Initiating coverage | Paints

February 28, 2017

Akzo Nobel India

BUY

CMP

`1,496

On a colorful growth trajectory

Target Price

`1,720

Akzo Nobel India Ltd (Akzo) is one of the leading paint manufacturers in India under

Investment Period

12 Months

the brand name ‘Dulux’. Akzo has ~11% share by revenue among the top 5 players.

It manufactures and markets a wide range of coatings (contributes ~90%) and

specialty chemicals & others (~10%). Akzo has six manufacturing facilities in

Stock Info

Hyderabad, Bengaluru, Gwalior, Mohali, Raigad & Navi Mumbai.

Sector

Paints

Akzo gaining market share: Paint industry has grown at CAGR of ~12% over

Market Cap (` cr)

6,999

FY2011-16, and most of the players have reflected the same growth trend, however,

Net Debt (` cr)

(322)

Akzo stands out as a front runner, as it has grown at a pace of 20% CAGR over the

same period. This implies that the company is steadily increasing its share in the pie

Beta

0.5

and is expected to continue the growth momentum going ahead.

52 Week High / Low

1,745/1,204

Affordable Housing recovery provides a perfect blend for growth: Real Estate industry

Avg. Daily Volume

266

had been underperforming since the last few years, however, considering that the

Face Value (`)

10

government has relaxed the norms to push affordable housing under the scheme

‘Housing For All’ and given benefits to the first home buyers, we expect a recovery in

BSE Sensex

28,817

the Real Estate sector going ahead. We believe Akzo is strongly placed to ride on this

Nifty

8,899

wave, as its brand ‘Dulux’ is well positioned in the premium decorative paints segment

Reuters Code

AKZO.BO

(2nd largest after Asian Paints) and the company also has a well planned and instrumental

strategy to increase its presence in tier II & III cities through its 8,800 dealer & distributor

Bloomberg Code

AKZO@IN

network, where pricing provides a competitive advantage to ‘Dulux’ over peers.

New facility in Noida, JV with Atul Ltd & Powder Coating plant in Mumbai:

Considering the potential of Indian markets, Akzo is expanding its base and

Shareholding Pattern (%)

aggressively setting up new facilities. Recently it has commissioned specialty coatings

Promoters

73.0

facility and colour laboratory in Noida 600 kl.p.a capacity to service customers from

MF / Banks / Indian Fls

8.4

consumer electronics, automobile and cosmetic industries. Secondly, it has entered in

JV with Atul Ltd. to produce MCA (monochloroacetic acid) with its latest technology at

FII / NRIs / OCBs

1.8

Atul's existing infrastructure in Gujarat. Finally, to encash the incremental double digit

Indian Public / Others

16.8

demand in powder coating segment, Akzo is setting up a facility in Mumbai to serve its

customers in the Northern and Western parts of India.

Outlook & Valuation: We expect Akzo to report revenue at 11% CAGR to `3,773cr

Abs.(%)

3m 1yr 3yr

and Adj. PAT at 25% CAGR to `375cr over FY2016-19E on the back of recovery in the

Sensex

10.9

23.4

39.6

real estate sector, reduced repainting cycle, strong brand and expansion in specialty

chemical. Notably, at present, Akzo is at lower valuations as compared to its peers in

Akzo Nobel India

7.3

17.7

97.1

the industry. EV/Sales for Akzo is at 1.9x FY2019E, whereas all the peers (Asian Paints,

Berger Paints & Kansai Nerolac) are above 3x, and the company’s EV/EBITDA is in

lower teens (11.8x FY2019E), whereas peers are in 20x category. Moreover, Akzo is

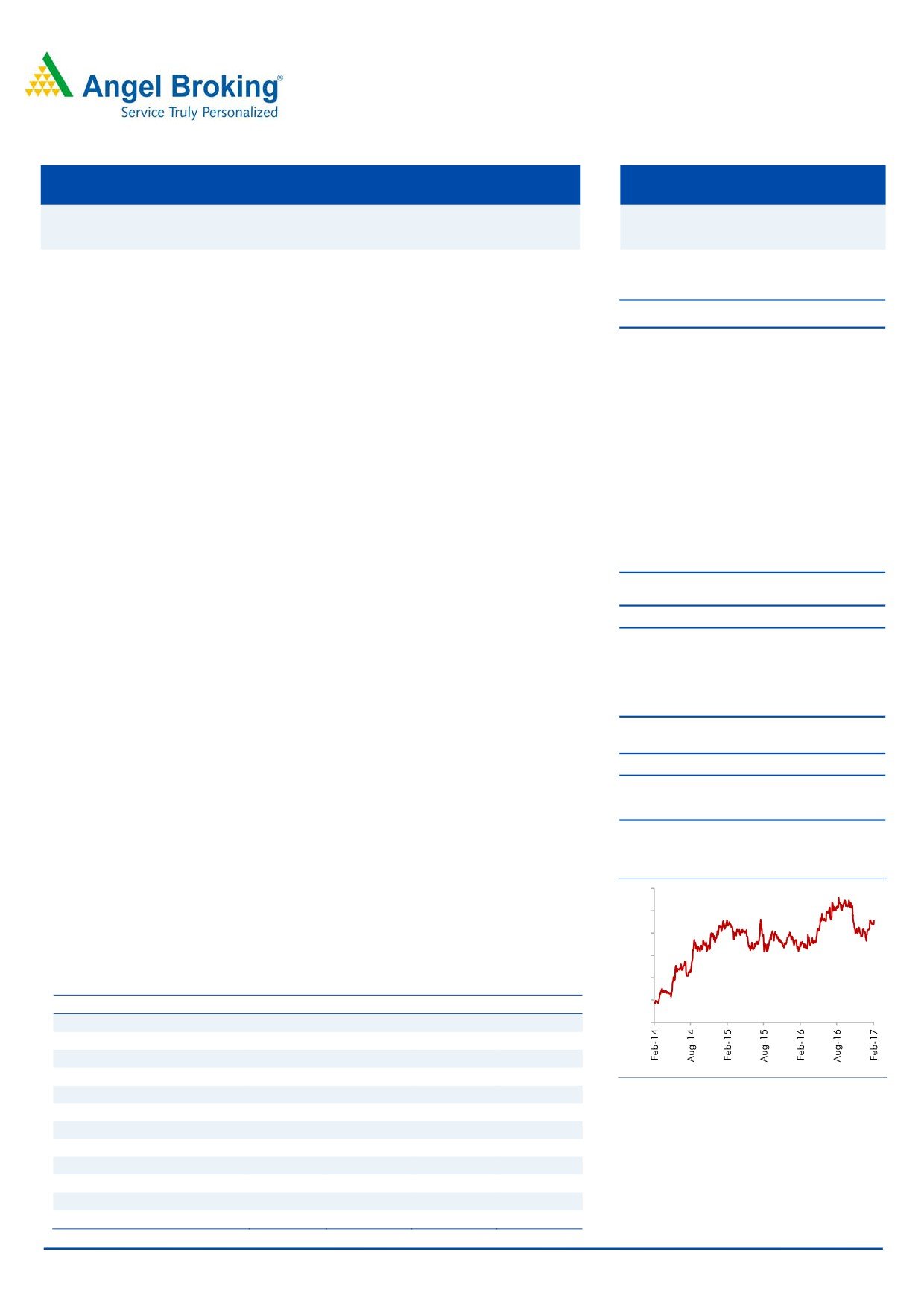

3-year price chart

currently trading at 18.6x P/E on FY2019E EPS, which is below its peers. We believe

1800

that the stock provides opportunity at these levels with attractive and relatively cheaper

valuations to the peers. At CMP of

`1,496, stock trading at

21.6x/18.6x of

1600

FY2018E/FY2019E EPS respectively, which we believe is attractive. We Initiate

1400

Coverage on the stock, with a ‘BUY’ recommendation, and a Target Price of `1,720

1200

(23x on Avg FY2018 & FY2019 EPS).

1000

Key Financials

800

Y/E March (` cr)

FY16

FY17E

FY18E

FY19E

Net Sales

2,740

2,955

3,309

3,773

600

% chg

8.4

7.8

12.0

14.0

Net Profit

192.2

266.7

323.4

375.3

% chg

4.7

38.8

21.3

16.0

Source: Company, Angel Research

EBITDA (%)

11.1

13.3

13.7

13.6

EPS (`)

41.2

57.2

69.3

80.4

P/E (x)

36.3

26.2

21.6

18.6

P/BV (x)

9.6

8.5

7.2

5.9

RoE (%)

26.4

32.7

33.3

31.8

RoCE (%)

10.3

12.9

14.5

14.9

Abhishek Lodhiya

EV/Sales (x)

2.6

2.4

2.1

1.9

022 - 39357800 Ext: 6811

EV/EBITDA (x)

19.9

15.8

13.5

11.9

Source: Company, Angel Research; Note : CMP as of February 27, 2017

Please refer to important disclosures at the end of this report

1

Initiating coverage | Akzo Nobel India

Key investment arguments

Akzo gaining market share

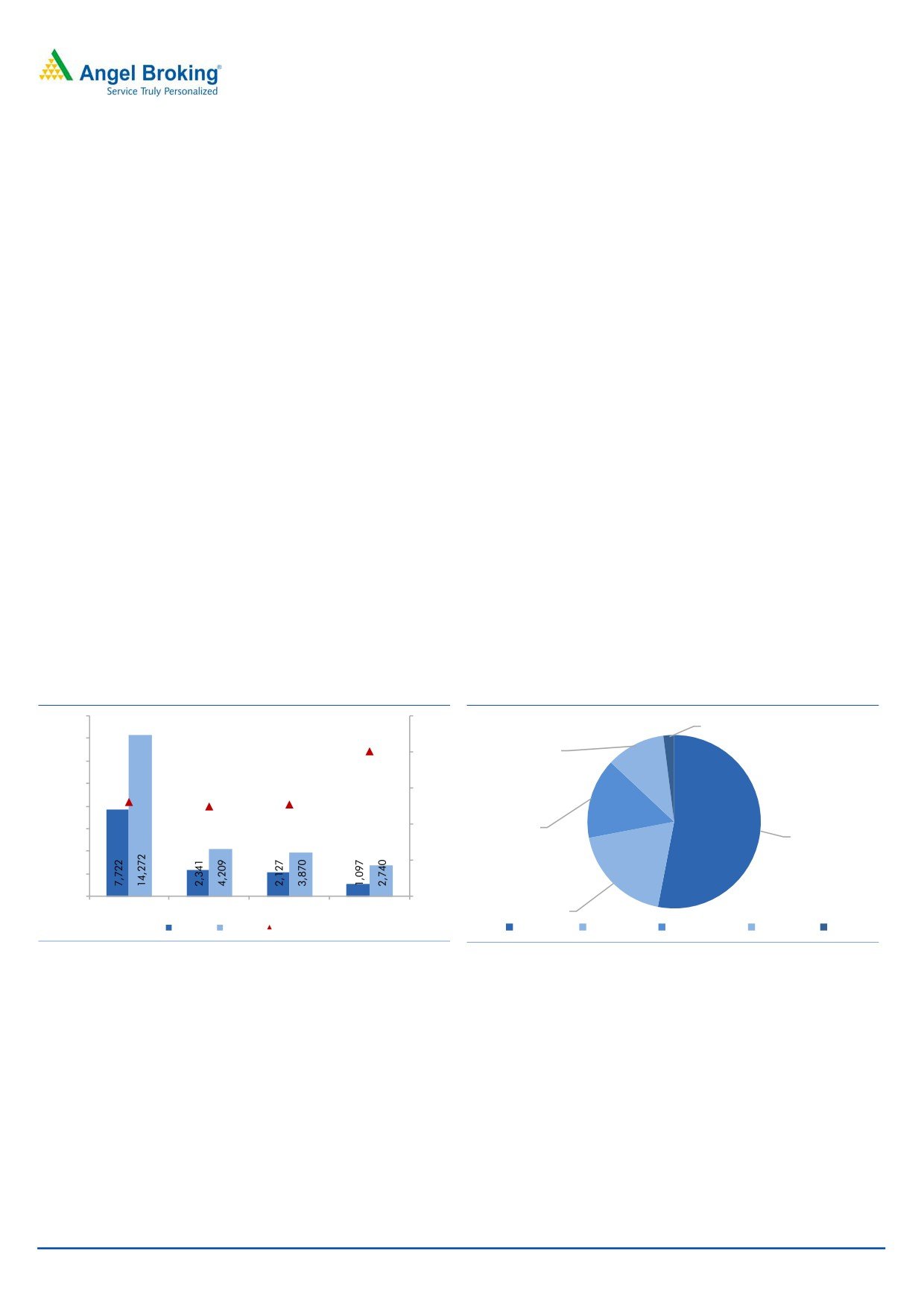

Industry has grown at ~12% CAGR

Paints industry is proxy to growth and consumption in the economy. The Indian

over FY2011-16, while Akzo stands out

Paints industry was around `40,300cr in FY2014-15 and is expected to reach

as front runner with 20% CAGR

`70,875cr by FY2019-20, according to India Paint Association (IPA). The industry

is divided into Decorative & Industrial Paints. The split of the Decorative Paints

market to Industrial Paints market is around 75-25 (Decorative Paints market size

in India was `30,385cr and the Industrial Paints was `9,915cr in FY2014-15).

Decorative Paints industry is mainly divided into organized players (~65%),

whereas remaining is constituted by the unorganized players. Unorganized players

predominantly serve the rural part of India where affordability is a bigger criterion

than quality & brand. Organized side of the industry is dominated by the 4-5

major players like Asian Paints, Berger Paints, Kansai Nerolac, Akzo Nobel (Dulux)

& Shalimar Paints. Asian Paints is the leader in industry with ~53% market share,

while Berger Paints 19%, Kansai Nerolac 15% and Akzo Nobel clocks 11% and

remaining is shared by other organized players. Paints industry has grown at a

CAGR of ~12% over FY2011-16 and most of the players have reflected the same

trend, however, Akzo stands out as front runner, as it has grown at the pace of

20% CAGR over same period, which implies it is steadily increasing its share in the

pie. We believe Akzo will maintain its historical growth trajectory and will continue

to grow at a steady pace. We expect Akzo's revenue to grow at 11.2% CAGR to

`3,773cr over FY2016-19E, on the back of incremental volumes and price hikes.

Exhibit 1: Revenue FY11-FY16 and CAGR growth

Exhibit 2: Market Share by Revenue

16,000

25.0

2

14,000

11

20.1

20.0

12,000

10,000

15.0

8,000

13.1

12.5

12.7

10.0

15

6,000

53

4,000

5.0

2,000

0

-

Asian Paints

Berger

Kansai

Akzo

19

FY11

FY16

% CAGR (FY11-16)

Asian Paints

Berger Paints

Kansai Nerolac

Akzo Nobel Others

Source: Company, Angel Research

Source: Company, Angel Research

Affordable Housing recovery provides a perfect blend for growth

Government’s push for Affordable

The demand for Decorative Paints is derived from B2B & B2C segments; where

Housing & benefits given to the first

B2B part of business serves the real estate developers and B2C business comes

home buyer to generate demand for

either from painting the new house or repainting of the existing house. Repainting

Decorative Paints

of house creates more than 65% of demand and remaining comes from the new

property and B2B business. Repainting cycle has shrunk to 4-5years from 7-

8years, which has helped the industry volumes to grow with steady pace, but as

real estate industry has been underperforming from the last few years, B2B

business has witnessed sharp decline. New launches and absorption rates have

dropped drastically in the country, which has led to the drop in the B2B business.

February 28, 2017

2

Initiating coverage | Akzo Nobel India

However, we are expecting recovery going ahead, as the government has relaxed

the norms to push affordable housing under the scheme ‘Housing For All’ and

given benefits to the first home buyers. We believe Akzo is strongly placed to ride

on this wave, as its brand ‘Dulux’ is well positioned in the premium decorative

paints segment (2nd largest after Asian Paints) and the company also has a well

planned and instrumental strategy to increase its presence in tier II & III cities

through its

8,800 dealer & distributor network, where pricing provides a

competitive advantage to ‘Dulux’ over peers. Further, the company spends ~5% of

its total revenue towards advertising & promotion in order to increase its brand

visibility and penetration, which is a positive for the company. Currently Shraddha

Kapoor and Farhan Akthar are the brand ambassadors for ‘Dulux’.

Exhibit 3: Advertising spend (%) of Revenue

6.0

5.6

5.5

5.1

5.0

5.0

5.0

5.0

4.8

4.7

4.5

4.3

4.0

FY12

FY13

FY14

FY15

FY16

FY17E FY18E FY19E

Source: Company, Angel Research

New facility in Noida, JV with Atul Ltd & Powder Coating plant in

Mumbai

Considering the potential of Indian markets, Akzo is expanding its base and

aggressively setting up new facilities. Recently, it has commissioned specialty

coatings facility and colour laboratory in Noida 600 kl.p.a capacity to service

customers from consumer electronics, automobile and cosmetic industries.

Company has invested `3cr of investment towards its Noida plant, thus catering to

the localization drive undertaken by many large players. Akzo has already

commissioned its first phase and is likely to complete its second phase by the end

of FY2017, which would provide further scope for expansion. According to the

Indian Brand Equity Foundation (IBEF), India is expected to be the fifth largest

market for consumer durables by

2025 and is also expected to reach at

US$400bn by 2020, and notably north India is the hub for this sector. The

company’s rational behind expanding in Noida is to serve this market better and

benefit from the incremental demand. Secondly, the size of the beauty, cosmetic

and grooming market is growing fast as well, and is expected to reach US$20bn,

which can be a further demand booster for the company’s product line.

Akzo has entered in JV with Atul Ltd. to install a world scale monocholoroacetic

acid (MCA) plant at Atul’s facility in Gujarat. It will use chlorine and hydrogen

manufactured by Atul to produce MCA (taking advantage of the Atul’s existing

February 28, 2017

3

Initiating coverage | Akzo Nobel India

infrastructure) and utilize Akzo Nobel’s latest eco friendly hydrogenation

technology for best results. Noida facility will serve the Indian MCA market along

with the captive requirement of Atul Ltd.

Finally, in order to encash the incremental double digit demand in powder coating

segment, Akzo has broken ground on its new powder coatings plant in Mumbai,

India. The investment of ₹63.5cr will allow the company to increase capacity in the

region, which forms an important part of its organic growth plans. The new facility

will complement Akzo’s existing plant in Bangalore, which is focused on supplying

to the Southern and Eastern parts of the country, whereas upcoming facility will

focus on the customers in the Northern and Western regions. The Mumbai facility

will also produce several new product lines for the Indian market, including

bonded metallic powders and localized products for markets such as pipe and re-

bar coatings. Revenue from new Mumbai facility will start contributing to the top-

line from the 2HFY2018.

Along with the Greenfield expansion Akzo also took a Brownfield route to further

boost the top-line. Akzo India acquired Indian industrial coatings business at

~`11cr comprising of Functional Materials & Solutions segment which caters to

wind energy segment & construction industry. Addition of BASF’s folio will

strengthen its position in the industrial coating and deepen its product offering to

the present clientele, which will reflect in the top-line going forward.

We believe these new facilities and recent acquisition will certainly contribute to the

company’s revenue in coming years.

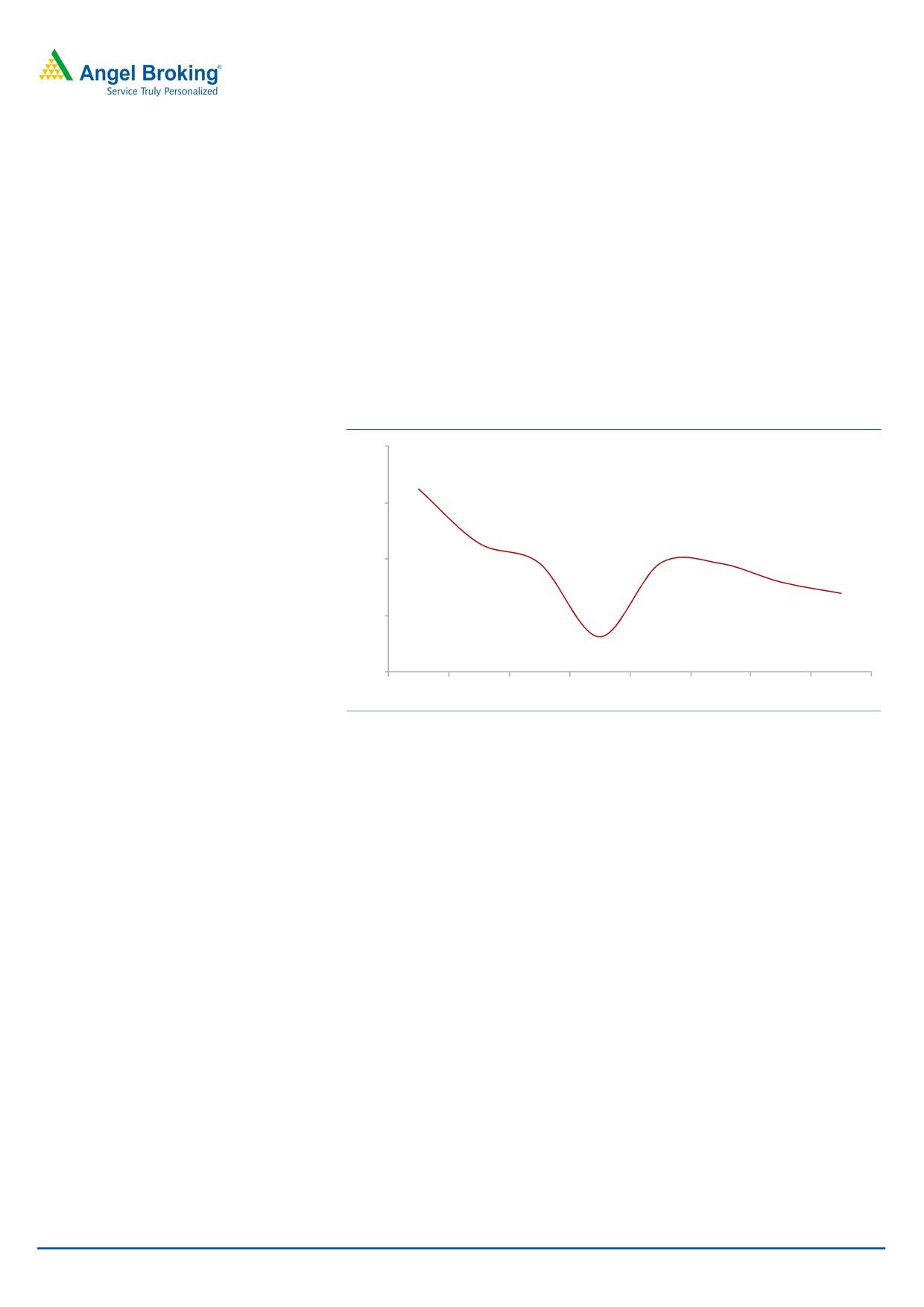

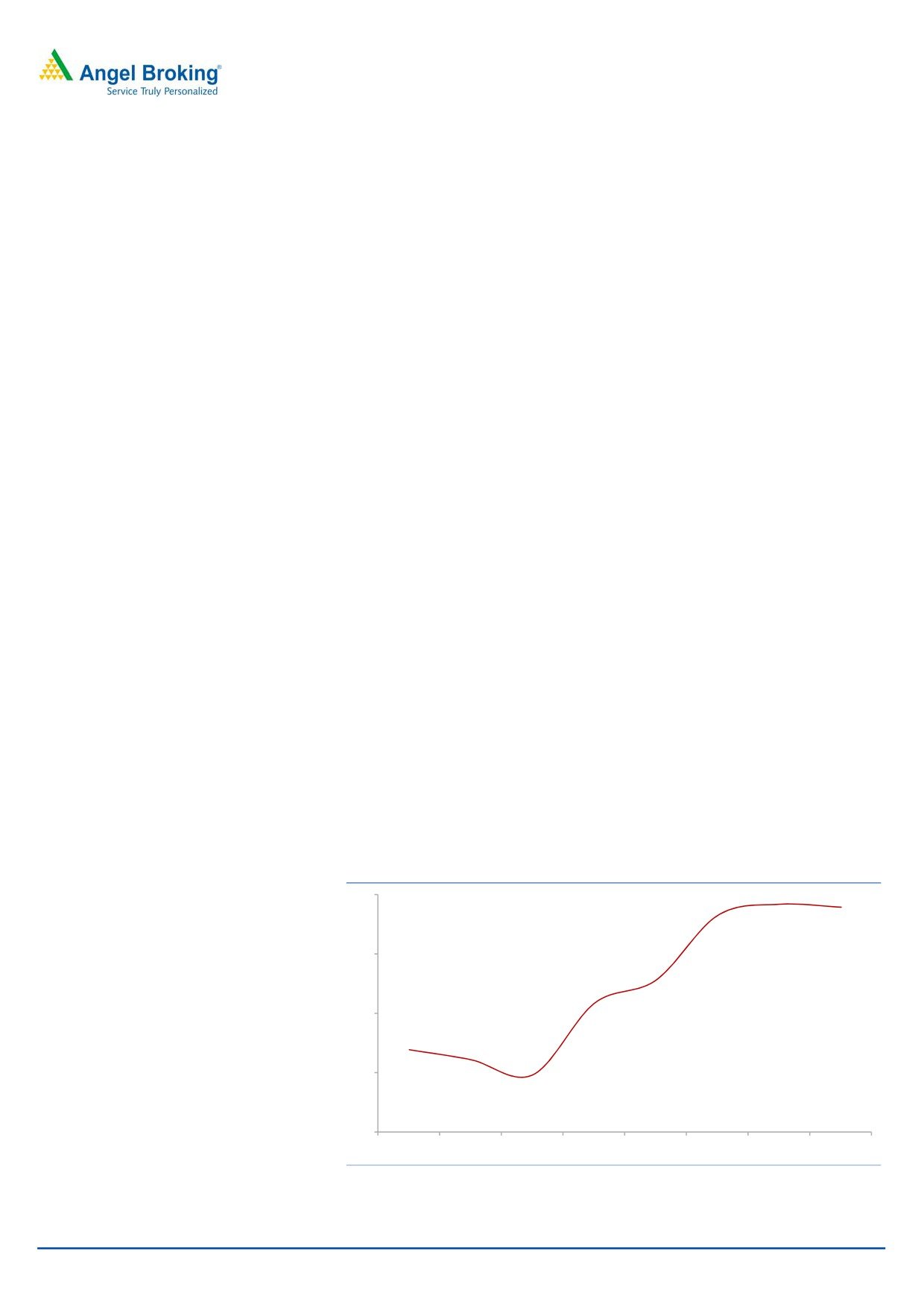

Operating margins recovering from the bottom

Akzo’s operating margin had taken a dip in FY2012 and remained in the range of

7.8%-8.8% untill FY2014 due to the amalgamation of 3 fellow subsidiaries with

Akzo operating in the country. Secondly Crude & Titanium dioxide prices were at

their highest levels during the same period. Margins witnessed decent recovery of

240bps from the bottom (FY2014) in FY2015 and will continue to inch up as input

cost is fairly stable.

Exhibit 4: EBITDA Margin (%)

14

13.7

13.6

13.3

12

11.1

10

10.3

8.8

8

8.4

7.9

6

FY12

FY13

FY14

FY15

FY16

FY17E FY18E FY19E

Source: Company, Angel Research

February 28, 2017

4

Initiating coverage | Akzo Nobel India

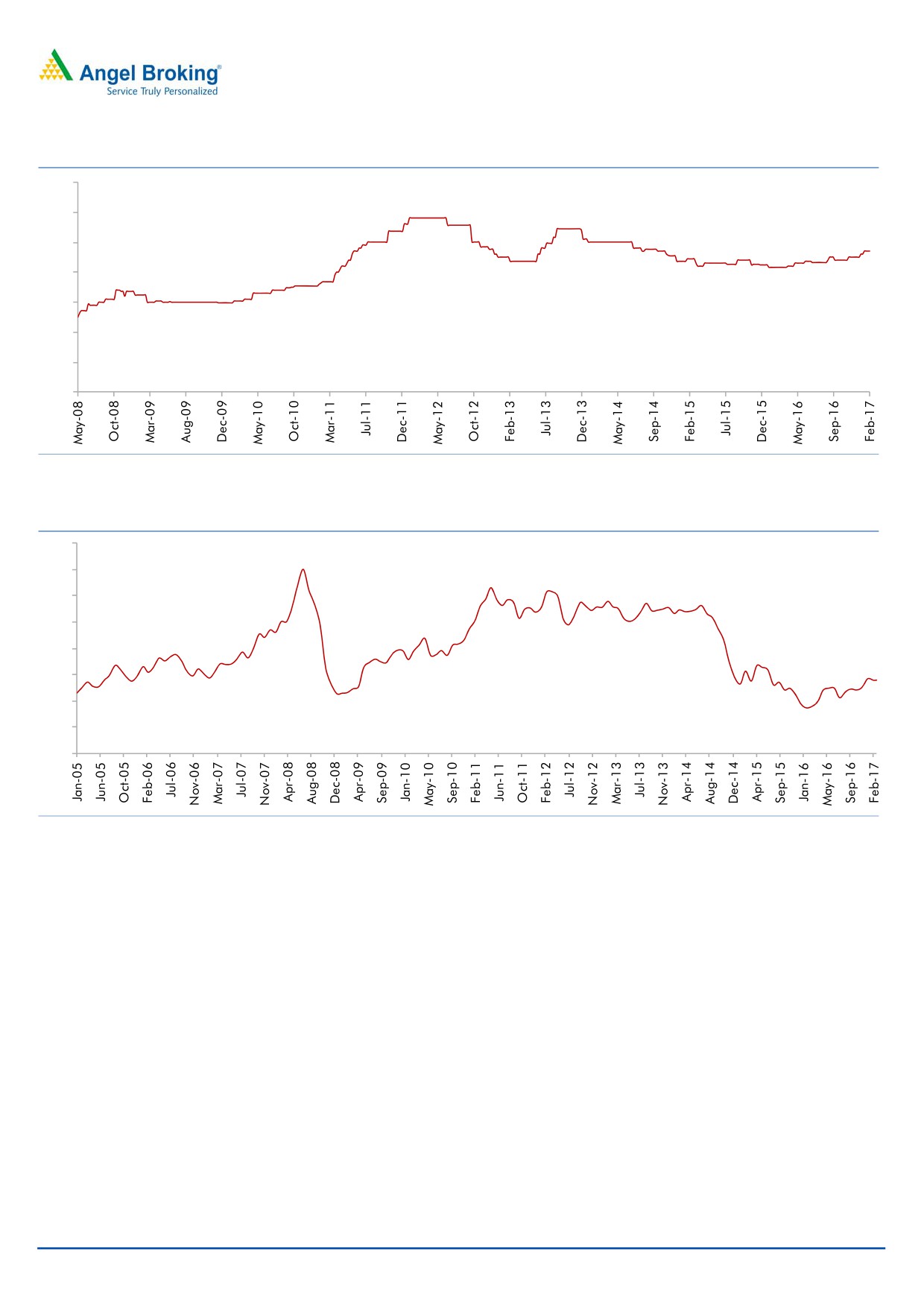

Exhibit 5: Titanium Dioxide Price (`/kg)

350

300

250

200

150

100

50

0

Source: Angel Research, Bloomberg

Exhibit 6: Brent Crude Prices (US$/b)

160

140

120

100

80

60

40

20

0

Source: Angel Research, Bloomberg

We believe there is further scope for Akzo’s operating margin to improve by

200-250bps from here, on the back of stable input price and the tight cost control

by the management on expenditures.

February 28, 2017

5

Initiating coverage | Akzo Nobel India

Outlook & Valuation

Considering the recovery in the affordable housing segment, reduced repainting

cycle and expansion plan of the Akzo, we believe that the company’s revenue

would grow at 11% CAGR to `3,773cr over the period of FY2016-19E and will

steadily increase its market share in the Premium Decorative Paints segment. As

Akzo’s operating margin is improving, we expect that profitability would also

simultaneously witness an upward trend and Adj. PAT will grow at 25% CAGR to

`375cr over the period of FY2016-19E.

Notably, at present, Akzo is at lower valuations compared to its peers in the

industry. EV/Sales for Akzo is at 1.9x FY19E, whereas all the peers (Asian Paints,

Berger Paints & Kansai Nerolac) are above 3x, and the company’s EV/EBITDA is in

lower teens (11.8x FY19E), whereas peers is in 20x category. Moreover, Akzo is

currently trading at 18.6x P/E on FY19E EPS, which is below its peers. We believe

the stock provides opportunity at these levels with attractive and relatively cheaper

valuations to the peers. At CMP of `1,496, stock trading at 21.6x/18.6x of

FY18E/FY19E EPS respectively which we believe is attractive. We Initiate Coverage

on the stock, with a ‘BUY’ recommendation and Target Price of `1,720 (23x on

Avg FY18&FY19 EPS).

Peer Analysis

Exhibit 7: Peer Analysis

Market Cap

EPS

P/E

EV/EBITDA

EV/Sales

ROE (%)

(` Cr.) FY17E

FY18E FY19E

FY17E FY18E FY19E

FY17E FY18E FY19E

FY17E FY18E FY19E

FY17E FY18E FY19E

Akzo Nobel

6,980

57.2

69.3

80.4

26.2

21.6

18.6

15.8

13.5

11.9

2.4

2.1

1.9

32.7

33.3

31.8

Asian Paints

96,375

21.8

25.9

27.9

46.2

38.9

36.1

33.5

28.4

23.8

6.7

5.7

4.5

34.4

34.9

35.6

Berger Paints

22,512

4.7

5.6

6.3

49.7

41.2

36.5

25.5

21.3

22.5

3.7

3.1

3.4

27.9

28.4

32.9

Kansai Nerolac

19,269

8.6

10.4

11.4

42.7

35.3

32.2

26.9

22.5 20.57

4.4

3.8

3.5

17.0

17.6

23.3

Source: Angel Research, Bloomberg

Downside risks to our estimates

Sharp increase in Crude and Titanium dioxide poses a risk to the operating

margins, even though some of its incremental input cost will be passed on to

the consumers.

Prolonged pain in the housing segment is a risk to the company’s incremental

revenue, as it contributes nearly 30-35% of top-line.

February 28, 2017

6

Initiating coverage | Akzo Nobel India

Company Background

Akzo Nobel India Ltd (Akzo) is a leading paint manufacturer in India with ~11%

market share by revenue among the top 5 players. It manufactures and markets a

wide range of coatings and specialty chemicals. It has been present in India for

over 100 years and is the fourth largest player in the Paints industry. Over 1,900

people work at Akzo Nobel India in its six production facilities, two state-of-the-art

research laboratories and 88 warehouses. Akzo’s 8,800 strong dealer/partners

network aggressively pushes sales, while the strong MNC backing of Akzo Nobel

NV ensures quality products and technical expertise. Akzo has plants at Bangalore,

Hyderabad, Mohali, Thane, Gwalior and Raigad. It is broadly into 9 different

coating segments including the decorative and the performance (Industrial

coatings). Some of the other important verticals include powder coatings, coil

coatings, protective coatings, wood coatings, etc. Coating business contributes

~90% of Akzo’s revenue, while the remaining 10% comes from specialty chemical

& others. The company’s decorative segment portfolio is skewed towards premium priced

products (‘Dulux’ brand). In the premium Decorative Paints segment, the company enjoys

a market share of around ~22% as compared to its overall market share of ~11%.

Akzo’s Decorative Paints business-line manufactures the ‘Dulux’ brand of paints for

interior and exterior decoration and protection as well as products for surface

preparation and wood care. The emphasis is on quality, aesthetics and high

performance in terms of longevity, washability and stain resistance, anti-colour

fading, water proofing, quicker & easier applicability, faster drying time, low VOC

and odour, and so on.

Akzo Nobel India’s Performance Coatings business-line provides some of the most

advanced packaging coatings and inks in the market, protecting everything from

food and drinks cans to aerosols and metal closures. Performance coatings have

diverse functions and have four applications viz. Industrial Coatings, Powder

Coatings, Automotive & Aerospace Coatings, Marine & Protective Coatings.

The Specialty Chemicals business in India deals in more than 30 products grouped

under organic peroxides, metal alkyls and polymer additives to pharmaceutical

companies, polymer producers, composite and rubber industry.

As a part of its growth strategy, in May 2012, Akzo merged three Indian

subsidiaries of Akzo Nobel NV - Akzo Nobel Coatings India, Akzo Nobel Car

Refinishes India, and Akzo Nobel Chemicals (India) - by issuing additional share

of 11.1mn in accordance with the share swap ratio of the scheme. The merger

brought the company’s operations in India under a single umbrella. Before

merger, Akzo operated in two segments of coating industry - decorative and auto

refinish, but after the merger, its operation has increased to 11 segments.

Exhibit 8: Akzo’s Product Portfolio

Premium Range

Mid - Range

Economy

Exterior

DSS Colour Bright

Dulux Promise Maxilite Acrylic Distemper,

Weathershield Max

Dulux Guardian

ICI Magik

ICI Acrylic Distemper

Weathersheild

Velvet Touch ‘Pearl Glo’

Maxilite

Plastic super smooth

Promise

Velvet Touch ‘Trends’ Rainbow Emulsion

WeatherShield Ultra Clean

Dulux satin Finish

WeatherShield Tex

Dulux super Gloss

Source: Company, Angel Research

February 28, 2017

7

Initiating coverage | Akzo Nobel India

Profit & Loss Statement

Y/E March (` cr)

FY15

FY16

FY17E

FY18E

FY19E

Total operating income

2,527

2,740

2,955

3,309

3,773

% chg

4.5

8.4

7.8

12.0

14.0

Total Expenditure

2,266

2,435

2,562

2,857

3,261

Raw Material

1,406

1,469

1,545

1,731

1,992

Personnel

206

231

243

261

290

Others Expenses

654

736

774

865

978

EBITDA

261

305

393

453

512

% chg

36.2

16.6

28.9

15.1

13.2

(% of Net Sales)

11.5

12.5

15.3

15.8

15.7

Depreciation& Amortisation

53

53

54

57

63

EBIT

209

251

339

395

449

% chg

40.9

20.4

34.9

16.6

13.5

(% of Net Sales)

9.2

10.3

13.2

13.8

13.8

Interest & other Charges

2

1

1

2

2

Other Income

65

40

43

65

74

(% of PBT)

23.9

13.8

11.4

14.2

14.3

Recurring PBT

272

290

381

459

521

% chg

33.9

6.5

31.4

20.4

13.6

Tax

89

98

114

135

146

(% of PBT)

32.6

33.7

30.0

29.5

28.0

PAT (reported)

184

192

267

323

375

Extraordinary Items

3

10

-

-

-

PAT after MI (reported)

186

202

266

323

375

ADJ. PAT

183

192

266

323

375

% chg

22.3

4.7

38.8

21.3

16.0

(% of Net Sales)

7.3

7.0

9.0

9.8

9.9

Fully Diluted EPS (`)

39.3

41.2

57.2

69.3

80.4

% chg

(5.3)

4.7

38.8

21.3

16.0

February 28, 2017

8

Initiating coverage | Akzo Nobel India

Balance Sheet

Y/E March (` cr)

FY15

FY16

FY17E

FY18E

FY19E

SOURCES OF FUNDS

Equity Share Capital

47

47

47

47

47

Reserves& Surplus

873

682

770

925

1,133

Shareholders Funds

920

729

816

972

1,179

Deferred Tax Liability

11

14

14

14

13

Total Liabilities

931

743

831

986

1,192

APPLICATION OF FUNDS

Gross Block

581

583

630

626

618

Less: Acc. Depreciation

53

53

54

57

63

Net Block

528

530

576

568

555

Investments

394

546

569

630

726

Current Assets

876

943

989

1,160

1,430

Inventories

365

359

381

432

519

Sundry Debtors

278

318

329

388

474

Cash

60

55

59

96

159

Loans & Advances

159

186

192

213

243

Other Assets

14

25

27

31

35

Current liabilities

868

1,276

1,302

1,373

1,518

Net Current Assets

8

(333)

(314)

(213)

(88)

Total Assets

931

743

831

986

1,192

Cashflow Statement

Y/E March (` cr)

FY15

FY16

FY17E

FY18E

FY19E

Profit before tax

275

300

381

459

521

Depreciation

53

54

54

57

63

Change in Working Capital

(35)

65

(14)

(65)

(63)

Interest / Dividend (Net)

2

1

1

2

2

Direct taxes paid

(73)

(113)

(114)

(135)

(146)

Others

(66)

(42)

(11)

0

0

Cash Flow from Operations

155

264

297

318

378

(Inc.)/ Dec. in Fixed Assets

(51)

(39)

(100)

(50)

(50)

(Inc.)/ Dec. in Investments

287

(128)

(23)

(61)

(96)

Others

3

11

0

0

0

Cash Flow from Investing

239

(157)

(123)

(111)

(146)

Issue of Equity

0

0

0

0

0

Dividend Paid (Incl. Tax)

(409)

(112)

(168)

(168)

(168)

Interest / Dividend (Net)

(2)

(1)

(1)

(2)

(2)

Cash Flow from Financing

(406)

(113)

(169)

(170)

(170)

Inc./(Dec.) in Cash

(12)

(5)

4

37

62

Opening Cash balances

72

60

55

59

96

Closing Cash balances

60

55

59

96

159

February 28, 2017

9

Initiating coverage | Akzo Nobel India

Key Ratios

Y/E March

FY15

FY16

FY17E

FY18E

FY19E

Valuation Ratio (x)

P/E (on FDEPS)

38.0

36.3

26.2

21.6

18.6

P/CEPS

29.2

27.3

21.8

18.3

15.9

P/BV

7.6

9.6

8.5

7.2

5.9

Dividend yield (%)

2.7

9.4

4.0

4.0

4.0

EV/Sales

2.8

2.6

2.4

2.1

1.9

EV/EBITDA

21.4

19.9

15.8

13.5

11.9

EV / Total Assets

3.6

3.6

3.3

3.1

2.8

Per Share Data (`)

EPS (Basic)

39.3

41.2

57.2

69.3

80.4

EPS (fully diluted)

39.3

41.2

57.2

69.3

80.4

Cash EPS

51.2

54.8

68.7

81.6

94.0

DPS

20.0

70.0

30.0

30.0

30.0

Book Value

197.0

156.2

175.0

208.3

252.7

Dupont Analysis

EBIT margin

9.2

10.3

13.2

13.8

13.8

Tax retention ratio

0.7

0.7

0.7

0.7

0.7

Asset turnover (x)

1.3

1.4

1.4

1.5

1.5

Operating ROE

20.0

26.4

32.7

33.3

31.8

Returns (%)

ROCE

9.7

10.3

12.9

14.5

14.9

ROE

20.0

26.4

32.7

33.3

31.8

Turnover ratios (x)

Asset Turnover (Gross Block)

1.3

1.4

1.4

1.5

1.5

Inventory / Sales (days)

47

45

45

46

48

Receivables (days)

20

21

20

21

23

Payables (days)

60

74

70

65

65

WC cycle (ex-cash) (days)

8

(8)

(4)

2

5

Solvency ratios (x)

Net debt to equity

-

-

-

-

-

Interest Coverage (EBIT / Int.)

139.2

199.5

240.8

249.4

248.4

February 28, 2017

10

Initiating coverage | Akzo Nobel India

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Akzo Nobel India

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 28, 2017

11