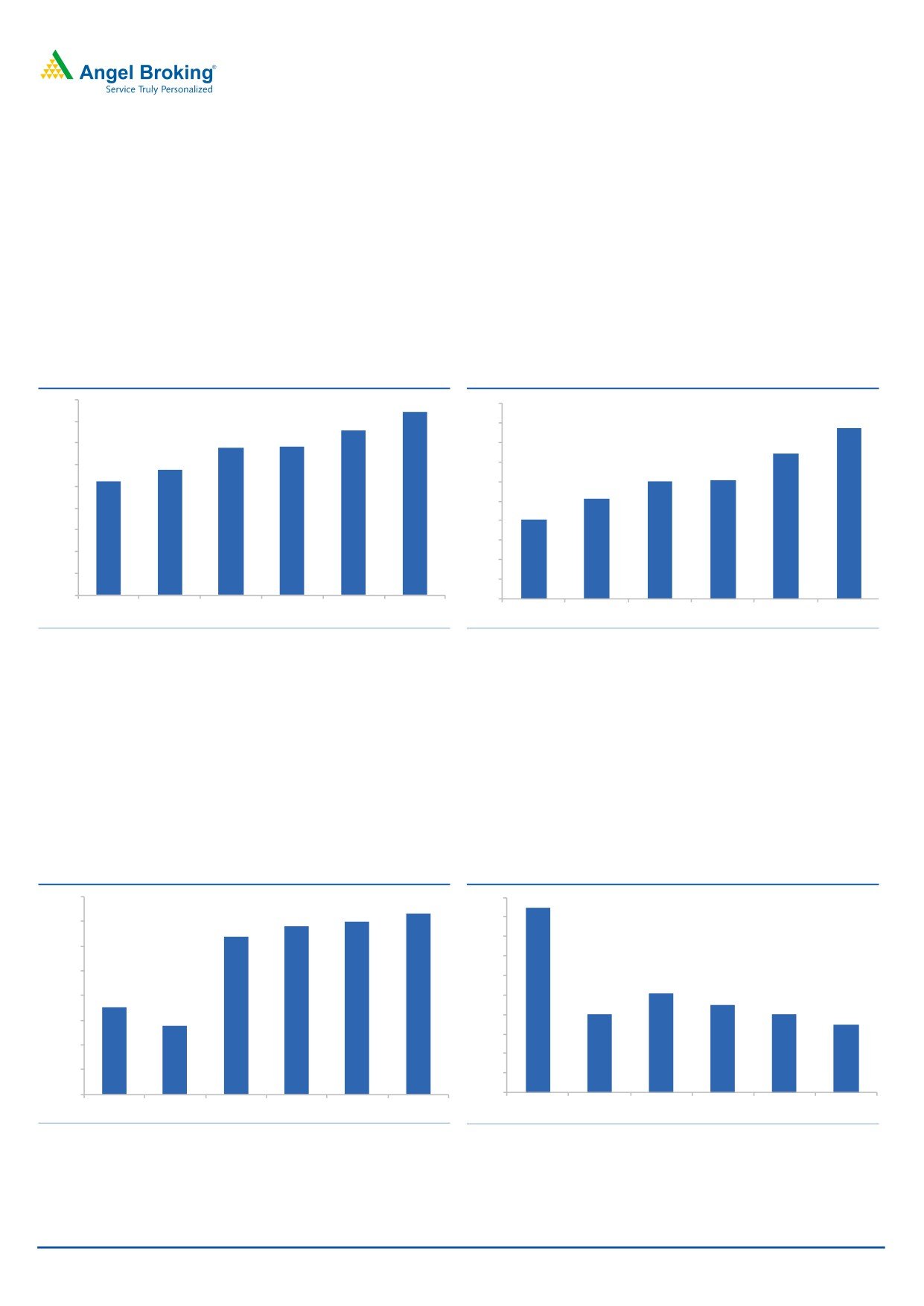

Shift towards higher yielding assets and lower Opex cost on incremental business

in 2W/CD to result in ROE improvement: CFL has successfully transitioned from a

wholesale financer to a retail financer over the last five years. However, within the

retail space higher dependency on LAP and front loading of operating cost, both in

terms of technology and manpower had impacted the cost structure. With

maturing business in the consumer durable financing and two wheeler financing

segments, Opex cost would reduce for incremental business in 2W/CD. In the

absence of major equity dilution in the near term and moderating Opex cost, we

expect ROE to improve from 11.9% in FY2017 to ~17% by FY2020.

Exhibit 8: ROA (%)

Exhibit 9: ROE (%)

1.8

1.7

20

1.5

17

1.6

18

1.4

1.4

1.4

16

15

1.2

1.2

14

1.0

12

12

12

1.0

10

10

0.8

8

8

0.6

6

0.4

4

0.2

2

-

-

FY15

FY16

FY17

FY18E

FY19E

FY20E

FY15

FY16

FY17

FY18E

FY19E

FY20E

Source: Company, Angel Research

Source: Company, Angel Research

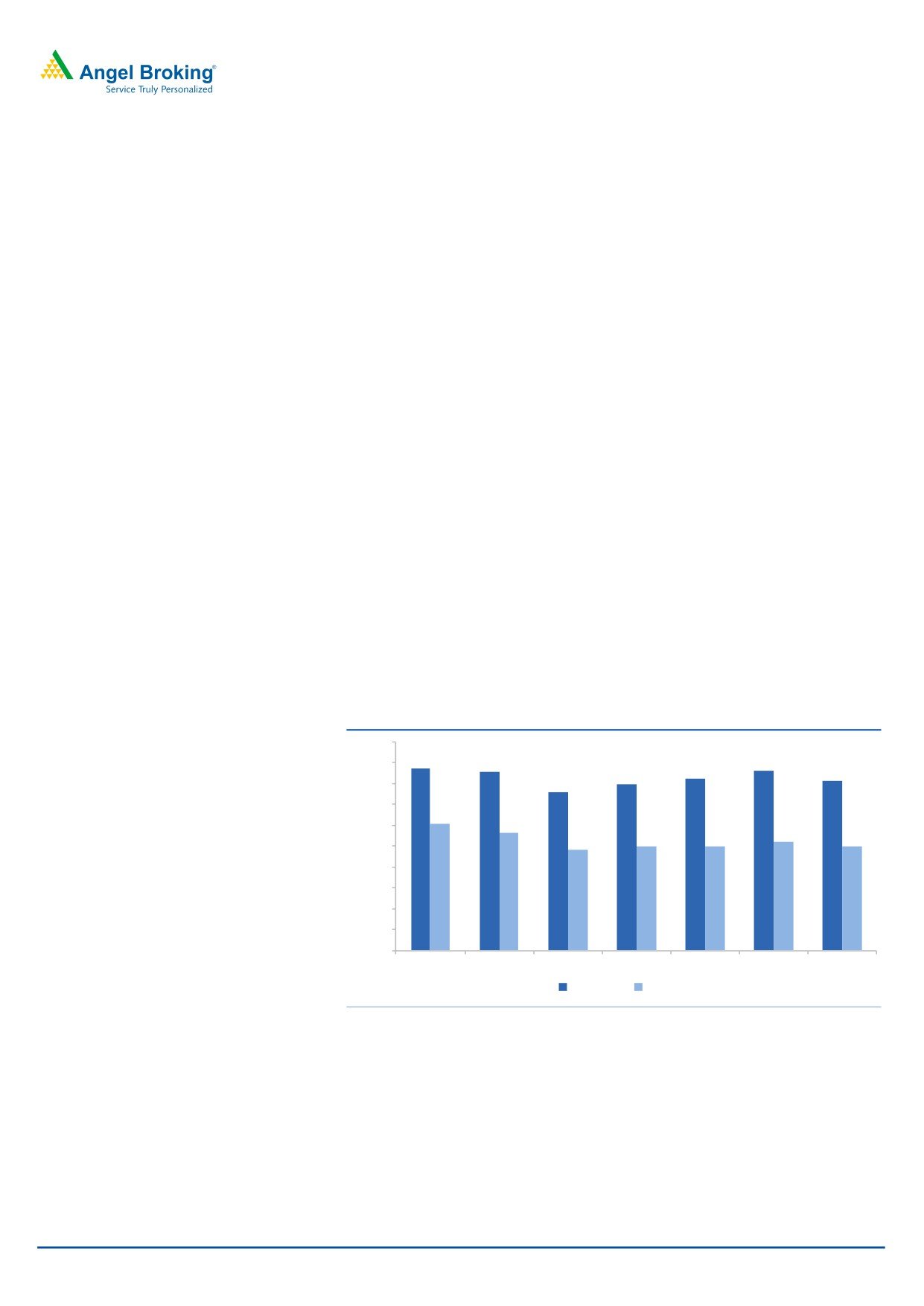

Product mix revival, lower bank borrowings to be margin accretive: CFL has

gradually reduced its share of wholesale book and is focusing more on the retail

lending. Within the retail space, the company is still highly dependent on the

mortgage based SME lending (LAP). However, as a strategy, it intends to further

reduce its dependence on the LAP and is now focusing more on the granular retail

loans like Consumer durables and two wheelers, which also generates higher

yield, and hence, we expect yield on advances to improve further.

Exhibit 10: Yield (%)

Exhibit 11: Cost of funds (%)

18.0%

9.4%

9.3%

17.7%

17.5%

17.4%

9.3%

17.5%

17.2%

9.2%

17.0%

9.1%

16.5%

9.0%

8.9%

16.0%

15.8%

8.9%

8.9%

8.8%

8.8%

15.4%

8.8%

8.8%

15.5%

8.7%

15.0%

8.6%

14.5%

8.5%

14.0%

8.4%

FY15

FY16

FY17

FY18E

FY19E

FY20E

FY15

FY16

FY17

FY18E

FY19E

FY20E

Source: Company, Angel Research

Source: Company, Angel Research

January 01, 2018

6

Capital First Ltd | Initiating Coverage

Historically, CFL had high dependency on bank borrowings for its business.

However, with better ratings & money market instruments becoming more

attractive, it has started raising funds via NCDs. This, together with lower cost of

funds, due to reduction in MCLR based borrowings will help in NIM improvement.

We have factored in an 80bps improvement in NIM over FY2017-20.

Exhibit 12: NIM to increase 80bps with product mix shift

12.0

9.7

10.0

9.2

9.4

8.8

8.0

7.1

6.1

6.0

5.0

4.0

2.0

-

FY14

FY15

FY16

FY17

FY18E

FY19E

FY20E

NIM (%)

Source: Company, Angel Research

NII growth will be in sync with AUM growth: We expect NII to grow at healthy

CAGR of 27.3% over FY2017-20. NII growth would be backed by (a) AUM growth

of 23.3%, (2) change in product mix from low yielding loan book to high yielding

loan book (2W/CD), (3) Reduction in cost of funds due to higher borrowing from

market instrument and cut in MCLR rates to help in refinancing existing high cost

borrowing at lower cost.

Exhibit 13: NII Growth has been in sync with AUM growth

3,000

26%

70%

61%

61%

2,500

60%

27%

50%

2,000

31%

40%

1,500

30%

1,000

20%

500

10%

-

0%

FY15

FY16

FY17

FY18E

FY19E

FY20E

NII

% Growth YoY

Source: Company, Angel Research

January 01, 2018

7

Capital First Ltd | Initiating Coverage

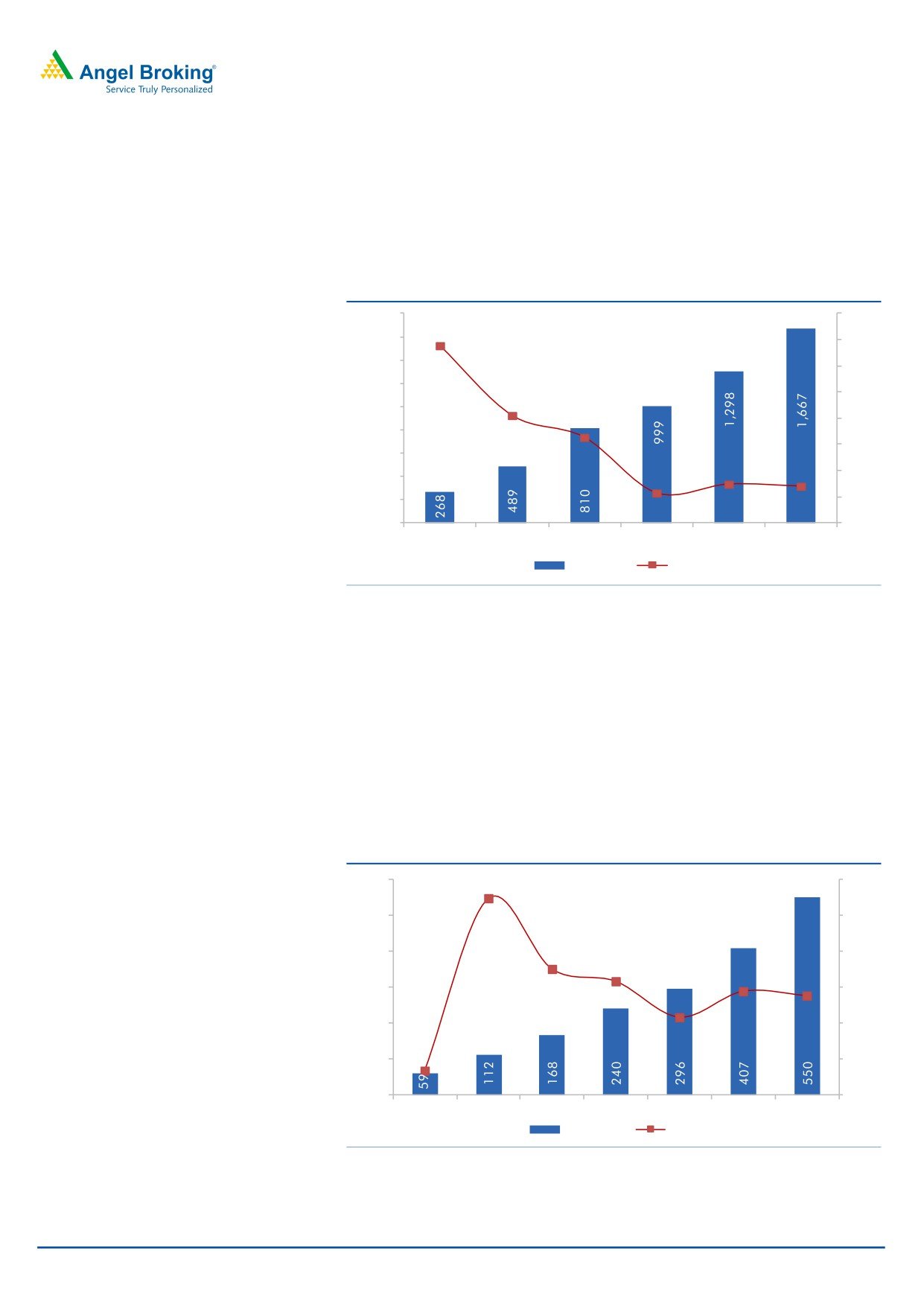

Pre-provisioning profit (PPP) to get a boost from fee income: The granular asset

base of the company has helped in strong growth in fee income as well, and we

expect fee income to contribute meaningfully to the pre-provisioning profit. CFL

has incurred capex to develop 2W/CD financing business since 2011; hence going

forward C/I ratio would witness a declining trend.

Exhibit 14: PPP growth trend

1,800

160%

136%

1,600

140%

1,400

120%

1,200

100%

82%

1,000

66%

80%

800

60%

600

30%

28%

400

23%

40%

200

20%

-

0%

FY15

FY16

FY17

FY18E

FY19E

FY20E

PPP (`cr)

% Growth

Source: Company, Angel Research

PAT growth will outpace NII growth, backed by moderating cost: We expect the

PAT growth of the company to outpace its loan and NII growth, largely backed by

lower cost structure and stable credit cost. With higher adoption of technology and

Algo based lead generation, the company intends to reduce its cost structure, and

this should aid the bottom-line growth. The cost income ratio of the company has

already come down to 50.6% in FY2017 from a high of 59% in FY2015. However,

it still remains high and we believe there is scope for the same to come down

further.

Exhibit 15: PAT growth trend

600

89%

100%

500

80%

400

50%

60%

43%

38%

35%

300

40%

23%

200

20%

-7%

100

0%

-

-20%

FY14

FY15

FY16

FY17

FY18E

FY19E

FY20E

PAT (`Cr)

% Growth

Source: Company, Angel Research

January 01, 2018

8

Capital First Ltd | Initiating Coverage

Outlook and valuation

Strong capital adequacy and pick up in retail credit will ensure 24% loan growth

over FY2017-20. Favorable loan mix coupled with expansion in NIM would drive

32% earnings CAGR over the same period. Given improving return ratios we

believe the stock is poised for further re-rating. The stock is trading at 2.2x it

FY2020 ABV. We have valued the stock at 2.7x its FY2020E ABV and recommend

BUY with a target price of `850 over the next 12 months.

Exhibit 16: Comparative valuations & return ratios

P/BV (x)

ROE%

ROA%

FY17

FY18E

FY19E

FY17

FY18E

FY19E

FY17

FY18E

FY19E

Capital First

3.0

2.7

2.4

12.0

12.2

14.9

1.4

1.4

1.5

Bajaj Fin

9.5

6.1

5.1

21.6

20.5

20.2

3.3

3.5

3.6

L&T Fin

3.6

3.2

2.7

12.1

14.9

16.9

1.5

1.7

1.9

M&M Fin

3.7

3.2

2.8

7.6

13.5

15.5

1.1

1.8

2.2

Chola

4.6

3.9

3.3

18.1

19.3

19.9

2.5

2.6

2.7

Shriram City

2.6

2.3

2.1

11.8

15.1

16.4

2.3

2.9

3.0

Magma

1.8

4.7

4.2

0.9

9.3

12.3

0.1

1.3

1.8

STFC

2.9

0.9

0.8

11.7

13.9

16.5

1.7

2.2

2.6

Sundaram Fin

4.2

1.3

1.1

15.2

16.1

16.1

2.3

2.8

2.9

Source: Company, Angel Research, based on closing price of 26th Dec

2017, other NBFC estimates taken from Bloomberg,

Exhibit 17: One Year Forward P/BV

1200.00

1000.00

800.00

600.00

400.00

200.00

0.00

CAFL

0.8 X

1.3 X

1.8 X

2.3 X

3.0 X

Source: Company, Angel Research

January 01, 2018

9

Capital First Ltd | Initiating Coverage

Income statement

Y/E March (` cr)

FY16

FY17

FY18E

FY19E

FY20E

NII

771

1,228

1,571

2,008

2,536

- YoY Growth (%)

54

59

28

28

26

Other Income

221

412

424

525

643

- YoY Growth (%)

45

86

3

24

22

Operating Income

992

1,640

1,995

2,533

3,179

- YoY Growth (%)

52

65

22

27

26

Operating Expenses

503

830

996

1,234

1,511

- YoY Growth (%)

30

65

20

24

22

Pre - Provision Profit

489

810

999

1,298

1,667

- YoY Growth (%)

82

66

23

30

28

Prov. & Cont.

236

453

558

691

846

- YoY Growth (%)

125

92

23

24

22

Profit Before Tax

252

357

441

608

821

- YoY Growth (%)

55

42

23

38

35

Prov. for Taxation

85

117

146

200

271

- as a % of PBT

34

33

33

33

33

PAT

168

240

296

407

550

- YoY Growth (%)

50

43

23

38

35

Balance Sheet

Y/E March (` cr)

FY16

FY17

FY18E

FY19E

FY20E

Share Capital

91

97

97

97

97

Reserve & Surplus

1,612

2,206

2,465

2,820

3,301

Net Worth

1,703

2,304

2,562

2,918

3,398

Borrowings

11,955

14,108

17,635

21,691

26,246

- Growth (%)

42

18

25

23

21

Other Liabilities

65

80

88

109

133

Total Provisions

113

119

142

175

214

Current Liabilities

689

1,044

1,270

1,886

2,645

Total Liabilities

14,525

17,655

21,697

26,779

32,637

Total Loans & Advances

12,656

15,136

19,071

23,648

28,851

- Growth (%)

40

20

26

24

22

Cash and Cash equivalents

1,113

1,594

1,648

2,042

2,489

Investments

184

259

269

334

407

Fixed Assets

29

65

57

71

86

Other CA

333

392

441

546

666

Other Non Current Assets

210

211

210

138

138

Total Assets

14,525

17,655

21,697

26,779

32,637

January 01, 2018

10

Capital First Ltd | Initiating Coverage

Exhibit 18: Key Ratio

Y/E March

FY16

FY17

FY18E

FY19E

FY20E

Profitability ratios (%)

NIMs

7.1

8.8

9.2

9.4

9.7

RoA

1.2

1.4

1.4

1.5

1.7

RoE

10.2

12.0

12.2

14.9

17.4

Cost/Income

50.7

50.6

49.9

48.7

47.5

Asset Quality (%)

Gross NPAs %

1.1

1.7

1.8

1.9

1.9

Net NPAs %

0.6

1.0

1.1

1.1

1.2

Credit Cost

1.9

2.8

2.8

2.8

2.8

PCR %

48.6

39.4

38.9

42.1

39.5

Per Share Data (`)

EPS

17

25

30

42

56

BVPS

174

236

262

298

347

Adj BV

167

220

240

272

313

DPS

2.2

2.6

3.2

4.4

5.9

Valuation Ratios

PER (x)

40.3

28.2

22.9

16.6

12.3

P/BVPS (x)

4.0

2.9

2.6

2.3

2.0

P/ABVPS (x)

4.1

3.1

2.9

2.5

2.2

Dividend Yield (%)

0.3

0.4

0.5

0.6

0.9

DuPont Analysis

Interest Income

11.5

13.5

13.7

14.0

14.2

Interest Expenses

6.2

6.6

6.5

6.5

6.4

NII

5.3

7.0

7.2

7.5

7.8

Provision

1.6

2.6

2.6

2.6

2.6

Fees & Other

1.5

2.3

2.0

2.0

2.0

Total Income Adj Prov

5.2

6.7

6.6

6.9

7.1

Opex

3.5

4.7

4.6

4.6

4.6

PBT

1.7

2.0

2.0

2.3

2.5

Tax

0.6

0.7

0.7

0.7

0.8

ROA

1.2

1.4

1.4

1.5

1.7

Leverage

8.9

8.8

8.9

9.8

10.3

ROAN

10.2

12.0

12.2

14.9

17.4

Source: Note - Valuation done on closing price of 28/12/2017

January 01, 2018

11

Capital First Ltd | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Capital First Ltd

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)