Initiating coverage | Capital Goods

March 18, 2015

Action Construction Equipment

BUY

CMP

`42

Turn-around on the Cards…

Target Price

`54

Action Construction Equipment (ACE) is among the leading crane manufacturers in

Investment Period

12 Months

the Indian construction equipment (CE) market with a share of 35% in the Pick and

Carry crane market. ACE’s product portfolio comprises of a range of Cranes,

Stock Info

Backhoe Loaders and Forklifts, Tractors, and Harvesters.

Sector

Construction Equip.

Business set to turn-around: Recent announcements in the Union Budget 2015-16

Market Cap (` cr)

417

strengthen our view that Cranes, CE, and Material Handling (MH) business

segments are up for revival. Considering ACE’s strong market positioning, wide

Net debt (` cr)

128

pan-India dealership network, long-standing relationship with customers who give

Beta

1.5

repeat business, and wide range of product portfolio, we expect segment volumes

52 Week High / Low

49/12

and blended realization to catch-up from here-on. We expect ACE to post

Avg. Daily Volume

107,463

an18.8% top-line CAGR during FY2015-17E to `838.5cr. Demand recovery,

Face Value (`)

2

coupled with cost cutting initiatives at the floor level, higher localization initiatives,

focus on lowering imports, and expected decline in Mild Steel (forms biggest raw

BSE Sensex

28,736

material component) prices, strengthens our view that ACE is well positioned to

Nifty

8,723

absorb fixed costs and experience margin expansion. Accordingly, EBITDA margins of

Reuters Code

ACEL.BO

the company would expand from 3.0% in FY2015E to 8.2% in FY2017E. Since its last

Bloomberg Code

ACCE@IN

round of capex in FY2011-12, with the onset of infra capex down-cycle, poor

demand led Cranes, CE and MH division plants to run at sub-50% capacity

utilization levels. ACE’s Management highlighted that there is no need for the

Shareholding Pattern (%)

company to pursue any major capex, until their revenues cross `1,200cr. In

Promoters

68.3

absence of any major capex, we expect entire benefits of EBITDA margin

expansion to trickle down to PAT level (PAT margins to expand from 0.9% in

MF / Banks / Indian Fls

3.3

FY2015E to 4.6% in FY2017E). In-line with strong growth in profitability and

FII / NRIs / OCBs

0.4

improved cash flow generating potential, RoEs would improve from 1.7% in

Indian Public / Others

28.1

FY2015E to 11.3% in FY2017E.

Compelling valuations at current levels: We are optimistic that ACE would be able

to maintain its numero uno position in the domestic Pick and Carry cranes

Abs. (%)

3m 1yr 3yr

segment. Further, the company’s wide range of product offerings, wide pan-India

Sensex

1.7

31.6

66.4

distribution network, and recent cost cutting initiatives, put ACE in a strong

ACE

10.2

195.4

28.1

position. Given the backdrop of strong earnings growth and RoE expansion, we

assign a P/E multiple of 14.0x to our FY2017E EPS of `3.9 and arrive at a price

target of `54 for the stock. Being a turnaround story, we alternatively checked

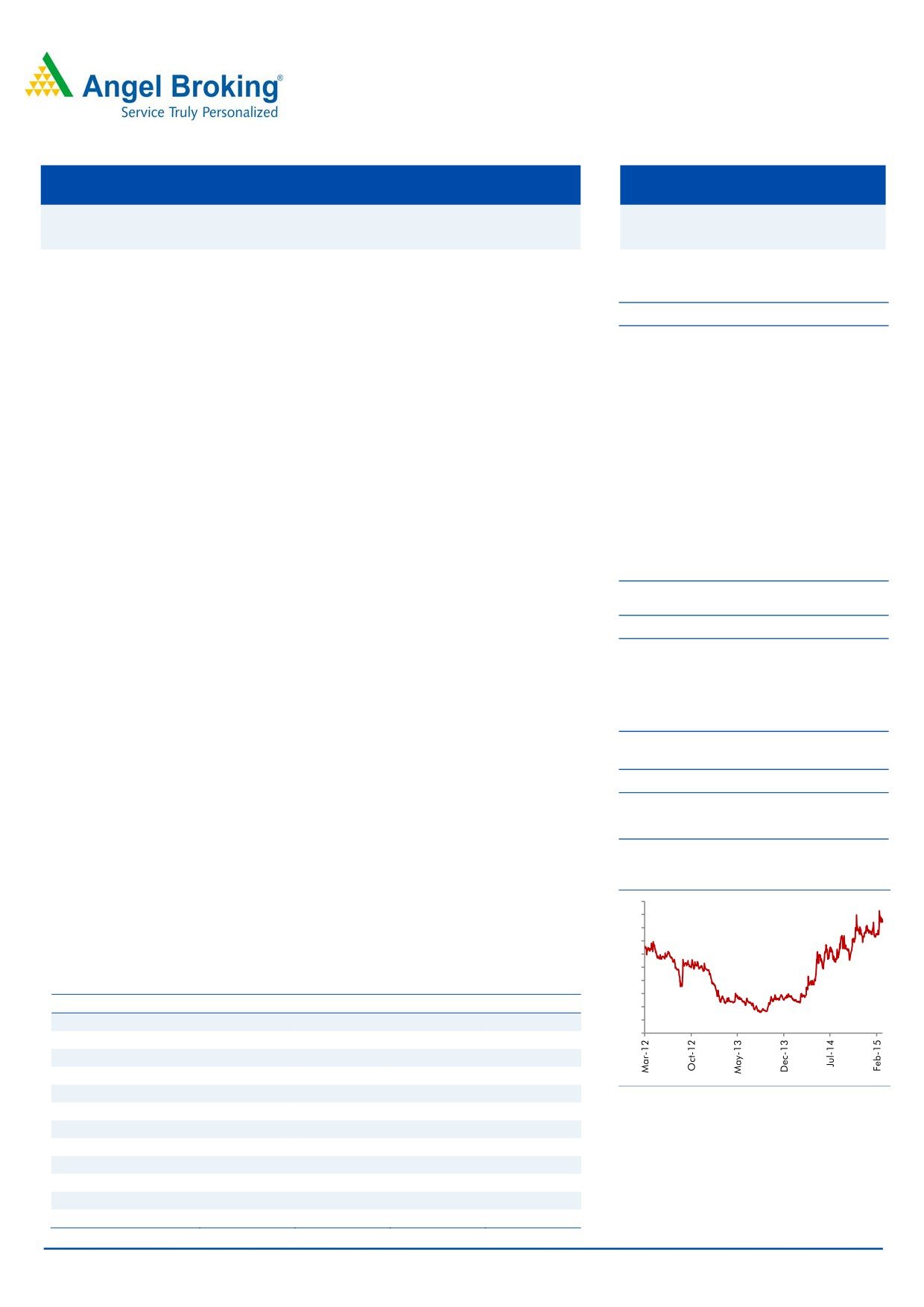

3-Year Daily price chart

ACE’s stock on EV/sales multiple. At target P/E multiple of 14.0x, the implied

50

45

FY2017E EV/sales multiple comes in at 0.75x, which is comforting. Given the

40

28.4% upside from the current market price of the stock, we initiate coverage on

35

30

ACE with a BUY recommendation.

25

20

Key Financials

15

Y/E March (` cr)

FY14

FY15E

FY16E

FY17E

10

Net Sales

615

594

660

839

5

0

% chg

(7.9)

(3.3)

11.0

27.1

Net Profit

4

5

10

38

% chg

(37.6)

30.4

93.5

276.8

EBITDA (%)

3.9

3.0

4.7

8.2

Source: Company, Angel Research

EPS (`)

0.4

0.5

1.0

3.9

P/E (x)

103.7

79.5

41.1

10.9

P/BV (x)

1.4

1.3

1.3

1.2

RoE (%)

1.3

1.7

3.2

11.3

RoCE (%)

3.4

4.2

5.3

13.1

Yellapu Santosh

EV/Sales (x)

0.9

0.9

0.8

0.6

022 - 3935 7800 Ext: 6828

EV/EBITDA (x)

22.0

28.7

16.6

7.5

Source: Company, Angel Research; Note: CMP as of March 17, 2015

Please refer to important disclosures at the end of this report

1

Initiating coverage | Action Construction Equipment

Construction Industry to see strong revival

In the last few years, Construction spending has witnessed a sharp decline.

Construction spending growth on a yoy basis during FY2011-12 witnessed a

double digit growth. Since then (during FY2013-14) spending has been on a

declining growth trend. In FY2015, Construction spending is expected to report a

4.5% yoy increase.

Exhibit 1: Construction Spending Growth (yoy)

25.0%

20.7%

20.0%

14.2%

15.0%

10.0%

7.4%

4.5%

5.0%

2.5%

0.0%

FY11

FY12

FY13

FY14

FY15

Source: MoSPI, Angel Research

The new government in the last few months (1) passed an ordinance with amends

to land acquisition bill, (2) increased foreign direct investment (FDI) in Defense and

Railways sectors, (3) is working on merging the Power and Coal ministries, (4)

merged/ abolished committees/ Ministerial groups for quicker Infra projects’

clearances, (5) exempted environmental clearance (EC) for Irrigation projects with

command area of up to 2,000 hectares, (6) made banks to adopt ‘5/25 lending

structure’, where loans can now be made up to 25 years (vs. earlier 15 years), with

an option to refinance after every 5 years, (7) delegated powers for grant of forest

clearances to the regional state level offices,

(8) enabled online filing for

clearances to construct road overbridge (RoB) and road underbridge (RuB),

(9) increased limits on sand mining, (10) EC through the e-portal route for Infra

projects, (11) brought more clarity on Real Estate Investment Trusts (REITs) and

Infrastructure Investment Trusts (InvITs), and (12) empowered Ministry of Road

Transport & Highways (MoRTH) to appraise and approve projects on its own up till

`1,000cr and made changes to Model Concession Agreement (MCA). Also,

positive commentary in the Union Budget FY2015-16, higher budgetary allocation

towards Infra sub-sectors, assurance to provide quicker clearances, and

opening-up of new funding avenues, indicate the government’s intent to revive the

ailing Infrastructure sector.

As highlighted below, budgetary allocation towards some of the key Ministries

which would impact the government’s Infra spending has been increased by

52.7% yoy to `83,255cr in FY2015-16E. The government’s reformist agenda and

its upbeat mood to spend towards the Infra sector creates a favourable outlook

towards the Infra sector in the near-to-medium term.

March 18, 2015

2

Initiating coverage | Action Construction Equipment

Exhibit 2: Budgetary Allocation for FY2015-16

Actual

Revised

Budget

Change

Details of the Ministry (` in cr)

(2013-14)

(2014-15)

(2015-16)

(%)

Ministry of Housing & Urban Develop.

6,703

7,547

10,068

33.4

Ministry of Roads & Highways

14,891

16,770

33,049

97.1

Ministry of Water Resources, River

86

103

138

34.0

Development & Ganga Rejuvenation

Ministry of Railways

27,072

30,100

40,000

32.9

Total Budgetary Allocations

48,752

54,520

83,255

52.7

Source: Union Budget Docs, Angel Research

In order to understand growth drivers for the CE sector, we try to study the outlook

of some of the key Infra sub-verticals.

Roads & Highways

Taking into consideration

(1)

97.1% yoy increase in budgetary allocation (to

`33,049cr), (2) ~100,000km of rural roads construction across the country (at

different stages), and (3) government target to construct another ~100,000km of

rural roads in years to come, we expect the outlook for the Road sector to improve

form here on. In addition to higher award activity, reform announcements

strengthen our view that road construction/ day would pick-up from 4.3km/day in

FY2014 to 11.8km/day in FY2016E.

Exhibit 3: MoRTH Road Activity (in kms)

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015E

FY2016E

Construct

Target to Award

Awarded

Source: NHAI, Media Publication, Angel Research

On the whole, we expect `90,000cr of road construction (MoRTH + State

Highways + Rural) business opportunity to emerge during FY2016-17E. Our

above-stated estimates factor major contribution of private road Engineering

Procurement and Construction (EPC) players.

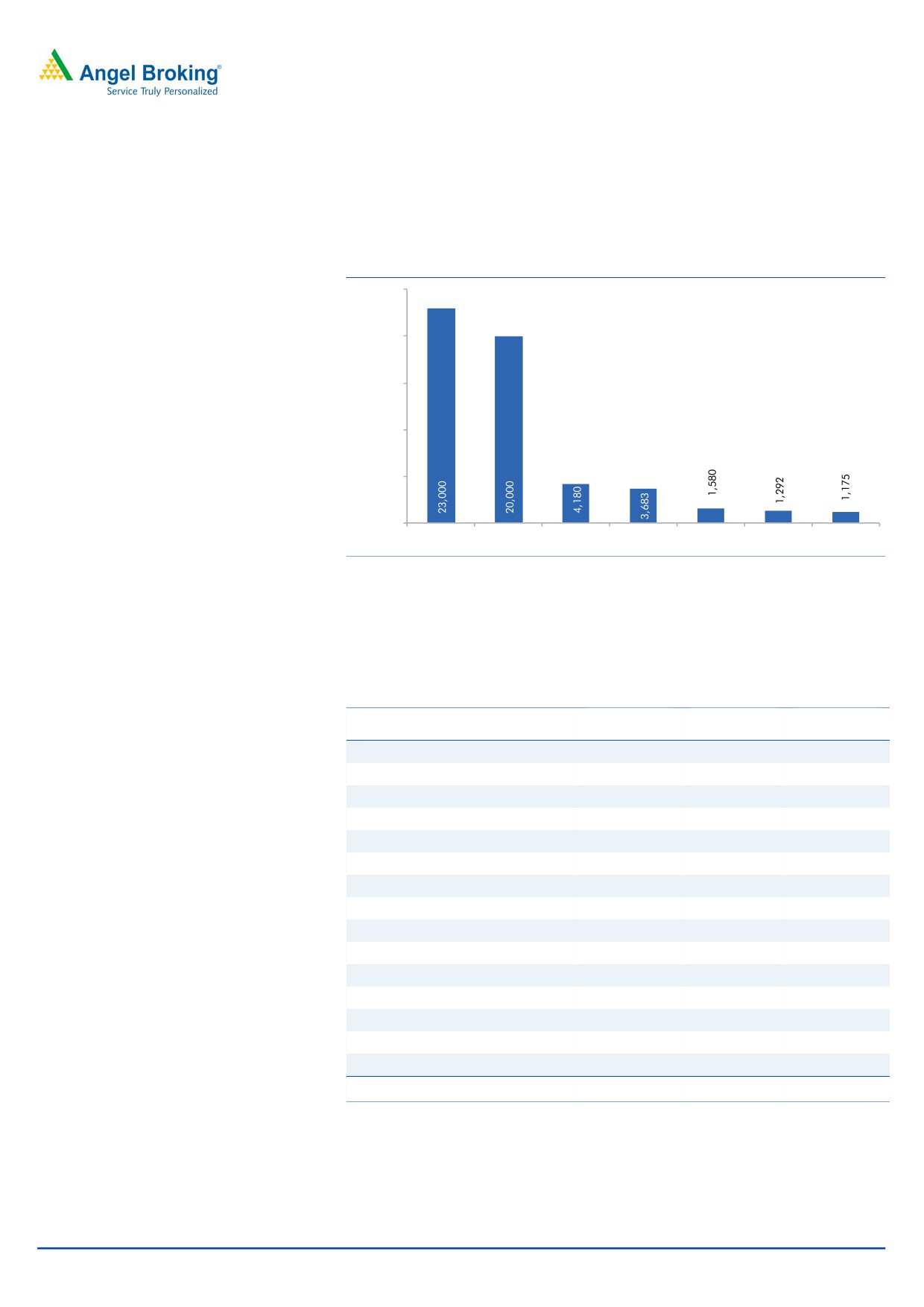

Power

The government has timely announced its support to ensure faster completion of

~87GW of Thermal Power plants, which are under different stages of construction.

In order to address issues impeding the sector, the government has set ambitious

coal production targets to address fuel linkage issues, assured quicker EC and

March 18, 2015

3

Initiating coverage | Action Construction Equipment

forest clearance (FC) clearances for power projects, and opened up new avenues

of fund raising for power developers. In the recent Union Budget 2015-16E, the

Finance Minister (FM) announced that Power PSUs would increase their yoy capex

outlay by 6.8% to `54,910cr.

Exhibit 4: Power PSUs Capex (` cr)

25,000

20,000

15,000

10,000

5,000

0

NTPC

PGCIL

NHPC

DVC

THDC

NEEPCO

SJVNL

Source: Company, Angel Research

We expect revival in the Power capex cycle to be led by PSUs and Power Gencos.

We see strong visibility over 15GW of Thermal and Hydro Power projects to be

awarded by PSU Gencos, which have EPC works scope.

Exhibit 5: Power PSUs’ capex (` cr)

Power Gen.

Size

Contract Size

Project Details

Type

(MW)

(` cr)

Udangudi, TANGEDCO

Thermal

1,320

6,600

Manuguru, TSGENCO

Thermal

1,080

5,400

Darjeeling, NTPC

Hydro

120

300

Khargone, NTPC

Thermal

1,320

6,600

Kothagudem, APGENCO

Thermal

800

4,000

Nellore, APGENCO

Thermal

800

4,000

Nashik, MAHAGENCO

Thermal

660

3,300

Para, MAHAGENCO

Thermal

250

1,300

Sagardighi, WBPDCL

Thermal

500

2,500

Patratu, JSEB

Thermal

1,320

6,600

Ghatampur, Nevyeli Lignite

Thermal

1,980

9,900

Harduagunj, UPRVUNL

Thermal

660

3,300

Bhanswara, RRVUNL

Thermal

1,320

6,600

Satpura, MPPGCL

Thermal

660

3,300

Dondaicha, MAHAGENCO

Thermal

1,980

9,900

Totals

14,770

73,600

Source: Company, Govt. website, Media Publications, Angel Research

In the recent budget, the FM has shown thrust towards Renewable Energy by

raising Renewable Energy capacity target to 175GW by 2022. NTPC recently got

approval to set up 15GW of grid-connected solar power projects under National

Solar Mission (NSM).

March 18, 2015

4

Initiating coverage | Action Construction Equipment

On the whole, considering Power PSUs’ capex and the EPC opportunity from

Power Gencos, we expect overall award activity to be northwards of ~`91,495cr

during 4QFY2015-FY2017E. For our calculation purpose, we have excluded EPC

works originating from both, Renewable Energy and Private Power Genco

Developers.

Irrigation & Water Treatment

Irrigation & Water Treatment also happen to be the focus area of the government.

This can be gauged from the following announcements in the Union Budget

FY2015-16E, (1) `1,000cr allocation towards “Pradhan Mantri Krishi Sinchayee

Yojna (PMKSY)” for assured irrigation, (2) `4,173cr budgetary allocation towards

Water Resources and Namami Ganga project (clubbed under other Ministry), and

(3) announcement on National River Linking Project (NRLP). Even though

budgetary allocation in the recent Union Budget was increased by 34.0% yoy to

`138cr, we expect higher state government spending and private sector

participation in irrigation to increase as some large ticket projects could be

implemented on PPP basis. We expect an opportunity northward of `6,104cr to

emerge from this vertical over FY2016-17E.

Railways

Recent announcements by the Railway Minister, like (1) allowing 100% FDI in select

sub-segments in Railways, (2) decentralization of tendering process, (3) rewarding

railway officers for delivering results (with 2% of the project value as incentives),

(4) increase in freight tariff rates, (5) willingness to modernize and upgrade

Railway resources through PPP route, (6) monetize idly lying land bank of Railways,

(7) increase dependency on Alternate energy, (8) shift in focus from announcement

of new trains in the Budget to improvement of existing train services, indicate

Railways Ministers intent to revive the ailing Indian Railways (IR).

In the Rail Budget FY2015-16, the Railways Minister announced that in the next

five years, IR would spend `856,000cr with focus on network decongestion and

expansion. As a first step, in order to arrange long-term financing, IR signed a

MoU with Life Insurance Corporation (LIC) to raise `150,000cr in the form of

bonds (on an average `30,000cr worth of bonds would be issued every year by

Railway entities).

Even though the above mentioned initiatives would not make IR efficient

immediately, but all these announcements are in the positive direction. In the

long-run, with a gradual improvement in the health of IR, we expect gradual uptick

in the Railway capex cycle. Till then IR would have to continue to depend on

government funding. The government in the Union Budget FY2015-16E increased

yoy allocation towards IR by 32.9% to `40,000cr. Again, if we look into the details,

`14,170cr would flow towards the new lines construction and RoB/RuB works

(reflecting 28.8% yoy increase). Notably, we have excluded award activity flowing

in from any of the PPP projects and new monetization avenues identified by the

Railways Ministry.

March 18, 2015

5

Initiating coverage | Action Construction Equipment

Exhibit 6: Railways Capex Cycle (` cr)

Particulars

FY2015- BE

FY2015- RE

FY2016- BE

(%)

New Lines (Construction)

8,569

8,984

12,830

42.8

Road Safety Work - RoB/RuB

2,287

2,017

1,340

(33.6)

Totals

10,856

11,001

14,170

28.8

Source: Indian Railways, , Angel Research

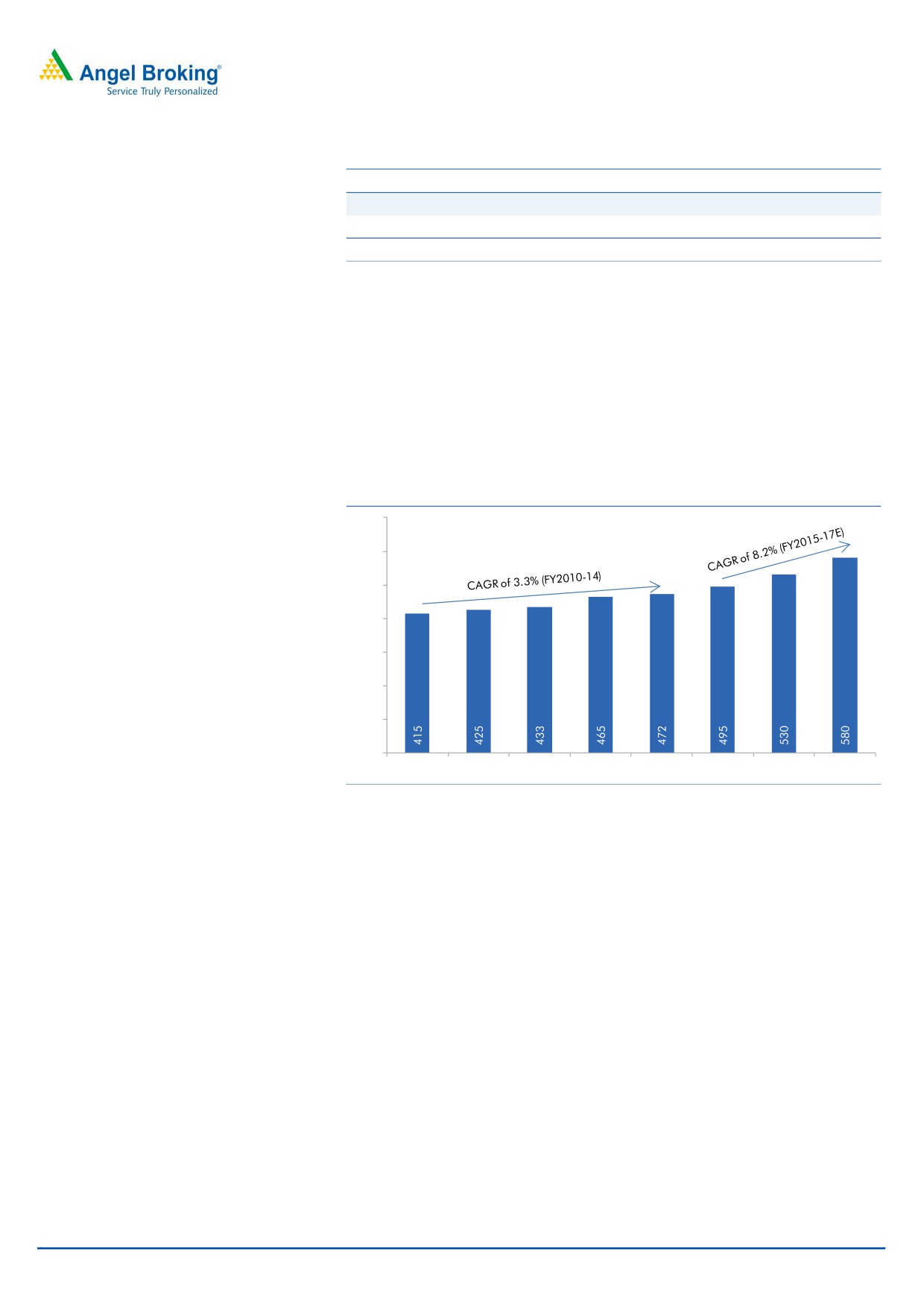

Coal Mining

Intending to tackle the fuel security issue, the government initiated (1) amends to

Mines & Mineral (Development and Regulation) bill, (2) re-auction/ auction of the

coal/ mineral resources, and (3) made favourable announcements to make

Thermal Power plants more efficient. The Government of India (GoI) has guided at

Coal India (accounts for over

80% of the domestic produce) doubling its

production from 494mn tonne in FY2014 to 1bn tonne by FY2020E.

Exhibit 7: Coal India Sales Volume (mn tn)

700

600

500

400

300

200

100

0

FY2010

FY2011

FY2012

FY2013

FY2014

FY2015E FY2016E FY2017E

Source: Company, Angel Research

With conclusion of Phase I and II coal block auctions, we expect coal production

from the private sector to increase from ~30mn tonne to ~60mn tonne in the next

1-2 years. Most of the coal blocks auctioned have all the clearances in place. On

the whole, we expect domestic coal production to see 115mn tonne of incremental

production during FY2016-17E. We expect `38,640cr worth of capex investments

to be made during FY2016-17E.

Urban Rail Transport

In the Union Budget FY2015-16, the government increased allocation towards

Metro Railway services for 11 cities, where either works are ongoing or are yet to

commence. We expect works across Ahmedabad, Nagpur, Lucknow and Mumbai

(expansion) to gain traction in FY2016-17E, whereas works across other cities

would commence in the next 3-5 years. We expect ~`16,000cr worth of Infra

award activity from this vertical to private players in the next 1-2 years (assuming

awarding from only these 4 cities).

March 18, 2015

6

Initiating coverage | Action Construction Equipment

Large Infra Projects- DFC & DMIC

The government’s focus on larger Infra projects (such as Dedicated Freight

Corridor [DFC]) and Delhi Mumbai Industrial Corridor [DMIC]) would also

contribute to the revival of Infra award activity.

DFC is a `120,000cr project covering ~3,300km, connecting Mumbai to Delhi on

the Western Corridor and Ludhiana to Kolkata on the Eastern Corridor. With more

than 80% of the land acquired, and majority of the clearances in place, award

activity would gain momentum across packages. These 2 corridors are expected to

commence operations in March 2018.

DMIC (Phase I) is a gigantic `540,000cr project, developed across the 1,500km

stretch on the Western corridors of DFC. Currently, land acquisition is going on at

Dholera, Shendra, and Pithampur stretches. Soon we expect civil works award

activity to commence.

On the whole, we expect awards to the tune of `174,400cr from these large ticket

Infra projects in the next 1-2 years.

Real Estate & 100 Smart Cities

The government has called for “Housing for all” by 2022, where it plans to build

6cr homes (4cr in rural and 2cr in urban areas). In line with its vision to have

Pucca house for everyone by

2022, the government in the Union Budget

FY2015-16, increased allocation under various ministries to `22,407cr. The

ambitious target set under “Housing for all” scheme translates to 85 lakh new

homes every year.

As per Cushman Wakefield report, new launches declined 12% yoy across top

8 cities (Ahmedabad, Bengaluru, Chennai, Delhi NCR, Hyderabad, Kolkata,

Mumbai Metropolitan and Pune) to 1.53 lakh housing units in CY2014, reflecting

weak absorption trends. Research firm RNCOS, predicts urban housing shortage

of 1.8cr units in 2012, which is expected to grow at a CAGR of 6.6% for the next

10 years till 2022. Considering the demand-supply mismatch, GDP revival, decline

in interest rates, and improvement in home-buyer affordability, we expect the Real

Estate sector to see strong growth in FY2017E.

The government announced the ‘100 Smart cities’ program, and as a first step,

city-wise task forces were identified for

3 cities viz Ajmer, Allahabad and

Visakhapatnam. Even though the Smart city program is a long-term play, we

expect increase in Civil and Real Estate works across these 3 cities in the next

2-5 years. On a whole, the Smart city Program opens up a huge window of

opportunity for Civil construction companies.

We have only considered the government spending targets, which in our view,

could open civil construction opportunity worth `14,565cr.

Manufacturing/ Industrial Capex

In order to understand how the Corporate Capex Cycle is likely to shape-up during

FY2016-17E, we studied the 110 widely tracked companies of the BSE 500 index.

Based on Bloomberg consensus estimates, capex spends during FY2016-17E for

these companies are expected to be northward of ~`450,000cr.

On the whole, we expect Infrastructure spending to pick-up, led by government

spending. With government increasing emphasis on Roads & Highways and Urban

Infra verticals, we expect Industrial Capex cycle to join the race soon.

March 18, 2015

7

Initiating coverage | Action Construction Equipment

CE market to report strong growth

With slow-down in the Infra capex cycle, as per Off Highway Research estimates,

CE Industry sale volumes also witnessed 15.0% yoy decline in FY2012 and 8.8%

yoy decline in FY2013.

Exhibit 8: CE Industry Sale Volumes

80,000

50.0

45.0

70,000

40.0

60,000

30.0

50,000

22.0

20.0

40,000

10.0

8.4

30,000

-

20,000

(8.8)

(10.0)

10,000

(11.0)

(15.0)

0

(20.0)

FY2009

FY2010

FY2011

FY2012

FY2013

FY2014

CE Sales (Unit volumes)

yoy growth (%)

Source: Off Highway Research, Angel Research

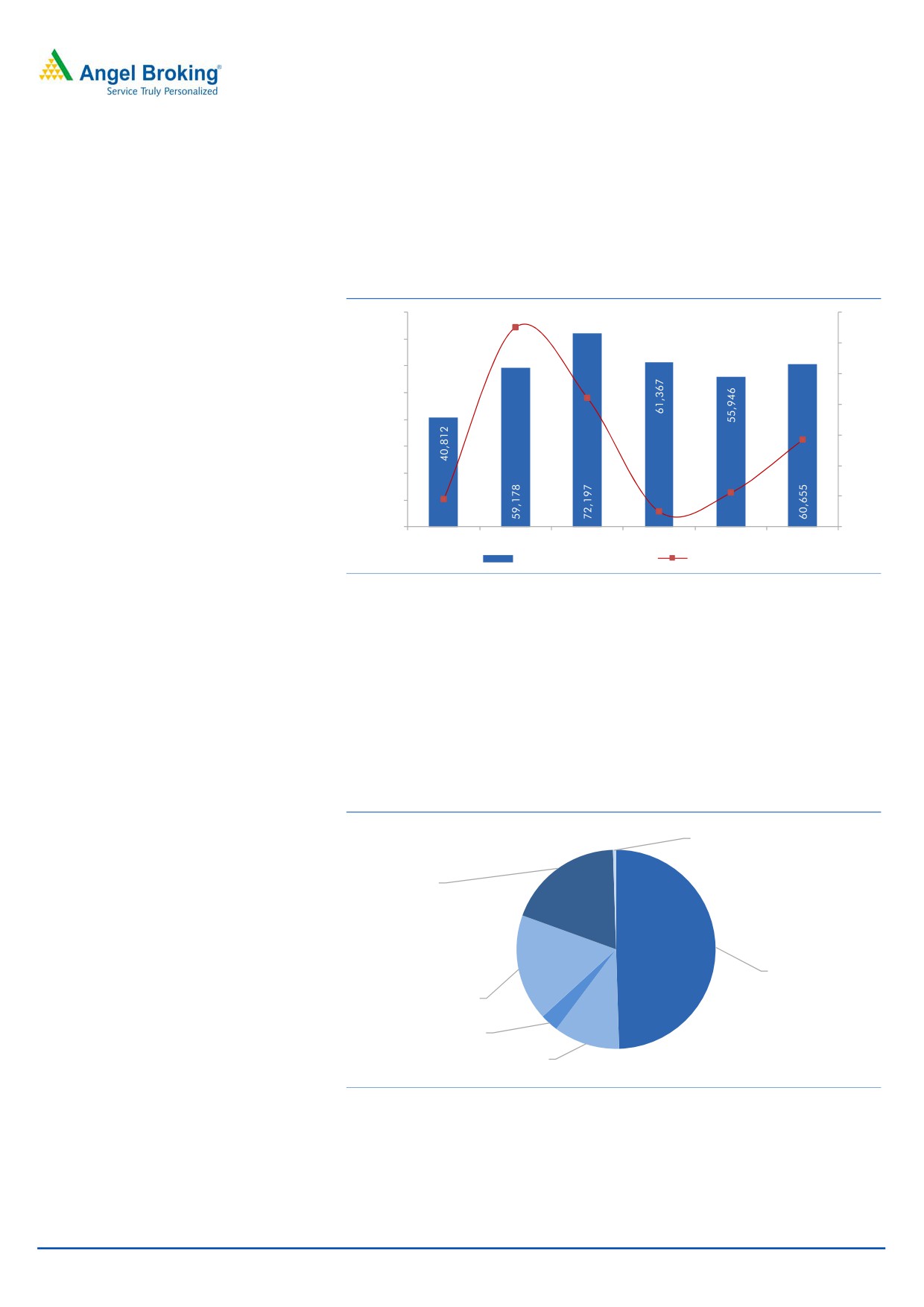

As per Off Highway Research estimates ~60,655 CEs were sold in FY2014,

reflecting 8.4% yoy growth. Of the total FY2014 CE sales, 49.5% were Backhoe

Loaders, followed by Crawler Excavators (accounting for 19.0% of CE sales), and

Mobile Cranes (accounting for 10.7% of CE sales). Again, if we split the Mobile

Cranes market, then Pick and Carry Cranes accounted for 86% of the total

volumes. The remaining domestic Mobile Crane market was constituted by

Crawler Cranes, Truck Mounted Cranes and Rough Terrain Cranes.

Exhibit 9: CE Industry Sale Volumes (FY2014)

Motor Graders,

Total of 60,655 CE

0.5%

units sold in FY2014

Crawler

Excavators, 19.0%

Backhoe Loaders,

49.5%

Others, 17.3%

Wheeled Loaders,

3.0%

Mobile Cranes,

10.7%

Source: Off Highway Research

The above table clearly highlights that a major chunk of the Indian CE market in

FY2014 was constituted by Earthmoving and Road Construction Equipments.

March 18, 2015

8

Initiating coverage | Action Construction Equipment

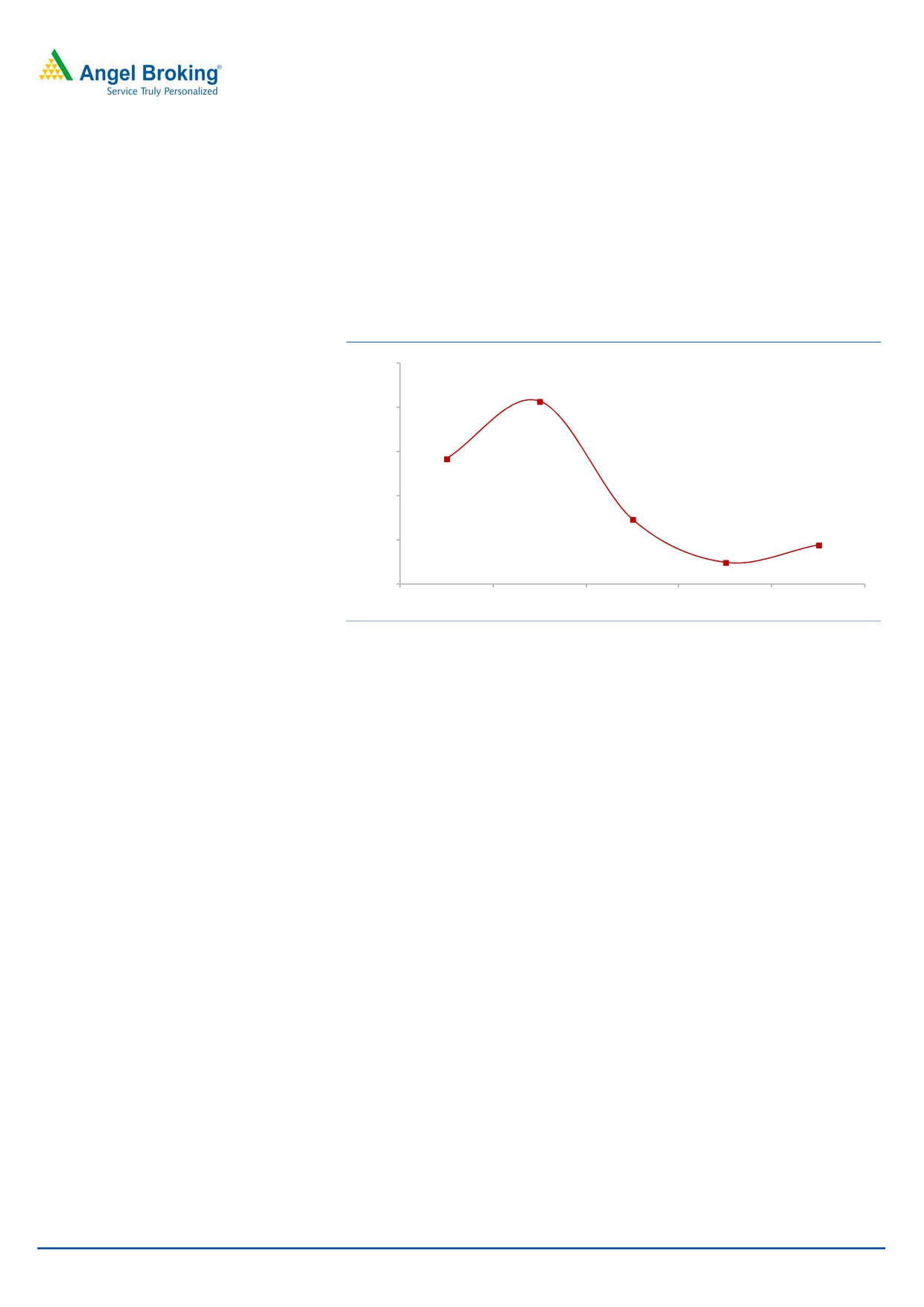

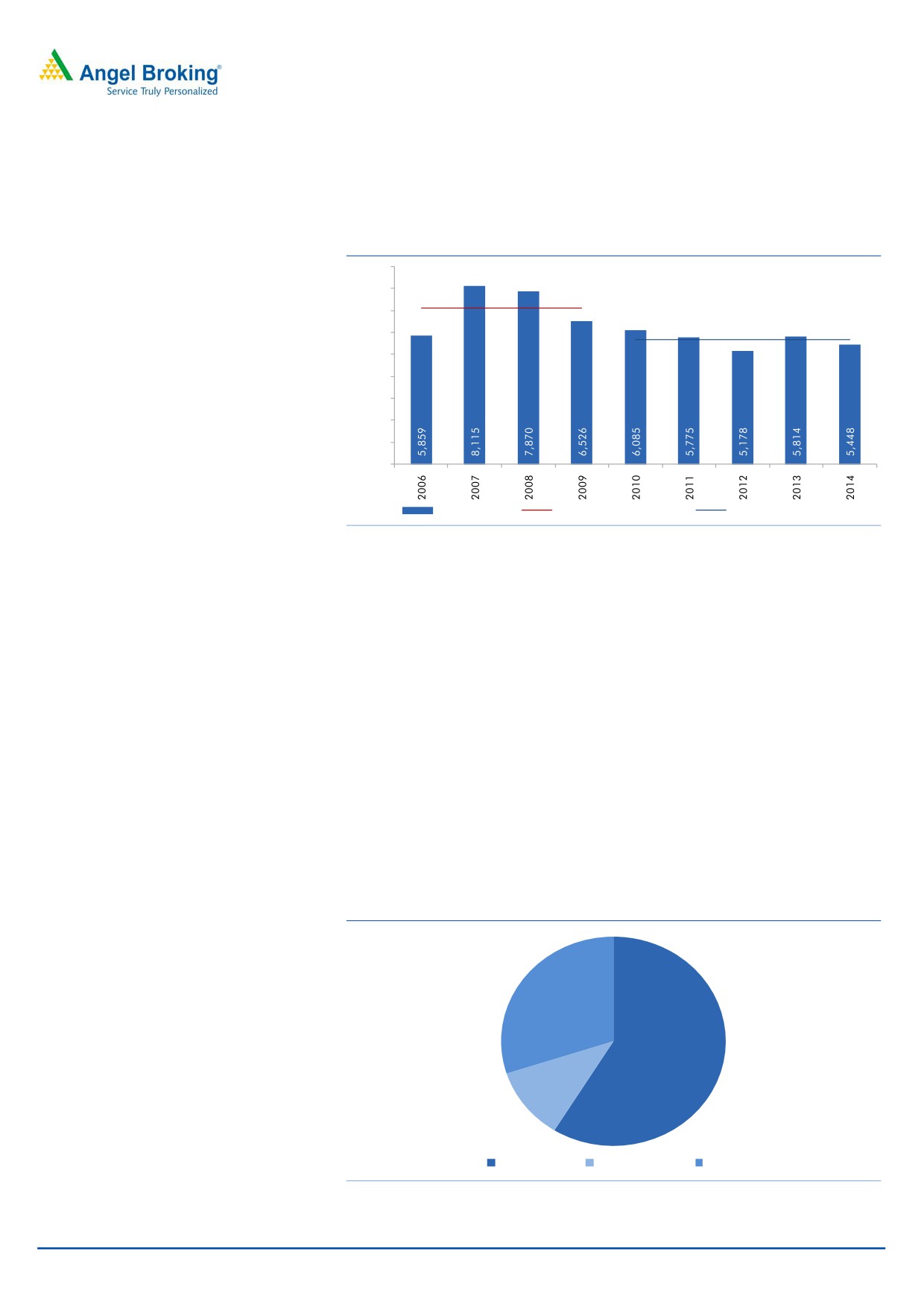

In line with the CE industry volumes, which have seen de-growth, industry level

Pick-n-Carry crane volumes also reported de-growth. Average sale volumes for the

industry declined from 7,092 units (in FY2006-09) to 5,860 units (in FY2010-14).

Exhibit 10: Pick-n-Carry Cranes Industry Volumes

9,000

FY06-09 avg. sales: 7,092

8,000

7,000

FY10-14 avg. sales: 5,860

6,000

5,000

4,000

3,000

2,000

1,000

0

Yrly. Sale Vol.

Avg. Sale Vol. (FY06-09)

Avg. Sale Vol. (FY10-14)

Source: Company, Angel Research

With government emphasizing increased spending towards Roads & Highways and

Urban Infra verticals, we are optimistic that Infra capex cycle would pick-up from

here on. Higher Infrastructure spending in our view would lead to multiplier effect

on the entire CE sector. ACE being a market leader in the Pick-n-Carry Cranes space,

would resultantly benefit from such government focus on the infrastructure sector.

ACE to gain from CE market revival

Having set its foot-hold successfully in the domestic Cranes market, at a time when

GDP was growing over

8%, ACE in FY2008-09 diversified in to MH and

Agri-Equipments (especially Tractors) business. In FY2011-12, ACE went for

aggressive capacity expansion across sub-verticals. Since completion of the capex,

end-user Infra industry experienced a sharp slowdown, as it grappled with various

structural issues related to land acquisition, getting requisite clearances and project

funding. As a result the entire CE industry witnessed a sharp de-growth in business

and ACE was no exception to it.

Exhibit 11: Segment-wise Revenue mix (FY2014)

FY14 Revenues

(`614.9 cr)

30%

59%

11%

Cranes

MH & CE

Agri Equip.

Source: Company, Angel Research

March 18, 2015

9

Initiating coverage | Action Construction Equipment

Starting as a Crane manufacturer, over the years, ACE diversified in to MH and

Tractors business. ACE in FY2014 reported a major 59% of its sales from Cranes

segment with a majority of the sales being accounted by Pick-n-Carry cranes. The

MH&CE segment contributed 11% of revenues, where revenues from Forklifts were

a major contributor at the segment level. The Agri Equipments segment contributed

30% to total sales, mainly led by tractors.

Notably, ACE enjoys strong market positioning in the domestic Pick-n-Cary Cranes

market (with 35% market share) and Forklifts market (with 18% market share). We

expect the company to be able to maintain its market share across these

2

categories, as the overall pie is likely to see sharp growth. In addition to Pick and

Carry cranes, ACE also manufactures Self Erecting Mobile cranes used in

construction of buildings up to 4/5 floors, and Fixed Tower cranes which are used

in the construction of high-rise buildings.

With outlook for the entire CE industry expected to improve, we are optimistic that

both, Crane and MH-CE segment sale volumes for ACE would catch-up from here

on. Even though many new players, especially MNCs, have entered Indian markets

in the last few years, the current unfavorable USD-INR rates make imports costlier.

Hence, foreign competition may not be a threat to the domestic players’ growth

outlook.

Further, with revival in the Construction sector, we expect a majority of the

Construction companies to first put their idly lying Construction Equipments into

use and then pursue CE purchases. We therefore expect domestic CE players’ sale

volumes to report strong growth from FY2017E onwards. On the backdrop of

sharp catch-up in demand, despite increased competition across segments, we

expect ACE to maintain its current market share.

Exhibit 12: ACE Market Positioning

Segment

Market

Equipment Type

Competitors

Application

Type

Share (%)

Cranes

Supports equipment in construction projects;

Pick n Carry Crane

35

Escorts, TIL, Indo Farm

Lift and move Stone slabs for realty projects

Crawler Cranes

ND

Tata-Hitachi, Escorts

Power, Industrial & Infra projects

Fixed Tower Cranes

ND

Potain, Escorts

High Rise Buildings

MH & CE (Material Handling & Other Construction Equipments)

JCB, BEML, Escorts,

Backhoe Loaders/ Wheeled Loaders

1

Load-Unload, Move, Erect Aggregates

Tata-Hitachi

To lift and stack material in Manufacturing/

Forklifts

18

Godrej, Voltas (Kion), Toyota

Logistics/Warehousing units

Road Compactors

ND

Escorts, JCB, L&T Komatsu

Used mainly for Road Construction

Agri Equipment

Tractors

1

M&M, Escorts, Tafe

Farming purposes

Hind Agro, CLASS, John

Harvesting of grain crops (mainly Paddy &

Harvesters

2

Deere

Wheat)

Source: Company, Angel Research; Note: Market share calculated on Volume basis, ND- Not Determined

March 18, 2015

10

Initiating coverage | Action Construction Equipment

Business segments set to revive

On ACE’s expanded capacity base, slowdown in overall Infrastructure spending

led to 24.3% and 25.9% (CAGR) volume de-growth during FY2012-14 across

Cranes and MH-CE business segments, respectively. This de-growth across

business segments reflect lower utilization levels and decline in overall asset-

turnover ratios (from 3.9x in FY2012 to 1.9x in FY2014), which further translated

to a decline in the EBITDA margin (from 6.0% in FY2012 to 3.9% in FY2014) and

Net margins (from 3.2% in FY2012 to 0.7% in FY2014).

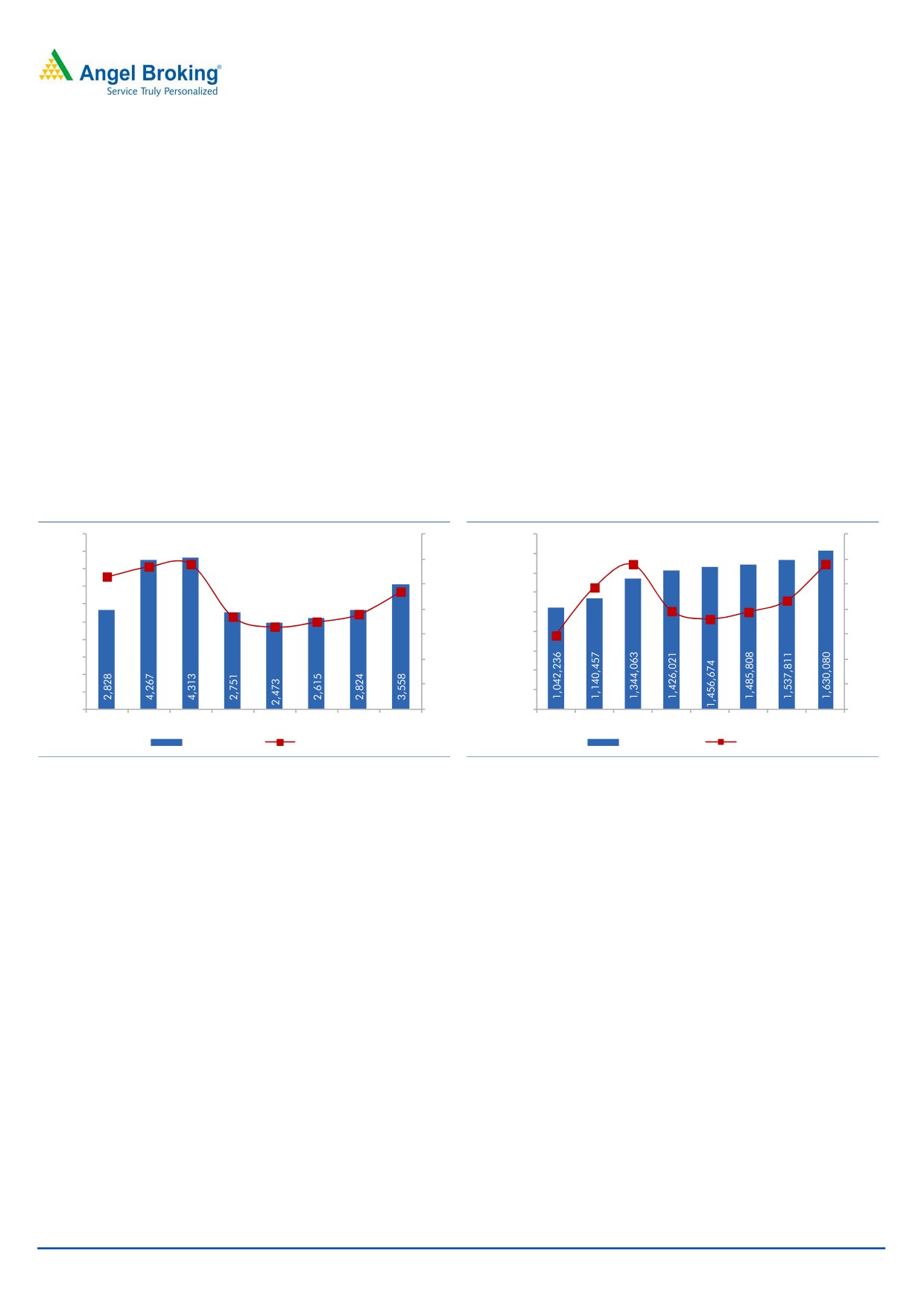

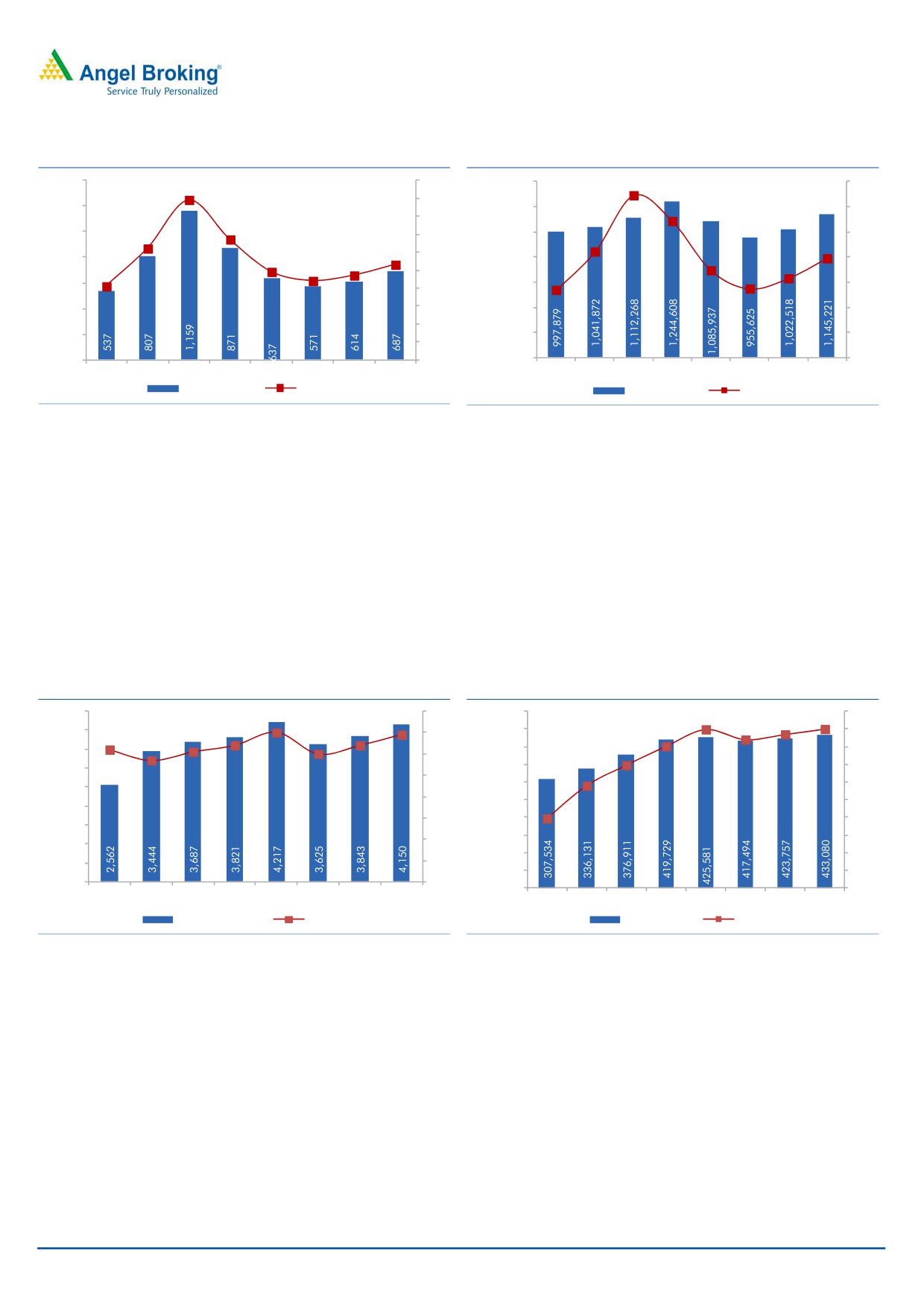

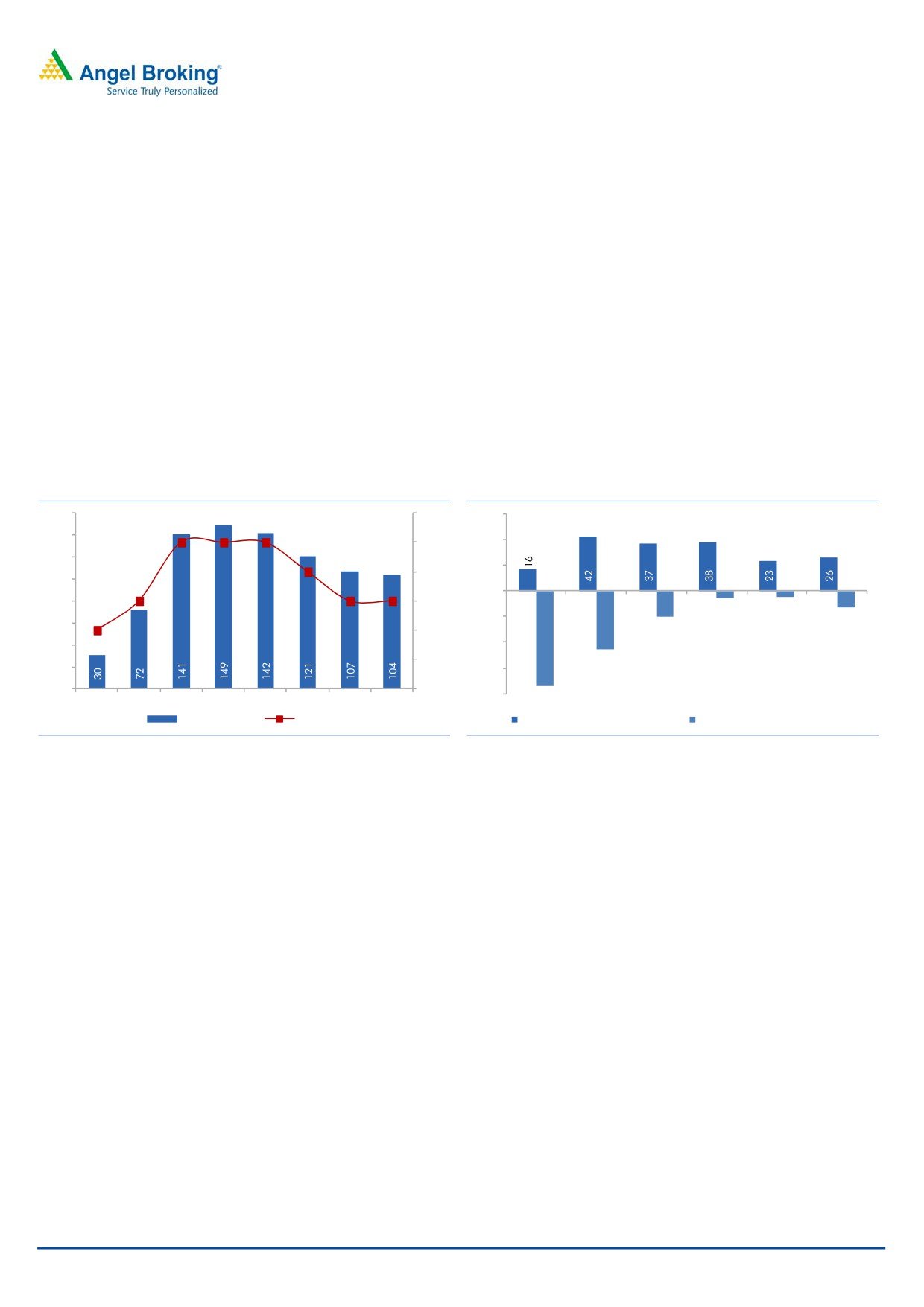

Strong volumes to drive Crane segment sales

We expect the Cranes segment to report a

16.7% volume CAGR during

FY2015-17E to 3,558 units. On the backdrop of demand revival and higher

realization, we expect the Cranes segment sales to report a 22.2% CAGR during

FY2015-17E to `580.1cr.

Exhibit 13: Crane Volumes & Utilization (%)

Exhibit 14: Crane Realization & Sales (` cr)

5,000

58

70

1,800,000

700

580

434

580

4,500

57

360

389

53

60

1,600,000

392

600

47

4,000

1,400,000

487

3,500

50

500

1,200,000

295

37

38

3,000

35

33

40

1,000,000

400

2,500

30

800,000

300

2,000

600,000

1,500

20

200

1,000

400,000

10

100

500

200,000

0

0

0

0

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

Crane Vol.

Utilization (%)

Blended Real.

Sales (` cr)

Source: Company, Angel Research

Source: Company, Angel Research

Road CE growth rate to outpace that of MH

At its peak, ACE sold ~850 Forklift units (reflecting 106.3% capacity utilization) in

FY2012. Recent reform announcements, expectations of GDP revival and

government’s increased thrust towards Warehouse and Logistics sector, strengthen

our view that long-term demand for Forklifts would catch-up from here on. Being a

top 3 player, and with industry expected to report strong growth, we expect ACE to

benefit. With demand revival, we expect ACE to increase Forklift prices.

We expect segment volumes to report 9.7% CAGR during FY2015-17E to 687

units. Of the total 637 units sold in FY2014, 530 were Forklifts (66.3% utilization)

and the remaining 107 were Road Construction & Other Construction Equipments

(21.4% utilization). We expect the rate of growth of Road CE to outpace Forklift

growth rate, going forward.

ACE currently reports sales of Forklifts, Backhoe Loaders, Wheeled Loaders, Road

Compactors and Motor Graders under the MH and CE segment. On the whole,

uptick in Forklift prices and shift in product mix (with higher contribution from Road

CEs, which have high realization), lead us to assume the segment to report a

20.1% CAGR in sales during FY2015-17E to `78.7cr.

March 18, 2015

11

Initiating coverage | Action Construction Equipment

Exhibit 15: MH&CE Volumes & Utilization (%)

Exhibit 16: MH&CE Blended Realization & Sales (` cr)

1,400

89

100

1,400,000

129

140

108

90

1,200

1,200,000

79

120

80

84

69

63

67

54

55

1,000

62

70

1,000,000

100

53

49

60

800

47

800,000

80

44

41

50

600

600,000

60

40

400

30

400,000

40

20

200

200,000

20

10

0

0

0

0

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

MH & CE Vol.

Utilization (%)

Blended Real.

Sales (` cr)

Source: Company, Angel Research

Source: Company, Angel Research

Entry into new geographies to drive Agri-Equipment volumes

Since its entry in the domestic tractors market 4-5 years back, ACE has tasted

success with the launch of 35hp, 45hp and 50hp tractors. The states of Punjab,

Haryana and Uttar Pradesh account for a majority of ACE’s tractor sales. ACE, in

FY2015, embarked upon a geographical expansion strategy, wherein it entered

Gujarat, Jharkhand, Bihar, Maharashtra and Tamil Nadu. The full benefits of entry

into the new geographies are to be accrued in the mid-to-long run. Tractor sales

currently account for ~70% of Agri-Equipment division’s sales, while harvesters

account for the balance ~30%.

Exhibit 17: Agri Volumes & Utilization (%)

Exhibit 18: Agri Blended Realization & Sales (` cr)

4,500

69

80

500,000

180

180

200

70

174

168

4,000

61

64

64

450,000

180

62

70

160

60

57

400,000

139

160

3,500

60

116

350,000

140

3,000

50

300,000

120

2,500

40

250,000

79

100

2,000

30

200,000

80

1,500

150,000

60

20

1,000

100,000

40

500

10

50,000

20

0

0

0

0

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

Agri. Equip. Vol.

Utilization (%)

Blended Real.

Sales (` cr)

Source: Company, Angel Research

Source: Company, Angel Research

Given that tractor and harvester sales in India are highly dependent on rainfall

and rural spending power, we have modeled a 9.0% top-line CAGR for this

segment over FY2015-17E to `179.7cr.

Market penetration efforts, new launches, to scale up business

ACE, over the years, has added new products and variants, with different

capacities and power, to its product portfolio. Also, since 2010, the company has

been investing in building a strong distribution network. The sales network of ACE

has increased from ~80 distributors in FY2010 to ~200 distributors by mid-

FY2015. Widened range of product offerings coupled with their wide sales network

should help ACE scale its business from here on. ACE’s Research & Development

March 18, 2015

12

Initiating coverage | Action Construction Equipment

(R&D) team is working on developing (1) Skid-Steer Loader, (2) Truck Mounted Full

Slew cranes with different capacities, (3) Crawler cranes (varied capacities), (4) Self

propelled Truck Mounted cranes, (5) Power Tillers, and (6) new variants of

Harvesters, amongst others. In absence of launch dates for these products, we

have not modeled any growth from these launches.

Exhibit 19: Standalone Revenues (` cr) & yoy change

Exhibit 20: Sales Network

900

60

70

250

800

60

700

50

200

40

600

27

23

30

500

150

11

20

400

10

(3)

300

(8)

100

0

200

-10

(22)

100

-20

50

0

-30

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

0

Revenues (` cr)

y/y change (%)

FY10

FY11

2HFY15

Source: Company, Angel Research

Source: Company, Angel Research

Higher Utilization to drive FY2015-17E sales

Increase in capacity utilization levels across the Cranes (from 33% in FY2014 to

47% in FY2017E) and MH and CE segments (from 49% in FY2014 to 53% in

FY2017E) should help ACE report a decent top-line growth. This coupled with

realization growth across all 3 segments should help ACE report an 18.8% top-line

CAGR over FY2015-17E to `838.5cr.

Cost rationalization, weak RM prices to aid Margin expansion

Hit by infra capex cycle slowdown, ACE in the last few quarters initiated cost cutting

measures. Till a few quarters back, ~90% of Forklift manufacturing was done

using imported inputs, which has now been brought down to ~40%, thus

indicating that ~60% of Forklift manufacture is now localized. The Management

highlighted on attaining scale; it would allow further localization, which in turn

could further lower import costs. This strategy lowers dependency on import,

thereby alleviating ACE from any forex risk. Imported raw materials in FY2014

accounted for 21% of the reported raw material costs. We expect this ratio to

decline to 19.3% by FY2017E.

Exhibit 21: Raw Material Exp. & RM as % of sales

Exhibit 22: Raw Mat. Exp. split - Domestic & Imports (%)

800

84.0

120

81.8

700

78.5

82.0

100

80.3

80.0

80.0

600

79.5

80.0

80

500

76.9

78.0

400

60

75.3

75.0

76.0

300

40

74.0

200

20

100

72.0

0

70.0

0

FY09

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

FY09

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

Raw Material Exp.

Raw Material as % of Sales

Domestic Raw Material Exp.

Imported Raw Material Exp.

Source: Company, Angel Research

Source: Company, Angel Research

March 18, 2015

13

Initiating coverage | Action Construction Equipment

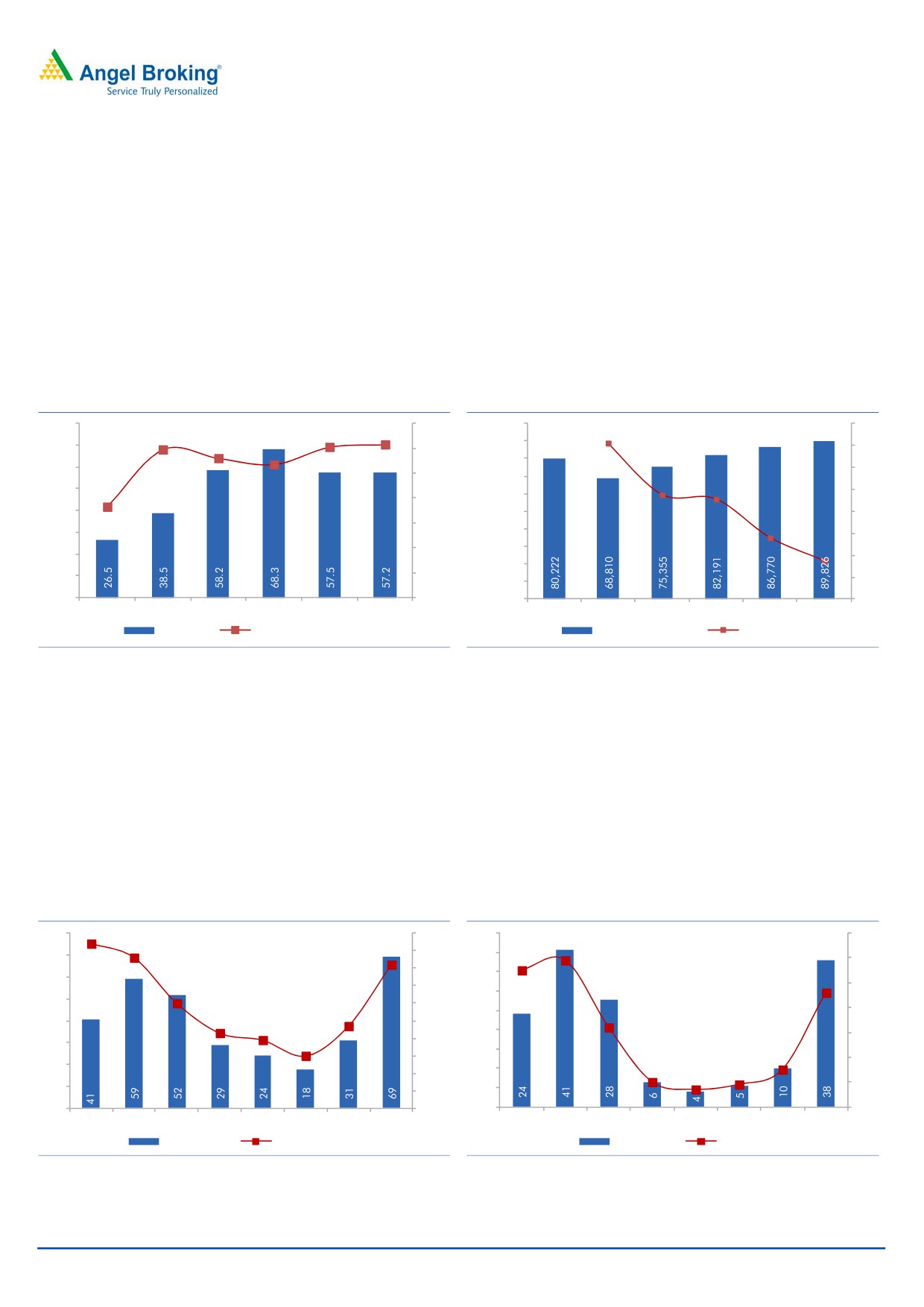

Till now, ACE has been procuring engines for all of its business segments from

companies like Simpson, Mahindra Navstar, and Kirloskar, among others. In order

to further cut down costs, ACE backed by its 80-90-member R&D team, has started

making in-house engines for its tractors. By January 2015-end, ACE got in place a

Central Pollution Control Board (CPCB) clearance for manufacturing tractor

engines. The Management expects to save ~`15,000 per tractor by using in-house

developed engines. ACE is also working on engines for its other products, ie Motor

Grader, Wheel Loader, Mini Compactor, Cranes, and other CEs. The Management

highlighted that if the company tastes success with the in-house engines currently

used in tractors, then it could extrapolate the use of in-house engines across other

products as well. We have not modeled the same into our estimates.

Exhibit 23: Engines cost (` cr) & as % of Raw Mat. Exp.

Exhibit 24: Engine cost & As % of Raw Material Exp.

80.0

14.0

100,000

16

12.1

12.3

14.2

11.9

5.6

3.5

11.2

10.7

90,000

9.1

70.0

12.0

14

80,000

9.5

60.0

12

10.0

70,000

50.0

7.3

10

60,000

8.0

40.0

50,000

8

6.0

30.0

40,000

6

4.0

30,000

20.0

4

20,000

10.0

2.0

2

10,000

0.0

0.0

0

0

FY09

FY10

FY11

FY12

FY13

FY14

FY09

FY10

FY11

FY12

FY13

FY14

Engine Cost

As % of Raw Material Exp.

Blended Engine Cost

yoy change

Source: Company, Angel Research

Source: Company, Angel Research

Mild Steel is a major raw material (accounting for 25-35% of the total raw material

cost) item used for manufacturing all types of equipments. Our Metals sector

analyst is of the view that domestic steel prices are likely to be under pressure over

FY2016-17E. This could result in cost savings for the company and in turn

contribute to our margin expansion assumption.

Already, results of some of the floor level cost cutting initiatives are evident, as

operating expenses in the last 12 months declined 10.9% yoy in comparison to just

2.0% yoy decline in sales. We are of the view that demand recovery should support

our margin expansion assumption.

Exhibit 25: Standalone EBITDA & EBITDA Margin

Exhibit 26: Standalone PAT & PAT Margin

80

9.4

10.0

45

7.0

8.6

5.9

8.2

9.0

4.6

70

40

5.5

6.0

6.0

8.0

35

60

7.0

5.0

30

3.2

50

6.0

4.7

25

4.0

4.3

40

3.9

5.0

20

3.0

3.0

4.0

30

15

1.5

3.0

2.0

20

10

1.0

0.9

2.0

0.7

1.0

10

5

1.0

0

0.0

0

0.0

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

EBITDA (` cr)

EBITDA Margin (%)

PAT (` cr)

PAT Margin (%)

Source: Company, Angel Research

Source: Company, Angel Research

March 18, 2015

14

Initiating coverage | Action Construction Equipment

Operating leverage to trickle down to PAT level

Considering (1) benefits of cost cutting measures initiated earlier, (2) higher

emphasis on localization of Forklift manufacture, (3) lower Mild Steel prices

assumption; when coupled with demand recovery suggest that ACE is poised for a

sharp 522bp EBITDA margin expansion over FY2015-17E to 8.2%. We expect the

operating leverage to result in a strong 97.2% EBITDA CAGR over FY2015-17 to

`68.7cr. Notably, we have not modeled any savings resulting from ACE pursuing

in-house engines manufacturing.

With no capex lined-up (except maintenance capex), and ACE expected to

generate `87cr of cash flow from operations during FY2015-17E, we expect ACE

to reduce its debt partially. Accordingly, we expect debt and interest expenses to

decline from FY2014 levels. For 9MFY2015 ACE reported a 36.3% yoy decline in

depreciation expenses to `7.2cr, as (1) the depreciation policy was changed to

meet amended Companies Act requirements and (2) the company sold one of its

major assets. However, we have assumed aggressive depreciation numbers for

FY2016 and FY2017 at `13cr and `14cr, respectively. Sale of the major asset led

ACE report `6.5cr of profit from sale of asset in 3QFY2015 (of the reported other

income of `7.5cr). As a result, Other Income numbers for FY2015 will look higher

at ~`11cr. We have assumed `5cr and `4cr of other income for FY2016E and

FY2017E. ACE is expected to be subjected to an effective tax rate of 22-23% for

FY2015-17E, on account of 200% deduction on their approved R&D centre. We

have assumed a 23% effective tax rate for FY2015-17E.

On the whole, strong EBITDA growth coupled with (1) decline in interest expenses,

and (2) lower effective tax rate assumption of 23%, translate to an 170.0% PAT

CAGR over FY2015-17 to `38.3cr.

Well positioned to move to the next growth level

ACE last pursued capacity expansion in FY2011-12. With slowdown in the infra

capex cycle; Cranes, CE and MH division plants have been running at sub-50%

capacity utilization levels. Given the smaller base, and presence only in lower

engine capacity tractors, the Agri-division (mainly led by tractors) has been

operating at 70% capacity levels. The Management highlighted that it does not

need to pursue any major capex until their revenues cross `1,200cr. With a revival

on the cards, expected improvement in utilization levels, and with minimal

requirement for incremental capital investments, we see ACE well positioned to

scale its business quickly.

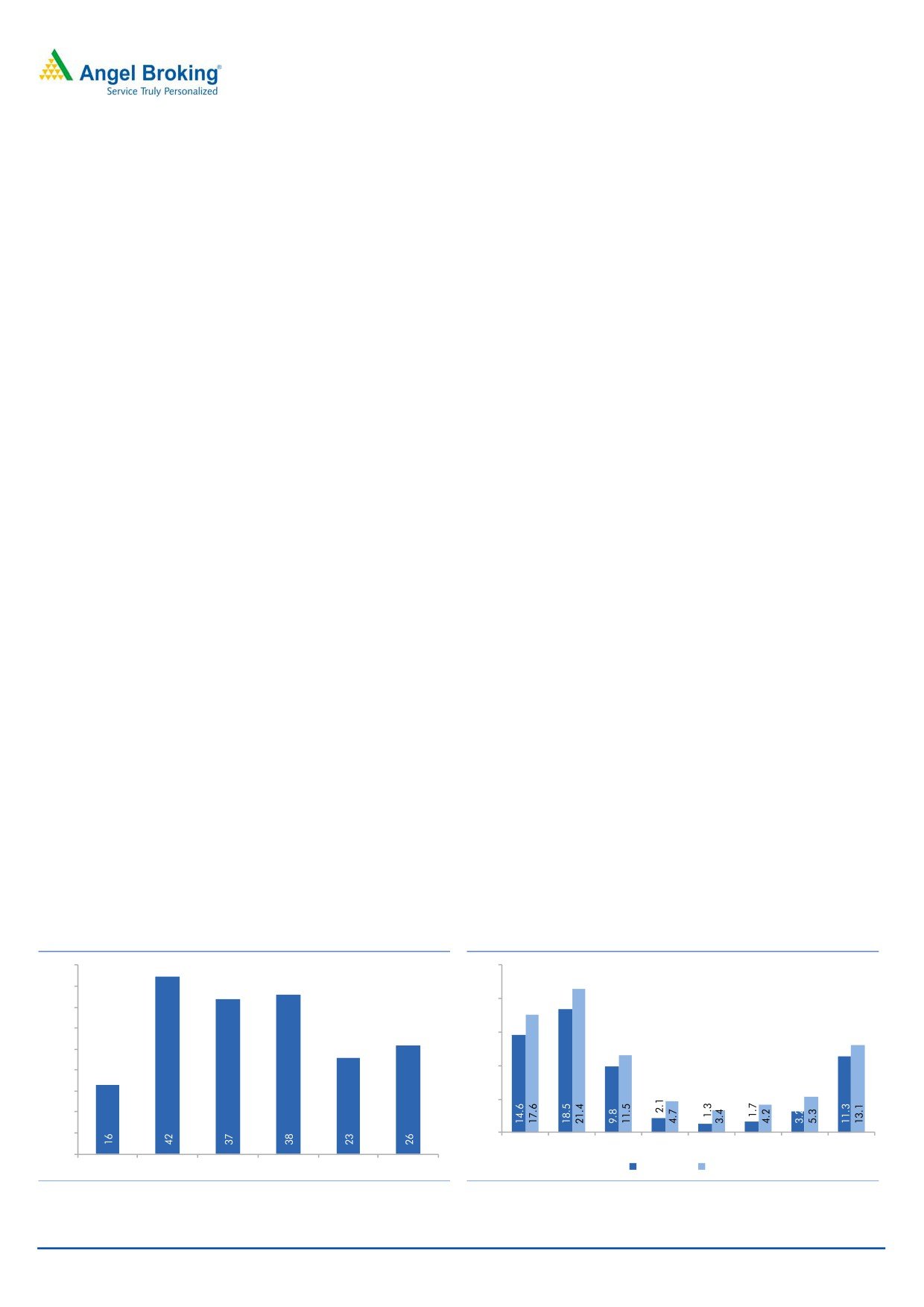

Exhibit 27: Cash flow from Operations (` cr)

Exhibit 28: RoE & RoCE

45

25

40

20

35

30

15

25

10

20

15

5

10

5

0

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

0

FY12

FY13

FY14

FY15E

FY16E

FY17E

RoE (%)

RoCE (%)

Source: Company, Angel Research

Source: Company, Angel Research

March 18, 2015

15

Initiating coverage | Action Construction Equipment

We expect ACE to generate `87cr of cash flow from operations during FY2015-

17E, which could be used to partly repay debt and partly re-invest back into the

business. In-line with the strong growth in profitability and improved cash flow

generating potential, the RoEs should improve from 1.7% in FY2015E to 11.3% in

FY2017E.

D/E ratio to decline

Despite the severe slowdown in CE cycle, after ACE having pursued its last round

of capex in FY2011-12, ACE has been able to maintain its D/E ratio within comfort

levels.

ACE’s D/E ratio stands at 0.4x and its business model has the potential to generate

over `87cr of cash flow from operations over FY2015-17E. Hence, we are

comforted about the company’s future growth prospects, which would come with

minimal capital requirement.

Exhibit 29: Debt (` cr) and D/E ratio (x)

Exhibit 30: CFO & CFI (` cr)

160

0.5x

0.6x

60

0.5x

0.5x

140

40

0.5x

0.4x

120

0.3x

0.3x

20

0.4x

100

0.3x

0

80

0.3x

FY12

FY13

FY14

FY15E

FY16E

FY17E

0.2x

(20)

60

(5)

(13)

0.2x

(20)

(6)

40

(40)

0.1x

(45)

20

(60)

0

0.0x

(80)

(73)

FY10

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

Debt (` cr)

D/E ratio (x)

Cash flow from Operations (` cr)

Cash flow from Investing (` cr)

Source: Company, Angel Research

Source: Company, Angel Research

With uptick in the infra-capex cycle, we expect the working capital cycle days to

decline from 69 days in FY2014 to 51 days in FY2017E. This could be on

expectation of lower debtor as well as inventory days. A squeeze in working capital

days and strong profitability growth should help ACE report `87cr of cash flow

from operations during FY2015-17E. We expect ACE to deploy cash flow

generated from operations towards (1) maintenance capex of `20cr in FY2016

and `21cr in FY2017, and (2) towards debt repayment of `17cr during FY2015-

17E. Accordingly, we expect the D/E ratio to slightly decline to 0.3x by FY2017E.

Risks to Our Estimates

Any further delays in infra capex cycle recovery from here on could be a big

risk to our estimates.

Loss of market share vs. our assumption of holding market share could be a

risk to our assumptions.

Any sharp appreciation in the Rupee (INR) could make CE imports lucrative,

thereby increasing competition, which again could be a threat to our

estimates.

Any increase in raw material prices from here on would be a risk to our

margin expansion assumption and our estimates.

March 18, 2015

16

Initiating coverage | Action Construction Equipment

Valuation

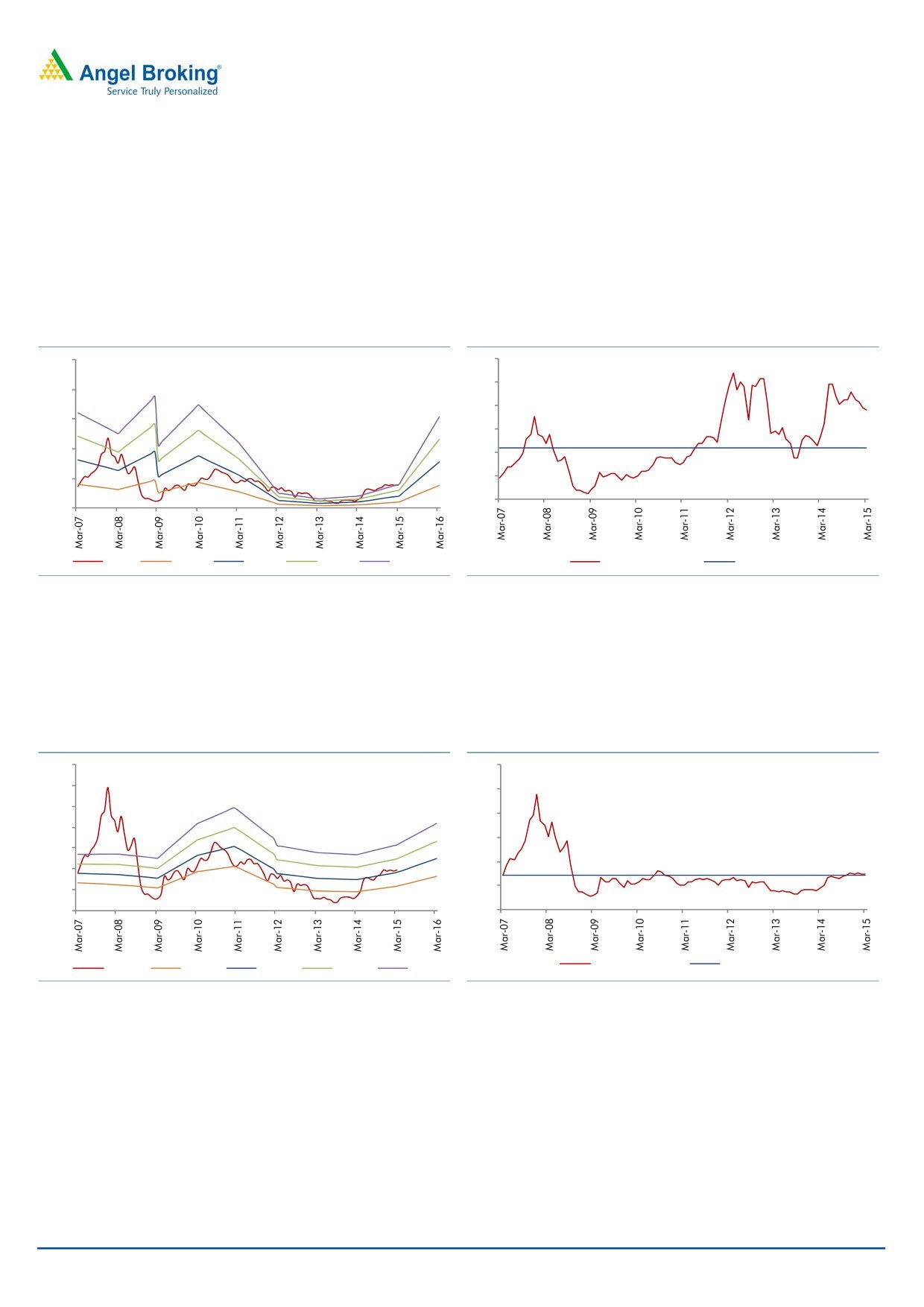

At the current market price of `42/share, ACE is trading at FY2016E and FY2017E

P/E multiple of 41.1x and 10.9x, respectively. Historically, since the time of listing

(January-2007), ACE’s stock has traded at a 1-year forward P/E multiple of 24.3x.

The earnings growth of the company has been volatile and the street has always

built higher earnings growth expectation from ACE. This has led ACE’s stock to

trade at higher valuations.

Exhibit 31: 1-year forward P/E band

Exhibit 32: 1-year forward P/E (x)

250

60

50

200

40

150

30

100

20

50

10

0

0

Price

10.0x

20.0x

30.0x

40.0x

1-yr Fwd PE (x)

Avg. PE

Source: Company, Angel Research

Source: Company, Angel Research

Given that ACE is more of a turnaround story, we did a check to assess whether

the assigned target P/E multiple justifies the target price. ACE’s stock is alternatively

trading at FY2016E and FY2017E EV/sales multiple of 0.8x and 0.6x, respectively. We

assign a multiple of 0.75x to our target FY2017E EV/sales to arrive at a FY2017E based

price target of `54/share. This translates into FY2017E based implied P/E multiple of 14.0x.

Exhibit 33: 1-year forward EV/Sales band

Exhibit 34: 1-year forward EV/Sales (x)

140

3.0

120

2.5

100

2.0

80

1.5

60

1.0

40

20

0.5

0

0.0

1-yr Fwd EV/Sales

Avg. EV/Sales

Price

0.5x

0.7x

0.9x

1.1x

Source: Angel Research

Source: Angel Research

We are optimistic that ACE would be able to maintain its numero uno position in

the domestic Pick and Carry cranes business. This, when coupled with a wide

range of product offerings, wide pan-India distribution network, along with their

recent cost cutting initiatives, comforts us. We estimate ACE to report an 18.8%

and 170.0% top-line and bottom-line CAGR, respectively, during FY2015-17E.

Accordingly, we expect the RoE to improve from 1.3% in FY2014 to 11.3% in

FY2017E. At the backdrop of sharp growth in profitability and RoE expansion, we

assign 14.0x P/E multiple to our FY2017E EPS estimate of `3.9/share to arrive at a

price target of `54. Given the 28.4% upside in the stock from the current levels, we

initiate coverage on the stock with a BUY rating.

March 18, 2015

17

Initiating coverage | Action Construction Equipment

Profit and Loss Statement

Y/E March (` cr)

FY11

FY12

FY13

FY14

FY15E

FY16E

FY17E

Net Sales

694

856

668

615

594

660

839

% Chg

59.8

23.4

(21.9)

(7.9)

(3.3)

11.0

27.1

Total Expenditure

634

804

639

591

577

629

770

Cost of Raw Mat. Consumed

476

667

530

491

475

522

656

Purchase of Stock-in-trade

47

33

5

1

2

2

3

Employee benefits Expense

33

45

49

46

48

52

58

Other Expenses

79

59

56

52

52

53

53

EBITDA

59

52

29

24

18

31

69

% Chg

46.2

(13.1)

(43.9)

(16.6)

(26.8)

74.7

122.6

EBIDTA %

8.6

6.0

4.3

3.9

3.0

4.7

8.2

Depreciation

7

11

14

15

10

13

14

EBIT

52

40

15

9

8

18

54

% Chg

65.9

(23.2)

(61.9)

(42.2)

(12.2)

129.7

204.2

Interest and Fin. Charges

4

7

10

10

12

10

8

Other Income

5

5

5

7

11

5

4

PBT

54

37

10

5

7

13

50

Tax

14

10

4

1

2

3

11

% of PBT

25.3

26.4

37.3

21.4

23.0

23.0

23.0

PAT before Exceptional item

41

28

6

4

5

10

38

Exceptional item

0

0

0

0

0

0

0

PAT

41

28

6

4

5

10

38

% Chg

69.5

(32.1)

(76.6)

(37.6)

30.4

93.5

276.8

PAT %

5.9

3.2

1.0

0.7

0.9

1.5

4.6

Basic EPS

4.4

2.8

0.7

0.4

0.5

1.0

3.9

Diluted EPS

4.4

2.8

0.7

0.4

0.5

1.0

3.9

% Chg

69.5

(32.1)

(76.6)

(37.6)

30.4

93.5

276.8

March 18, 2015

18

Initiating coverage | Action Construction Equipment

Balance Sheet

Y/E March (` cr)

FY11

FY12

FY13

FY14

FY15E FY16E FY17E

Sources of Funds

Equity Capital

19

20

20

20

20

20

20

Reserves Total

249

278

284

288

292

300

335

Networth

267

298

303

308

312

319

355

Total Debt

72

141

149

141

121

107

104

Other Long-term Liabilities

3

3

4

4

5

5

5

Deferred Tax Liability

1

3

5

5

5

5

5

Total Liabilities

343

445

461

458

443

436

469

Application of Funds

Gross Block

174

260

297

333

338

358

379

Accumulated Depreciation

22

33

46

65

75

88

102

Net Block

152

227

251

268

263

270

277

Capital WIP

3

5

10

2

0

0

0

Investments

8

10

16

15

19

7

1

Current Assets

Inventories

121

136

143

161

148

161

200

Sundry Debtors

83

86

83

68

65

69

84

Cash and Bank Balance

24

20

17

14

13

4

3

Loans, Advances & Deposits

46

41

29

29

32

36

46

Current Liabilities

153

147

160

163

164

178

209

Net Current Assets

121

135

112

108

93

92

124

Other Assets

58

67

72

65

68

68

68

Total Assets

343

445

461

458

443

436

469

March 18, 2015

19

Initiating coverage | Action Construction Equipment

Cash Flow Statement

Y/E March (` cr)

FY11

FY12

FY13

FY14

FY15E

FY16E FY17E

Profit before tax

54

38

11

5

7

13

50

Depreciation

7

11

14

15

10

13

14

Change in Working Capital

(52)

(25)

12

7

11

(10)

(34)

Interest & Financial Charges

4

7

10

10

12

10

8

Direct taxes paid

(12)

(15)

(5)

(1)

(2)

(3)

(11)

Cash Flow from Operations

(0)

16

42

37

38

23

26

(Inc)/ Dec in Fixed Assets

(30)

(73)

(42)

(25)

(6)

(20)

(22)

(Inc)/ Dec in Inv. & Int. reced.

(2)

(0)

(3)

5

0

15

8

Cash Flow from Investing

(32)

(73)

(45)

(20)

(6)

(5)

(13)

Issue/ (Buy Back) of Equity

21

0

0

0

0

0

0

Inc./ (Dec.) in Loans

41

72

11

(7)

(20)

(14)

(3)

Dividend Paid (Incl. Tax)

(21)

(11)

(2)

(2)

(2)

(3)

(3)

Interest Expenses

(4)

(7)

(10)

(10)

(12)

(10)

(8)

Cash Flow from Financing

37

54

(2)

(19)

(34)

(26)

(14)

Inc./(Dec.) in Cash

5

(3)

(4)

(2)

(2)

(8)

(1)

Opening Cash balances

19

24

21

17

15

13

4

Closing Cash balances

24

21

17

15

13

4

3

Key Ratios

Y/E March

FY11

FY12

FY13

FY14

FY15E

FY16E

FY17E

Valuation Ratio (x)

P/E (on FDEPS)

9.6

15.1

64.7

103.7

79.5

41.1

10.9

P/CEPS

8.2

10.7

20.8

21.6

27.6

18.0

7.9

Dividend yield (%)

5.5

0.6

0.6

0.3

0.4

0.6

0.6

EV/Sales

0.6

0.6

0.8

0.9

0.9

0.8

0.6

EV/EBITDA

7.3

10.2

18.4

22.0

28.7

16.6

7.5

EV / Total Assets

1.3

1.2

1.2

1.2

1.1

1.2

1.1

Per Share Data (`)

EPS (Basic)

4.4

2.8

0.7

0.4

0.5

1.0

3.9

EPS (fully diluted)

4.4

2.8

0.7

0.4

0.5

1.0

3.9

Cash EPS

5.1

3.9

2.0

1.9

1.5

2.3

5.3

DPS

2.3

0.2

0.2

0.1

0.2

0.3

0.3

Book Value

29

30

31

31

32

32

36

Returns (%)

RoCE (Pre-tax)

21.4

11.5

4.7

3.4

4.2

5.3

13.1

Angel RoIC (Pre-tax)

17.1

10.2

4.6

3.5

4.3

5.3

12.6

RoE

18.5

9.8

2.1

1.3

1.7

3.2

11.3

Turnover ratios (x)

Asset Turnover (Gross Block) (x)

5.3

3.9

2.4

1.9

1.8

1.9

2.3

Inventory / Sales (days)

47

55

76

90

95

85

79

Receivables (days)

35

36

46

45

41

37

33

Payables (days)

49

42

50

66

71

66

61

WC days

33

49

73

69

65

56

51

Leverage Ratios (x)

D/E ratio (x)

0.3

0.5

0.5

0.5

0.4

0.3

0.3

Interest Coverage Ratio (x)

16.4

6.1

2.0

1.5

1.6

2.4

7.0

March 18, 2015

20

Initiating coverage | Action Construction Equipment

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and MCX Stock Exchange Limited. It is also registered as a Depository Participant with CDSL and

Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel has received in-principal approval

from SEBI for registering as a Research Entity in terms of SEBI (Research Analyst) Regulations, 2014. Angel or its associates has not

been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its associates

including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in the company covered by

Analyst. Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of securities of

the company covered by Analyst during the past twelve months. Angel/analyst has not served as an officer, director or employee of

company covered by Analyst and has not been engaged in market making activity of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also,

please refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt.

Limited and its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Action Construction Equipment

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15

March 18, 2015

21