3QFY2017 Result Update | Automobile

February 13, 2017

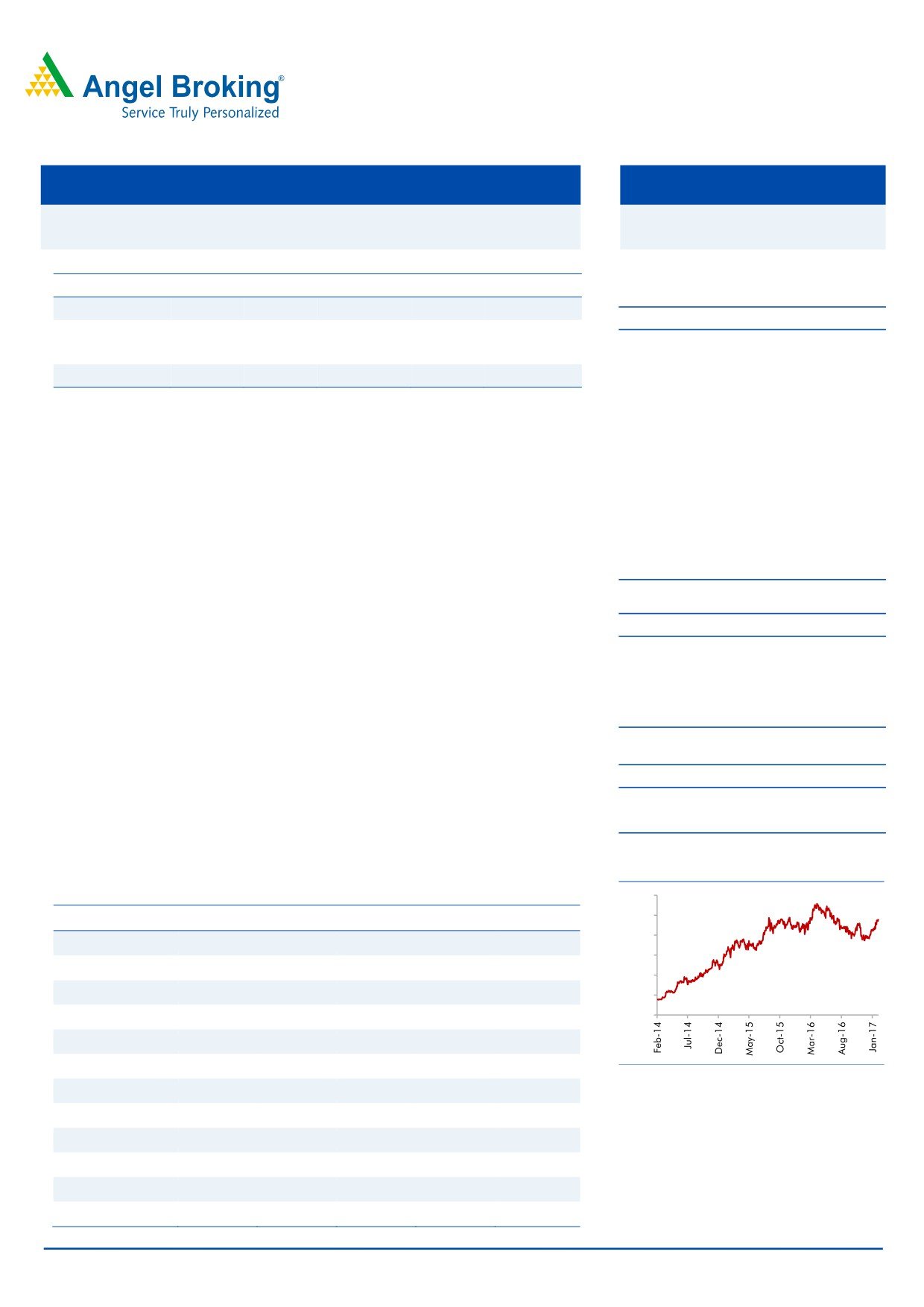

Ashok Leyland

BUY

CMP

`93

Performance Highlights

Target Price

`111

Quarterly highlights (Standalone)

Investment Period

12 Months

Y/E March (` cr)

3QFY17 3QFY16

% chg (yoy) 2QFY17

% chg (qoq)

Net Sales

4,431

4,114

7.7

4,622

(4.1)

Stock Info

EBITDA

454

444

2.3

536

0.0

Sector

Automobile

EBITDA margin (%)

10

11

(55 bps)

12

(136 bps)

Market Cap (` cr)

26,452

Adj. PAT

250

217

14.8

294

196.0

Net Debt (` cr)

(1,211)

Source: Company, Angel Research

Beta

1.2

Overall good results during tough times: Ashok Leyland reported 7.7% growth in

52 Week High / Low

113/74

top line and 14.8% growth in the bottom line. Net realization grew by 1.3% yoy to

Avg. Daily Volume

1,330,069

`13.20 lakh per vehicle. Operating profit grew by 2.2% to `454cr in Q3FY17;

Face Value (`)

1.0

EBITDA margins declined by 55bps yoy to 10.25% vs. 10.80% in Q3FY16. The

BSE Sensex

28,334

decline in EBITDA margins was due to higher discounts and increase in raw

Nifty

8,794

material prices. Reported PAT declined by 13% yoy to `185.9cr due to loss of

Reuters Code

ASOK.BO

`67.3cr on swap contracts. Adjusted PAT grew by 14.8% yoy to 249.6cr. The

Bloomberg Code

AL@IN

company during the quarter saw 6% yoy growth in its total volumes to 32,838.

This came despite industry witnessed negative impact of demonetisation. The

MHCV volumes grew by 9% while LCV volumes declined by 2%.

Shareholding Pattern (%)

Promoters

50.4

Outlook and valuation While demonetisation has negatively impacted the

automobile industry, we are expecting faster recovery in the volumes with

MF / Banks / Indian Fls

8.9

improving liquidity. The quantum of recovery cannot be assessed at this time. We

FII / NRIs / OCBs

28.7

forecast ALL’s volume growth of 8% and 9% in FY18E and FY19E. Company has

Indian Public / Others

12.0

taken a 4% price hike in January hence we believe that margins are likely to see

minor expansion going ahead. We forecast average 21% ROE for FY18E and

Abs. (%)

3m 1yr 3yr

FY19E showing significant improvement from its ROE profile in FY16. The

Sensex

5.6

23.4

39.1

improving consumer sentiment and government’s initiative to boost the

Ashok Leyland

9.0

17.4

506.7

infrastructure would play out positively for Ashok Leyland. Overall we expect 10%

and 13% CAGR in revenue and net profit over next two years. We value the stock at

19x of FY2019E EPS `5.8 and maintain buy rating with price target of `111.

3 year price chart

Key financials (Standalone)

120.0

100.0

Y/E March (` cr)

FY2015

FY2016

2017E

2018E

2019E

80.0

Net Sales

13,562

18,822

20,021

21,915

24,076

60.0

% chg

36.4

38.8

6.4

9.5

9.9

40.0

Adjusted net profit

234

1,111

1,294

1,514

1,655

20.0

0.0

% chg

-

375.1

16.4

17.0

9.3

EBITDA (%)

7.7

11.6

11.6

11.9

11.6

EPS (`)

1.2

2.5

4.5

5.3

5.8

Source: Company, Angel Research

P/E (x)

79.0

36.6

20.4

17.5

16.0

P/BV (x)

5.2

4.8

4.2

3.8

3.4

RoE (%)

6.5

13.1

20.6

21.5

21.0

RoCE (%)

7.2

21.1

20.2

21.2

21.7

Shrikant Akolkar

EV/Sales (x)

1.9

1.4

1.3

1.1

1.0

022-3935 7800 Ext: 6846

EV/EBITDA (x)

25.7

11.8

11.1

9.6

8.7

Source: Company, Angel Research; Note: CMP as of February 10, 2017

Please refer to important disclosures at the end of this report

1

Ashok Leyland | 3QFY2017 Result Update

Exhibit 1: Quarterly financial performance (Standalone)

Y/E March (` cr)

3QFY17

3QFY16

% chg (yoy)

2QFY17

% chg (qoq)

9MFY17

9MFY17

% chg (yoy)

Net Sales

4,431

4,114

7.7

4,622

(4.1)

13,312

12,964

2.7

Consumption of RM

3,134

2,875

9.0

3,134

0.0

9,198

8,994

2.3

(% of sales)

70.7

69.9

67.8

69.1

69.4

Staff costs

362

347

4.1

369

(2.1)

1,089

1,053

3.5

(% of sales)

8.2

8.4

8.0

8.2

8.1

Purchase of traded goods

481

447

7.8

583

(17.4)

1,558

1,614

(3.4)

(% of sales)

10.9

10.9

12.6

11.7

12.4

Total Expenditure

3,977

3,670

8.4

4,086

(2.7)

11,845

11,660

1.6

Operating Profit

454

444

2.3

536

(15.3)

1,467

1,304

12.5

OPM (%)

10.3

10.8

11.6

11.0

10.1

Interest

31

60

(48.4)

34

(8.2)

99

193

(48.9)

Depreciation

119

119

(0.1)

126

(5.4)

366

356

2.8

Other income

(40)

28

(243.1)

38

(205.3)

92

73

25.3

PBT (excl. Extr. Items)

264

293

415

1,094

827

Extr. income/expense

0

0

0

0

0

PBT (incl. Extr. Items)

264

293

(9.9)

415

(36.4)

1,094

827

32.2

(% of sales)

6.0

7.1

9.0

8.2

6.4

Provision for taxation

78

79

120

323

297

(% of PBT)

29.5

27.0

29.0

29.5

35.9

Reported PAT

186

214

(13.0)

294

(36.9)

771

530

45.4

Adj PAT

250

217

14.8

294

835

619

Adj. PATM

5.6

5.3

6.4

6.3

4.8

Equity capital (cr)

285

285

285

285

285

Adjusted EPS (`)

0.9

0.8

1.0

2.9

2.2

Source: Company, Angel Research

Exhibit 2: Quarterly volume performance

(units)

3QFY17

3QFY16

% chg (yoy)

2QFY17

% chg (qoq)

9MFY17

9MFY17

% chg (yoy)

MHCV passenger

25,284

23,176

9.1

25,341

(0.2)

74,652

74,513

0.2

MHCV goods

7,554

7,752

(2.6)

8,100

(6.7)

22,792

21,950

3.8

Total volume (ex. Dost)

32,838

30,928

6.2

33,441

(1.8)

97,444

96,463

1.0

Source: Company, Angel Research

February 13, 2017

2

Ashok Leyland | 3QFY2017 Result Update

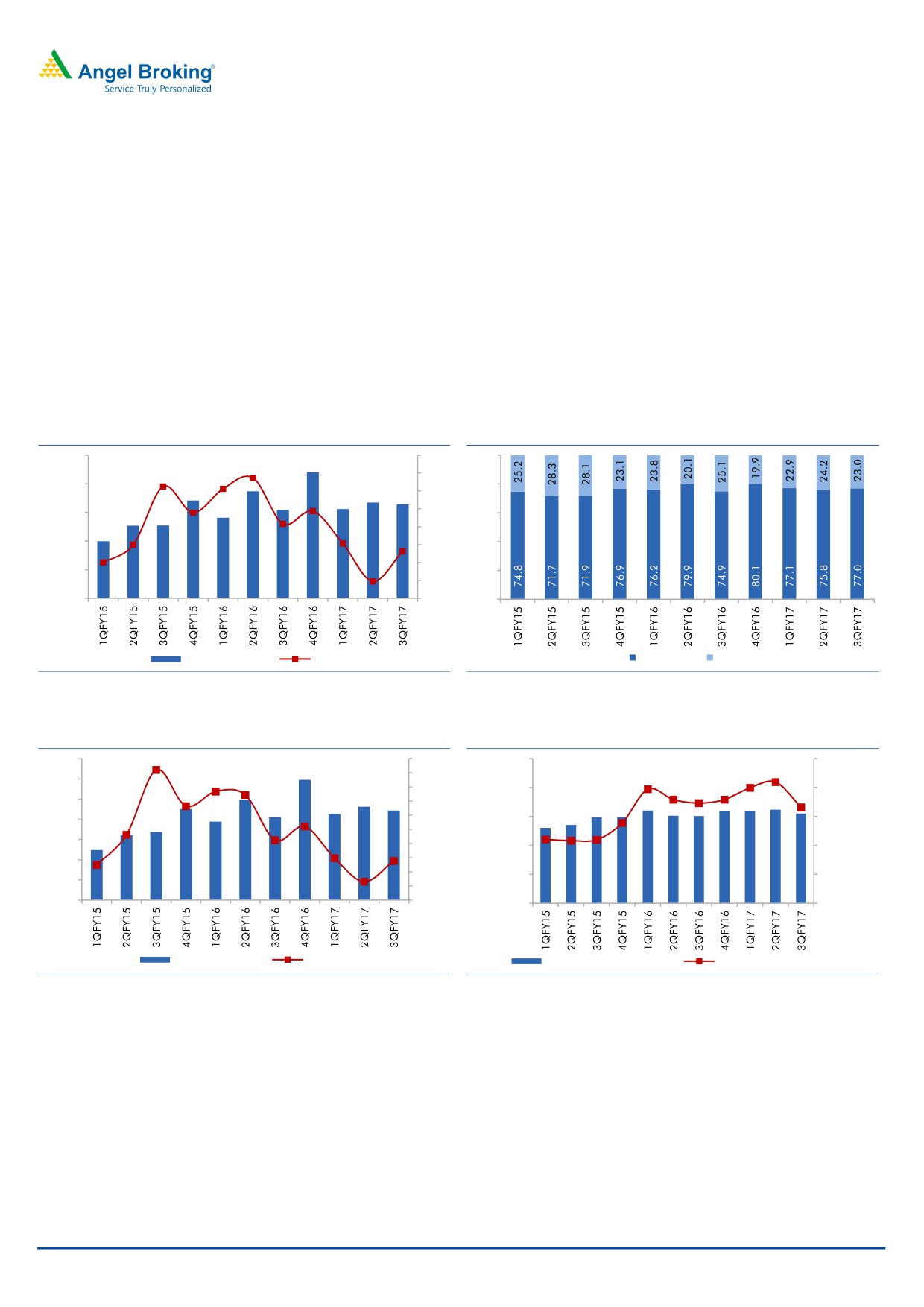

ALLs MHCV volumes grew by

9% yoy during the quarter showing

demonetisation has not led to a negative impact on its MHCV business. The

industry, during this period grew by 3%.

Realization/vehicle declined by

1.3% yoy to

`13.20 lakh, as company

increased discounts from `2.5 lakh per vehicle to ~`3.3 lakh per vehicle.

RM cost per vehicle increased by 2.6% yoy to ` 9.54 lakh. This was due to

increase in the raw material costs.

ALL has continued to increase its market share on the back of higher

proportion of the fast growing heavy trucks and geographical expansion. ALL’s

market share improved from 30.1% in Q3FY16 to 33.7% in Q3FY17.

Exhibit 3: Volume grew despite demonetisation

Exhibit 4: MHCVs share in product mix rises yoy

50,000

60

100

50

40,000

80

40

30,000

30

60

20

20,000

40

10

0

10,000

20

(10)

0

(20)

0

Overall Volumes

yoy chg %

MHCV (%)

LCV (%)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 5: Net sales growth at 7.7%

Exhibit 6: Realisation & contribution trend

7,000

80.0

17,00,000

4,50,000

70.0

6,000

60.0

15,00,000

4,00,000

5,000

50.0

4,000

40.0

13,00,000

3,50,000

30.0

3,000

20.0

11,00,000

3,00,000

2,000

10.0

0.0

9,00,000

2,50,000

1,000

-10.0

0

-20.0

7,00,000

2,00,000

Net sales (` cr)

Growth %

Realisation/vehicle (`)

Contribution/vehicle (`)

Source: SIAM, Angel Research

Source: SIAM, Angel Research

Company has indicated of greater focus on exports, LCV and aftermarket

business going ahead.

February 13, 2017

3

Ashok Leyland | 3QFY2017 Result Update

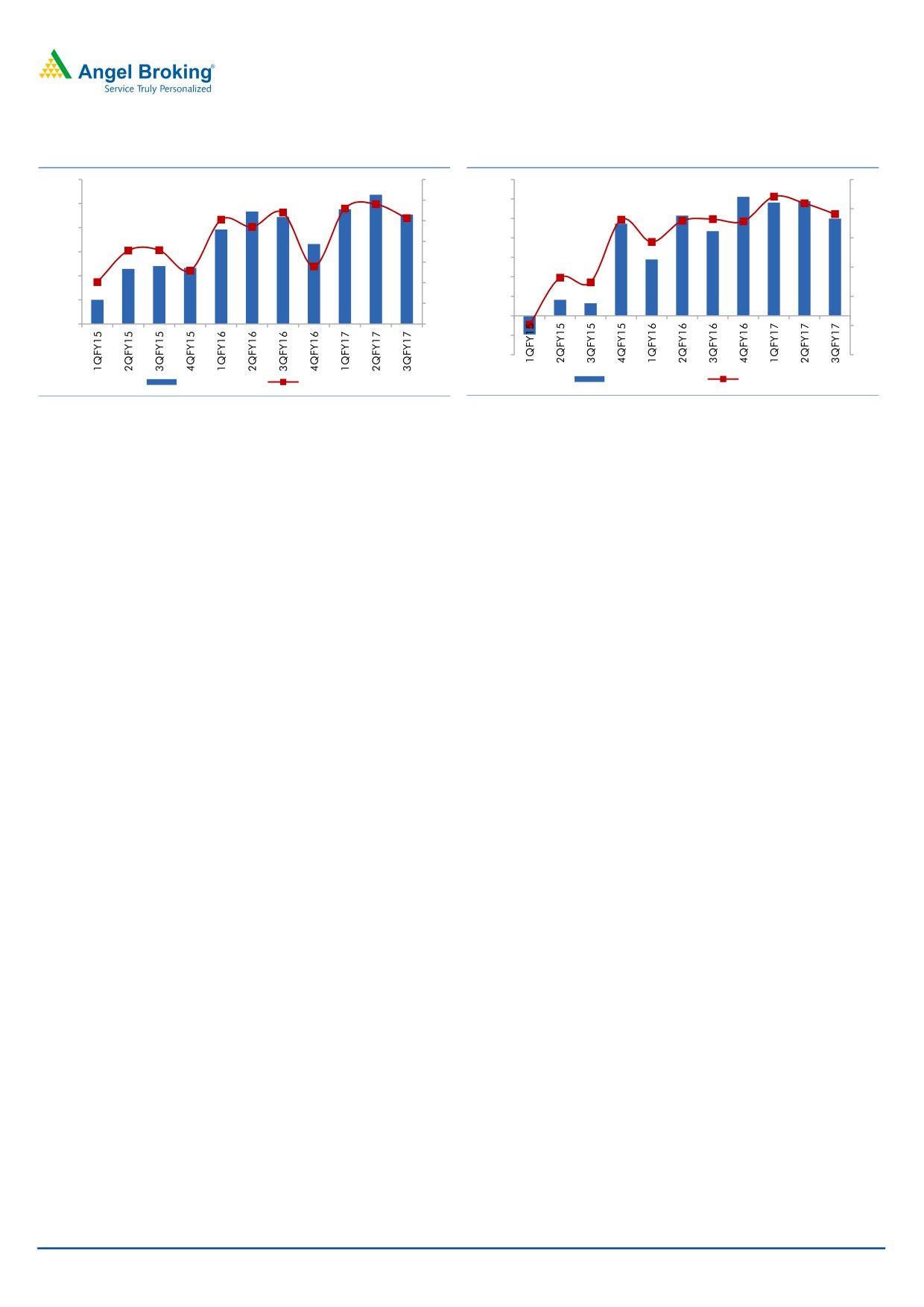

Exhibit 7: EBITDA margin declines due to higher costs

Exhibit 8: Bottom-line continues to improve yoy

600.0

14

350.0

8

12

300.0

500.0

6

10

250.0

400.0

8

200.0

4

300.0

150.0

6

2

200.0

100.0

4

100.0

50.0

0

2

0.0

0.0

0

(2)

(50.0)

(100.0)

(4)

EBIDTA (` cr)

Margin %

Net Profit (` cr)

Margin %

Source: Company, Angel Research

Source: Company, Angel Research

Conference call - Key highlights

Company reported 9% yoy growth in its MH&CV (bus + truck) volumes

whereas LCV volumes saw 2.5% yoy decline

During the quarter, exports revenue was at `388cr and company expects

export revenue contribution to be ~25% of sales in next 4-5 years.

FY17E Capex at `500cr

Company’s market share increased from 30.1% in Q3FY16 to 33.7% in

Q3FY17

During the quarter company reported higher discounts of ~ `3.30 lakh.

Due to higher RM prices, company reported decline in the operating margins.

While in Q3, company was not able to pass on the prices, it has increased

prices by ~4% in January.

Company has indicated of higher LCV sales going ahead and expects to

increase its aftermarket share from 10% to 15%.

Investment arguments

Volumes recovery in FY18E: ALL continues to report a good set of volumes. The

Implementation of BSIV standards is also expected to be positive for the stock and

company expects pre-buying in next few months. This implies that the volumes are

expected to recover faster, shrugging off the demonetisation impact. We remain

positive on its volume growth. Company has also indicated to increase its LCV

market share to ~30% with new product launches in coming years.

Pure CV play: ALL is a pure CV play and is expected to benefit from government’s

push to improve infrastructure. The MHCV segment, accounts for 3/4th of ALLs total

volumes and has grown at a 3 year CAGR of 11% by FY16. We expect the

momentum to continue, in FY18E and FY19E as economic outlook improves.

Return ratio to improve: ALL has taken 4% price hike in January and we expect

further price hikes as company anticipates volume growth on the back of

February 13, 2017

4

Ashok Leyland | 3QFY2017 Result Update

implementation of new emission standards. We expect ALL’s margins to remain at

the current levels for new two years (11.6%). This level of margins is significantly

higher than the margins seen during FY12-FY15 when automobile industry was

going through a period of slower growth. Owing to this, company is expected to

see improvement in RoE profile. We expect ALL’s average RoE to remain at

~21.2% over next two years indicating strong improvement in return ratios.

Outlook and valuation

While demonetisation has negatively impacted the automobile industry, we are

expecting faster recovery in the volumes with improving liquidity. The quantum of

recovery cannot be assessed at this time. We forecast ALL’s volume growth of 8%

and 9% in FY18E and FY19E. Company has taken a 4% price hike in January

hence we believe that margins are likely to see minor expansion going ahead. We

forecast average 21% ROE for FY18E and FY19E showing significant improvement

from its ROE profile in FY16. The improving consumer sentiment and

government’s initiative to boost the infrastructure would play out positively for

Ashok Leyland. Overall we expect 10% and 13% CAGR in revenue and net profit

over next two years. We value the stock at 19x of FY2019E EPS `5.8 and maintain buy

rating with PT of `111 (11x FY2019E EV/EBITDA multiple).

Exhibit 9: Key assumptions

(units)

FY2013

FY2014

FY2015

FY2016E

FY2017E

FY2018E

MH&CV

79,694

60,342

77,660

109,762

112,674

122,821

LCV

34,917

28,995

27,242

30,695

31,980

33,904

Total volume (units)

114,611

89,337

104,902

140,457

144,654

156,725

% yoy chg

12.4

(22.1)

17.4

33.9

3.0

8.3

Source: Company, Angel Research

Company background

Ashok Leyland Ltd (ALL) is the country's second largest CV manufacturer. The

company has a strong presence in the MHCV segment, with a domestic market

share of ~34% as of Q3FY2017. ALL enjoys a dominant position in southern

India, and has been focusing on expanding its presence in northern and western

India by increasing its touch points in the region. The company intends to increase

its market share in trucks by launching new products under Guru and Partner

range.

February 13, 2017

5

Ashok Leyland | 3QFY2017 Result Update

Profit and loss statement (Standalone)

Y/E March (` cr)

FY2015

FY2016

2017E

2018E

2019E

Total operating income

13,562

18,822

20,021

21,915

24,076

% chg

36.4

38.8

6.4

9.5

9.9

Total Expenditure

12,536

16,656

17,748

19,352

21,333

Cost of Materials

9,965

13,262

13,692

14,977

16,528

Personnel

1,184

1,399

1,626

1,759

1,933

Others Expenses

1,386

1,995

2,430

2,615

2,872

EBITDA

1,027

2,166

2,273

2,564

2,743

% chg

778.3

111.0

4.9

12.8

7.0

(% of Net Sales)

7.7

11.6

11.6

11.9

11.6

Depreciation& Amortisation

416

444

459

486

486

EBIT

610

1,722

1,814

2,078

2,257

% chg

(334.6)

182.2

5.3

14.5

8.6

(% of Net Sales)

4.6

9.3

9.3

9.7

9.6

Interest & other Charges

394

274

133

134

134

Other Income

124

110

159

219

241

(% of PBT)

36.5

7.0

8.6

10.1

10.2

Share in profit of Ass.

-

-

-

-

-

Recurring PBT

341

1,559

1,840

2,163

2,364

% chg

(157.2)

356.7

18.1

17.5

9.3

Prior Period & Extra. Exp.

(101)

389

-

-

-

PBT (reported)

442

1,169

1,840

2,163

2,364

Tax

107

447

547

649

709

(% of PBT)

24.3

38.3

29.7

30.0

30.0

PAT (reported)

335

722

1,294

1,514

1,655

Add: Share of earnings of ass.

-

-

-

-

-

Less: Minority interest (MI)

-

-

-

-

-

PAT after MI (reported)

335

722

1,294

1,514

1,655

ADJ. PAT

234

1,111

1,294

1,514

1,655

% chg

(149.1)

375.1

16.4

17.0

9.3

(% of Net Sales)

1.7

5.9

6.5

6.9

6.9

Basic EPS (`)

1.2

2.5

4.5

5.3

5.8

Fully Diluted EPS (`

1.2

2.5

4.5

5.3

5.8

% chg

-

375.1

16.4

17.0

9.3

February 13, 2017

6

Ashok Leyland | 3QFY2017 Result Update

Balance sheet statement (Standalone)

Y/E March (` cr)

FY2014

FY2015

FY2016

2017E

2018E

2019E

SOURCES OF FUNDS

Equity share capital

266

285

285

285

285

285

Reserves & surplus

4,182

4,834

5,230

6,006

6,763

7,590

Shareholders’ Funds

4,448

5,119

5,514

6,290

7,048

7,875

Total loans

Deferred tax liability

4,690

3,350

2,659

2,709

2,759

2,509

Other long term liabilities

70

99

142

137

151

165

Long term provisions

624

611

589

589

589

589

Total Liabilities

9,833

9,178

8,903

9,725

10,546

11,138

APPLICATION OF FUNDS

Gross block

8,672

8,555

8,747

9,178

9,716

10,306

Less: Acc. depreciation

3,012

3,300

3,693

4,152

4,638

5,153

Net Block

5,660

5,256

5,054

5,026

5,078

5,153

Capital work-in-progress

182

120

76

60

40

40

Goodwill

2,790

2,649

1,918

2,000

2,100

2,200

Investments

4,177

5,287

6,338

7,242

8,408

9,314

Long term loans and adv.

1,189

1,399

1,731

2,147

2,478

2,716

Other noncurrent assets

1,299

1,243

1,251

1,342

1,475

1,617

Current assets

12

751

1,568

1,911

2,431

2,762

Cash

643

892

741

764

840

921

Loans & advances

1,035

1,002

1,048

1,078

1,184

1,298

Other

3,193

4,234

4,535

4,656

5,133

5,622

Current liabilities

984

1,053

1,803

2,586

3,274

3,692

Net current assets

217

101

53

53

53

53

Misc. exp. not written off

-

-

-

-

-

-

Total Assets

9,833

9,178

8,903

9,725

10,546

11,138

February 13, 2017

7

Ashok Leyland | 3QFY2017 Result Update

Cash flow statement (Standalone)

Y/E March (` cr)

FY2015

FY2016

2017E

2018E

2019E

Profit before tax

442

1,169

1,840

2,163

2,364

Depreciation

416

444

459

486

515

Change in Working Capital

705

(128)

(410)

(62)

28

Interest / Dividend (Net)

367

229

133

134

134

Direct taxes paid

(50)

(441)

(547)

(649)

(709)

Others

(104)

402

-

-

-

Cash Flow from Operations

1,777

1,676

1,475

2,072

2,332

(Inc.)/ Dec. in Fixed Assets

(211)

(147)

(415)

(518)

(590)

(Inc.)/ Dec. in Investments

314

537

(112)

(207)

(214)

Cash Flow from Investing

103

390

(527)

(725)

(804)

Issue of Equity

667

-

-

-

-

Inc./(Dec.) in loans

(1,401)

(799)

46

64

(236)

Dividend Paid (Incl. Tax)

-

(154)

(518)

(757)

(827)

Interest / Dividend (Net)

(406)

(296)

(133)

(134)

(134)

Cash Flow from Financing

(1,140)

(1,249)

(605)

(828)

(1,197)

Inc./(Dec.) in Cash

740

817

343

520

331

Opening Cash balances

12

751

1,568

1,911

2,431

Closing Cash balances

751

1,568

1,911

2,431

2,762

February 13, 2017

8

Ashok Leyland | 3QFY2017 Result Update

Key ratios

Y/E March

FY2014

FY2015

FY2016

2017E

2018E

2019E

Valuation Ratio (x)

P/E (on FDEPS)

841.7

79.0

36.6

20.4

17.5

16.0

P/CEPS

60.9

35.2

22.7

15.1

13.2

12.4

P/BV

5.9

5.2

4.8

4.2

3.8

3.4

Dividend yield (%)

-

206.6

97.8

51.1

34.9

32.0

EV/Sales

2.9

1.9

1.4

1.3

1.1

1.0

EV/EBITDA

242.5

25.7

11.8

11.1

9.6

8.7

EV / Total Assets

2.2

2.0

1.9

1.8

1.6

1.4

Per Share Data (`)

EPS (Basic)

0.1

1.2

2.5

4.5

5.3

5.8

EPS (fully diluted)

0.1

1.2

2.5

4.5

5.3

5.8

Cash EPS

1.5

2.6

4.1

6.2

7.0

7.5

DPS

0.0

0.5

1.0

1.8

2.7

2.9

Book Value

15.6

18.0

19.4

22.1

24.8

27.7

Returns (%)

ROCE

(2.8)

7.2

21.1

20.2

21.2

21.7

Angel ROIC (Pre-tax)

(4.1)

12.0

36.7

35.7

39.4

41.6

ROE

0.7

6.5

13.1

20.6

21.5

21.0

Turnover ratios (x)

Asset Turnover (Gross Block)

1.1

1.6

2.2

2.2

2.3

2.3

Inventory / Sales (days)

45

38

34

40

42

42

Receivables (days)

49

34

25

25

25

25

Payables (days)

89

78

51

50

50

50

WC cycle (ex-cash) (days)

5

(6)

8

15

17

17

February 13, 2017

9

Ashok Leyland | 3QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Ashok Leyland

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 13, 2017

10