Angel Top Picks - September 2016

Angel Top Picks - September 2016

Top Picks

We have been highlighting over the past few months as to how some pockets of the

Company

CMP (`)

TP (`)

economy are showing signs of relatively higher traction despite the overall economy

Amara Raja

1,018

1,174

recovering only gradually. While investment demand in India has remained

BEL

1,213

1,414

subdued, consumption patterns show a healthy picture.

HCL Tech

787

1,000

Two wheelers & Passenger cars continued to accelerate

: If we go by the latest

Infosys

1,055

1,370

numbers, two-wheeler sales for the month of August 2016 have grown by 25%

Bajaj Electricals

272

306

month on month (YTD 8%), while passenger car sales commensurately reported a

Blue Star

514

578

12% growth (YTD 9%). After two years of drought-like situation, a favourable

Dewan Housing

298

325

monsoon this year has revived tractors sales, which grew by 22% month on month

Equitas Holdings

182

235

during the same period (YTD 19%). Also, Royal Enfield representing the premium

Goodyear India

601

684

bike segment continued to report a strong 32% month on month growth (YTD 35%).

IL&FS Transport.

76

93

White goods & other consumer products saw further pickup in growth: Harsh

Jagran Prakashan

195

225

summers across the country led to a strong increase in 1QFY2017 AC sales for

Mahindra Lifespace

431

522

Voltas (29% yoy) and Bluestar (34% yoy). If we extend the consumption trend and

Navkar Corp.

191

265

look into Appliance (Refrigerators, Washing Machine, ACs, Kitchenware) sales, then

Radico Khaitan

102

125

Whirlpool and IFB reported 16%/20% yoy increase in their 1QFY2017 sales.

Siyaram Silk Mills

1,281

1,469

Further, within the Electric Consumer Durable space, Crompton Greaves

TV Today

300

363

Electrical/V-Guard reported 23%/15% yoy increase in their 1QFY2017 sales. The

Source: Angel Research;

Building Products segment of HSIL has grown 17% yoy in 1QFY2017. Paint

Note: CMP as of Sept. 7, 2016

companies like Asian Paints, Berger, Kansai Nerolac reported 11-12% yoy volume

growth in 1QFY2017. The consumption story can be better ratified by the growing

Two wheelers sales accelerated backed

retail loan books of private sector banks and housing finance companies, which

by good monsoon

have grown by 20%+ and 15%+ yoy in 1QFY2017, respectively.

Service sector was again the start performer in GDP: We sense that a part of this

growth is fuelled by government spending, which should also spur a revival in the

corporate capex cycle. The 1QFY2017 GVA data shows that the economy has

Service sector continues to drive the

grown by 7.3%, with industry growing by 6% and services growing by 9.6%. Better

economic growth

than expected growth in services segment reinforces our view that the growth in the

economy is now being led by consumption.

Retail inflation to see moderation post monsoon: With retail inflation at 6.07% for

July 2016, it seems the RBI may not resort to rate cuts any time soon in the next few

months. CPI inflation above RBI’s comfort zone of 5% is a concern; however a large

art of the rise in inflation has been due to escalating food articles. However, the

p

good news is that food prices are likely to undergo moderation post monsoon. The

Weather Department as of September 02, 2016 has maintained its forecast of a

Expect moderation in retail inflation

above normal monsoon for this year. On the back of good monsoon season, we

expect softening in food prices, going forward. Our view gets substantiated from the

point that area under Kharif pulses cultivation for the year has gone up by 33% to

14.2mn hectares and total acreage under various crops cultivation has gone up by

3.7% to 103.4mn hectares.

We expect the Indian economy to see a relief from rising inflation in the near term,

courtesy good monsoon season. Further, we believe that consumption which is

growing better than rest of the economy can get further boost if the RBI initiates rate

cuts, provided inflation remains under control.

Please refer to important disclosures at the end of this report

1

Top Picks Report | September 2016

Higher disposable income, backed by 7th pay commission: We are of the view that

implementation of the 7th Pay Commission will further boost consumption. The

government is likely to release arrears of the same for Jan-Aug 2016 period and

cash-in-hand could flow in the month of September. Higher disposable income in

the hands of consumers in the festive season would be an icing on the cake.

Green shoots visible for capex cycle

Capex cycle has been delayed, but green shoots visible: The government on the

revival

other hand, has taken the lead initiative to revive capex spending. This can be

seen from high budgetary allocation and higher spending. Some of the key

pockets, where we see increased government thrust, include Roads, Defence, Rural

Electrification and Housing.

To start with, in case of Roads, of the total 25,000kms of awarding guidance for

FY2017, 1,840kms have been awarded during Apr-Jul 2016 (MoRTH-1,070kms

and NHAI-770kms). This is healthy considering that majority of this awarding is

back-ended to the financial year. Currently, bids are being filed for tenders

covering ~4,500kms (valued at over `65,000cr).

The government’s emphasis on the Indian Defence sector has led India to emerge

as the fourth highest spender (vs sixth highest largest last year) as per a recent IHS

report. India is expected to finalise `2.8tn of Defence projects in FY2017, with 40%

of the project being indigenised. Surge in defence spending can be seen from the

fact that one of the largest listed defence players, BEL has reported 53% yoy

growth in its 1QFY2017 order book.

The government has set an ambitious target of electrifying 18,452 un-electrified

villages by May 1, 2018. To-date 10,079 villages have been electrified. Notably,

8,425 of villages were electrified during 15th August, 2015 and 21st August, 2016.

Affordable and mid end housing demand seems picking up: Another push area

Housing data too has been

has been “Housing for All by 2022” scheme, which has led to surge in MIG/LIG

encoraging,which is again supported by

housing. A recent report by Cushman Wakefield substantiates our view that

uptick in cement demand

affordable housing has seen massive surge of close to 100% (double) in new

launches in 1HFY2016 as against the same time last year. Also from volume point

of view, mid-ranged housing (`70lakh-`2cr for Mumbai and Delhi; `50-`1.2cr for

Rest of India) saw the maximum launches of 36,267 units in Top 8 cities, recording

10% yoy increase in 1HFY2016.

Higher government spending has led to increase in cement demand, which

validates our point that revival in Infra spending is gradually picking-up. Cement

volumes of top

18 companies cumulatively reported

8.7% yoy increase to

48.2mntn in 1QFY2017.

In addition to above-mentioned verticals, Railways, Power, Irrigation and Water

Treatment Ministries have taken baby steps to clear the deck for big awarding to

be made going forward. Already some of the state governments have gone ahead

with the awarding of large ticket projects in the Irrigation and Water Treatment

space. We expect broader Infra segment spending to be seen going forward.

September 7, 2016

2

Top Picks Report | September 2016

RBI’s view reinforces our thesis that consumption will continue to be the growth

driver: In its annual report, the RBI reiterated that “while a durable pick up in

investment activity remains elusive, consumption will continue to provide main

support to aggregate demand and may receive boost from revival of rural demand

in response to the above normal monsoon”. In FY2016, India received the highest

ever FDI to the tune of US$35bn, reflecting at it being a preferred investment

destination. This has brought in a lot of stability to the INR.

On the whole, we sense that while investment demand will gradually pick up with

a lag effect, the Indian economy is likely to see improvement on the back of

increasing consumerism.

We have been vocal about consumption and infrastructure based themes playing

out well and the recent favourable developments and cues mentioned above add

to our conviction. We continue to like consumption based companies like Blue Star,

Bajaj Electricals, Siyaram Silk Mills and Radico Khaitan. We have already seen

revival in tractor demand and to play the monsoon theme we believe Goodyear

India is the right candidate as it is among the leaders in terms of market share in

tractor tyres. To play on government’s infrastructure spending and in anticipation

of a lower interest rates regime, we believe ITNL, Mahindra Life Space, Equitas

Holding are good picks.

September 7, 2016

3

Top Picks Report | September 2016

Exhibit 1: Cross section of recent growth trends in various pockets of the economy

Sector

Description

Data/ Growth

Period

Source

Auto sales numbers showed improvement in 5MFY17

Automobile

compared to previous year’s disappointing numbers. 2W

25%

Aug-16

Auto companies

segment has reported ~25% yoy growth in August.

PVs too have reported good growth of 12%

12%

Auto companies

Aug-16

Tractor sales (key players like M&M & Escort) have grown

by ~22% in August partially due to lower base and also

22%

Aug-16

Auto companies

led by favorable monsoon

Smartphone shipments in India rose by 15% in 2QCY2016

Smartphone

15%

Mint

and are expected to increase further

Voltas/ Bluestar reported impressive yoy AC sales growth.

AC sales

Daikin, Panasonic, Blue Star expect Industry to grow 18-

29/34%

1QFY2017

Industry

20% in FY2017E

Real Estate

Affordable Housing Launches surge across Top 8 cities

100%

1HFY2017

Cushman Wakefield

MoRTH has guided awarding target (from 10,000kms in

Roads & High.

150%

FY2016

Pib.nic.in

FY2016 to 25,000kms in FY2017E)

NHAI tendering pipeline stood at ~`65,000cr

19%

Aug-16

NHAI, Angel

New Initiative: Bharatmala Project to lead to strong

17,200kms

FY2016

Pib.nic.in

awarding

Expect finalization of `2.8tn of (Capital) Defence projects in

Defence

Multi-fold growth

CY2016

IHS Inc.

CY2016

New Initiative: 100 Smart Cities to create huge

Urban Infra

~`6 lakh cr

4QFY2016

Pib.nic.in

opportunities

New Initiative: Build 2cr Urban Houses, under the 'Housing

~`11 lakh cr

4QFY2016

Pib.nic.in

for All'

Combined retail loans of the top five pvt banks and three

Retail loan

housing finance companies reported a healthy growth of

19%

1QFY2017

company

growth

19% to `10.7 lac cr vs `9 lac cr in Q1FY16 indicating pick

up in consumption demand.

The organised dairy industry in India is estimated to have

Dairy

grown ~20% in FY2015 and as per industry reports will

20%

FY2015

IMARC

maintain the growth over next 5 years

Domestic passenger traffic has grown at 23% YoY (for the

Directorate General of

Aviation

23%

1HCY2016

first seven months of CY2016).

Civil Aviation

Foreign tourist arrivals increased 17.1% YoY for July 2016,

which improved hotel occupancy rates (6.4%). Further,

Pib.nic.in,

Hotels

6-7%

Jul-16

Revenue per average room increased by 9.6% for the same

STR

period

LED lighting market in India is projected to register a CAGR

LED Lighting

30%

TechSci Research report

of over 30%, during 2016-2021

Source: Company, Angel Research

September 7, 2016

4

Top Picks Report | September 2016

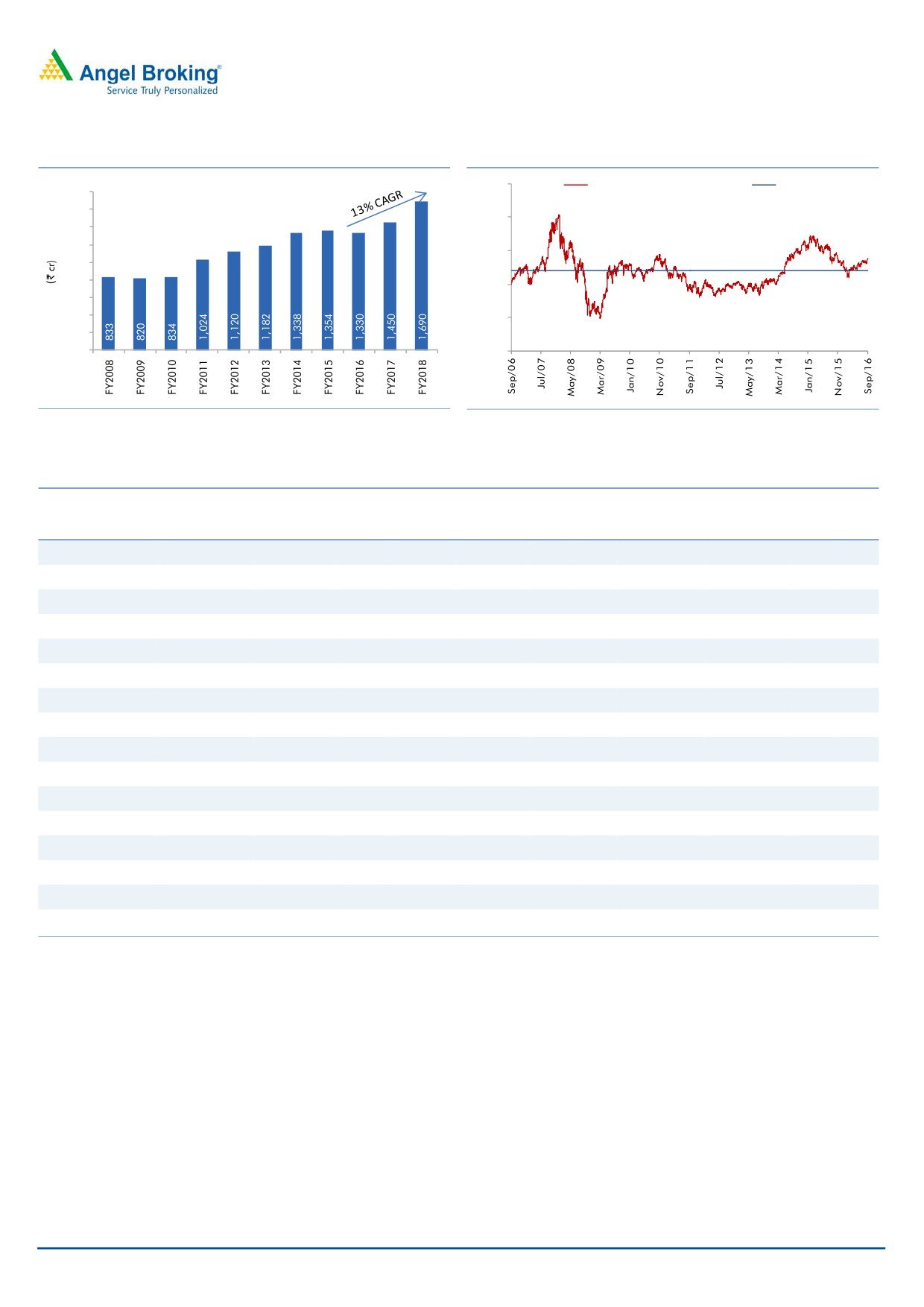

Exhibit 2: Historical Sensex EPS chart

Exhibit 3: One year forward sensex PE Chart

30.0

Sensex 1 year forward P/E

10 year Avg

1800

1600

25.4

25.0

1400

1200

18.7

20.0

1000

800

15.0

600

400

10.0

9.8

200

0

5.0

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 4: Top Picks

EPS

PER

EV/Sales

ROE

Company

Sector

Rating

CMP (`) Target (`) Upside (%) FY17E FY18E FY17E FY18E FY17E FY18E FY17E FY18E

Amara Raja

Auto Ancill.

Buy

1,018

1,174

15.3

35.3

43.5

28.8

23.4

3.1

2.5

25.9

26.0

BEL

Capital Goods

Buy

1,210

1,414

16.9

58.7

62.5

20.6

19.4

2.6

2.3

44.6

46.3

HCL Tech

IT

Buy

787

1,000

27.4

55.7

64.1

14.1

12.3

2.1

1.7

20.3

17.9

Infosys

IT

Buy

1,055

1,370

29.9

64.8

72.0

16.3

14.7

2.9

2.5

22.0

22.3

Bajaj Electricals

Cons. Durable Accumulate

272

306

12.5

11.4

14.6

23.9

18.6

0.5

0.5

13.4

15.1

Blue Star

Cons. Durable Accumulate

514

578

12.5

14.9

22.1

34.2

23.0

1.1

1.0

23.1

24.1

Dewan Housing

Financials

Buy

298

325

9.1

29.7

34.6

10.0

8.6

-

-

16.1

16.8

Equitas Holdings

Financials

Buy

182

235

29.5

5.8

8.2

31.4

22.2

-

-

10.9

11.5

Goodyear India

Tyre

Accumulate

601

684

13.8

49.4

52.6

12.2

11.4

0.5

0.5

18.2

17.0

IL&FS Transport.

Infra

Buy

76

93

22.4

8.1

9.1

9.4

8.3

3.6

3.3

4.2

5.0

Jagran Prakashan

Media

Buy

195

225

15.0

10.8

12.5

18.1

15.6

2.7

2.4

21.7

21.7

Mahindra Lifespace Real Estate

Buy

431

522

21.1

29.9

35.8

14.4

12.1

2.2

1.9

7.6

8.6

Navkar Corp.

Logistics

Buy

191

265

38.7

6.8

11.5

28.2

16.6

7.6

5.1

6.9

10.5

Radico Khaitan

Breweries & Dist.

Buy

102

125

22.0

6.3

7.4

16.1

13.8

1.3

1.2

8.6

9.3

Siyaram Silk Mills

Textile

Buy

1,281

1,469

15.0

104.9 122.4

12.2

10.5

0.9

0.8

16.4

16.4

TV Today

Media

Buy

300

363

21.0

18.4

21.4

16.3

14.0

2.5

2.0

17.4

17.2

Source: Angel Research

September 7, 2016

5

Top Picks Report | September 2016

Top Picks

September 7, 2016

6

Top Picks Report | September 2016

Stock Info

Amara Raja Batteries

CMP

1,018

Amara Raja Batteries Ltd (ARBL) is the second largest lead acid storage battery

TP

1,174

manufacturer in the country. It has been outpacing market leader Exide (ARBL

Upside

15.3%

grew at a 24% CAGR over FY2010-15 as compared to Exide's growth of 13%),

leading to its market share improving from 25% in FY10 to about 35%

Sector

Auto Ancillary

currently. ARBL's outperformance has been mainly on back of its association

Market Cap (` cr)

17,387

with global battery leader Johnson Controls Inc (which also holds 26% stake in

Beta

0.8

ARBL) for manufacturing ducts.

52 Week High / Low

1,077 / 773

With the automotive OEMs following a policy of having multiple vendors and

with ARBL’s products enjoying a strong brand recall in the replacement

segment, the company is well poised to gain further market share. Given the

3 year-Chart

economic recovery and market share gains, the company is expected to grow at

a CAGR of 18% over the next two years as against industry growth of 10-12%.

1200

1000

ARBL is a well diversified auto ancillary player having presence across the

800

automotive and the industrial segment. It has a broad OEM as well as

replacement customer base. We believe ARBL is a high quality stock to play

600

the auto sector revival. We maintain our Buy rating on the stock.

400

200

Key Financials

0

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

5,429

17.5

604

35.3

25.9

28.8

6.6

15.8

3.1

Source: Company, Angel Research

FY2018E

6,471

17.6

742

43.5

26.0

23.4

5.4

13.0

2.5

Source: Company, Angel Research

Stock Info

Bharat Electronics (BEL)

CMP

1,210

High priority to the defense sector in the government’s ‘Make in India’

TP

1,414

campaign, with (1) emphasis on indigenization, (2) increase in FDI limits from

26% to 49%, and (3) over $50bn worth of projects cleared by Defense

Upside

16.9%

Acquisition Council (DAC) in the last 26 months, indicate at the sector being at

Sector

Capital Goods

an inflexion point where Indian defense capex cycle is entering a new era of

Market Cap (` cr)

29,039

growth. The current bid pipeline could lead to strong award activity for the

next few years and BEL could emerge as a beneficiary.

Beta

1.1

BEL in FY2016 had ~35% market share in the defense electronics space.

52 Week High / Low

1,417 / 983

Considering (1) bid-pipeline of Indian Air Force and Navy’s platform projects,

which have high defense electronic component, (2) BEL’s in-house R&D

3 year-Chart

capabilities, and (3) its zero debt status, we believe that BEL would maintain its

1,600

strong market positioning in the defense electronics space.

1,400

We expect BEL to trade at a premium to its historical valuations on account of

1,200

uptick in investment cycle. Current low competitive intensity which should

1,000

enable BEL to justifiably command scarcity premium, coupled with the fact that

800

the company is the largest listed defense player, makes the stock more

600

attractive. We maintain BUY rating on the stock with price target of `1,414.

400

200

Key Financials

0

Y/E

Sales

OPM PAT EPS Adj. ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

8,137

16.8

1,410

58.7

44.6

20.6

3.2

15.7

2.6

Source: Company, Angel Research

FY2018E

9,169

17.2

1,499

62.5

46.3

19.4

2.8

13.7

2.3

Source: Company, Angel Research

September 7, 2016

7

Top Picks Report | September 2016

Stock Info

HCL Technologies

CMP

787

Healthy pipeline: The company’s engineering services has been seeing lumpy

TP

1,000

growth over the last few quarters. This is however largely a function of the

Upside

27%

timing of large transformational deals. 6-8 of the large deals signed a few

Sector

IT

quarters ago will aid the company to continue to post industry leading growth.

We expect HCL Tech to post a USD and INR revenue CAGR of 16.3% and

Market Cap (` cr)

111,012

18.0%, respectively, over FY2016-18E (inclusive of the acquisition of

Beta

0.8

Geometric Software and the Volvo deal).

52 Week High / Low

986 / 707

Robust outlook: For FY2017 revenues are expected to grow between 12.0-

14.0% in CC. Revenue guidance is based on FY2016 (April to March’2016)

3 year-Chart

average exchange rates. The above constant currency guidance translates to

1,100

11.2% to 13.2% growth in US$ terms.

1,000

900

Outlook and Valuations: The stock is attractively valued at the current market

800

price and hence we maintain our Buy with a price target of `1,000.

700

600

Key Financials

500

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

400

June

(`cr)

(%)

(`cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

49,242

20.5

7,862

55.7

20.3

14.1

2.9

7.6

2.1

FY2018E

57,168

20.5

9,037

64.1

17.9

12.3

2.2

5.6

1.7

Source: Company, Angel Research

Source: Company, Angel Research

Stock Info

Infosys

CMP

1,055

Strong revenue guidance for FY17: The Management has guided towards

TP

1,370

higher revenue growth for FY2017, ie of 11.5-13.5% in CC terms and 12.7-

Upside

30%

14.7% in INR terms (exchange rate as on March 31, 2016). For FY2016, the

company posted a 13.3% growth in CC terms V/s a guidance of 12.8-13.2%

Sector

IT

growth (in CC). We expect the company to post ~13.0% USD revenue growth

Market Cap (` cr)

242,328

in FY2017.

Beta

0.8

Aims to be US$20bn company by FY20: The company expects its revenue to

52 Week High / Low

1,278 / 1,009

rise to US$20bn by FY2020, up from US$8.7bn in FY2015, as it focuses on

acquisitions and winning more new technology services, implying a

14%

3 year-Chart

CAGR over the period. Over the near term, we expect Infosys to post a 13.0%

1,400

USD revenue growth in FY2017. Over FY2016-18E, we expect USD and INR

1,300

revenue to grow at a CAGR of 13.0% and 13.0%, respectively.

1,200

1,100

Outlook and Valuations: The stock trades at a valuation of 15.1x FY2018E

1,000

earnings. We recommend Buy on the stock with a price target of `1,370.

900

800

Key Financials

700

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

600

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

69,934

27.5

14,886

64.8

22.2

16.3

3.6

10.8

2.9

Source: Company, Angel Research

FY2018E

79,025

27.5

16,529

72.0

22.3

14.7

3.3

9.3

2.5

Source: Company, Angel Research

September 7, 2016

8

Top Picks Report | September 2016

Stock Info

Bajaj Electricals

CMP

272

The company is among the top 4 players in the consumer durables space

TP

306

across all its product categories (leader in small appliances; number-4 in fans

Upside

12.5%

and lighting). It has a strong distribution reach with 4,000 distributors

Sector

Cons. Durable

reaching out to 400,000 retailers.

Market Cap (` cr)

2,747

In the 3 years preceding FY2016, the company’s E&P segment had been

Beta

0.9

underperforming owing to cost overruns and delays in project executions.

However, the segment has turned around in FY2016 on the profitability front

52 Week High / Low

280 / 155

and delivered a healthy EBIT margin of ~6% for the year. Currently the

segment’s order book stands at `2,480cr.

3 year-Chart

With expectation of timely execution of new projects in the E&P segment and

400

with the Lighting and Consumer Durables segments expected to benefit from

350

an improvement in consumer sentiments going forward, we expect the

300

company’s top-line to grow at a CAGR of ~12% to `5,805cr and bottom-line

250

to grow at a CAGR of 24% to `147cr over FY2016-FY2018E. We recommend

200

a Buy rating on the stock.

150

Key Financials

100

Y/E

Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

5,099

5.6

115

11.4

13.4

23.9

3.2

9.8

0.5

Source: Company, Angel Research

FY2018E

5,805

5.9

147

14.6

15.1

18.6

2.8

8.2

0.5

Source: Company, Angel Research

Stock Info

Blue Star

CMP

514

BSL is one of the largest air-conditioning companies in India. With a mere

TP

578

3% penetration level of ACs vs 25% in China, the overall outlook for the room

Upside

12%

air-conditioner (RAC) market in India is favourable.

Sector

Cons. Durable

BSL’s RAC business has been outgrowing the industry by ~10% points over the

Market Cap (` cr)

4,898

last few quarters, resulting in the company consistently increasing its market

share (~7% in FY2014 to 10.5% at present). This has resulted in the Cooling

Beta

0.6

Products Division (CPD)'s share in overall revenues increasing from~23% in

52 Week High / Low

517 / 306

FY2010 to ~42% in FY2016 (expected to improve to ~47% in FY2018E). With

strong brand equity and higher share in split ACs, we expect the CPD to

3 year-Chart

continue to drive growth.

600

Aided by increasing contribution from the CPD, we expect the overall top-line

500

to post a revenue CAGR of ~15% over FY2016-18E and margins to improve

400

from 5.7% in FY2015 to 7.1% in FY2018E. Moreover, the merger of Blue Star

300

Infotech has infused cash and strengthened the balance sheet. We have an

Accumulate recommendation on the stock.

200

100

Key Financials

0

Y/E

Sales OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

4,283

5.9

142

14.9

23.1

34.2

6.8

20.1

1.1

Source: Company, Angel Research

FY2018E

5,077

7.3

211

22.1

24.1

23.0

5.8

13.6

1.0

Source: Company, Angel Research

September 7, 2016

9

Top Picks Report | September 2016

Stock Info

Dewan Housing

CMP

298

3rd largest private sector housing finance company: We expect DHFL’s AUM to

TP

325

grow at a CAGR of 21% over FY2016-18, as demand for housing in the middle

Upside

9.1%

and low income group picks up, while PAT CAGR is expected to be 22%.

Sector

Financials

Seasoned and granular loan book with stable asset quality: Individual

borrowers account for 72%, while the high yielding loan against property (LAP)

Market Cap (` cr)

8,662

+SME and projects loans account for 19% and 9% of advances respectively. Despite

Beta

1.6

strong loan growth, the GNPAs and NNPAs are likely to be at ~1.17% and 0.82%,

52 Week High / Low

299 / 141

respectively, for FY2017. We don’t expect any major deterioration in the asset

quality going ahead.

3 year-Chart

Lower cost of funds will help maintain NIM: Nearly 70% of the bank

350

borrowings are due for maturity over the next three years and swapping a part

300

of that with non-convertible debentures (NCDs), where it has ~100bp cost

250

benefit, will help DHFL in maintaining its NIM at ~2.9%.

Outlook: We expect the company to post a healthy loan book CAGR of 21%

200

over FY2015-18E, which is likely to translate in an earnings CAGR of 22%,

150

over the same period. The stock currently trades at 1.4x FY2018E ABV. We

100

maintain Buy on the stock, with a target price of `325.

50

-

Key Financials

Y/E

Op. Inc NIM

PAT

EPS

ABV ROA ROE P/E P/ABV

March

(` cr)

(%)

(` cr)

(`)

(`)

(%)

(%)

(x)

(x)

FY2017E

2,225

2.9

866

29.7

184.0

1.1

16.1

10.0

1.6

Source: Company, Angel Research

FY2018E

2,688

2.9

1,084

34.6

215.3

1.2

16.8

8.6

1.4

Source: Company, Angel Research

Equitas Holdings

Stock Info

CMP

182

Early mover advantage in the SFB category: Equitas was one of the ten NBFCs

TP

235

to get the license to start a small finance bank (SFB). As the entire book of

Upside

29.1%

Equitas qualifies for PSL, meeting the 75% PSL target will not be a challenge.

Sizeable and diversified loan book will keep it ahead of other upcoming SFBs.

Sector

Financials

Asset quality and return ratios are likely to remain stable: Equitas will have to

Market Cap (` cr)

6,123

maintain CRR & SLR going ahead; hence yield on total assets is likely to come

Beta

0.9

down. However, as a bank it will be able to raise deposits and hence there will

52 Week High / Low

206 / 134

be reduction in cost of funds. As a result, spreads may not decline much which

in turn will help in maintaining the ROE & ROA which although could undergo

a marginal decline. Also we don’t expect any major deterioration in the asset

3 year-Chart

quality going ahead.

220

210

NIM likely to remain healthy: Equitas will be able to take deposits after it

200

formally starts banking operations leading to ~250bp reduction in cost of

190

funds. Hence we expect the NIM to remain strong at ~11%, going ahead.

180

Outlook: We expect the company to post a strong loan book & earnings

170

160

CAGR of 38% & 37% over FY2016-18E. The stock currently trades at 2.3x

150

FY2018E BV. We maintain Buy on the stock, with a target price of `235.

140

130

120

Key Financials

Y/E

Op. Inc NIM

PAT

EPS

ABV ROA ROE P/E P/ABV

March

(` cr)

(%)

(` cr)

(`)

(`)

(%)

(%)

(x)

(x)

FY2017E

1,076

11.7

224

6.7

68.2

2.8

12.4

31.4

2.7

Source: Company, Angel Research

FY2018E

1,465

11.4

315

9.4

77.6

2.8

12.9

22.2

2.3

Source: Company, Angel Research

September 7, 2016

10

Top Picks Report | September 2016

Stock Info

Goodyear India

CMP

601

Normal monsoon to energize stagnant tractor demand: Goodyear India (GIL)

TP

684

is a leader in the tractor tyre segment in India with tractor tyres accounting for

Upside

14%

~50% of its overall revenues. GIL’s performance on the top-line front has

Sector

Tyres

been under pressure on account of below par monsoon over the past two

years. As tractor sales have strong correlation with monsoons, the normal

Market Cap (` cr)

1,386

monsoon this year should translate into a higher demand for tractor tyres.

Beta

0.6

Strong finances and Balance Sheet: GIL is a debt free-cash rich company with

52 Week High / Low

609 / 443

RoIC estimated at ~84% for FY2018. The company’s cash and equivalents

are `334cr for FY2016, which amount to ~28% of the current market cap.

3 year-Chart

Outlook and valuation: On an adjusted basis (for FY end March), we expect

800

the top-line to post a CAGR of 7.5% over FY2016-18E to `1,704cr mainly on

700

account of rebound in tractor tyre volumes and expect net profit to improve to

600

`121cr in FY2018E. At the current market price, the stock is trading at a PE of

500

10.0x its FY2018E earnings. We have a Buy rating on the stock and assign a

400

target price of `631 based on a target PE of 12.0x for FY2018E.

300

200

100

Key Financials

0

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

1,598

10.4

114

49.4

18.2

12.2

1.8

4.3

0.5

FY2018E

1,704

10.2

121

52.6

17.0

11.4

1.6

3.6

0.5

Source: Company, Angel Research

Source: Company, Angel Research

Stock Info

IL&FS Transportation Networks

CMP

76

ITNL reported commercial operations date (CoD) for JSEL and PSRDCL. Also,

TP

93

completion certificate was issued for BKEL. TRDCL P-III and CNTL are expected

Upside

22.4%

to commence in the next few months. Further, RIDCRO P-III, KSEL, KNEL, and

BAEL are expected to commence operations in next few months. Accordingly,

Sector

Construction

we expect revenue from these projects to increase by ~`4cr/day (unadj. for

Market Cap (` cr)

2,497

stake).

Beta

1.0

Strategic initiatives like stake sale at SPV level, listing of operational BOT

52 Week High / Low

145/64

projects under InvITs, and re-financing of BOT projects should help the

company unlock value. Money raised from these initiatives could be used to

3 year-Chart

lower debt and improve the profitability.

300

With 7+ projects expected to commence in the next 12 months, we expect the

250

debt repayment cycle at SPV level to commence, resulting in the overall consol.

200

D/E levels peaking out at ~4.0x. With concerns over higher D/E levels allayed

to a certain extent, coupled with the attractive valuations of 0.3x FY2017E

150

P/BV multiple that the ITNL stock is trading at, we maintain our Buy on the

100

stock with price target of `93.

50

Key Financials

0

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

8,946

31.0

266

8.1

4.2

9.4

0.3

11.6

3.6

Source: Company, Angel Research

FY2018E

10,017

31.6

299

9.1

5.0

8.3

0.3

10.5

3.3

Source: Company, Angel Research

September 7, 2016

11

Top Picks Report | September 2016

Stock Info

Jagran Prakashan

CMP

195

We expect JPL to register a net sales CAGR of ~12% over FY2016-18E, on

TP

225

back of (a) strong growth in advertising revenue due to improvement in GDP

growth, and (b) improvement in circulation revenue owing to combination of

Upside

15%

increase in cover price and volume growth.

Sector

Media

Further the acquisition of Radio City would also boost the company's revenue

Market Cap (` cr)

6,378

going ahead. Radio City has ~20 stations across 7 states in the country and is

second only to ENIL in all its operating circles, ie Delhi, Mumbai, Bengaluru,

Beta

0.6

Chennai, Ahmedabad, Hyderabad, Pune and Lucknow. The company covers

52 Week High / Low

200/126

~51% (~66mn people) of the total radio population.

Raw material prices have been in a declining trend. Thus, considering lower

3 year-Chart

news print costs, healthy sales, and higher margins in the radio business, we

250

expect an adj. net profit CAGR of ~12% over FY2016-18E to `409cr.

Considering Dainik Jagran's strong presence in the rapidly growing Hindi

200

markets, we expect JPL to benefit from an eventual recovery in the Indian

150

economy. Hence, we maintain an Accumulate rating on the stock with a target

price of `225.

100

Key Financials

50

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

0

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

2,355

28.0

353

10.8

21.7

18.1

3.9

9.2

2.7

FY2018E

2,635

28.0

409

12.5

21.7

15.6

3.4

8.0

2.4

Source: Company, Angel Research

Source: Company, Angel Research

Mahindra Lifespace

Stock Info

CMP

431

Speedy execution & speedier sales: MLF has 13 projects under implementation

TP

522

across cities. MLF has exhibited fast completion of projects (4-4.5 years in

Mumbai, other-wise 3-3.5 years across other cities), compared to others. Sales

Upside

21.1%

cycle in ~65% of projects is faster than execution cycle, contrary to industry

Sector

Real Estate

trends. This fast execution and sales is optimal, as it helps MLF in revenue

recognition, inventory cycle (better than Oberoi, DLF), cash flows and

Market Cap (` cr)

1,770

profitability. This translates in creating a virtuous cycle of continuous fast growth.

Beta

0.4

Strong revenue growth visibility in short-to-long run: MLF as of 4QFY2016 is

52 Week High / Low

559 / 415

pursuing ~4.0mn sq. ft. of sale of the total ~15.0mn sq. ft. of saleable area.

Having sold ~60% of ongoing projects, we expect MLF to launch ~2.8mn

3 year-Chart

sq.ft. of saleable area in rational way during 4QFY2016-2QFY2018E, across

6 cities. Maturity at existing projects, new launches give better revenue visibility

650

for medium-term. Further, MLF is sitting on land bank of 11.0mn sq.ft across

600

4 cities, which allays any concern over long-term revenue growth.

550

With Real Estate Regulatory Bill closer to reality, MLF should be minimally

500

impacted, given their strong parentage and ethically implemented processes.

450

In the longer-term organized, professionally run, well funded players would

400

enjoy strong trust due to their reliable and fast execution strategies. With

350

improvement in company’s fundamentals, strong earnings growth visibility

300

and long-term growth outlook, at current valuations of 1.1x FY2017E P/BV,

MLF looks attractive. We maintain BUY on MLF with target price of `554.

Key Financials

Source: Company, Angel Research

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

1,152

22.7

75

29.9

4.9

14.4

1.1

15.7

2.2

FY2018E

1,300

24.6

138

35.8

8.5

12.1

1.0

10.1

1.9

Source: Company, Angel Research

September 7, 2016

12

Top Picks Report | September 2016

Stock Info

Navkar

CMP

191

NCL is one of the largest and one of the three CFS at JNPT with rail

TP

265

connectivity, helping it garner high market share at the port. NCL is in a massive

Upside

39%

expansion mode where it is increasing its capacity by 234% to 1,036,889 TEUs

at JNPT and coming up with an ICD at Vapi (with Logistics Park).

Sector

Logistics

Market Cap (` cr)

2,721

The ICD with rail link should benefit from first mover advantage in a region

that has huge market potential and accounts for ~27% of volumes at JNPT.

Beta

0.6

The ICD should be able to capture the EXIM volumes from the region through

52 Week High / Low

224 / 151

rail link that till now was being custom cleared at JNPT (Import) or being

transported via road and consolidated at JNPT (Export). South Gujarat

3 year-Chart

volumes will now head straight to the Vapi ICD; thus the company can now

240

cater to bulk commodities and domestic traffic that it had been rejecting owing

220

to capacity constraints at CFS.

200

We expect NCL to successfully use its rail advantage and scale up its

utilizations at both JNPT and Vapi ICD. We have a Buy rating on the stock.

180

160

Key Financials

140

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

120

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

408

42.9

97

6.8

6.9

28.2

2.0

18.8

7.6

FY2018E

612

42.3

164

11.5

10.5

16.6

1.8

12.7

5.1

Source: Company, Angel Research

Source: Company, Angel Research

Stock Info

Radico Khaitan

CMP

102

The IMFL segment is under penetrated. Going forward, increase in income

TP

125

levels would lead to higher growth in IMFL brands. RKL has strong brands in

Upside

22%

the premium liquor category which reported a CAGR of ~26% over the last

seven-year period. We expect the growth momentum to continue.

Sector

Breweries & Distilleries

Market Cap (` cr)

1,355

We expect the price of ENA, a key raw material, to remain stable and

potentially even decline going forward due to higher sugar production and

Beta

0.8

lower demand for ethanol from Indian oil marketing companies

52 Week High / Low

131/82

We expect a significant hike in liquor prices in the coming financial year as

there haven't been any significant ones in recent times. Also, we believe that

3 year-Chart

industry leader - United Spirits would shift focus on profitability over volume

180

growth considering the debt on its balance sheet, which in turn, would lead to

160

increased scope for other liquor companies to hike prices.

140

On valuation basis, Radico is trading at huge discount to its close peer United

120

Spirits. We have a Buy rating on the stock and target price of

`125

100

(18x FY2018E EPS)

80

Key Financials

60

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

1,659

13.0

84

6.3

8.6

16.1

1.4

8.9

1.3

Source: Company, Angel Research

FY2018E

1,802

13.2

98

7.4

9.3

13.8

1.3

8.0

1.2

Source: Company, Angel Research

September 7, 2016

13

Top Picks Report | September 2016

Siyaram Silk Mills

Stock Info

CMP

1,281

SSML has strong brands which cater to premium as well as popular mass

TP

1,469

segments of the market. Further, in FY2014, SSML entered the ladies' salwar

Upside

15.0%

kameez and ethnic wear segment. Going forward, we believe that the company

would be able to leverage its brand equity and continue to post strong performance.

Sector

Textile

Market Cap (` cr)

1,201

The company has a nationwide network of about 1,600 dealers and business

partners. It has a retail network of 160 stores and plans to add another

Beta

0.8

300-350 stores going forward. Further, the company's brands are sold across

52 Week High / Low

1,353/896

3,00,000 multi brand outlets in the country.

Going forward, we expect SSML to report a net sales CAGR of ~12% to

3 year-Chart

~`2,040cr and adj.net profit CAGR of ~14% to `115cr over FY2016-18E on

1,600

back of market leadership in blended fabrics, strong brand building, wide

1,400

distribution channel, strong presence in tier II and tier III cities and emphasis

1,200

on latest designs and affordable pricing points. At the current market price,

1,000

SSML trades at an inexpensive valuation. We have a Buy rating on the stock

800

600

and target price of `1,469.

400

200

Key Financials

0

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

1,799

11.6

98

104.9

16.4

12.2

2.0

6.4

0.9

Source: Company, Angel Research

FY2018E

2,040

11.7

115

122.4

16.4

10.5

1.7

5.5

0.8

Source: Company, Angel Research

TV Today Network

Stock Info

CMP

300

TTNL enjoys a strong viewership ranking in the Hindi and English news

TP

363

channel categories. The company’s Hindi news channel - Aaj Tak has

maintained its market leadership position occupying the No.1 rank for several

Upside

21%

consecutive years in terms of viewership. Its English news channel - India

Sector

Textile

Today too has been continuously gaining viewership; it has now captured the

Market Cap (` cr)

1,790

No. 2 ranking from No. 4 earlier. Its other channels like Dilli Aaj Tak and Tez

Beta

1.3

are also popular among viewers.

52 Week High / Low

351 /205

Out of the 7 radio stations, TTNL has sold off 4 (Jodhpur, Amritsar, Patiala

and Shimla) for `4cr. The remaining 3 stations are in the process of getting

3 year-Chart

sold off to ENIL but the sale will have to wait until concerns raised by the MIB

400

are resolved. Going forward, we expect them to be sold off and this would

350

prop up the company’s profitability.

300

We expect TTNL to report a net revenue CAGR of ~16% to ~`743cr and net

250

profit CAGR of ~16% to `128cr over FY2016-18E. We have a Buy rating on

200

the stock and target price of `363.

150

100

50

Key Financials

0

Y/E

Sales

OPM PAT EPS ROE P/E P/BV EV/EBITDA EV/Sales

March

(` cr)

(%)

(` cr)

(`)

(%)

(x)

(x)

(x)

(x)

FY2017E

637

27.5

110

18.4

17.4

16.3

2.8

8.7

2.5

Source: Company, Angel Research

FY2018E

743

27.5

128

21.4

17.2

14.0

2.4

7.1

2.0

Source: Company, Angel Research

September 7, 2016

14

Top Picks Report | September 2016

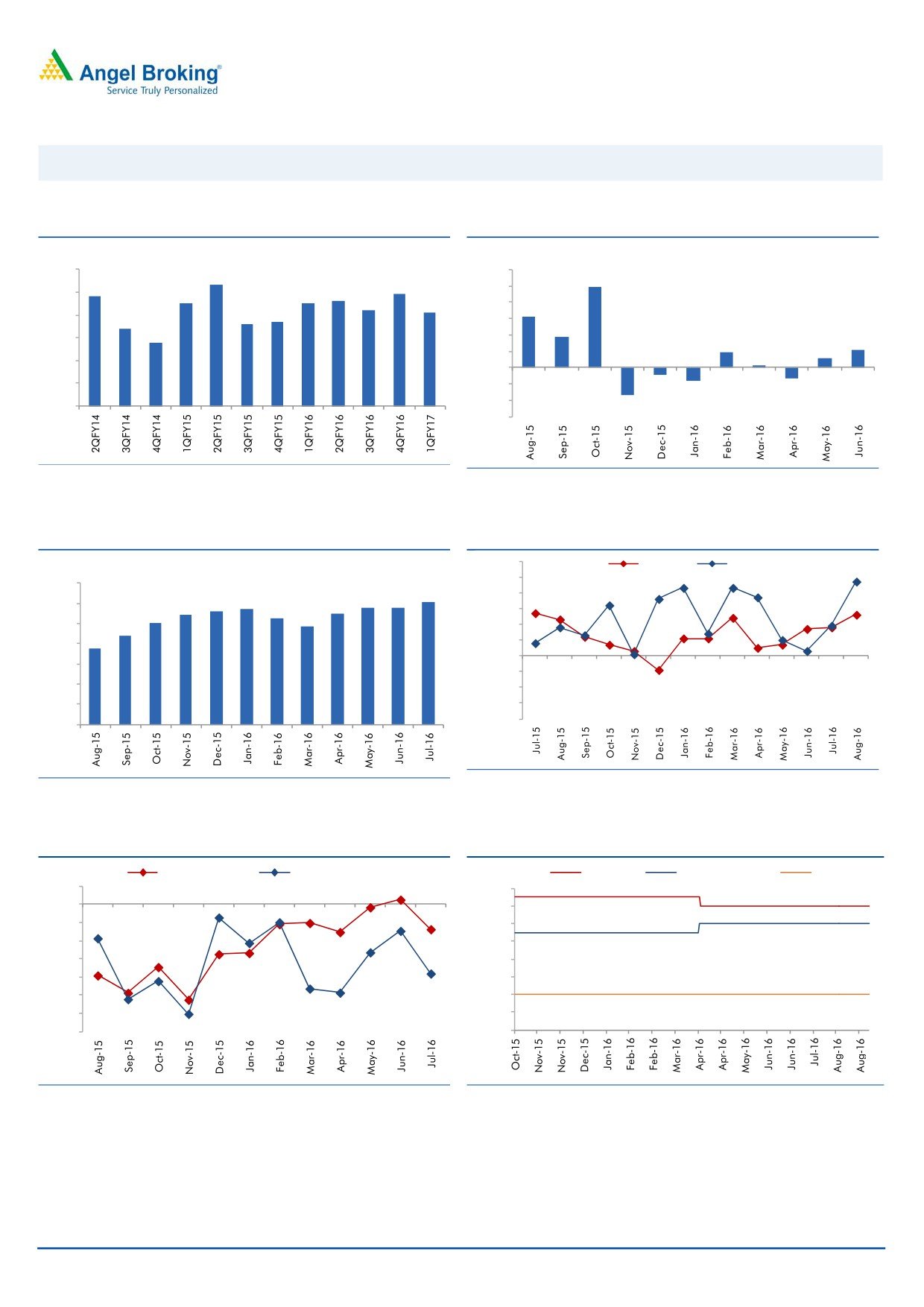

Macro watch

Exhibit 1: Quarterly GDP trends

Exhibit 2: IIP trends

(%)

(%)

9.0

8.3

12.0

9.9

7.8

7.9

10.0

8.0

7.5

7.5

7.6

7.2

7.1

8.0

6.3

6.6

6.7

7.0

6.4

6.0

3.7

5.8

6.0

4.0

1.9

2.1

1.1

2.0

0.3

5.0

-

4.0

(2.0)

(0.9)

(1.3)

(1.6)

(4.0)

3.0

(3.4)

(6.0)

Source: CSO, Angel Research

Source: MOSPI, Angel Research

Exhibit 3: Monthly CPI inflation trends

Exhibit 4: Manufacturing and services PMI

56.0

Mfg. PMI

Services PMI

(%)

55.0

7.0

6.1

5.7

5.8

5.8

54.0

5.6

5.5

6.0

5.4

5.3

5.0

53.0

4.8

5.0

4.4

52.0

3.7

51.0

4.0

50.0

3.0

49.0

2.0

48.0

1.0

47.0

46.0

-

Source: Market, Angel Research; Note: Level above 50 indicates expansion

Source: MOSPI, Angel Research

Exhibit 5: Exports and imports growth trends

Exhibit 6: Key policy rates

(%)

Exports yoy growth

Imports yoy growth

(%)

Repo rate

Reverse Repo rate

CRR

5.0

7.00

0.0

6.50

(5.0)

6.00

(10.0)

5.50

(15.0)

5.00

(20.0)

4.50

(25.0)

4.00

(30.0)

3.50

(35.0)

3.00

Source: Bloomberg, Angel Research

Source: RBI, Angel Research

September 7, 2016

15

Top Picks Report | September 2016

Global watch

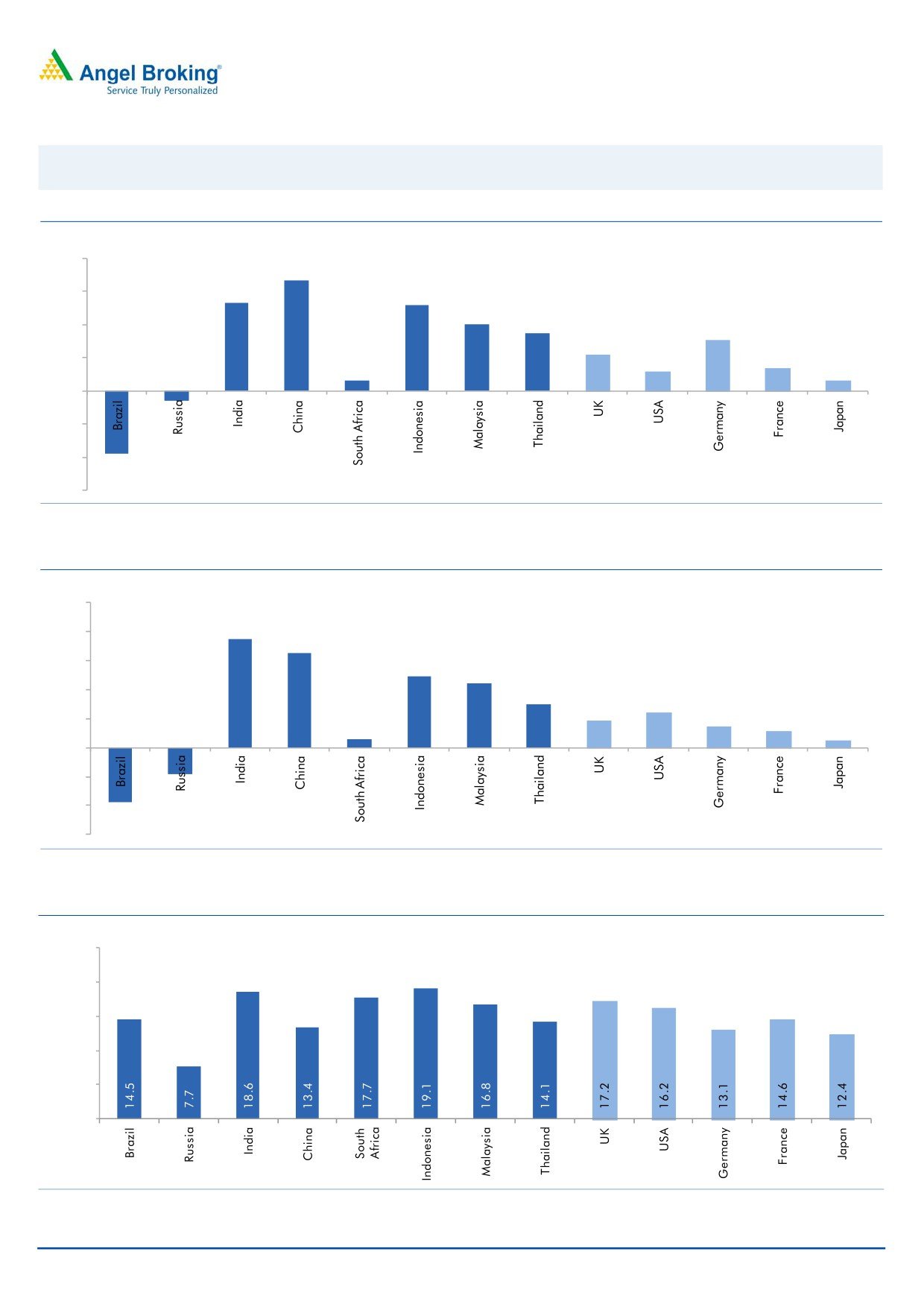

Exhibit 7: Latest quarterly GDP Growth (%, yoy) across select developing and developed countries

(%)

8.0

6.7

6.0

5.3

0.6

5.2

4.0

3.5

4.0

3.1

2.2

2.0

1.2

1.4

0.6

-

(2.0)

(0.6)

(4.0)

(3.8)

(6.0)

Source: Bloomberg, Angel Research

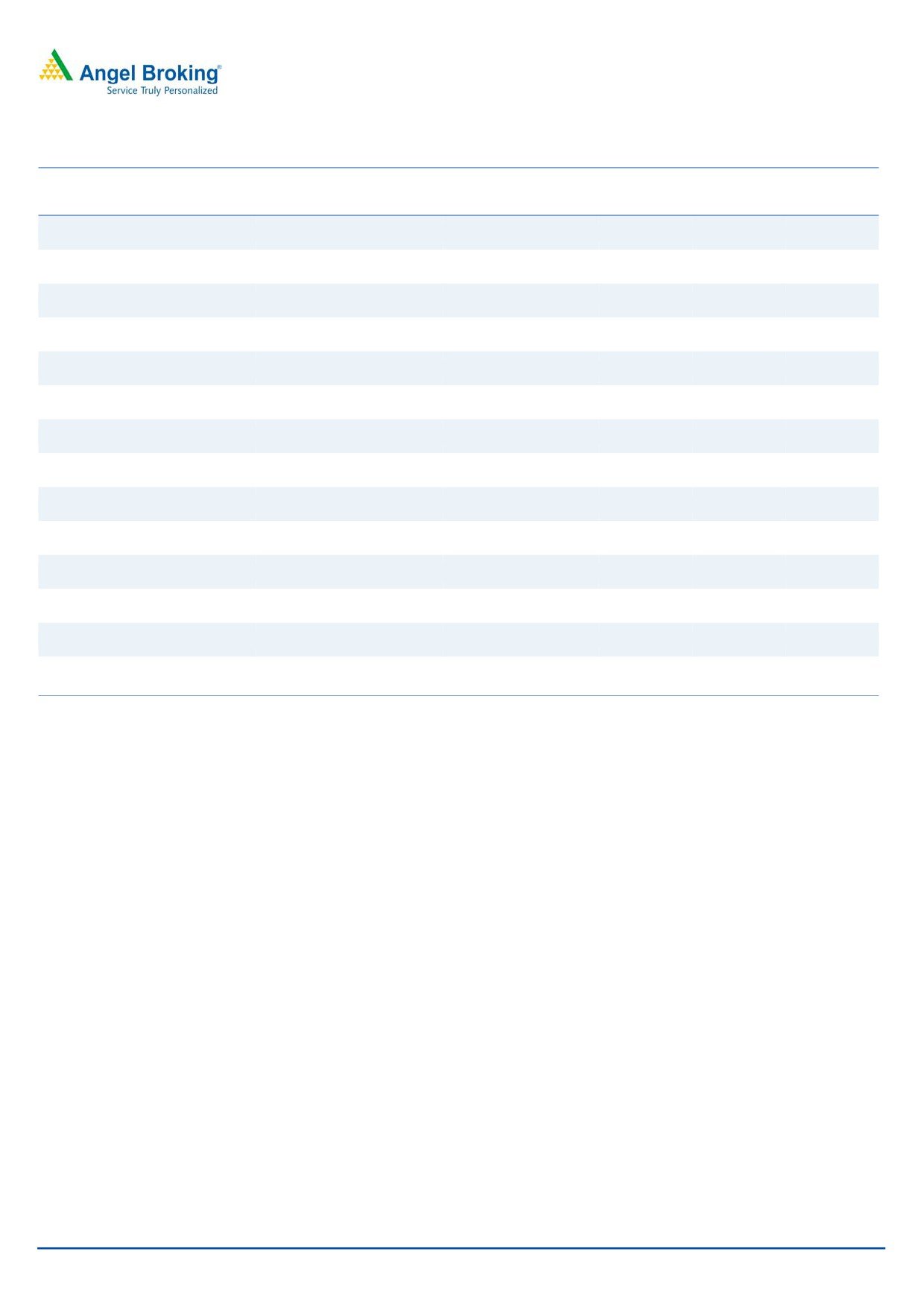

Exhibit 8: 2016 GDP Growth projection by IMF (%, yoy) across select developing and developed countries

(%)

10.0

7.5

8.0

6.5

6.0

4.9

4.4

4.0

3.0

2.4

1.9

1.5

2.0

1.1

0.6

0.5

(3.8)

(1.8)

-

(2.0)

(4.0)

(6.0)

Source: IMF, Angel Research

Exhibit 9: One year forward P-E ratio across select developing and developed countries

(x)

25.0

20.0

15.0

10.0

5.0

-

Source: IMF, Angel Research

September 7, 2016

16

Top Picks Report | September 2016

Exhibit 10: Relative performance of indices across globe

Returns (%)

Country

Name of index

Closing price

1M

3M

1YR

Brazil

Bovespa

60,129

4.3

16.5

32.2

Russia

Micex

2,040

4.9

5.2

20.7

India

Nifty

8,943

4.3

8.7

11.4

China

Shanghai Composite

3,091

2.9

5.3

(4.3)

South Africa

Top 40

47,008

3.0

(2.2)

7.3

Mexico

Mexbol

47,627

0.9

2.9

10.5

Indonesia

LQ45

926

(0.5)

11.9

22.9

Malaysia

KLCI

1,690

2.1

3.6

5.5

Thailand

SET 50

950

(2.0)

2.9

6.4

USA

Dow Jones

18,538

1.0

3.4

12.4

UK

FTSE

6,826

1.3

8.6

9.6

Japan

Nikkei

17,082

5.1

3.0

(7.0)

Germany

DAX

10,687

2.8

6.3

5.9

France

CAC

4,530

2.9

3.2

(2.2)

Source: Bloomberg, Angel Research

September 7, 2016

17

Top Picks Report | September 2016

Stock Watch

September 7, 2016

18

Stock Watch | September 2016

Company Name

Reco

CMP

Target

Mkt Cap

Sales (` cr)

OPM (%)

EPS (`)

PER (x)

P/BV (x)

RoE (%)

EV/Sales (x)

(`)

Price (`)

(` cr)

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

Agri / Agri Chemical

Rallis

Neutral

224

-

4,363

1,937

2,164

13.3

14.3

9.0

11.0

24.9

20.4

4.3

3.8

18.4

19.8

2.3

2.0

United Phosphorus

Accumulate

660

684

28,301

15,176

17,604

18.5

18.5

37.4

44.6

17.7

14.8

3.5

2.9

21.4

21.2

1.9

1.6

Auto & Auto Ancillary

Ashok Leyland

Buy

89

111

25,186

22,407

26,022

10.6

10.6

5.2

6.4

17.0

13.8

3.8

3.2

23.6

24.7

1.2

1.0

Bajaj Auto

Neutral

2,986

-

86,401

25,093

27,891

19.5

19.2

143.9

162.5

20.7

18.4

5.8

5.0

30.3

29.3

3.2

2.8

Bharat Forge

Neutral

885

-

20,591

7,726

8,713

20.5

21.2

35.3

42.7

25.1

20.7

4.6

4.2

18.9

20.1

2.7

2.3

Eicher Motors

Neutral

22,973

-

62,397

16,583

20,447

17.5

18.0

598.0

745.2

38.4

30.8

13.1

10.0

41.2

38.3

3.6

2.8

Gabriel India

Neutral

116

-

1,666

1,544

1,715

9.0

9.3

5.4

6.3

21.5

18.4

4.1

3.6

18.9

19.5

1.0

0.9

Hero Motocorp

Neutral

3,610

-

72,084

31,253

35,198

15.3

15.0

172.3

192.1

21.0

18.8

7.7

6.6

38.9

37.0

2.2

1.9

Jamna Auto Industries Neutral

216

-

1,726

1,486

1,620

9.8

9.9

15.0

17.2

14.4

12.6

3.2

2.7

21.8

21.3

1.2

1.1

L G Balakrishnan & Bros Neutral

557

-

875

1,302

1,432

11.6

11.9

43.7

53.0

12.8

10.5

1.8

1.6

13.8

14.2

0.7

0.6

Mahindra and Mahindra Neutral

1,489

-

92,462

46,534

53,077

11.6

11.7

67.3

78.1

22.1

19.1

3.6

3.1

15.4

15.8

2.0

1.7

Maruti

Neutral

5,338

-

161,250

69,186

82,217

14.7

14.4

198.5

241.4

26.9

22.1

5.2

4.2

20.2

19.9

2.0

1.6

Minda Industries

Neutral

1,580

-

2,506

2,728

3,042

9.0

9.1

68.2

86.2

23.2

18.3

5.3

4.2

23.8

24.3

0.9

0.8

Motherson Sumi

Neutral

336

-

44,490

45,896

53,687

7.8

8.2

13.0

16.1

25.8

20.9

8.3

6.6

34.7

35.4

1.0

0.8

Rane Brake Lining

Neutral

1,045

-

827

511

562

11.3

11.5

28.1

30.9

37.2

33.8

5.7

5.2

15.3

15.0

1.6

1.5

Setco Automotive

Neutral

44

-

584

741

837

13.0

13.0

15.2

17.0

2.9

2.6

0.5

0.4

15.8

16.3

1.2

1.1

Tata Motors

Neutral

588

-

169,681

300,209

338,549

8.9

8.4

42.7

54.2

13.8

10.8

2.2

1.9

15.6

17.2

0.7

0.6

TVS Motor

Neutral

330

-

15,697

13,390

15,948

6.9

7.1

12.8

16.5

25.9

20.0

6.4

5.1

26.3

27.2

1.2

1.0

Amara Raja Batteries

Accumulate

1,018

1,174

17,387

5,429

6,471

17.5

17.6

35.3

43.5

28.8

23.4

6.6

5.4

25.3

24.8

3.1

2.5

Exide Industries

Neutral

191

-

16,214

7,439

8,307

15.0

15.0

8.1

9.3

23.5

20.5

3.3

2.9

14.3

16.7

1.8

1.6

Apollo Tyres

Neutral

206

-

10,488

12,877

14,504

14.3

13.9

21.4

23.0

9.6

9.0

1.5

1.3

16.4

15.2

1.0

0.9

Ceat

Buy

1,017

1,119

4,113

7,524

8,624

13.0

12.7

131.1

144.3

7.8

7.0

1.4

1.2

19.8

18.6

0.6

0.5

JK Tyres

Neutral

145

-

3,290

7,455

8,056

15.0

15.0

21.8

24.5

6.7

5.9

1.4

1.1

22.8

21.3

0.6

0.5

Swaraj Engines

Neutral

1,208

-

1,500

660

810

15.2

16.4

54.5

72.8

22.2

16.6

6.9

6.3

31.5

39.2

2.0

1.6

Subros

Neutral

127

-

760

1,488

1,681

11.7

11.9

6.4

7.2

19.8

17.7

2.1

1.9

10.8

11.4

0.7

0.6

Indag Rubber

Neutral

186

-

489

286

326

19.8

16.8

11.7

13.3

15.9

14.0

2.7

2.5

17.8

17.1

1.4

1.2

Banking

Axis Bank

Neutral

625

-

149,172

58,081

66,459

3.5

3.5

32.3

44.6

19.3

14.0

2.5

2.21

13.6

16.5

-

-

Bank of Baroda

Neutral

175

-

40,277

19,980

23,178

1.8

1.8

11.5

17.3

15.2

10.1

1.7

1.4

8.3

10.1

-

-

Canara Bank

Neutral

307

-

16,645

15,225

16,836

1.8

1.8

14.5

28.0

21.1

10.9

1.5

1.2

5.8

8.5

-

-

Dewan Housing Finance Neutral

297

-

8,663

2,225

2,688

2.9

2.9

29.7

34.6

10.0

8.6

1.6

1.4

16.1

16.8

-

-

Equitas Holdings

Buy

182

235

6,090

939

1,281

11.7

11.5

5.8

8.2

31.3

22.1

2.7

2.4

10.9

11.5

-

-

Federal Bank

Neutral

74

-

12,792

9,353

10,623

2.9

2.9

4.4

5.8

16.9

12.8

1.6

1.4

9.5

11.0

-

-

HDFC

Neutral

1,428

-

225,714

11,475

13,450

3.4

3.4

45.3

52.5

31.5

27.2

6.1

5.4

20.2

20.5

-

-

HDFC Bank

Neutral

1,288

-

326,025

46,097

55,433

4.5

4.5

58.4

68.0

22.1

18.9

3.9

3.23

18.8

18.6

-

-

ICICI Bank

Neutral

278

-

161,798

39,029

45,903

3.3

3.3

16.7

16.3

16.7

17.1

2.1

1.9

10.1

12.4

-

-

LIC Housing Finance

Neutral

588

-

29,692

3,712

4,293

2.6

2.5

39.0

46.0

15.1

12.8

2.8

2.4

19.9

20.1

-

-

September 7, 2016

19

Stock Watch | September 2016

Company Name

Reco

CMP

Target

Mkt Cap

Sales (` cr)

OPM (%)

EPS (`)

PER (x)

P/BV (x)

RoE (%)

EV/Sales (x)

(`)

Price (`)

(` cr)

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

Punjab Natl.Bank

Neutral

139

-

27,343

23,532

23,595

2.3

2.4

6.8

12.6

20.5

11.1

3.2

2.2

3.3

6.5

-

-

South Ind.Bank

Neutral

24

-

3,288

6,435

7,578

2.5

2.5

2.7

3.1

9.0

7.9

1.2

1.0

10.1

11.2

-

-

St Bk of India

Neutral

267

-

206,917

88,650

98,335

2.6

2.6

13.5

18.8

19.7

14.2

1.9

1.6

7.0

8.5

-

-

Union Bank

Neutral

151

-

10,391

13,450

14,925

2.3

2.3

25.5

34.5

5.9

4.4

0.9

0.7

7.5

10.2

-

-

Yes Bank

Neutral

1,405

-

59,167

8,978

11,281

3.3

3.4

74.0

90.0

19.0

15.6

3.6

3.1

17.0

17.2

-

-

Capital Goods

ACE

Neutral

45

-

443

709

814

4.1

4.6

1.4

2.1

32.0

21.3

1.3

1.2

4.4

6.0

0.8

0.7

BEML

Accumulate

1,082

1,157

4,508

3,451

4,055

6.3

9.2

31.4

57.9

34.5

18.7

2.1

1.9

6.3

10.9

1.4

1.2

Bharat Electronics

Buy

1,210

1,414

29,039

8,137

9,169

16.8

17.2

58.7

62.5

20.6

19.4

3.2

2.8

44.6

46.3

2.6

2.3

Voltas

Neutral

391

-

12,933

6,511

7,514

7.9

8.7

12.9

16.3

30.3

24.0

5.5

4.8

16.7

18.5

1.7

1.5

BGR Energy

Neutral

119

-

859

16,567

33,848

6.0

5.6

7.8

5.9

15.3

20.2

0.9

0.8

4.7

4.2

0.1

0.1

BHEL

Neutral

160

-

39,113

28,797

34,742

-

2.8

2.3

6.9

69.5

23.2

1.2

1.1

1.3

4.8

0.8

0.6

Blue Star

Accumulate

514

578

4,898

4,283

5,077

5.9

7.3

14.9

22.1

34.2

23.0

16.8

15.8

23.1

24.1

1.1

1.0

Crompton Greaves

Neutral

84

-

5,236

5,777

6,120

5.9

7.0

3.3

4.5

25.3

18.6

1.1

1.1

4.4

5.9

0.8

0.7

Greaves Cotton

Neutral

135

-

3,292

1,755

1,881

16.8

16.9

7.8

8.5

17.3

15.9

3.5

3.2

20.6

20.9

1.6

1.4

Inox Wind

Buy

180

286

3,995

5,605

6,267

15.7

16.4

24.8

30.0

7.3

6.0

2.0

1.5

25.9

24.4

0.8

0.6

KEC International

Neutral

133

-

3,430

9,294

10,186

7.9

8.1

9.9

11.9

13.5

11.2

2.0

1.7

15.6

16.3

0.6

0.5

Thermax

Neutral

844

-

10,053

5,421

5,940

7.3

7.3

25.7

30.2

32.8

27.9

4.0

3.6

12.2

13.1

1.7

1.6

VATech Wabag

Buy

573

681

3,121

3,136

3,845

8.9

9.1

26.0

35.9

22.0

16.0

2.8

2.3

13.4

15.9

0.9

0.7

Cement

ACC

Neutral

1,692

-

31,775

11,225

13,172

13.2

16.9

44.5

75.5

38.0

22.4

3.6

3.3

11.2

14.2

2.8

2.4

Ambuja Cements

Neutral

274

-

54,397

9,350

10,979

18.2

22.5

5.8

9.5

47.2

28.8

4.0

3.6

10.2

12.5

5.9

5.0

India Cements

Neutral

154

-

4,732

4,364

4,997

18.5

19.2

7.9

11.3

19.5

13.6

1.4

1.4

8.0

8.5

1.9

1.6

JK Cement

Neutral

802

-

5,605

4,398

5,173

15.5

17.5

31.2

55.5

25.7

14.4

3.1

2.7

12.0

15.5

1.8

1.5

J K Lakshmi Cement

Neutral

468

-

5,506

2,913

3,412

14.5

19.5

7.5

22.5

62.4

20.8

3.8

3.2

12.5

18.0

2.4

2.0

Orient Cement

Neutral

194

-

3,971

2,114

2,558

18.5

20.5

8.1

11.3

23.9

17.2

3.5

3.0

9.0

14.0

2.6

2.0

UltraTech Cement

Neutral

4,089

-

112,208

25,768

30,385

21.0

23.5

111.0

160.0

36.8

25.6

4.7

4.1

13.5

15.8

4.4

3.7

Construction

ITNL

Buy

76

93

2,497

8,946

10,017

31.0

31.6

8.1

9.1

9.4

8.3

0.3

0.3

4.2

5.0

3.6

3.3

KNR Constructions

Accumulate

712

802

2,003

1,385

1,673

14.7

14.0

41.2

48.5

17.3

14.7

3.2

2.8

14.9

15.2

1.5

1.2

Larsen & Toubro

Accumulate

1,519

1,700

141,591

67,665

77,249

10.7

11.5

57.3

71.2

26.5

21.3

2.4

2.3

12.6

14.3

2.3

2.0

Gujarat Pipavav Port

Neutral

184

-

8,876

705

788

52.2

51.7

5.0

5.6

36.7

32.8

3.6

3.2

11.2

11.2

12.4

10.6

Nagarjuna Const.

Neutral

87

-

4,856

8,842

9,775

9.1

8.8

5.3

6.4

16.5

13.6

1.3

1.2

8.2

9.1

0.7

0.6

PNC Infratech

Accumulate

122

129

3,140

2,350

2,904

13.4

13.7

48.0

42.0

2.6

2.9

0.5

0.4

16.8

13.2

1.4

1.2

Simplex Infra

Neutral

353

-

1,745

6,829

7,954

10.5

10.5

31.4

37.4

11.2

9.4

1.2

1.1

9.9

13.4

0.7

0.6

Power Mech Projects

Neutral

472

-

695

1,801

2,219

12.7

14.6

72.1

113.9

6.6

4.1

1.2

1.0

16.8

11.9

0.4

0.3

Sadbhav Engineering

Neutral

298

-

5,117

3,598

4,140

10.3

10.6

9.0

11.9

33.1

25.1

3.5

3.0

9.9

11.9

1.7

1.4

NBCC

Neutral

252

-

15,117

7,428

9,549

7.9

8.6

8.2

11.0

30.7

22.9

1.5

1.2

28.2

28.7

1.7

1.3

MEP Infra

Neutral

43

-

700

1,877

1,943

30.6

29.8

3.0

4.2

14.4

10.3

6.9

4.7

0.6

0.6

1.8

1.6

September 7, 2016

20

Stock Watch | September 2016

Company Name

Reco

CMP

Target

Mkt Cap

Sales (` cr)

OPM (%)

EPS (`)

PER (x)

P/BV (x)

RoE (%)

EV/Sales (x)

(`)

Price (`)

(` cr)

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

FY17E

FY18E

SIPL

Neutral

104

-

3,665

1,036

1,252

65.5

66.2

(8.4)

(5.6)

-

-

3.9

4.4

(22.8)

(15.9)

11.8

9.8

Engineers India

Neutral

268

-

9,020

1,725

1,935

16.0

19.1

11.4

13.9

23.5

19.3

3.2

3.1

13.4

15.3

4.2

3.7

FMCG

Asian Paints

Neutral

1,178

-

112,965

17,128

18,978

16.8

16.4

19.1

20.7

61.7

56.9

21.5

20.2

34.8

35.5

6.6

6.0

Britannia

Neutral

3,489

-

41,860

9,795

11,040

14.6

14.9

80.3

94.0

43.4

37.1

17.9

13.8

41.2

-

4.1

3.6

Colgate

Neutral

990

-

26,933

4,605

5,149

23.4

23.4

23.8

26.9

41.6

36.8

23.0

18.0

64.8

66.8

5.7

5.1

Dabur India

Neutral

297

-

52,255

8,315

9,405

19.8

20.7

8.1

9.2

36.7

32.3

10.2

8.5

31.6

31.0

6.0

5.3

GlaxoSmith Con*

Neutral

6,226

-

26,182

4,350

4,823

21.2

21.4

179.2

196.5

34.7

31.7

9.2

7.8

27.1

26.8

5.4

4.8

Godrej Consumer

Neutral

1,670

-

56,859

10,235

11,428

18.4

18.6

41.1

44.2

40.6

37.8

9.0

7.6

24.9

24.8

5.5

4.8

HUL

Neutral

932

-

201,643

35,252

38,495

17.6

17.4

20.4

21.9

45.6

42.5

37.5

32.9

82.2

77.3

5.6

5.1

ITC

Accumulate

262

283

315,893

40,059

44,439

39.0

39.2

9.1

10.1

28.8

25.9

7.8

6.9

27.2

26.5

7.4

6.6

Marico

Neutral

297

-

38,350

6,430

7,349

18.8

19.5

6.4

7.7

46.4

38.6

14.0

11.8

33.2

32.5

5.8

5.0

Nestle*

Neutral

6,479

-

62,467

10,073

11,807

20.7

21.5

124.8

154.2

51.9

42.0

21.3

19.2

34.8

36.7

6.1

5.2

Tata Global

Neutral

142

-

8,975

8,675

9,088

9.8

9.8

7.4

8.2

19.2

17.3

2.2

2.1

7.9

8.1

0.9

0.9

Procter & Gamble

Accumulate

6,601

7,369

21,427

2,939

3,342

23.2

23.0

146.2

163.7

45.1

40.3

101.1

96.9

25.3

23.5

6.8

5.9

IT

HCL Tech^

Buy

787

1,000

111,012

49,242

57,168

20.5

20.5

55.7

64.1

14.1

12.3

2.9

2.2

20.3

17.9

2.1

1.7

Infosys

Buy

1,055

1,370

242,328

69,934

79,025

27.5

27.5

64.8

72.0

16.3

14.7

3.6

3.3

22.0

22.3

2.9

2.5

TCS

Buy

2,447

3,004

482,164

121,684

136,286

27.3

27.3

135.0

150.1

18.1

16.3

6.0

5.5

33.2

33.9

3.8

3.3

Tech Mahindra

Buy

471

700

45,744

30,347

33,685

17.0

17.0

37.5

41.3

12.6

11.4

2.7

2.4

21.8

20.7

1.3

1.1

Wipro

Buy

482

680

117,198

51,631

55,822

21.7

17.9

35.9

36.9

13.4

13.1

2.8

2.6

19.0

18.1

2.0

1.7

Media

D B Corp

Neutral

412

-

7,565

2,297

2,590

27.4

28.2

21.0

23.4

19.6

17.6

4.6

4.0

23.7

23.1

3.1

2.7

HT Media

Neutral

86

-

2,007

2,693

2,991

12.6

12.9

7.9

9.0

10.9

9.6

0.9

0.9

7.8

8.3

0.3

0.2

Jagran Prakashan

Buy

195

225

6,378

2,355

2,635

28.0

28.0

10.8

12.5

18.1

15.6

3.9

3.4

21.7

21.7

2.7

2.4

Sun TV Network

Neutral

487

-

19,200

2,850

3,265

70.1

71.0

26.2

30.4

18.6

16.0

4.8

4.2

24.3

25.6

6.2

5.3

Hindustan Media Ven.

Neutral

285

-

2,095

1,016

1,138

24.3

25.2

27.3

30.1

10.5

9.5

2.0

1.8

16.2

15.8

1.3

1.2

TV Today Network

Buy

300

363

1,790

637

743

27.5

27.5

18.4

21.4

16.3

14.0

2.8

2.4

17.4

17.2

2.5

2.0

Metal

Coal India

Neutral

331

-

208,977

84,638

94,297

21.4

22.3

24.5

27.1

13.5

12.2

5.6

5.4

42.6

46.0

2.0

1.8

Hind. Zinc

Neutral

228

-

96,485

14,252

18,465

55.9

48.3

15.8

21.5

14.5

10.6

2.4

2.1

17.0

20.7

6.8

5.3

Hindalco

Neutral

160

-

32,998

107,899

112,095

7.4

8.2

9.2

13.0

17.4

12.3

0.8

0.8

4.8

6.6

0.8

0.8

JSW Steel

Neutral

1,851

-

44,731

53,201

58,779

16.1

16.2

130.6

153.7

14.2

12.0

1.9

1.7

14.0

14.4

1.6

1.4

NMDC

Neutral

115

-

45,416

6,643

7,284

44.4

47.7

7.1

7.7

16.1

14.9

1.4

1.4

8.8

9.2

4.2

3.7

SAIL

Neutral

52

-

21,435

47,528

53,738

(0.7)

2.1

(1.9)

2.6

-

20.0

0.6

0.5

(1.6)

3.9

1.3

1.2

Vedanta

Neutral

174

-

51,467