3QFY2018 Result Update | IT

January 16, 2018

Infosys

NEUTRALMULATE

CMP

`1,080

Performance highlights

Target Price

-

(` cr)

3QFY18

2QFY18

% chg (qoq)

3QFY17

% chg (yoy)

Investment Period

12 Months

Net revenue

17,794

17,567

1.3

17,273

3.0

EBITDA

4,817

4,702

2.4

4,767

1.0

EBITDA margin (%)

27.1

26.8

30bps

27.6

(53)bps

Stock Info

Adj. PAT

3,697

3,727

(0.8)

3,708

(0.3)

Sector

IT

Source: Company, Angel Research

Market Cap (` cr)

235,954

For 3QFY2018, on sales front Infosys posted 1.0% sequential growth in USD

Net Debt (` cr)

(32,666)

revenues to US$2,755mn in line with expectations. In Constant Currency terms

Beta

0.7

(CC), the company posted a 0.8% qoq growth. Volume growth during the quarter

52 Week High / Low

1,092/862

was 1.6% qoq. EBIT margin came in at 24.3% v/s. 24.2% expected, mainly driven

Avg. Daily Volume

352,628

by improved utilization levels (which came in at 84.9% v/s. 84.7% in 2QFY2018).

Face Value (`)

5

Consequently, PAT came in at `3,697cr v/s. `3,587cr expected, a dip of 0.8% qoq.

BSE Sensex

34,844

FY2018 revenue guidance has been kept at 5.5-6.5% in Constant Currency.

Nifty

10,742

Operating margin guidance unchanged at 23-25%. We maintain Neutral rating.

Reuters Code

INFY.BO

Bloomberg Code

INFY@IN

Quarterly highlights: On sales front, the company posted 1.0% sequential

growth in USD revenues to US$2,755mn in line with the expectations. In Constant

Currency terms (CC), the company posted a 0.8% qoq growth. Volume growth

Shareholding Pattern (%)

during the quarter was 1.6% qoq. In terms of geography, North America posted

Promoters

12.9

0.7% CC growth, Europe 4.7% qoq CC, India 5.9% qoq CC and ROW posted 4.0%

MF / Banks / Indian Fls

21.8

qoq CC growth. In terms of Industry, FSI posted 0.1% qoq CC growth, MFG

FII / NRIs / OCBs

52.2

declined 0.1% qoq CC, RCL 1.2% qoq CC and ECS posted 2.5% qoq CC growth.

Indian Public / Others

13.1

EBIT margin came in at 24.3% v/s. 24.2% expected, mainly driven by improved

utilization levels (which came in at 84.9% v/s. 84.7% in 2QFY2018). Consequently,

PAT came in at `3,697cr v/s. `3,587cr expected, a dip of 0.8% qoq.

Abs.(%)

3m 1yr

3yr

Sensex

6.8

27.7

24.1

Outlook and valuation: For FY2018, Infosys has maintained its revenue growth

Infosys

15.0

13.0

1.2

guidance to 5.5-6.6% v/s. 6.5-8.5% earlier in CC terms, while EBIT is expected to

be around 23-25%. We maintain our Neutral rating on the stock.

Key financials (Consolidated, IFRS)

3-year price chart

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

1,400

Net sales

62,441

68,484

70,665

76,318

% chg

17.1

9.7

3.2

8.0

1,200

Adj. net profit

13,491

14,353

14,479

15,460

1,000

% chg

9.4

6.4

0.9

6.8

800

EBITDA margin (%)

27.4

27.2

26.5

26.5

EPS (`)

59.0

62.5

63.1

67.3

600

P/E (x)

18.3

17.3

17.1

16.0

400

P/BV (x)

4.0

3.6

3.3

3.1

RoE (%)

21.8

20.8

19.3

19.1

RoCE (%)

20.7

20.3

19.6

19.8

Source: Company, Angel Research

EV/Sales (x)

3.4

3.1

2.9

2.6

EV/EBITDA (x)

12.5

11.5

10.9

9.8

Sarabjit kour Nangra

Source: Company, Angel Research; Note: CMP as of January 15, 2018

+91 22-39357800 Ext: 6806

Please refer to important disclosures at the end of this report

1

Infosys | 3QFY2018 Result Update

Exhibit 1: 3QFY2018 performance (IFRS, consolidated)

(` cr)

3QFY18

2QFY18

% chg (qoq)

3QFY17

% chg (yoy) 9MFY18 9MFY17

% chg (yoy)

Net revenue

17,794

17,567

1.3

17,273

3.0

52,439

51,365

2.1

Cost of revenue

10,952

10,771

1.7

10,407

5.2

32,172

31,230

3.0

Gross profit

6,842

6,796

0.7

6,866

(0.3)

20,267

20,135

0.7

SG&A expenses

2,025

2,094

(3.3)

2,099

(3.5)

6,187

6,192

(0.1)

EBITDA

4,817

4,702

2.4

4,767

1.0

14,080

13,943

1.0

Depreciation

498

456

9.2

433

15.0

1,404

1,253

12.1

EBIT

4,319

4,246

1.7

4,334

(0.3)

12,676

12,690

(0.1)

Other income

962

883

8.9

820

17.3

2,659

2,333

14.0

PBT

5,281

5,129

3.0

5,154

2.5

15,335

15,023

2.1

Income tax

152

1,403

(89.2)

1,446

(89.5)

2,925

4,268

(31.5)

Exceptional item

-

-

-

71

(5)

Reported PAT

5,129

3,727

37.6

3,708

38.3

12,339

10,749

14.8

Adjusted PAT

3,697

3,727

(0.8)

3,708

(0.3)

10,907

10,749

1.5

EPS

16.2

16.3

(0.8)

16.2

(0.3)

47.7

47.0

1.5

Gross margin (%)

38.5

38.7

(24)bps

39.7

(130)bps

38.6

39.2

(55)bps

EBITDA margin (%)

27.1

26.8

30bps

27.6

(53)bps

26.9

27.1

(29)bp

EBIT margin (%)

24.3

24.2

10bps

25.1

(82)bps

24.2

24.7

(53)bp

PAT margin (%)

20.8

21.2

(44)bps

21.5

(69)bps

20.8

20.9

(13)bp

Source: Company, Angel Research

Exhibit 2: 3QFY2018 - Actual Vs Angel estimates

(` cr)

Actual

Estimate

% Var.

Net revenue

17,794

17,770

0.1

EBITDA margin (%)

27.1

26.7

37bps

PAT

3,697

3,587

3.1

Source: Company, Angel Research

Revenues just in-line with expectation

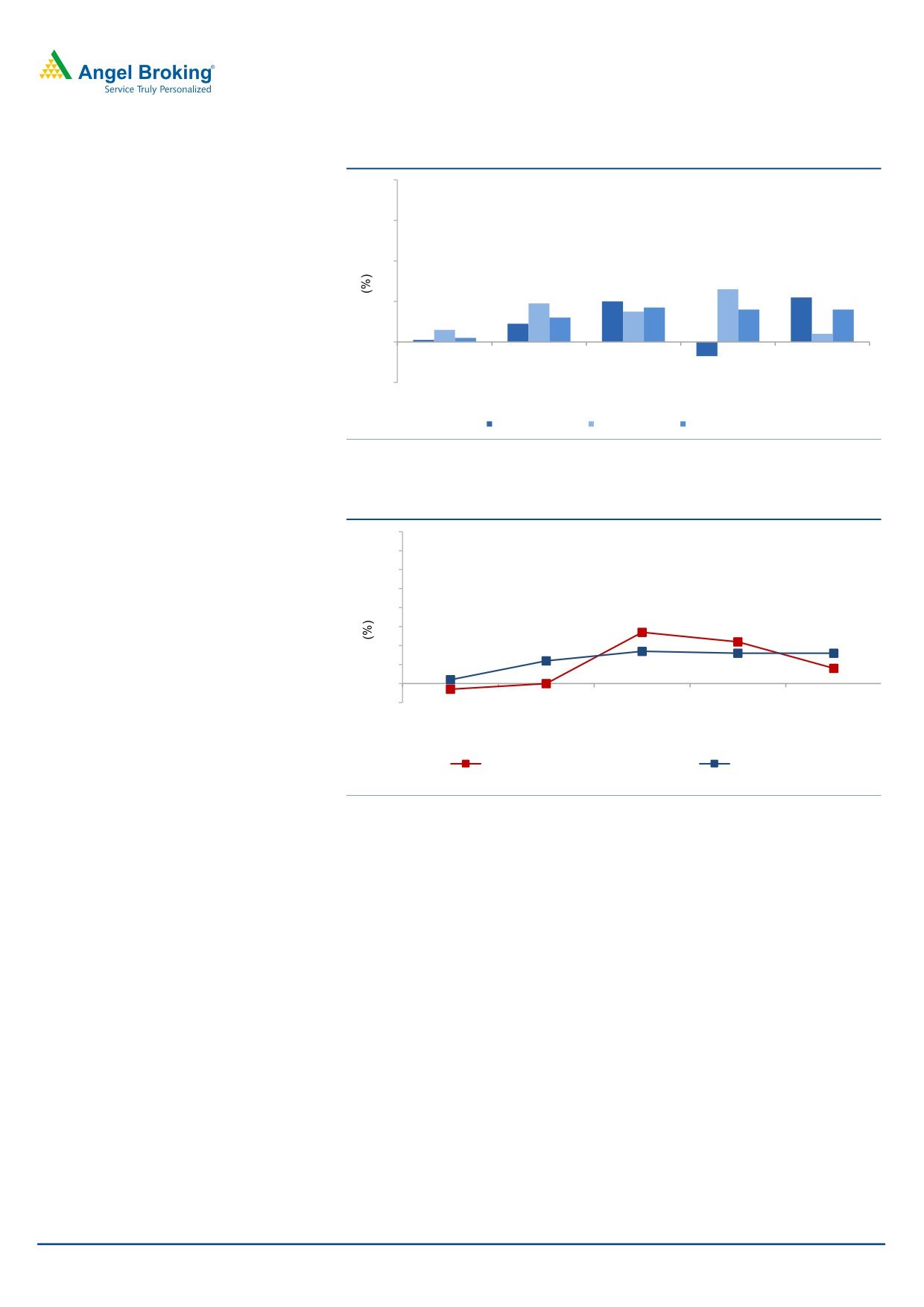

On sales front, the company posted 1.0% sequential growth in USD revenues to

US$2,755mn in line with the expectations. In Constant Currency terms (CC), the

company posted a 0.8% qoq growth. Volume growth during the quarter was 1.6%

qoq.

In terms of geography, North America posted 0.7% CC growth, Europe 4.7% qoq

CC India 5.9% qoq CC and ROW posted 4.0% qoq CC growth.

In terms of Industry, FSI posted 0.1% qoq CC growth, MFG declined 0.1% qoq CC,

RCL 1.2% qoq CC and ECS posted 2.5% qoq CC growth.

January 16, 2018

2

Infosys | 3QFY2018 Result Update

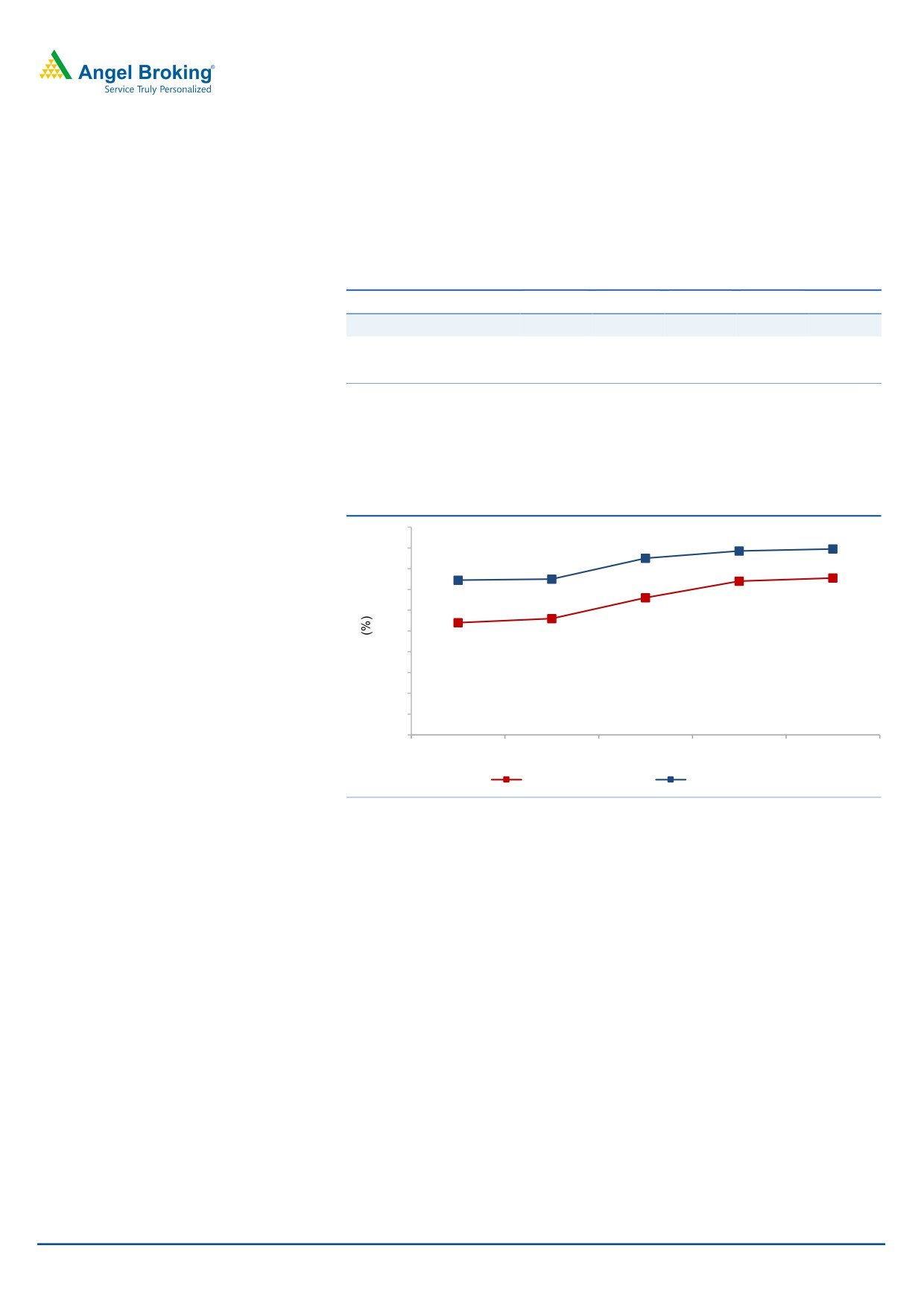

Exhibit 3: Trend in volume growth qoq (Effort wise)

8

6

4

2.6

1.9

2.2

2.0

1.5

1.7

1.6

1.6

2

1.2

0.6

0.9

0.4

0.1

0.2

0

(0.7)

(2)

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

Offshore

Onsite

Total volume growth

Source: Company, Angel Research

Exhibit 4: Trend in volume and USD revenue growth (qoq)

8

7

6

2.7

5

4

3

1.6

1.6

2

2.2

1

0.0

1.2

0

1.7

0.8

(1)

0.2

(0.3)

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

Revenue growth (constant currency)

Volume growth

Source: Company, Angel Research

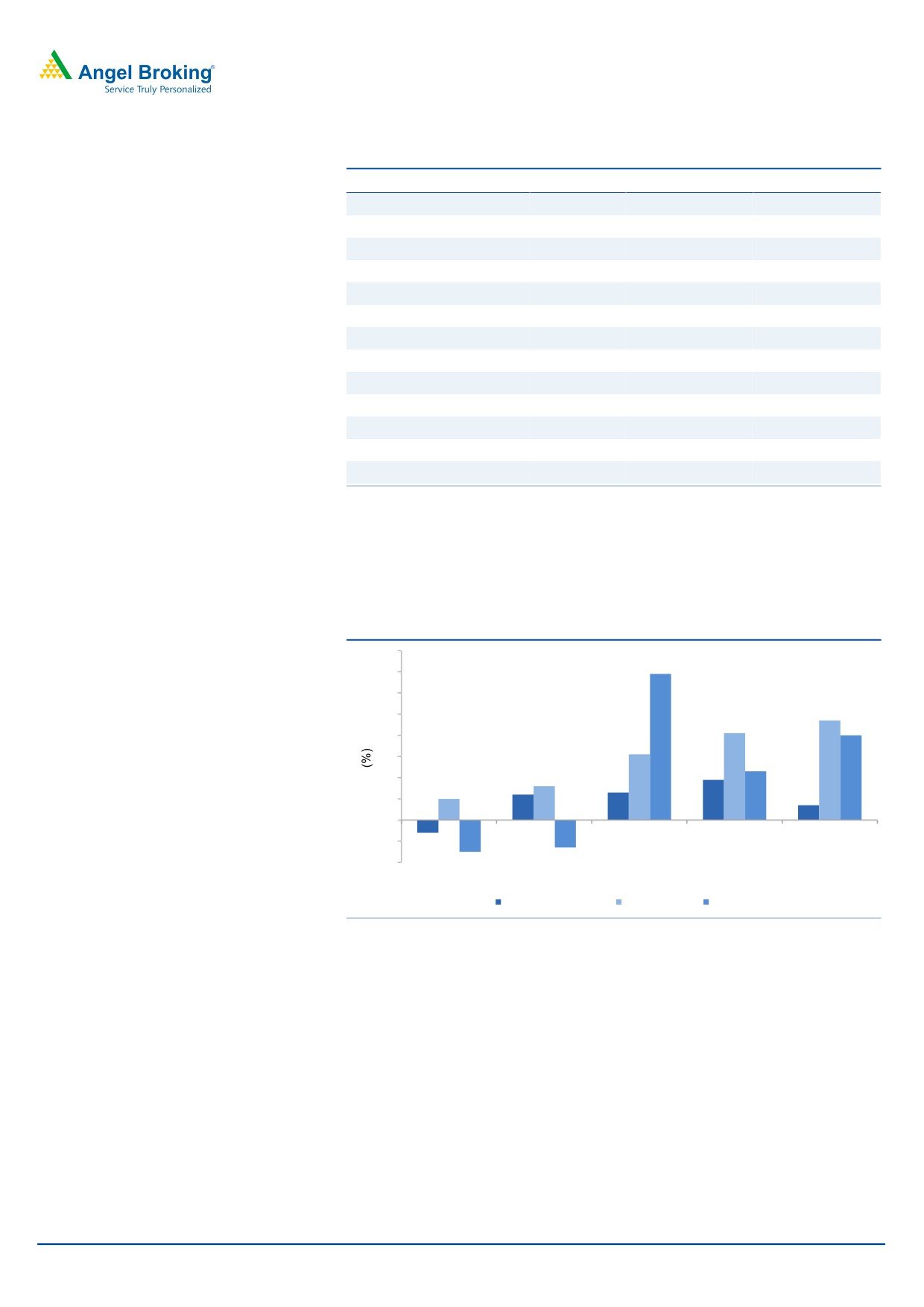

Industry wise, revenues from FSI, the company’s anchor vertical contributing 33.1%

to revenues, grew by 0.1% qoq in CC terms and 0.3% qoq. The Manufacturing

industry vertical, which contributed 21.8% to revenues, grew by 0.1% qoq. In CC

terms, the revenue from this vertical posted a qoq de-growth of 0.1%.

The Retail, CPG and Logistics segment (or RCL that contributed 22.7% to revenues)

reported a 1.4% qoq growth. In CC terms, the revenues from RCL grew by 1.2%

qoq. The Energy Utilities and Communications & Services segment contributed

22.4% to revenue, reporting a growth of 2.6% qoq in revenue and 2.5% qoq on CC

basis.

January 16, 2018

3

Infosys | 3QFY2018 Result Update

Exhibit 5: Growth trend in industry segments (Reported basis)

Particulars

% to revenue

% growth QoQ

% growth YoY

FSI

33.1

0.1

7.3

Banking and financial services

26.3

(1.6)

4.4

Insurance

6.8

7.3

20.4

Manufacturing

21.8

0.1

4.6

RCL

22.7

1.4

4.3

Retail and CPG

14.1

3.2

4.3

Transport and logistics

2.1

6.0

13.4

Life Sciences

4.6

(3.2)

8.0

Healthcare

1.9

(4.1)

(10.8)

ECS

22.4

2.8

16.9

Energy and utilities

5.8

6.5

25.3

Communication and services

10.5

2.0

24.6

Others

6.1

1.0

(0.2)

Source: Company, Angel Research

In terms of geographies, revenue from North America grew by 0.7% qoq in CC

terms, while other geographies such as Europe and RoW grew by 4.7% and 4.0%

qoq respectively (both in CC terms). India posted 5.9% qoq de-growth in CC terms.

Exhibit 6: USD growth trend in geographies qoq (CC basis)

8

6.9

7

6

4.7

5

4.1

4

4

3.1

3

2.3

1.9

2

1.2

1.6

1.3

1

1

0.7

0

(1)

(0.6)

(2)

(1.5)

(1.3)

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

North America

Europe

Rest of the world

Source: Company, Angel Research

January 16, 2018

4

Infosys | 3QFY2018 Result Update

Hiring and utilization

Infosys added 12,622 gross employees in 3QFY2018. The net addition for the

quarter stood at 3,251. Attrition (for consolidated entity) moved down in 3QFY2018;

it came at 18.7% (LTM) v/s. 21.4% in 2QFY2018.

Exhibit 7: Employee metrics

3QFY17 4QFY17 1QFY18 2QFY18 3QFY18

Gross addition

9,120

9,130

8,645

10,514

12,622

Net addition

(66)

601

(1,811)

(113)

3,251

Attrition - LTM basis (%)*

18.4

17.1

21.0

21.4

18.7

Source: Company, Angel Research, Note-* including subsidiaries

The utilization rate including trainees grew by 30bps qoq to 82.1% (81.8% in

2QFY2018); excluding trainees, it grew by 20bps qoq to 84.9%.

Exhibit 8: Trend in utilization (Services and Consulting + Projects)

87

84.7

84.9

84

85

81.9

82

83

81

81.8

82.1

79

80.2

77

77.8

78.2

75

73

71

69

67

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

Including trainees

Excluding trainees

Source: Company, Angel Research

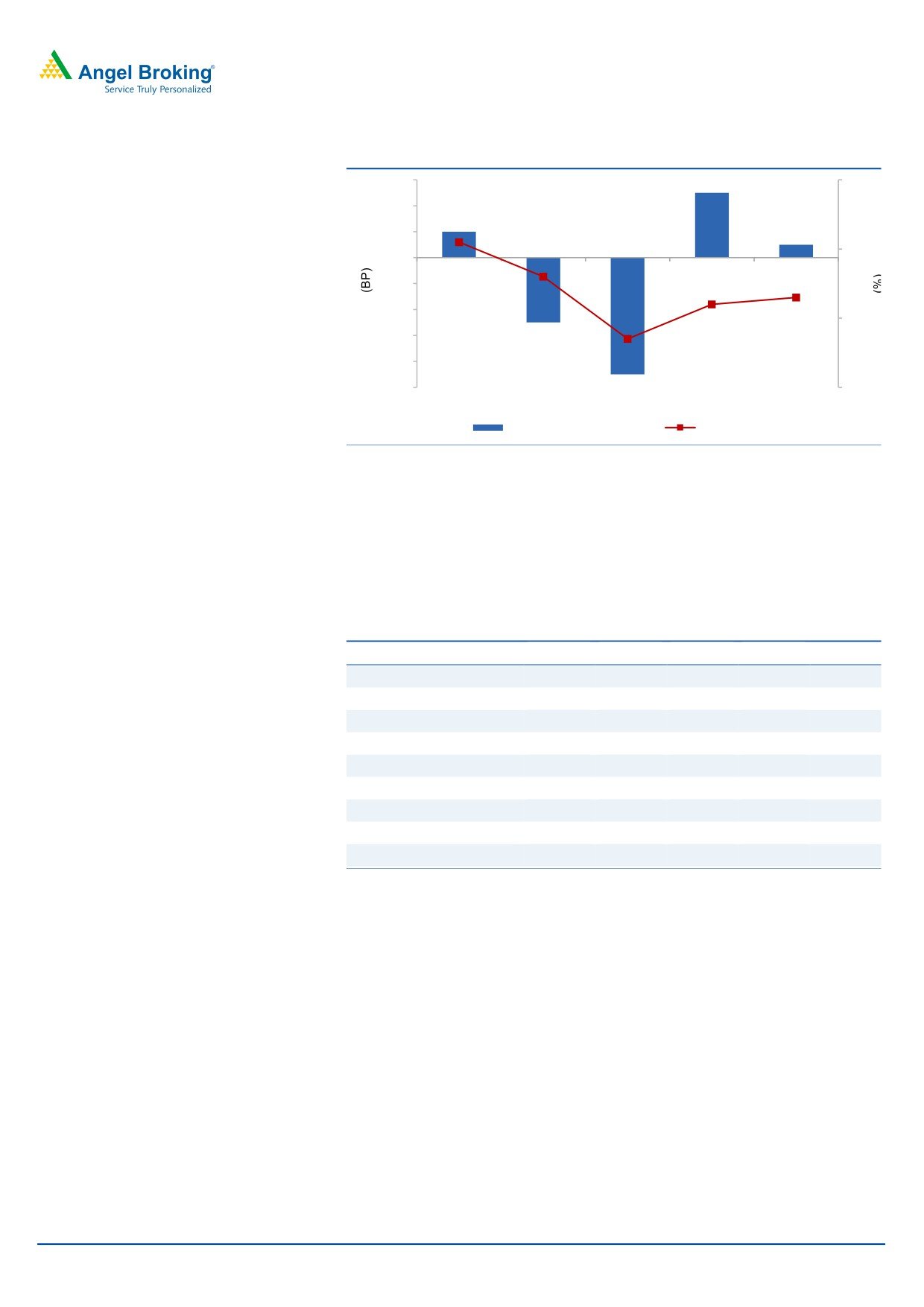

Margins expand

On operating front, the EBITDA margins came in at 24.3% V/s 24.2% expected with

an uptick of 10bps qoq, on back of good volume growth and consequently better

employee (excluding trainees) utilization rate of 84.9% V/s 84.7% in 2QFY2018.

January 16, 2018

5

Infosys | 3QFY2018 Result Update

Exhibit 9: Trend in EBIT margin

60

26

40

50

25.1

20

20

25

0

10

24.6

(20)

(50)

24.3

(40)

23.7

24.2

24

(60)

(90)

(80)

(100)

23

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

Margin movement (qoq)

EBIT margin (%)

Source: Company, Angel Research

Client pyramid

Infosys added 79 new clients (gross additions) during the quarter, taking its

total active client base to 1,191. The client addition was across the board. The

company added 2 client in the US100+mn & 9 clients in the US$20+mn.

Exhibit 10: Client metrics

Particulars

3QFY17 4QFY17 1QFY18 2QFY18 3QFY18

Top client (% of revenue)

3.1

3.3

3.3

3.4

3.4

Gross Client addition

77

71

59

72

79

Active client

1152

1162

1164

1173

1191

US$1mn-5mn

316

316

327

334

340

US$5mn-10mn

80

93

89

100

92

US$10mn-20mn

97

98

93

86

97

US$20mn-50mn

36

35

41

45

45

US$50mn-100mn

22

25

25

24

22

US$100mn+

14

13

18

12

14

Source: Company, Angel Research

Investment arguments

Revenue guidance maintained for FY2018: The Management has given the

revenue growth guidance for FY2018, which is moderate. The company has

maintained its guidance of 6.5-8.5% CC growth earlier. The company faced multiple

challenges in FY2017, amongst which execution issues in Consulting and the loss

of the RBS contract were the major ones, resulting in a loss of revenue growth

momentum. For FY2017, the company posted 8.3% growth in CC terms V/s a

guidance of 8.4-8.8% growth (in CC terms). Currently, we have factored a growth

for FY2018 (INR and USD growth of 2.7% and 6.0% respectively). Over FY2017-19E,

we expect USD and INR revenue to grow at a CAGR of 7.0% and 5.3% respectively.

Operating margin likely to be range bound in near term: For FY2018, the

company has reiterated its guidance for EBIT margins of 23-25%, mainly factoring

January 16, 2018

6

Infosys | 3QFY2018 Result Update

in currency impact and investment in onsite facility. For FY2017, the EBIT margins

came in at 24.7%, which was against the guidance of 24-26%. Over FY2017-19E, we

expect an EBIT CAGR of 4.3%, with FY2018E and FY2019E EBIT margins expected to

come in at 24.1% respectively. The moderation in margin expected to be for the

near term, as the company plans to move towards automation, in order to

safeguard its EBIT margin pressures.

Outlook and valuation

The company has marinated its USD revenue growth guidance for FY2018 to

5.5-6.5% on CC basis. We expect the company to post ~6.5% USD revenue growth

in FY2018. The company has changed its capital allocation policy from paying out

50% of PAT to 70% of Free Cash Flow. The stock currently trades at a valuation of

16.0x its FY2019E earnings. We recommend a Neutral on the stock.

Exhibit 11: Key assumptions

Parameters

FY2018E

FY2019E

Revenue growth - USD terms (%)

6.5

8.0

USD-INR rate

65.0

65.0

Revenue growth - INR terms (%)

3.2

8.0

EBITDA margin (%)

26.5

26.5

Tax rate (%)

28.0

28.0

EPS growth (%)

0.9

6.8

Source: Company, Angel Research

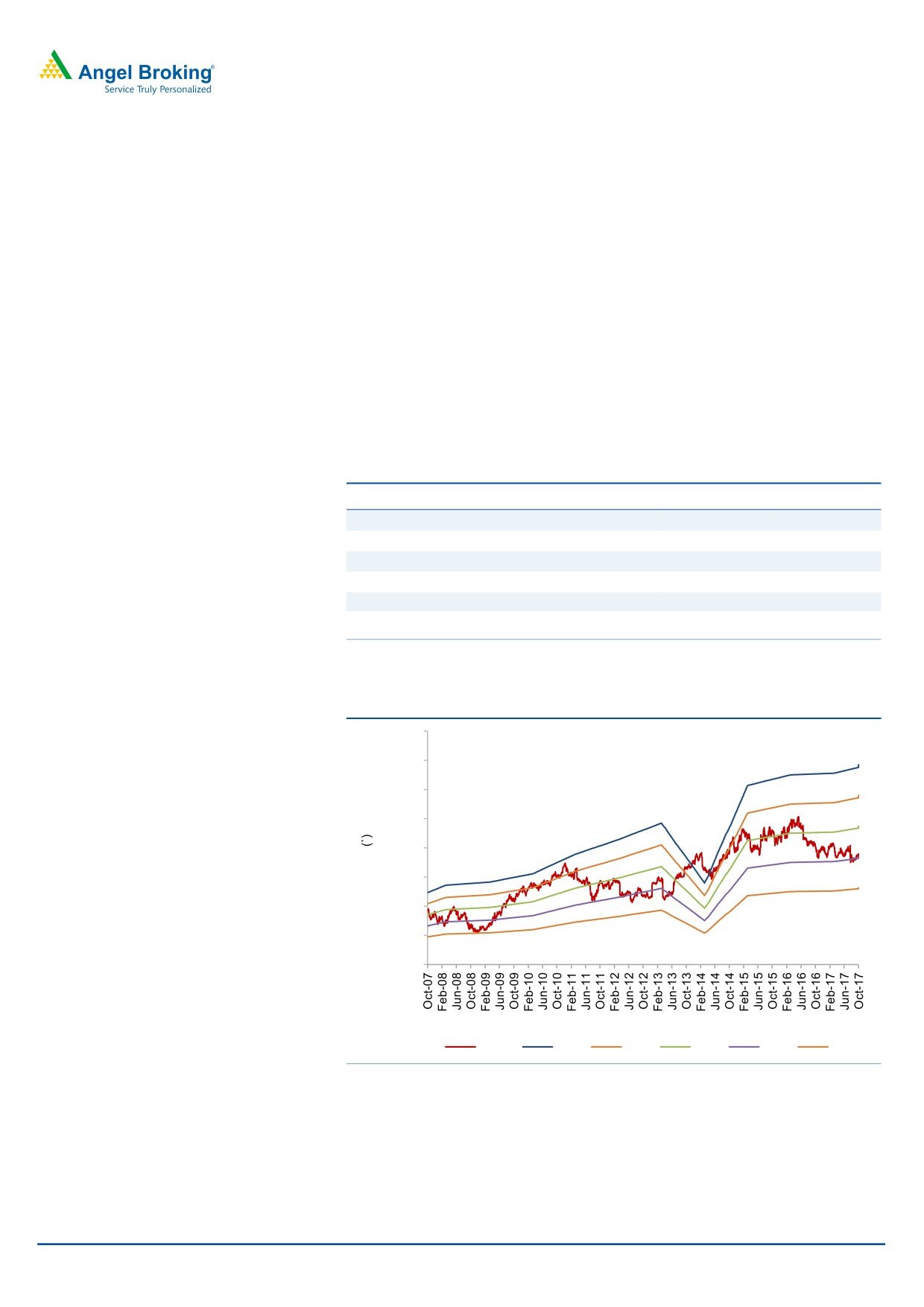

Exhibit 12: One-year forward PE (x)

2000.0

1750.0

1500.0

1250.0

1000.0

750.0

500.0

250.0

0.0

Price

26x

22x

18x

14x

10x

Source: Company, Angel Research

January 16, 2018

7

Infosys | 3QFY2018 Result Update

Exhibit 13: Recommendation summary

Company

Reco

CMP Tgt. price

Upside

FY2019E FY2019E

FY2017-19E

FY2019E

FY2019E

(`)

(`)

(%) EBITDA (%)

P/E (x)

EPS CAGR (%) EV/Sales (x)

RoE (%)

HCL Tech

Accumulate

907

1,014

11.8

22.1

13.4

6.2

1.9

20.6

Infosys

Neutral

1,080

-

-

26.5

16.0

3.8

2.6

18.7

TCS

Reduce

2,747

2,493

(9.3)

26.3

18.7

3.4

3.5

28.3

Tech Mahindra

Neutral

544

-

-

15.0

14.5

8.6

1.3

16.2

Wipro

Reduce

316

280

(11.5)

22.3

16.2

4.4

1.8

13.6

Source: Company, Angel Research

Company Background

Infosys is the second largest IT company in India, employing over

2,00,364

professionals (as of FY2017). The company services more than 1,000 clients across

various verticals, such as financial services, manufacturing, telecom, retail and

healthcare. Infosys has the widest portfolio of service offerings amongst Indian IT

companies, spanning across the entire IT service value chain - from traditional

Application Development and Maintenance to Consulting and Package

Implementation to Products and Platforms.

January 16, 2018

8

Infosys | 3QFY2018 Result Update

Profit and loss statement (IFRS, consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

FY2018E FY2019E

Net sales

50,133

53,319

62,441

68,484

70,665

76,318

Cost of revenue

30,767

31,817

37,595

41,550

35,686

38,541

Gross profit

19,366

21,502

24,846

26,934

27,206

29,382

% of net sales

38.6

40.3

39.8

39.3

38.5

38.5

Selling and mktg exp.

2,625

2,941

3,431

3,591

3,887

4,197

% of net sales

5.2

5.5

5.5

5.2

5.5

5.5

General and admin exp.

3,107

3,663

4,292

4,739

4,593

4,961

% of net sales

6.2

6.9

6.9

6.9

6.5

6.5

EBITDA

13,634

14,898

17,123

18,604

18,726

20,224

% of net sales

27.2

27.9

27.4

27.2

26.5

26.5

Dep and amortization

1,374

1,066

1,503

1,703

1,696

1,832

% of net sales

2.7

2.0

2.4

2.5

2.4

2.4

EBIT

12,260

13,832

15,620

16,901

17,030

18,393

% of net sales

24.5

25.9

25.0

24.7

24.1

24.1

Other income

2,669

3,427

3,122

3,080

3,080

3,080

Profit before tax

14,929

17,259

18,742

19,981

20,110

21,473

Provision for tax

4,062

4,929

5,251

5,598

5,631

6,012

% of PBT

27.2

28.6

28.0

28.0

28.0

28.0

PAT

10,648

12,330

13,491

14,383

14,479

15,460

Exceptional item

219

-

-

(30)

-

-

Adj. PAT

10,867

12,330

13,491

14,353

14,479

15,460

EPS (`)

47.3

53.7

59.0

62.5

63.1

67.3

January 16, 2018

9

Infosys | 3QFY2018 Result Update

Balance sheet (IFRS, consolidated)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017

FY2018E FY2019E

Current assets

Cash and cash equivalents

25,950

30,367

32,697

22,625.0

33,054.0

37,750.0

Available for sale fin. assets

2,197

874

75

9,970

9,970

9,970

Invest. in certificates of deposit

859

93

103

71

71

71

Trade receivables

8,351

9,713

11,330

12,322

11,872

12,821

Unbilled revenue

2,811

2,845

3,029

3,648

3,648

3,648

Derivative financial instrum.

215

101

116

284

284

284

Prepayments and other CA

2,636

3,296

4,448

4,856

4,099

4,426

Total current assets

43,019

47,289

51,798

53,776

62,997

68,971

Non-current assets

Property, plant and equipm.

7,887

9,125

10,530

11,716

11,916

12,116

Goodwill

2,157

3,091

3,764

3,652

2,157

2,158

Intangible assets

342

638

985

776

342

343

Available for sale fin. Assets

1,252

1,345

1,811

6,382

1,252

1,253

Deferred income tax assets

656

537

536

540

656

657

Income tax assets

1,522

4,089

5,230

5,716

5,716

5,716

Other non-current assets

220

238

735

797

1,793

1,794

Total non-current assets

14,036

19,063

23,591

29,579

23,832

24,037

Total assets

57,055

66,352

75,389

83,355

86,829

93,008

Current liabilities

Trade payables

173

140

386

367

173

174

Derivative financial instrum.

-

3

5

2

-

1

Current income tax liabilities

2,187

2,818

3,410

3,885

3,787

3,788

Client deposits

40

27

28

32

40

41

Unearned revenue

660

1,052

1,332

1,777

660

661

Employee benefit obligations

954

1,069

1,341

1,359

954

955

Provisions

379

478

512

405

379

380

Other liabilties

4,745

5,796

6,225

6,186

5,545

5,546

Total current liabilities

9,138

11,383

13,239

14,013

11,538

11,546

Non-current liabilities

Deferred income tax liabilties

64

160

256

207

64

65

Employee benefit obligations

323

46

115

153

323

324

Other liabilities

-

-

-

-

-

-

Total non-current liabilities

387

206

371

360

387

388

Total liabilities

9,525

11,589

13,610

14,373

11,925

11,934

Equity

Share capital

286

572

1,144

1,144

1,144

1,144

Share premium

3,090

3,090

2,241

2,356

2,356

2,356

Retained earnings

43,584

50,531

57,655

65,056

70,833

77,002

Other components of equity

570

570

739

426

571

572

Total equity

47,530

54,763

61,779

68,982

74,904

81,074

Total liabilties and equity

57,055

66,352

75,389

83,355

86,829

93,008

January 16, 2018

10

Infosys | 3QFY2018 Result Update

Cash flow statement (IFRS, consolidated)

Y/E March (` cr)

FY2014 FY2015 FY2016 FY2017 FY2018E FY2019E

Pre tax profit from operations

12,260

13,832

15,620

16,901

17,030

18,393

Depreciation

1,374

1,066

1,503

1,703

1,696

1,832

Pre tax cash from operations

13,634

14,898

17,123

18,604

18,726

20,224

Other income/prior period ad

2,669

3,427

3,122

3,080

3,080

3,080

Net cash from operations

16,303

18,325

20,245

21,684

21,806

23,304

Tax

4,062

4,929

5,251

5,598

5,631

6,012

Cash profits

12,241

13,396

14,994

16,086

16,175

17,292

(Inc)/dec in current assets

(2,271)

(1,942)

(2,968)

(2,187)

1,208

(1,278)

Inc/(dec) in current liabilties

2,852

2,245

1,856

774

(2,475)

8

(Inc)/dec in net trade WC

581

303

(1,112)

(1,413)

(1,267)

(1,270)

12,822

13,699

13,882

14,673

14,908

16,022

Cashflow from operating actv.

(Inc)/dec in fixed assets

(2,793)

(2,304)

(2,908)

(2,889)

(1,896)

(2,032)

(Inc)/dec in investments

(1,317)

2,089

789

(9,863)

-

-

(inc)/dec in sale of financial assets

(858)

(93)

(466)

(4,571)

5,130

(1)

(Inc)/dec in deferred tax assets

(583)

(2,448)

(1,140)

(490)

(116)

(1)

119

(181)

165

(11)

27

1

Inc/(dec) in other non current liab.

(Inc)/dec in other non current ass.

(138)

(1,248)

(1,517)

259

933

(3)

Cashflow from investing actv.

(5,570)

(4,185)

(5,077)

(17,565)

4,078

(2,036)

Inc/(dec) in debt

-

-

-

-

-

-

Inc/(dec) in equity/premium

1,099

450

889

515

(404)

(1,242)

4,233

5,547

7,364

7,695

8,153

8,049

Dividends

Cashflow from financing actv.

(3,134)

(5,097)

(6,475)

(7,180)

(8,557)

(9,291)

Cash generated/(utilised)

4,118

4,417

2,330

(10,072)

10,429

4,696

Cash at start of the year

21,832

25,950

30,367

32,697

22,625

33,054

Cash at end of the year

25,950

30,367

32,697

22,625

33,054

37,750

January 16, 2018

11

Infosys | 3QFY2018 Result Update

Key ratios

Y/E March

FY2014 FY2015 FY2016 FY2017 FY2018E FY2019E

Valuation ratio (x)

P/E

22.8

20.1

18.3

17.3

17.1

16.0

P/CEPS

20.3

18.5

16.5

15.4

15.3

14.3

P/BVPS

5.2

4.5

4.0

3.6

3.3

3.1

Dividend yield (%)

1.5

1.7

2.3

2.3

2.9

3.1

EV/Sales

4.3

4.0

3.4

3.1

2.9

2.6

EV/EBITDA

16.0

14.5

12.5

11.5

10.9

9.8

EV/Total assets

3.8

3.2

2.8

2.6

2.3

2.1

Per share data (`)

EPS

47

54

59

63

63

67

53

58

65

70

70

75

Cash EPS

Dividend

16

19

25

25

32

34

Book value

207

239

269

300

326

353

Dupont analysis

Tax retention ratio (PAT/PBT)

0.7

0.7

0.7

0.7

0.7

0.7

1.2

1.2

1.2

1.2

1.2

1.2

Cost of debt (PBT/EBIT)

EBIT margin (EBIT/Sales)

0.2

0.3

0.3

0.2

0.2

0.2

Asset turnover ratio (Sales/Assets)

0.9

0.8

0.8

0.8

0.8

0.8

Leverage ratio (Assets/equity)

1.2

1.2

1.2

1.2

1.2

1.1

Operating ROE

22.4

22.5

21.8

20.9

19.3

19.1

Return ratios (%)

RoCE (pre-tax)

21.5

20.8

20.7

20.3

19.6

19.8

Angel RoIC

43.7

39.5

36.7

33.3

38.9

40.7

RoE

22.9

22.5

21.8

20.8

19.3

19.1

Turnover ratios(x)

6.4

5.8

5.9

5.8

5.9

6.3

Asset turnover (fixed assets)

Receivables days

81

86

84

85

80

79

January 16, 2018

12

Infosys | 3QFY2018 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits

and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Infosys

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

January 16, 2018

13