4QFY2016 Result Update | Pharmaceutical

May 21, 2016

Cadila Healthcare

BUY

CMP

`325

Performance Highlights

Target Price

`400

Investment Period

12 Months

Y/E March (` cr)

4QFY2016 3QFY2016

% chg (qoq) 4QFY2015

% chg (yoy)

Net sales

2,376

2342

1.4

2247

5.7

Stock Info

Other income

99

112

(12.1)

63

57.3

Sector

Pharmaceutical

Gross profit

1553

1542

0.7

1445

7.5

Market Cap (` cr)

33,220

Operating profit

508

492

3.2

455

11.7

Net debt (` cr)

1,550

Adj. Net profit

388

390

(0.4)

351

10.6

Source: Company, Angel Research

Beta

0.7

52 Week High / Low

454 / 296

For 4QFY2016, Cadila Healthcare (Cadila) posted a robust performance on the

Avg. Daily Volume

1,12,106

net profit front while sales came in lower than expected. Sales came in at

Face Value (`)

1

`2,376cr (V/s `2,400cr expected), growing by 5.7% yoy. On the operating front,

BSE Sensex

25,400

the OPM came in at 21.4% V/s 21.1% expected and V/s 20.2% in 4QFY2015.

Nifty

7,783

The expansion in the OPM was driven by expansion in the GPM to 65.4% (V/s

Reuters Code

CADI.BO

64.3% in 4QFY2015) despite increase in staff expenditure and other expenditure

Bloomberg Code

CDH@IN

by 13.7% yoy 3.8% yoy respectively. R&D expenditure during the quarter came in

at 7.6% V/s 8.4% of sales in 4QFY2015. The Adj. net profit came in at `388cr V/s

`373cr expected and V/s `351cr in 4QFY2015, ie a yoy growth of 10.6%. We

Shareholding Pattern (%)

maintain our Buy on the stock.

Promoters

74.8

MF / Banks / Indian Fls

9.7

Results better than expected at the net profit level: For 4QFY2016, sales came in

FII / NRIs / OCBs

9.6

at `2,342cr (V/s `2,400cr expected), growing by 5.7% yoy. On the operating

Indian Public / Others

6.0

front, the OPM came in at 21.4% V/s 21.1% expected and V/s 20.2% in

4QFY2015. The expansion in the OPM was driven by expansion in the GPM to

65.4% (V/s 64.3% in 4QFY2015) and despite 13.7% yoy growth in the staff

Abs.(%)

3m 1yr 3yr

expenditure and 3.8% yoy rise in other expenditure. R&D expenditure during the

Sensex

7.1

(8.1)

(8.1)

quarter came in at 7.6% V/s 8.4% of sales in 4QFY2015. The Adj. net profit came

Cadila

(0.8)

(6.3)

(84.4)

in at `388cr V/s `351cr in 4QFY2015, a yoy growth of 10.6%.

Outlook and valuation: We expect Cadila’s net sales to post a 17.8% CAGR to

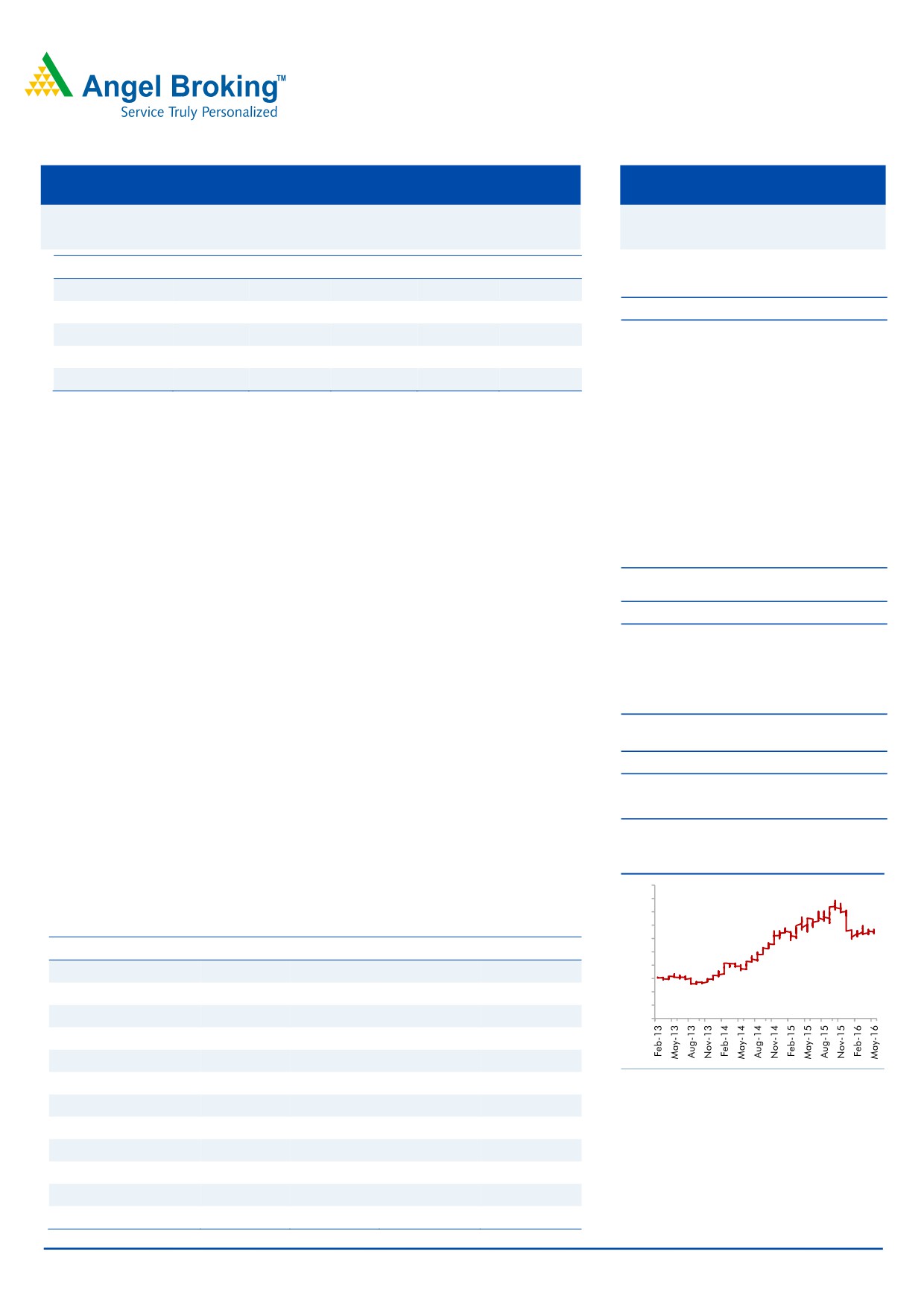

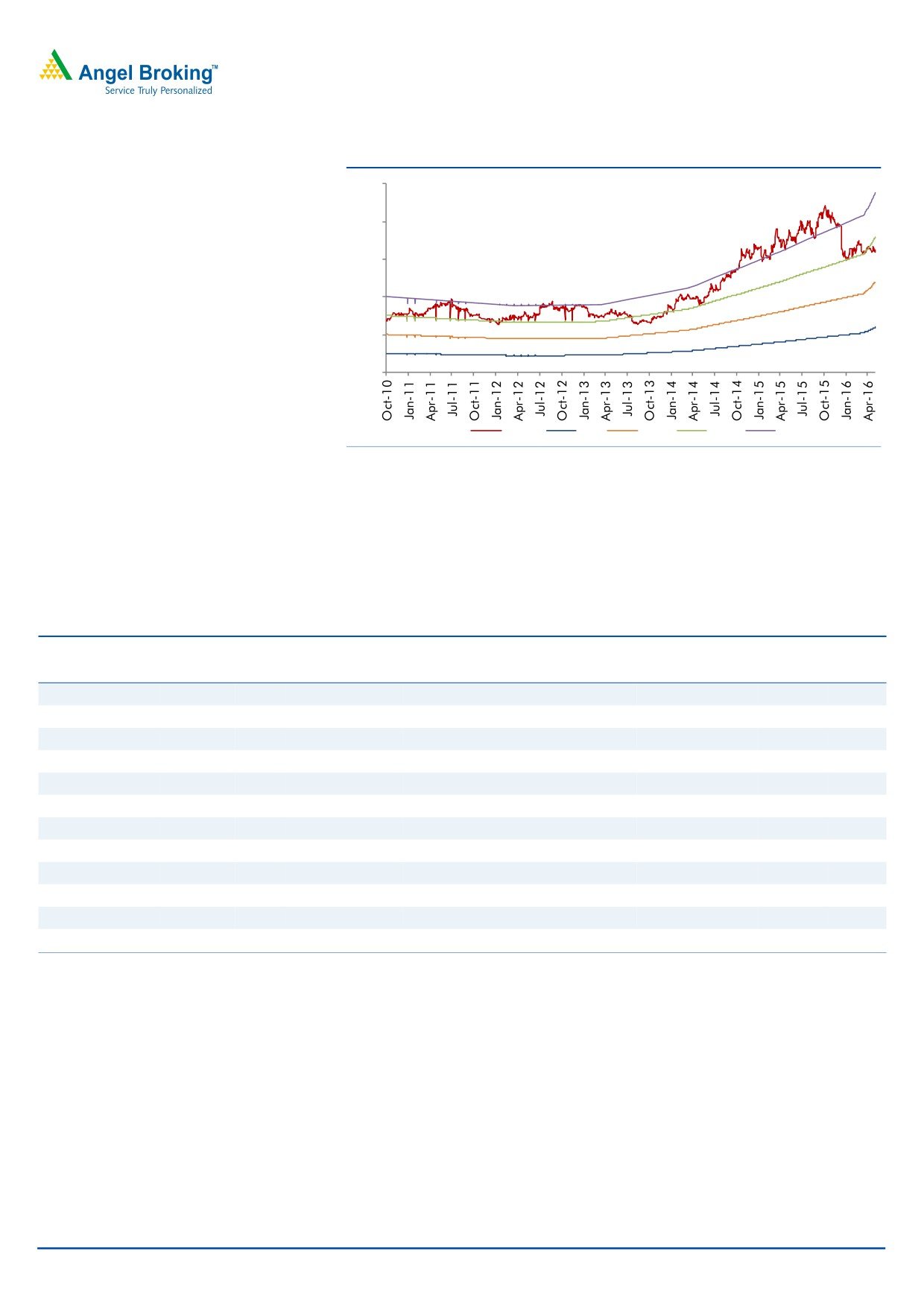

3-Year Daily Price Chart

`13,148cr and EPS to report a 15.8% CAGR to `20.0 over FY2016-18E. We

500

maintain our Buy rating on the stock.

450

400

Key financials (Consolidated)

350

300

Y E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

250

200

Net sales

8,497

9,469

11,126

13,148

150

100

% chg

20.4

11.4

17.5

18.2

50

Net profit

1,159

1,524

1,752

2,044

0

% chg

41.5

31.5

14.9

16.7

EPS

11.3

14.9

17.1

20.0

Source: Company, Angel Research

EBITDA margin (%)

18.8

21.2

22.0

22.0

P/E (x)

28.2

21.5

18.7

16.0

RoE (%)

30.1

31.7

28.8

26.6

RoCE (%)

20.2

23.1

24.2

24.3

P/BV (x)

7.7

6.1

4.8

3.8

Sarabjit Kour Nangra

EV/Sales (x)

4.0

3.5

2.9

2.3

+91 22 39357600 Ext: 6806

EV/EBITDA (x)

21.1

16.6

13.2

10.7

Source: Company, Angel Research; Note: CMP as of May 19, 2016

Please refer to important disclosures at the end of this report

1

Cadila Healthcare | 4QFY2016 Result Update

Exhibit 1: 4QFY2016 performance (Consolidated)

Y/E March (` cr)

4QFY2016

3QFY2016

% chg (qoq)

4QFY2015

% chg (yoy) FY2016 FY2015

% chg

Net Sales

2,376

2,342

1.4

2,247

5.7

9,469

8,497

11.4

Other Income

99

112

(12.1)

63

57.3

460

210

119.2

Total Income

2,474

2,454

0.8

2,310

7.1

9,930

8,707

14.0

Gross profit

1553

1542

0.7

1445

7.5

6192

5106

21.3

Gross margin (%)

65.4

65.9

64.3

65.4

60.1

Operating profit

508

492

3.2

455

11.7

2012

1600

25.8

Operating Margin (%)

21.4

21.0

20.2

21.2

18.8

Financial Cost

10

13

(20.6)

16

(38.6)

49

68

(28.5)

Depreciation

78

77

1.7

76

3.6

302

287

5.3

PBT

518

515

0.7

426

21.8

2122

1455

45.8

Tax

126

115

9.6

71

78.0

571

259

120.5

Adj. PAT before Extra-ordinary item

392

400

(1.8)

355

10.6

1551

1196

29.7

Exceptional loss/(gain)

(1)

0

1

2

(9)

Minority

(3)

9

(137.0)

5

30

36

Reported PAT

389

390

(0.2)

350

10.9

1523

1151

32.3

Adj. PAT

388

390

(0.4)

351

10.6

1524

1159

31.5

EPS (`)

3.8

3.8

3.4

14.9

11.3

Source: Company, Angel Research

Exhibit 2: 4QFY2016 - Actual vs. Angel estimates

(` cr)

Actual

Estimates

Variance

Net Sales

2,376

2,400

(1.0)

Operating profit

508

507

0.2

Tax

126

115

9.6

Net profit

388

373

3.9

Source: Company, Angel Research

Revenue up 8.4% yoy; marginally lower than our expectation

For 4QFY2016, the company posted sales of `2,376cr (V/s `2,400cr expected), a

growth of 8.4% yoy. Exports (`1,459.3cr) posted a 2.5% yoy growth during the

quarter while domestic markets (`968.7cr) posted a 10.4% yoy growth.

In exports the key market US (`961.0cr) posted a yoy de-growth of

1.8%,

while Europe (`70.6cr) posted a dip of 4.6%. Emerging Markets Formulations

(`134.3cr) posted a yoy growth of 21.3%. JVs and alliances (`145.9cr) posted a

dip of 23.8% yoy. In domestic markets, Indian formulations (`767.4cr) posted a

yoy growth of 12.9%.

May 21, 2016

2

Cadila Healthcare | 4QFY2016 Result Update

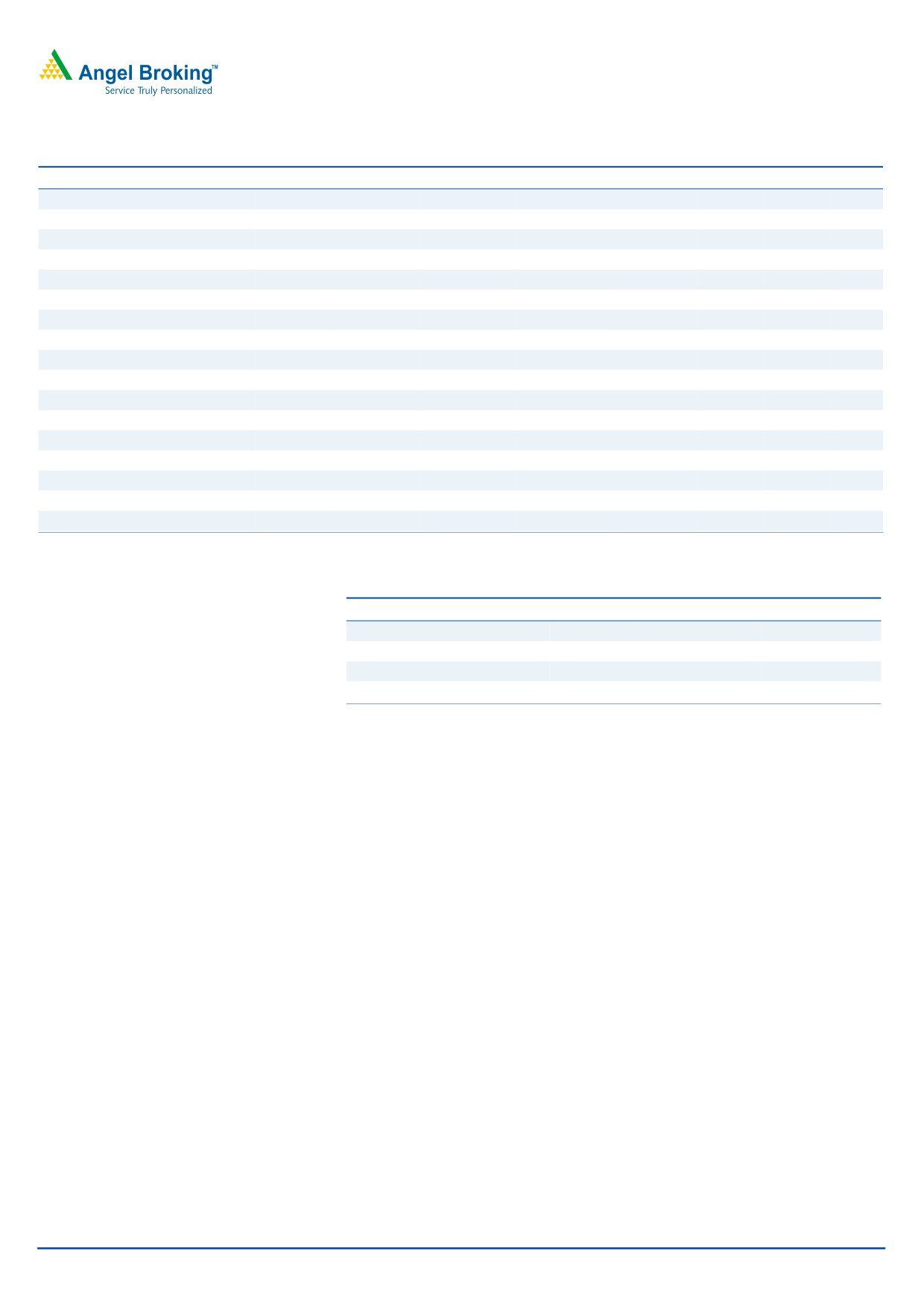

Exhibit 3: Sales trend in the US and Europe

1,200

1,072

979

985

1,004

961

1,000

800

600

400

200

74

84

65

76

70

0

4QFY2015

1QFY2016

2QFY2016

3QFY2016

4QFY2016

US

Europe

Source: Company, Angel Research

The growth in the domestic market (~40% of sales) was of 10.4% yoy, mainly led

by formulations (`767.4cr) which grew by 12.9% yoy. API (`92.2cr) on the other

hand grew by 6.0% yoy, while Wellness (`116.9cr) grew by 5.0% yoy. Animal

Health and others (`84.4cr) grew by 2.5% yoy.

Exhibit 4: Sales trend in Domestic Formulation and Consumer Wellness Divisions

900

767

800

742

751

713

680

700

600

500

400

300

200

111

111

112

118

117

100

0

4QFY2015

1QFY2016

2QFY2016

3QFY2016

4QFY2016

Domestic Formulation

Consumer division

Source: Company, Angel Research

On the CRAMS front, the company generated sales of `145.9cr (vs `117.8cr in

4QFY2015), reporting a growth of 23.8% yoy.

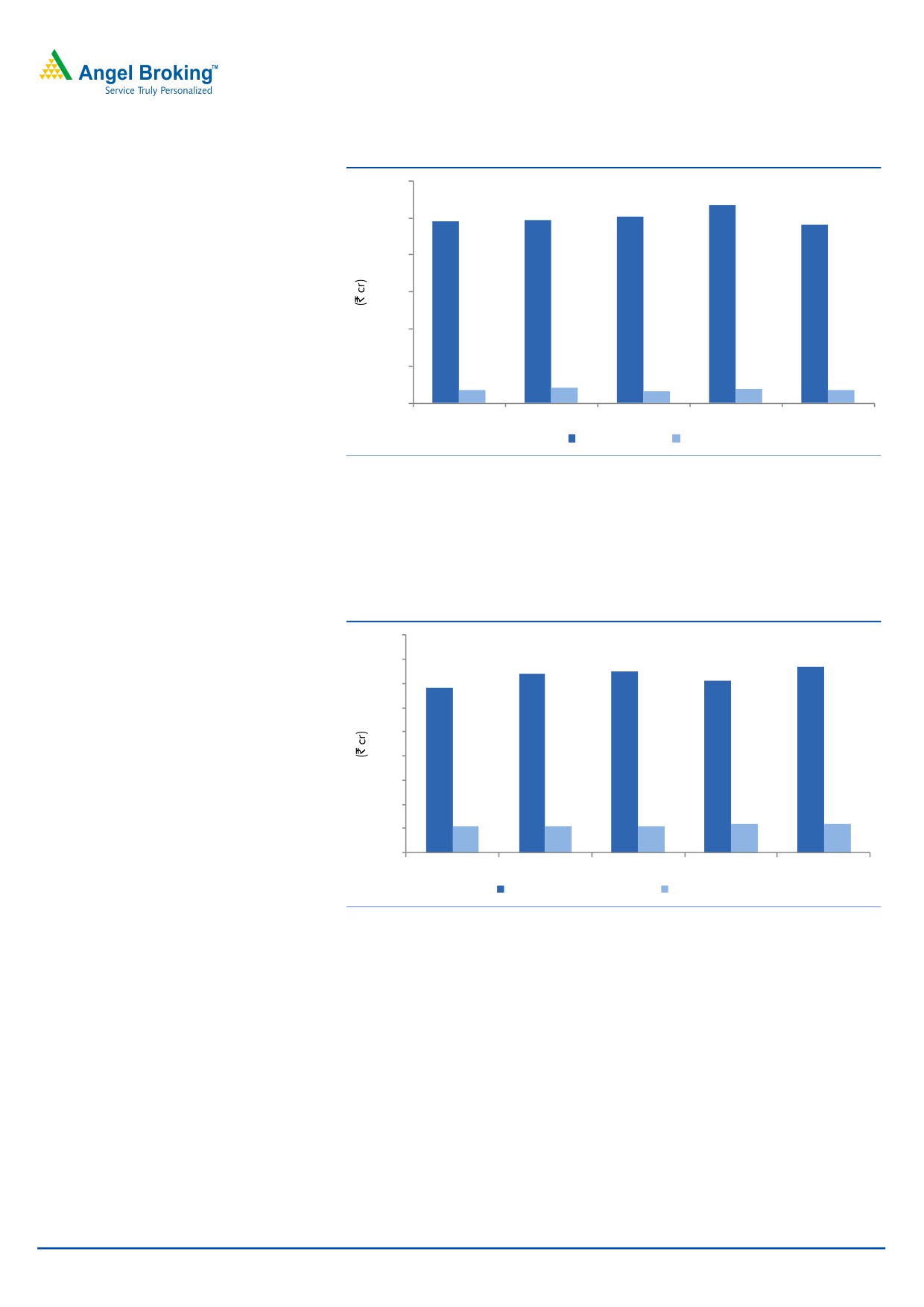

OPM better than expectation

On the operating front, the OPM came in at 21.4% V/s 21.1% expected and V/s

20.2% in 4QFY2015. The expansion in the OPM was driven by expansion in the

GPM to 65.4% (V/s 64.3% in 4QFY2015) and despite a 13.7% yoy growth in staff

expenditure and 3.8% rise in other expenditure. R&D expenditure during the

quarter came in at 7.6% V/s 8.4% of sales in 4QFY2015.

May 21, 2016

3

Cadila Healthcare | 4QFY2016 Result Update

Exhibit 5: OPM trend

23.0

22.5

22.6

22.0

21.5

21.4

21.0

20.5

21.0

20.0

20.2

20.1

19.5

19.0

18.5

4QFY2015

1QFY2016

2QFY2016

3QFY2016

4QFY2016

Source: Company, Angel Research

Net profit up 12.1% yoy: During the quarter, the company posted other income of

`99cr V/s `63cr in 4QFY2015. This aided the net profit to come in at `389cr V/s

`373cr expected and V/s `350cr in 4QFY2015, ie yoy growth of 10.9%. The Adj.

net profit came in at `388cr V/s `351cr in 4QFY2015, a yoy growth of 10.6%.

Exhibit 6: Adjusted Net profit trend

400

391

390

388

390

380

370

360

352

351

350

340

330

4QFY2015

1QFY2016

2QFY2016

3QFY2016

4QFY2016

Source: Company, Angel Research

Concall takeaways

Remediation at Moraiya is to be completed by May 2016. Cadila plans to

meet the USFDA over the next two months.

Tax rate is expected at ~20% in FY2017.

R&D as a percentage of sales to be at ~6% in FY2017.

Five product transfers have been carried out from Moraiya to Baddi in

4QFY2016 (taking the total to 12).

May 21, 2016

4

Cadila Healthcare | 4QFY2016 Result Update

Recommendation rationale

Strong domestic portfolio: Cadila is the fifth largest player in the domestic market

with sales of about `2,973cr in FY2016; the domestic market contributes ~39% to

its top-line. The company enjoys a leadership position in the CVS, GI, women

healthcare and respiratory segments, and has a sales force of 4,500 executives.

The company, on an aggressive front, launched more than 75 new products in

FY2014. During FY2009-14, the company reported a ~13% CAGR in its top-line

in the domestic formulation business.

Further, the company has a strong consumer division through its stake in Zydus

Wellness, which has premium brands such as Sugarfree, Everyuth and Nutralite,

under its umbrella. This segment which contributes ~4.7% of sales, registered a

growth of 3.2% yoy during FY2016.

Going forward, the company expects the segment to grow at an above-industry

rate on the back of new product launches and field force expansion. In FY2014,

sales were lower; however, FY2016 witnessed a rebound. During FY2016-18E, we

expect the domestic segment to grow at a CAGR of 9.6%.

Exports on a strong footing: Cadila has a two-fold focus on exports, wherein it is

targeting developed as well as emerging markets, which contributed around 61%

to its FY2016 top-line. The company has established a formidable presence in the

developed markets of US, Europe (France and Spain) and Japan. In the US, the

company achieved critical scale of `3,393cr on the sales front in FY2016. The

growth in exports to the US along with other regions like Europe would be driven

by new product launches, going forward. Overall, exports are expected to post a

CAGR of 17.5% over FY2016-18E.

Outlook and valuation

We expect Cadila’s net sales to post a 17.8% CAGR to `13,148cr and EPS to

report a 15.8% CAGR to `20.0 over FY2016-18E. We maintain our Buy rating on

the stock.

Exhibit 7: Key Assumptions

Key assumptions

FY2017E

FY2018E

Domestic growth (%)

13.0

15.0

Exports growth (%)

20.0

20.0

Growth in employee expenses (%)

24.1

15.8

Operating margins (excl tech. know-how fees) (%)

22.0

22.0

Capex (` cr)

650

650

Source: Company, Angel Research

May 21, 2016

5

Cadila Healthcare | 4QFY2016 Result Update

Exhibit 8: One-year forward PE band

500

400

300

200

100

0

Price

7x

14x

21x

28x

Source: Company

Company background: Cadila Healthcare‘s operations range across API,

formulations, animal health products and cosmeceuticals. The group has global

operations spread across USA, Europe, Japan, Brazil, South Africa and 25 other

emerging markets. Having already achieved the US$1bn sales mark in 2011, the

company aims to be a research-driven pharmaceutical company by 2020.

Exhibit 9: Recommendation Summary

Company

Reco

CMP Tgt. price Upside

FY2017E

FY15-17E

FY2017E

(`)

(`)

% PE (x) EV/Sales (x) EV/EBITDA (x)

CAGR in EPS (%) RoCE (%) RoE (%)

Alembic Pharma

Neutral

556

-

-

19.4

2.7

13.7

11.4

23.5

21.3

Aurobindo Pharma Accumulate

770

856

11.2

18.0

2.9

12.6

15.6

23.5

30.2

Cadila Healthcare Buy

325

400

23.3

18.7

2.9

12.6

22.9

24.2

28.8

Cipla

Buy

513

605

18.0

18.6

2.4

13.1

18.3

16.7

16.1

Dr Reddy's

Buy

3,021

3,476

15.0

19.8

2.8

11.8

6.8

19.2

18.7

Dishman Pharma Neutral

165

-

-

16.5

1.8

8.1

15.9

9.4

11.0

GSK Pharma*

Neutral

3,345

-

-

49.0

8.6

38.7

6.6

33.7

34.3

Indoco Remedies Neutral

261

-

-

19.2

2.1

11.4

23.0

19.7

19.7

Ipca labs

Buy

448

750

67.4

16.0

1.7

9.1

17.9

11.8

14.9

Lupin

Neutral

1,656

-

-

24.2

4.2

15.4

13.1

29.6

24.7

Sanofi India

Accumulate

4,292

4,738

10.4

28.0

3.8

22.2

34.2

21.0

25.6

Sun Pharma

Buy

792

950

19.9

29.5

5.2

16.8

8.4

15.8

16.6

Source: Company, Angel Research; Note: *December year ending

May 21, 2016

6

Cadila Healthcare | 4QFY2016 Result Update

Profit & Loss statement (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017E

FY2018E

Gross sales

6,285

7,208

8,658

9,660

11,336

13,396

Less: Excise duty

129

148

161

190

210

248

Net sales

6,155

7,060

8,497

9,469

11,126

13,148

Other operating income

203

164

154

368

368

368

Total operating income

6,358

7,224

8,651

9,838

11,494

13,517

% chg

20.8

13.6

19.8

13.7

16.8

17.6

Total expenditure

5,232

6,024

6,896

7,457

8,673

10,250

Net raw materials

2,320

2,714

3,197

3,277

4,005

4,733

Other mfg costs

387

443

534

595

699

826

Personnel

903

1,071

1,209

1,334

1,633

1,929

Other

1,622

1,796

2,107

2,252

2,336

2,761

EBITDA

923

1,036

1,601

2,012

2,453

2,899

% chg

1.4

12.3

54.6

25.6

21.9

18.2

(% of Net Sales)

15.0

14.7

18.8

21.2

22.0

22.0

Depreciation& amortisation

183

201

287

302

393

439

EBIT

740

835

1,314

1,710

2,059

2,460

% chg

(1.7)

12.8

57.4

30.1

20.4

19.4

(% of Net Sales)

12.0

11.8

15.5

18.1

18.5

18.7

Interest & other charges

169

90

68

49

84

84

Other income

37

51

55

94

94

94

(% of PBT)

5

5

4

4

4

3

Recurring PBT

811

959

1,456

2,124

2,437

2,838

% chg

2.1

18.3

51.8

45.9

14.8

16.4

Extraordinary expense/(Inc.)

-

17

10

2

-

-

PBT (reported)

811

942

1,445

2,124

2,437

2,838

Tax

119.5

106.0

259.4

571.1

655.6

763.3

(% of PBT)

14.7

11.3

17.9

26.9

26.9

26.9

PAT (reported)

692

836

1,186

1,553

1,782

2,074

Less: Minority interest (MI)

36.4

32.6

35.5

30.0

30.0

30.0

PAT after MI (reported)

655

804

1,151

1,523

1,752

2,044

ADJ. PAT

655

819

1,159

1,524

1,752

2,044

% chg

0.8

25.0

41.5

31.5

14.9

16.7

(% of Net Sales)

10.6

11.4

13.5

16.1

15.7

15.5

Adj.Basic EPS (`)

6.4

8.0

11.3

14.9

17.1

20.0

Adj. Fully Diluted EPS (`)

6.4

8.0

11.3

14.9

17.1

20.0

% chg

0.8

25.0

41.5

31.5

14.9

16.7

May 21, 2016

7

Cadila Healthcare | 4QFY2016 Result Update

Balance Sheet (Consolidated)

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017E

FY2018E

SOURCES OF FUNDS

Equity share capital

102

102

102

102

102

102

Reserves & Surplus

2,938

3,337

4,149

5,250

6,714

8,471

Shareholders funds

3,040

3,439

4,252

5,352

6,816

8,574

Minority interest

119

144

169

135

165

195

Total loans

2,681

2,265

2,334

2,107

2,107

2,107

Other Long Term Liabilities

47

55

43

61

45

46

Long Term Provisions

64

76

110

77

78

79

Deferred tax liability

100

96

59

88

121

122

Total liabilities

6,053

6,075

6,966

7,820

9,209

10,998

APPLICATION OF FUNDS

Gross block

4,104

3,756

4,353

5,296

5,946

6,596

Less: Acc. depreciation

1,358

1,540

1,827

2,130

2,523

2,962

Net block

2,746

2,214

2,526

3,166

3,423

3,634

Capital Work-in-Progress

248

892

892

892

892

892

Goodwill

862

908

733

733

733

733

Investments

21

87

154

266

266

266

Long Term Loans and Adv.

411

495

637

756

663

779

Current assets

3,191

3,391

4,105

4,205

6,245

8,254

Cash

582

549

670

695

1,967

3,259

Loans & advances

279

341

334

335

336

337

Other

2,330

2,501

3,102

3,174

3,942

4,658

Current liabilities

1,426

1,912

2,081

2,196

3,012

3,560

Net Current assets

1,765

1,480

2,024

2,008

3,233

4,694

Mis. Exp. not written off

-

-

-

(1)

-

-

Total assets

6,053

6,075

6,966

7,820

9,209

10,998

May 21, 2016

8

Cadila Healthcare | 4QFY2016 Result Update

Cash Flow Statement (Consolidated)

Y/E March (` cr)

FY2013 FY2014 FY2015 FY2016 FY2017E FY2018E

Profit before tax

811

942

1,445

2,124

2,437

2,838

Depreciation

183

201

287

302

393

439

(Inc)/Dec in Working Capital

(223)

168

(565)

(78)

141

(286)

Less: Other income

37

51

55

94

94

94

Direct taxes paid

119

106

259

571

656

763

Cash Flow from Operations

614

1,154

853

1,683

2,222

2,133

(Inc.)/Dec.in Fixed Assets

(860)

(296)

(597)

(943)

(650)

(650)

(Inc.)/Dec. in Investments

3

(65)

(68)

(112)

-

-

Other income

37

51

55

94

94

94

Cash Flow from Investing

(820)

(310)

(609)

(960)

(556)

(556)

Issue of Equity

-

-

-

-

-

-

Inc./(Dec.) in loans

382

(397)

91

(242)

(16)

2

Dividend Paid (Incl. Tax)

(175)

(216)

(287)

(287)

(287)

(287)

Others

115

(264)

74

(168)

(91)

0

Cash Flow from Financing

322

(877)

(122)

(697)

(394)

(285)

Inc./(Dec.) in Cash

116

(33)

121

25

1,272

1,292

Opening Cash balances

467

582

549

670

695

1,967

Closing Cash balances

582

549

670

695

1,967

3,259

May 21, 2016

9

Cadila Healthcare | 4QFY2016 Result Update

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016

FY2017E

FY2018E

Valuation Ratio (x)

P/E (on FDEPS)

50.0

40.0

28.2

21.5

18.7

16.0

P/CEPS

39.0

32.0

22.6

17.9

15.2

13.2

P/BV

10.8

9.5

7.7

6.1

4.8

3.8

Dividend yield (%)

2.3

2.3

2.3

2.3

2.3

2.3

EV/Sales

1.4

1.1

4.0

3.5

2.9

2.3

EV/EBITDA

9.0

7.6

21.1

16.6

13.2

10.7

EV / Total Assets

1.4

1.3

4.9

4.3

3.5

2.8

Per Share Data (`)

EPS (Basic)

6.4

8.0

11.3

14.9

17.1

20.0

EPS (fully diluted)

6.4

8.0

11.3

14.9

17.1

20.0

Cash EPS

8.2

10.0

14.2

17.9

21.0

24.3

DPS

7.5

7.5

7.5

7.5

7.5

7.5

Book Value

29.7

33.6

41.5

52.3

66.6

83.8

Dupont Analysis

EBIT margin

12.0

11.8

15.5

18.1

18.5

18.7

Tax retention ratio

85.3

88.7

82.1

73.1

73.1

73.1

Asset turnover (x)

1.2

1.3

1.5

1.5

1.6

1.8

ROIC (Post-tax)

12.8

13.8

18.6

19.4

21.7

24.7

Cost of Debt (Post Tax)

5.8

3.2

2.4

1.6

2.9

2.9

Leverage (x)

0.7

0.6

0.4

0.3

0.1

0.0

Operating ROE

17.7

20.1

25.8

25.2

24.3

24.7

Returns (%)

ROCE (Pre-tax)

13.2

13.8

20.2

23.1

24.2

24.3

Angel ROIC (Pre-tax)

19.5

20.6

31.3

33.6

37.0

41.9

ROE

23.3

25.3

30.1

31.7

28.8

26.6

Turnover ratios (x)

Asset Turnover (Gross Block)

1.8

1.8

2.1

2.0

2.0

2.2

Inventory / Sales (days)

66

69

61

56

71

80

Receivables (days)

54

57

57

45

58

65

Payables (days)

42

55

46

45

53

53

WC (ex-cash) (days)

66

53

48

49

41

36

Solvency ratios (x)

Net debt to equity

0.7

0.5

0.4

0.3

0.0

(0.1)

Net debt to EBITDA

2.3

1.7

1.0

0.7

0.1

(0.4)

Interest Coverage (EBIT / Int.)

4.4

9.3

19.4

35.2

24.4

29.2

May 21, 2016

10

Cadila Healthcare | 4QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Cadila Healthcare

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

May 21, 2016

11